Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

TikTok may be the fastest-growing social network in the history of the internet, but it is also quickly becoming the fastest-growing security threat and thorn in the side of U.S. China hawks.

The latest, according to a notice published by the U.S. Navy this past week and reported on by Reuters and the South China Morning Post, is that TikTok will no longer be allowed to be installed on service members’ devices, or they may face expulsion from the military service’s intranet.

It’s just the latest example of the challenges facing the extremely popular app. Recently, Congress led by Missouri senator Josh Hawley demanded a national security review of TikTok and its Sequoia-backed parent company ByteDance, along with other tech companies that may share data with foreign governments like China. Concerns over the leaking of confidential communications recently led the U.S. government to demand the unwinding of the acquisition of gay social network app Grindr from its Chinese owner Beijing Kunlun.

The intensity of criticism on both sides of the Pacific has made it increasingly challenging to manage tech companies across the divide. As I recently discussed here on TechCrunch, Shutterstock has actively made it harder and harder to find photos deemed controversial by the Chinese government on its stock photography platform, a play to avoid losing a critical source of revenue.

We saw similar challenges with Google and its Project Dragonfly China-focused search engine as well as with the NBA.

What’s interesting here though is that companies on both sides are struggling with policy on both sides. Chinese companies like ByteDance are increasingly being targeted and stricken out of the U.S. market, while American companies have long struggled to get a foothold in the Middle Kingdom. That might be a more equal playing field than it has been in the past, but it is certainly a less free market than it could be.

While the trade fight between China and the U.S. continues, the damage will continue to fall on companies that fail to draw within the lines set by policymakers in both countries. Whether any tech company can bridge that divide in the future unfortunately remains to be seen.

Powered by WPeMatico

Every year, the tech industry experiences moments that serve as guideposts for future entrepreneurs and investors looking to profit from the wisdom of the past.

In 2017, Susan Fowler published her heroic blog post criticizing Uber for its culture of sexual harassment, helping spark the #MeToo movement within the tech industry; 2018 was the year of the scooter, in which venture capitalists raced to pour buckets of cash into startups like Bird, Lime and Spin, hoping consumer adoption of micro-mobility would make the rushed deals worth it.

These last twelve months have been replete with scandals, new and interesting upstarts, fallen CEOs and big fundraises. Theranos founder Elizabeth Holmes finally got a court date, SoftBank’s Masayoshi Son admitted defeat (see: “In the case of WeWork, I made a mistake”), venture capitalist Bill Gurley advocated for direct listings and denounced big banks’ underwriting skills, sperm storage startups battled for funding and Away’s dirty laundry was aired in an investigation conducted by The Verge.

The list of top moments and over-arching trends that defined this year is long. Below, I’ve noted what I think best represent the largest conversations that occurred in Silicon Valley this year, with a particular focus on venture capital, followed by honorable mentions. As always, you can email me (kate.clark@techcrunch.com) if you have thoughts, opposing opinions, strong feelings or relevant anecdotes.

SoftBank Group Corp. chairman and CEO Masayoshi Son speaks during a press conference on November 6, 2019 in Tokyo, Japan. (Photo by Alessandro Di Ciommo/NurPhoto via Getty Images)

1. SoftBank admitted failure: We’ll get to WeWork in a moment, but first, let’s talk about its multi-billion-dollar backer. SoftBank announced its Vision Fund in 2016, holding its first major close a year later. Ultimately, the Japanese telecom giant raised roughly $100 billion to invest in technology startups across the globe, upending the venture capital model entirely with its ability to write $500 million checks at the flip of a switch. It was an ambitious plan and many were skeptical; as it turns out, that model doesn’t work too well. Not only has WeWork struggled despite billions in funding from SoftBank, several other of the firm’s bets have wavered under pressure. Most recently, SoftBank confirmed it was selling its stake in Wag, the dog-walking business back to the company, nearly two years after funneling a whopping $300 million in the then-three-year-old startup. Wag failed to accumulate value and was struck by scandal, leading to SoftBank’s exit. Why it matters: ditching one of its more high profile bets out of the monstrous Vision Fund wasn’t even the first time this year SoftBank admitted defeat. Once an unstoppable giant, SoftBank has been forced to return to reality after years of prolific dealmaking. No longer a leader in VC or even a threat to other top venture capitalists, SoftBank’s deal activity has become a cautionary tale. Here’s more on SoftBank’s other uncertain bets.

2. WeWork pulled its IPO. The biggest story of 2019 was WeWork. Another SoftBank portfolio, in fact the former star of its portfolio, WeWork filed to go public in 2019 and gave everyone full access to its financials in its IPO prospectus. In August, the business disclosed revenue of about $1.5 billion in the six months ending June 30 on losses of $905 million. The IPO was poised to become the second-largest offering of the year behind only Uber, but what happened instead was much different: WeWork scrapped its IPO after ousting its founding CEO Adam Neumann, whose eccentric personality, expensive habits, alleged drug use, desire to become Israel’s prime minister and other aspirations led to his well-publicized ouster. There’s a lot more to this story, click here for more coverage of the 2019 WeWork saga. Why it matters: WeWork’s unforgiving IPO prospectus painted a picture of a high-spending company with no path to profit in sight. For years, Silicon Valley (or New York, where WeWork is headquartered) has allowed high-growth companies to raise larger and larger rounds of venture capital, understanding that eventually their revenues would outgrow their expenses and they would achieve profitability. WeWork, however, and its fellow ‘unicorn,’ Uber, made it all the way to IPO without carving out a strategy of reaching profitability. These IPOs ignited a wide-reaching debate in the tech industry: does Wall Street care about profitability? Should startups prioritize profits? Many said yes. Meanwhile, the threat of a downturn had startups across industries cutting back and putting cash aside for a rainy day. For the first time in years, and as The New York Times put it, Silicon Valley began trying out a new mantra: make a profit.

3. A whole bunch of CEOs stepped down: Adam Neumann wasn’t the only high profile CEO to move on from their company this year. In a move tied to The Verge’s investigation, Away co-founder and CEO Steph Korey stepped down from the luggage company, instead becoming its executive chairman. Lime’s CEO Toby Sun stepped down, shifting to another role within the company. On the public end of the ecosystem, McDonald’s, REI, Rite Aid and many others replaced their leaders. According to CNBC, nearly 150 CEOs left their post in November alone, setting up 2019 to break records for CEO departures with nearly 1,500 recorded already. Why it matters: All of these departures were caused by varying factors. I will focus on WeWork and Away, which took center stage of the startups and venture capital universe. The recent Away debacle reinforces the role of the tech media and its ability to present well-reported facts to the public and enact significant change to business as a result. Similarly, much of Adam Neumann’s ouster came as a result of strong reporting from outlets like The Wall Street Journal, Bloomberg and more. From facilitating a toxic, cutthroat culture to paying millions in company dollars for an unnecessary private jet, Away and WeWork’s situations proved standards for startup CEOs has shifted. Whether that shift is here to stay is still up for debate.

Ah the list we’ve all been waiting for. pic.twitter.com/PndSjQf8yt

— Kate Clark (@KateClarkTweets) December 3, 2019

4. The IPO market was unforgiving to unicorns: WeWork never made it to the stock markets, but Uber, another scandal-ridden unicorn, did. The company (NYSE: UBER), previously valued at $72 billion, priced its stock at $45 apiece in May for a valuation of $82.4 billion. It began trading at $42 apiece, only to close even lower at $41.57, or down 7.6% from its IPO price. Not stellar, in fact, quite bad for one of the largest venture-backed companies of all time. Uber, however, wasn’t the only one to struggle with its IPO and first few months on the stock market. Other companies like Lyft and Peloton had disappointing results this year confirming the damage inflated valuations can cause startups-turned-public companies. Though a rocky IPO doesn’t mark the end of a company, it does tell you a lot about Wall Street’s appetite for Silicon Valley’s top companies. Why it matters: 2019’s tech IPOs illustrated a disconnect between the public markets and venture capitalists, whose cash determines the value of these high-flying companies. Wall Street has realized these stocks, which NYT journalist Erin Griffith recently described as “Publicly Listed Unicorns Miserably Performing,” are far less magical than previously assumed. As a result, many companies, particularly consumer tech businesses, may delay planned offerings, waiting until the markets stabilize and become hungry again for big-dreaming tech companies.

Powered by WPeMatico

Now that the final technology IPOs of 2019 have touched down, it’s a good time to start looking back at what happened during the year. We’re hunting for trends as the clock winds down. Here’s one that’s obvious: Hardware startups are still struggling.

It’s cliché to note in startupland that hardware is hard. Everyone knows it. Making hardware is difficult by itself, but as all tech hardware requires software, hardware shops wind up needing wider domain expertise than pure-software startups. And that’s hard.

But even if a nuts-and-bolts tech company hits scale, it seems difficult to keep that momentum up.

This year we saw Peloton, a hybrid hardware and digital services company, go public and struggle. Despite a recent public market resurgence, the company is slipping back toward its IPO price. Today its equity is trading down about 6% to around $30 per share. The company’s IPO price of $29 is uncomfortably close to its current value.

2019’s IPO crop also included EHang, a late entry to the market (more here on its debut) that quickly began to lose altitude after it started to float. EHang traded up today, but the firm is still worth less than its IPO valuation, a reduced figure that was dinged during the China-based drone company’s march toward the public markets.

So, Peloton is about flat and EHang is down. That’s not a great mix of results for a year’s IPO class of hardware companies. Looking back in time, things don’t get much better.

NIO, a China-based electric car company (despite making this thing of beauty), has deleted about two-thirds of its value since its late-2018 U.S.-listed IPO. After going public at $6.25, shares of NIO are worth just $2.70 today.

Sonos also went public in the United States in 2018. It traded above its IPO price of $15 at first. Then it fell under $10 per share as 2018 came to a close. The smart speaker and stereo company spent 2019 recovering. It’s now worth its IPO price again, closing trading today worth about $14.80 per share.

If you go back to 2017, however, Roku has kicked ass. After pricing at $14 per share, the TV hardware and digital services firm is trading for $137 per share, a nearly 10x gain. But Roku was moving away from hardware at the time of its IPO, making it a somewhat poor example. Hardware revenues for Roku were just 31% of revenue in its most recent quarter, for example. That figure was 42% in the year-ago quarter. It will continue to fall.

We don’t need to go over what happened to Fitbit and GoPro, I don’t think.

Hardware can make a lot of money. Samsung and Apple make oceans of money from their hardware. Microsoft has managed to make Surface into a real business, with billions of dollars in yearly revenue. Amazon has a big hardware business with both consumer reading gadgets and consumer surveillance devices. Even Google is taking its new phone seriously enough to buy out a chunk of the NBA’s ad slots (I think it’s this one), according to my extensive in-market testing. Facebook is the laggard of the group.

But for smaller hardware companies going public, unless I’m missing a number of recent of IPOs — and I don’t think that I am — it’s a tough world out there.

Powered by WPeMatico

F5 got an expensive holiday present today, snagging startup Shape Security for approximately $1 billion.

What the networking company gets with a shiny red ribbon is a security product that helps stop automated attacks like credential stuffing. In an article earlier this year, Shape CTO Shuman Ghosemajumder explained what the company does:

We’re an enterprise-focused company that protects the majority of large U.S. banks, the majority of the largest airlines, similar kinds of profiles with major retailers, hotel chains, government agencies and so on. We specifically protect them against automated fraud and abuse on their consumer-facing applications — their websites and their mobile apps.

F5 president and CEO François Locoh-Donou sees a way to protect his customers in a comprehensive way. “With Shape, we will deliver end-to-end application protection, which means revenue generating, brand-anchoring applications are protected from the point at which they are created through to the point where consumers interact with them—from code to customer,” Locoh-Donou said in a statement.

As for Shape, CEO Derek Smith said that it wasn’t a huge coincidence that F5 was the buyer, given his company was seeing F5 consistently in its customers. Now they can work together as a single platform.

Shape launched in 2011 and raised $183 million, according to Crunchbase data. Investors included Kleiner Perkins, Tomorrow Partners, Norwest Venture Partners, Baseline Ventures and C5 Capital. In its most recent round in September, the company raised $51 million on a valuation of $1 billion.

F5 has been in a spending mood this year. It also acquired NGINX in March for $670 million. NGINX is the commercial company behind the open-source web server of the same name. It’s worth noting that prior to that, F5 had not made an acquisition since 2014.

It was a big year in security M&A. Consider that in June, four security companies sold in one three-day period. That included Insight Partners buying Recorded Future for $780 million and FireEye buying Verodin for $250 million. Palo Alto Networks bought two companies in the period: Twistlock for $400 million and PureSec for between $60 and $70 million.

This deal is expected to close in mid-2020, and is of course, subject to standard regulatory approval. Upon closing Shape’s Smith will join the F5 management team and Shape employees will be folded into F5. The company will remain in its Santa Clara headquarters.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week Kate was in SF, Alex was in Providence and there was a mountain of news to shovel through. If you’re here because we mentioned linking to a certain story in the show notes, that’s here. For everyone else, let’s get into the agenda.

We kicked off with a look at three new venture funds. In order:

From there we turned to the gender imbalance in the world of venture capital. This year, companies founded by women raised only 2.8% of capital. These not-so-stellar statistics are always worth digging into.

We then took a quick look at two different venture rounds, including ProdPerfect’s $13 million Series A and Pepper’s smaller $5.6 million round. ProdPerfect’s round was led by Anthos Capital (known for investing in Honey, which sold for $4 billion). The company has $2 million in ARR and is growing quickly. Pepper, formed by former Snap denizens, is working to help other startups lower their CAC costs in-channel. Smart.

And finally, Alex wanted to bring up his series on startups that reach the $100 million ARR threshold (Extra Crunch membership required). A first piece looking into the idea led to a few more submissions. There seem to be enough companies to name the grouping with something nice. Centurion? Centipede? Centaur? We’re working on it.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Do you remember as a kid going to the grocery store with your parents and being just totally overwhelmed by the bright, loud packaging of products on shelf after shelf, aisle after aisle?

I certainly do. Each product had a brand — you’d recognize the Kix by its bright red box and Tide by its loud orange bottle. Every package screamed its brand name at you.

Branded packaging as we know it hasn’t been around that long. While people have been packaging goods for millennia, trademarked printed boxes, tins and shrink-wrapped containers were only invented in the late 1800s — less than 150 years ago, beginning with Uneeda Biscuits around 1896.

When branded packaging was invented, and up until very recently, its purpose and value to nearly every industry made a ton of good sense. The average consumer would shop in a catalog, browsing ads and offerings, or in a store, perusing shelves of products. The more a product stood out and set itself apart, the more memorable it would be and the more likely it would be purchased. Good packaging made products easy to recommend and spread by sharing visually.

And then, the internet came along.

Our team recently launched our new studio product, Regular, a service directed at small businesses hitting their growth inflection point. As we began to design our own website and work on branding, we did a lot of research into branding trends for consumer packaged goods, and what we uncovered was surprising.

We found was that there is a surprising movement towards “unbranding” — specifically choosing not to create a strong association between a product and its maker. Instead of bright packaging, large logos and stamped products, many companies are now going the other direction by operating without logos and offering minimal (or no) packaging.

Pens from MUJI (Photo: Michael/Flickr)

One of the earliest companies to adopt this mindset was Japanese home goods store MUJI, whose name literally means “No Brand” (it doesn’t get more literal than that). Most of its products come unpackaged with just a small price tag, or in minimal packaging with a single informational label (e.g., “lotion,” “body soap”) to identify its contents.

But MUJI has been since the 1980s, so why are we talking about this now?

Powered by WPeMatico

A company building a very high-tech glove has just gotten its hands on some new money.

HaptX is building a sensor-packed glove for VR and robotics applications that simulates haptic and resistance feedback for enterprise users.

The Seattle startup has raised $12 million in new funding from Mason Avenue Investments, Taylor Frigon Capital Partners, Upheaval Investments, Votiv Capital, Keiretsu Forum, Keiretsu Capital, NetEase and Amit Kapur of Dawn Patrol Ventures. HaptX has now raised $19 million to date.

The company says this funding will go toward the company’s next generation of glove hardware.

I got a chance to demo the company’s glove last year and there are certainly some bizarre experiences that are enabled by the product, which uses an external pneumatic box to expand and contract air pockets inside a glove form factor to make it feel like the virtual object you’re holding onto in VR is actually in your hand.

Needless to say at this point, the virtual reality industry’s consumer ambitions haven’t quite panned out as expected. The enterprise space has found slightly more enduring success, though much of the enterprise use hasn’t expanded too far beyond “internal innovation hubs” and pilot programs. HaptX seems to have zeroed in on the same enterprise customer base as other VR startups, with a lot of its customers using the gloves in design and visualization processes. HaptX has moved away from marketing itself as a VR-only company and has expanded into robotics, reshaping its offering into a solution framed by real-world input and real-world output.

Alongside the funding announcement, HaptX is sharing that it has partnered with Advanced Input Systems to collaborate on “product development, manufacturing, and go-to-market.”

The company is focused on enterprise and unfortunately doesn’t seem to be building a mech suit for Jeff Bezos, although they sent me a great gif of him demoing the technology earlier this year at a conference.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today, we’re digging into a host of data concerning the East Coast venture capital scene, specifically looking into the performance of its two key startup markets.

It’s 12 degrees Fahrenheit as I write this in my office situated between Boston and New York City — a perfect vantage point for studying these vibrant tech ecosystems. Let’s see what the data tells us.

The information we’re examining today comes from White Star Capital (often via CBInsights), a venture capital firm that describes itself as “transatlantic” and takes part in seed, Series A and Series B rounds around the globe. The group last raised a $180 million fund that TechCrunch covered here, noting at the time that capital pool was “oversubscribed from an initial target of $140 million” and would be invested into “around 20 new companies from the new fund, writing opening cheques of between $1 million and $6 million.”

With boots on the ground in New York, White Star cares about the East Coast, so the fund’s put dossier on the region isn’t unexpected. What it includes, however, is.

We’ll start with NYC and its surprising 2019 before turning to Boston, digging into its super-giant venture totals and hearing from Founder Collective’s Eric Paley on the state of things in urban Massachusetts.

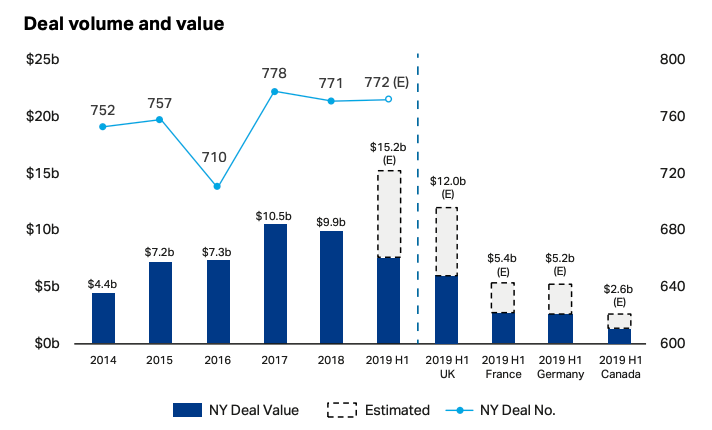

White Star’s report details record-breaking figures for NYC’s current year. Off of effectively flat deal volume (New York City sees around 775 venture deals per year at the moment, or a little more than two per day), the overgrown town should set record venture dollar volume in 2019.

Observe the following, astounding chart detailing the abnormality of 2019 from a comparative venture dollar perspective:

By smashing 2017’s local maximum, 2019 appears set to crush the city’s record — and rich — venture investment totals. The graphic also manages to point out (somewhat embarrassingly) that Gotham will manage to best a number of European countries’ aggregate venture dollar investments by itself this year.

That’s is a useful bit of context as in the United States, New York City is always Number Two to Silicon Valley. But, this chart argues, being number two in the number-one market is still a hell of a lot of capital.

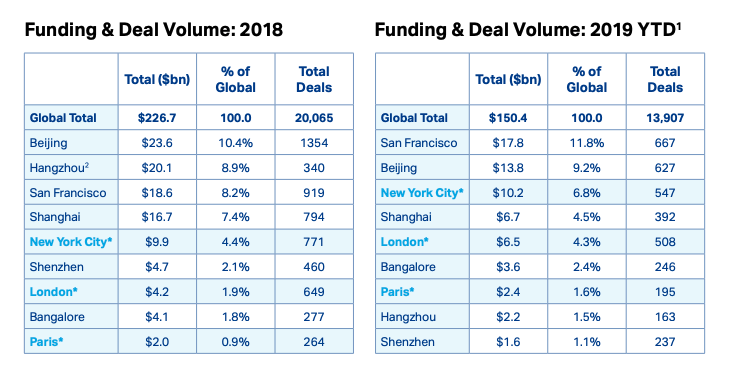

Putting New York City’s venture into even sharper comparative perspective, observe the following table:

Powered by WPeMatico

Scott Wolfe, chief executive officer of Levelset, the New Orleans-based money management and payment startup for contractors in the construction industry, always thought he’d be in the grocery business.

His family owned a number of grocery stores around New Orleans and he was readying himself to go into the family business when Hurricane Katrina hit.

As the family business faced significant losses in their stores, the construction and contracting service they’d built to develop the land the stores were on had a tremendous opportunity. Within the span of a year, Wolfe had pivoted the family’s operations to focus on renovations and restorations and launched fully into construction.

It was during that time that Wolfe saw the need for some sort of software service that could manage cash flow and payment for the tens to hundreds of small business contractors involved in getting a project done.

So he built Levelset to be that service.

Now the company has closed on $30 million in financing from Horizons Ventures, the investment firm backed by Li Ka-shing, who is one of the world’s wealthiest billionaire property developers.

When Bart Swanson, an advisor to Horizons, met Levelset through a mutual friend who did some investing around the New Orleans-based Tulane University ecosystem, he immediately felt it was an opportunity that the Horizons investment committee would understand.

“This is a global issue,” says Swanson. “Sixty-four percent of construction businesses fail in their first five years because they have nowhere to turn for help,” when it comes to ensuring payment.

For now, Levelset is focused on digitizing billing and payments and providing insights into who is actually on a job site and the responsibilities that those workers have on site, according to Wolfe.

“There’s a ton of investment that has gone into the field,” says Wolfe. “What has seen a lack of as prolific an investment are things behind the scenes outside of the field that happen in the office. This is the accountants and administrative workers who have to take the information that’s in the field and turn it into money.”

For developers like Cheung Kong Holdings, Li’s development business, the promise of Levelset’s software is a huge boon. The construction industry runs on small businesses that lack software and services to process payments quickly. The time it takes to deal with paperwork can delay a project and ultimately cost developers money.

Horizons was joined in the new round by S3 Ventures, Operating Venture Capital, Altos Ventures and Darren Bechtel of Brick & Mortar Ventures. As a result of the investment, Swanson will take a seat on the company’s board.

In a recent survey of contractors by Levelset and T-Sheets by Quickbooks, more than half of contractors stated they were not paid on time and had significant cash flow challenges, and more than 75% craved more transparency in the payment process. This is no surprise, given PWC’s working capital studies in the past decade demonstrating that construction industry payment speeds are the slowest of all (83+ days).

“The effort required to get paid, and the cash stress put on contractors is unbelievable,” said Wolfe, in a statement. “The world’s biggest industry is full of small and medium businesses who are the fabric of our economy. It’s crucial that they can do their work without worrying about cash.”

Powered by WPeMatico

Leapfin, a startup selling corporate finance tooling, announced a $4.5 million round this morning. The funding event was led by Bowery Capital, and included dollars from a number of former technology executives.

Before its newly announced investment, the company had raised just a small seed round. The small capital amounts may seem inconsequential, but they’re more strategic than anything. According to Leapfin CEO Raymond Lau, the company is running lean and keeping an eye on profitability.

After being founded in 2015 and starting commercialization of its product in 2018, the company is stepping a bit further out of the shadows this morning. Let’s talk about what it does, and why both its product and business philosophy are neat.

Leapfin helps companies track their revenue and cost of revenue expenses.

In more human terms, Leapfin helps companies track sales, and how much it costs to create and distribute its goods and services to customers. “Cost of revenue,” also known (roughly) as “cost of goods sold,” may sound like a jargony accounting term, but in reality it’s a bedrock business concept that anyone involved with startups needs to understand.

Let’s explain why. Once you deduct costs of revenue from revenue itself, you’re left with gross profit. That’s what businesses use to cover their operating costs. And, crucially, the larger a company’s gross profit is in relation to its revenue, the higher margin its revenue is; investors love high gross margin revenue.

In part, their high gross margins are why software startups are worth so much.

Back to Leapfin, its product is a shot at making business a more limpid process. In a call with TechCrunch, Leapfin’s Lau explained that many companies only have “one-in-thirty” visibility into their operations; that business owners only manage to fully collate their revenue and cost of revenue results monthly, meaning that the rest of the time they are flying at least partially blind.

The goal of Leapfin, according to Lau, is to provide a “single source of truth” for ongoing business results, using “robotic process automation” to help companies cut down on repetitive work. So Lepafin does two things: helps companies know where they stand financially, and saves them time on rote tasks that tend to come with accounting.

The company is pretty happy with its ability to sell its product so far. Lau told TechCrunch that it has found “very, very strong product market fit,” for example. Asked to describe when he felt that Leapfin had gelled with the market, Lau explained that in his view, product market fit is more “process” than a “tipping point,” but that he was confident in Leapfin’s product-market harmony when its customers began referring other companies (to a product that costs six-figures annually), and its sales cycle tightened.

Leapfin is run a bit differently from most SaaS companies that we cover. Instead of raising lots to invest in blow-out sales and marketing expenses, Leapfin is running pretty lean.

TechCrunch asked Lau why he only raised $4.5 million in the new round, which, given the product progress his company has made, felt modest. He said that the Leapfin staff “are outsiders in a way,” and that while his “peers are raising tens of millions,” his company could be profitable by the third quarter of next year. So Leapfin doesn’t need more money, and selling shares ahead of growth is an expensive way to raise capital.

Lau also said, however, that his company’s small raise “doesn’t mean that [it] won’t raise more down the road.” Another check in 2020 to ward off any downturn fears would make some sense. But Leapfin probably won’t sweat a crash too much, as the company keeps profitability and cash flow positivity “in sight,” according to its CEO.

Despite that, the company expects to hire quickly, expanding from around 20 people today to 50 by the end of next year. What we need next from Leapfin is an ARR number so we can vet just how much product market fit it really has.

Powered by WPeMatico