Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Venture capital investment exploded across a number of geographies in 2019 despite the constant threat of an economic downturn.

San Francisco, of course, remains the startup epicenter of the world, shutting out all other geographies when it comes to capital invested. Still, other regions continue to grow, raking in more capital this year than ever.

In Utah, a new hotbed for startups, companies like Weave, Divvy and MX Technology raised a collective $370 million from private market investors. In the Northeast, New York City experienced record-breaking deal volume with median deal sizes climbing steadily. Boston is closing out the decade with at least 10 deals larger than $100 million announced this year alone. And in the lovely Pacific Northwest, home to tech heavyweights Amazon and Microsoft, Seattle is experiencing an uptick in VC interest in what could be a sign the town is finally reaching its full potential.

Seattle startups raised a total of $3.5 billion in VC funding across roughly 375 deals this year, according to data collected by PitchBook. That’s up from $3 billion in 2018 across 346 deals and a meager $1.7 billion in 2017 across 348 deals. Much of Seattle’s recent growth can be attributed to a few fast-growing businesses.

Convoy, the digital freight network that connects truckers with shippers, closed a $400 million round last month bringing its valuation to $2.75 billion. The deal was remarkable for a number of reasons. Firstly, it was the largest venture round for a Seattle-based company in a decade, PitchBook claims. And it pushed Convoy to the top of the list of the most valuable companies in the city, surpassing OfferUp, which raised a sizable Series D in 2018 at a $1.4 billion valuation.

Convoy has managed to attract a slew of high-profile investors, including Amazon’s Jeff Bezos, Salesforce CEO Marc Benioff and even U2’s Bono and the Edge. Since it was founded in 2015, the business has raised a total of more than $668 million.

Remitly, another Seattle-headquartered business, has helped bolster Seattle’s startup ecosystem. The fintech company focused on international money transfer raised a $135 million Series E led by Generation Investment Management, and $85 million in debt from Barclays, Bridge Bank, Goldman Sachs and Silicon Valley Bank earlier this year. Owl Rock Capital, Princeville Global, Prudential Financial, Schroder & Co Bank AG and Top Tier Capital Partners, and previous investors DN Capital, Naspers’ PayU and Stripes Group also participated in the equity round, which valued Remitly at nearly $1 billion.

Up-and-coming startups, including co-working space provider The Riveter, real estate business Modus and same-day delivery service Dolly, have recently attracted investment too.

A number of other factors have contributed to Seattle’s long-awaited rise in venture activity. Top-performing companies like Stripe, Airbnb and Dropbox have established engineering offices in Seattle, as has Uber, Twitter, Facebook, Disney and many others. This, of course, has attracted copious engineers, a key ingredient to building a successful tech hub. Plus, the pipeline of engineers provided by the nearby University of Washington (shout-out to my alma mater) means there’s no shortage of brainiacs.

There’s long been plenty of smart people in Seattle, mostly working at Microsoft and Amazon, however. The issue has been a shortage of entrepreneurs, or those willing to exit a well-paying gig in favor of a risky venture. Fortunately for Seattle venture capitalists, new efforts have been made to entice corporate workers to the startup universe. Pioneer Square Labs, which I profiled earlier this year, is a prime example of this movement. On a mission to champion Seattle’s unique entrepreneurial DNA, Pioneer Square Labs cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest.

Boundless CEO Xiao Wang at TechCrunch Disrupt 2017

Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. Seattle is home to two of the most valuable businesses in the world, but it has not created as many founders as anticipated. PSL hopes that by removing some of the risk, it can encourage prospective founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon, to build.

“The studio model lends itself really well to people who are 99% there, thinking ‘damn, I want to start a company,’ ” PSL co-founder Ben Gilbert said in March. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Boundless is one of several successful PSL spin-outs. The business, which helps families navigate the convoluted green card process, raised a $7.8 million Series A led by Foundry Group earlier this year, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

Years-old institutional funds like Seattle’s Madrona Venture Group have done their part to bolster the Seattle startup community too. Madrona raised a $100 million Acceleration Fund earlier this year, and although it plans to look beyond its backyard for its newest deals, the firm continues to be one of the largest supporters of Pacific Northwest upstarts. Founded in 1995, Madrona’s portfolio includes Amazon, Mighty AI, UiPath, Branch and more.

Voyager Capital, another Seattle-based VC, also raised another $100 million this year to invest in the PNW. Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, closed on another $180 million to invest in early-stage consumer startups in May. And new efforts like Flying Fish Partners have been busy deploying capital to promising local companies.

There’s a lot more to say about all this. Like the growing role of deep-pocketed angel investors in Seattle have in expanding the startup ecosystem, or the non-local investors, like Silicon Valley’s best, who’ve funneled cash into Seattle’s talent. In short, Seattle deal activity is finally climbing thanks to top talent, new accelerator models and several refueled venture funds. Now we wait to see how the Seattle startup community leverages this growth period and what startups emerge on top.

Powered by WPeMatico

We love parties almost as much as we love startups, but we go absolutely bonkers for a hot startup/party mashup. That’s why we’re returning to host our 3rd Annual TechCrunch Winter Party in San Francisco on Friday, February 7. Even better news, party-goers — additional (the second batch) coveted tickets to this wild winter romp are available now. Better get your tickets while you can.

Last year’s inaugural event was a huge success, as nearly 1,000 of Silicon Valley’s brightest minds came to relax, connect and celebrate the entrepreneurial spirit of the startup community — and cast a keen eye over some promising startups.

This year’s soiree takes place at Galvanize and features tasty libations, delicious hors d’oeuvres and engaging conversation. That sounds so very civilized, right? Well, don’t dry clean your stuffed shirt just yet, because we’ll have plenty of party games and activities, giveaways and fun surprises. And, of course, plenty of photo ops, baby!

Galvanize may be a multi-level venue, but the space is still limited — as are the tickets. We’re rolling them out in batches over the next few weeks, so keep checking back if you can’t snag a ticket.

Here are the pertinent Winter Party details:

When: Friday, February 7, 6:00 p.m. – 9:00 p.m.

Where: Galvanize, 44 Tehama St., San Francisco, CA 94105

Ticket price: $85 (buy them here)

Here’s another great idea. Why just mingle and schmooze when you can mingle, schmooze and demo your early-stage startup in front of hundreds of the Valley’s top star-makers? Buy a demo table for $1,500 (the price also includes four attendee tickets). Demo tables are limited, so act now before other founders snatch ’em up.

Of course, no TechCrunch party is complete without plenty of awesome prizes, including TC swag and tickets to Disrupt San Francisco 2020. Come on out for a great midwinter’s night of relaxed connection, fun and opportunity. Get your tickets to the 3rd Annual TechCrunch Winter Party at Galvanize today.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

It’s the second to last day of 2019, meaning we’re very nearly out of time this year; our space for repretrospection is quickly coming to a close. Before we do run out of hours, however, I wanted to peek at some data that former Kleiner Perkins investor and Packagd founder Eric Feng recently compiled.

Feng dug into the changing ratio between enterprise-focused Seed deals and consumer-oriented Seed investments over the past decade or so, including 2019. The consumer-enterprise split, a loose divide that cleaves the startup world into two somewhat-neat buckets, has flipped. Feng’s data details a change in the majority, with startups selling to other companies raising more Seed deals than upstarts trying to build a customer base amongst folks like ourselves in 2019.

The change matters. As we continue to explore new unicorn creation (quick) and the pace of unicorn exits (comparatively slow), it’s also worth keeping an eye on the other end of the startup lifecycle. After all, what happens with Seed deals today will turn into changes to the unicorn market in years to come.

Let’s peek at a key chart from Feng, talk about Seed deal volume more generally, and close by positing a few reasons (only one of which is Snap’s IPO) as to why the market has changed as much as it has for the earliest stage of startup investing.

Feng’s piece, which you can read here, tracks the investment patterns of startup accelerator Y Combinator against its market. We care more about total deal volume, but I can’t recommend the dataset enough if you have the time.

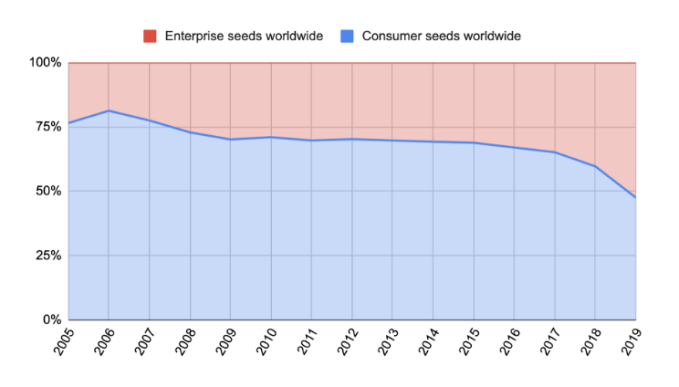

Concerning the universe of Seed deals, here’s Feng’s key chart:

Chart via Eric Feng / Medium

As you can see, the chart shows that in the pre-2008 era, Seed deals were amply skewed towards consumer-focused Seed investments. A new normal was found after the 2008 crisis, with just a smidge under 75% of Seed deals focused on selling to the masses for nearly a decade.

In 2016, however, a new trend emerged: a gradual decline in consumer Seed deals and a shift towards enterprise investments.

This became more pronounced in 2017, sharper in 2018, and by 2019 fewer than half of Seed deals focused on consumers. Now, more than half are targeting other companies as their future customer base. (Y Combinator, as Feng notes, got there first, making a majority of investments into enterprise startups since 2010, with just a few outlying classes.)

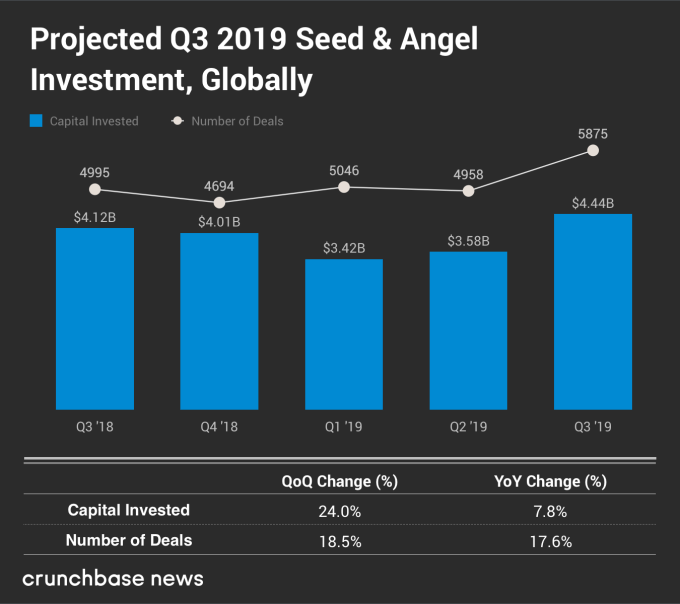

This flip comes as Seed deals sit at the 5,000-per-quarter mark. As Crunchbase News published as Q3 2019 ended, global Seed volume is strong:

So, we’re seeing a healthy number of deals as the consumer-enterprise ratio changes. This means that the change to more enterprise deals as a portion of all Seed investments isn’t predicated on their number holding steady while Seed deals dried up. Instead, enterprise deals are taking a rising share while volume appears healthy.

Now we get to the fun stuff; why is this happening?

As with many trends long in the making, there is no single reason why Seed investors have changed up their investing patterns. Instead, there are likely a myriad that added up to the eventual change. I’m going to ping a number of Seed investors this week to get some more input for us to chew on, but there are some obvious candidates that we can discuss today.

In no particular order, here are a few:

Powered by WPeMatico

Over the weekend, media and digital brand holding company IAC announced that it had agreed to buy Care.com, which describes itself as “the world’s largest online family care platform,” in a deal valued at about $500 million. Despite being the best-known marketplace in the United States for finding child and senior caregivers, Care.com has spent the past nine months dealing with the fallout from a Wall Street Journal investigative article that detailed potentially dangerous gaps in its vetting process. The company’s issues not only highlight the problems with scaling a marketplace created to find caregivers for the most vulnerable members of society, but also the United States’ childcare crisis.

Childcare in the United States is weighed down with many issues and arguably no one platform can fix it, no matter how large or well-known. Over the past year and a half, however, several startups dedicated to fixing specific challenges have raised funding, including Wonderschool, Kinside and Winnie.

IAC and Care.com’s announcement came at the end of a year when more media attention has been paid to the difficulties American parents face in finding and affording childcare, and how that contributes to gender disparities, falling birthrates and other social issues. The U.S. is the only industrialized nation in the world without mandated paid parental leave and childcare is one of the biggest expenses for families. Several Democratic presidential candidates, including Elizabeth Warren and Bernie Sanders, have made universal childcare part of their platform and business leaders like Alexis Ohanian are using their clout to advocate for better family leave policies.

But the issue has already created deep structural problems. From an economic perspective, a September 2018 study by ReadyNation and Council for a Strong America estimated that annually, the 11 million working parents in the United States lose a total of $37 billion in earnings because they lack adequate childcare. Businesses in turn lose a total of $13 billion a year as a result, while the impact on lower income and sales tax reduces tax revenues by $7 billion. Many parents change their career trajectories after they have children, even if they did not plan to. For example, a study published earlier this year in the Proceedings of the National Academy of Sciences found that 43% of women and 23% of men in STEM change fields, switch to part-time work or leave the workforce.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about the defining moments of VC in 2019. Before that, I noted some thoughts on U.S. VC activity in Europe.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you’re new, you can subscribe to Startups Weekly here.

Startups perish for many reasons but there’s one constant: this is an incredibly difficult business. Launching a successful company isn’t just a matter of drive and finding the right people (though both, clearly, are important). Doing well in this business requires the stars to align perfectly on a billion different things.

A cursory look at this year’s batch of companies doesn’t find any story quite as spectacular as last year’s big Theranos flameout, which gave us a best-selling book, documentary, podcast series and upcoming Adam McKay/Jennifer Lawrence film. Some, like MoviePass, however, may have come close.

And for every Theranos, there are dozens of stories of hardworking founders with promising products that simply couldn’t make it to the finish line. There’s also room for debate about what is and isn’t a startup. For our purposes, we’re focusing here on independent startups, not digital initiatives from larger companies — though in at least one case, the startup was acquired by a larger company before shutting down.

So without further ado, here are some of the biggest and most fascinating startups that closed up shop in 2019.

We have a holiday promotion going on right now with annual Extra Crunch membership. You can get an annual membership for only $79 (normally $150/year). This offer is available exclusively through this link, and the offer expires at the end of the month.

Powered by WPeMatico

The Daily Crunch is TechCrunch’s roundup of our biggest and most important stories. If you’d like to get this delivered to your inbox every day at around 9am Pacific, you can subscribe here.

1. Remembering the startups we lost in 2019

This year’s batch doesn’t include any story quite as spectacular as last year’s big Theranos flameout, which gave us a best-selling book, documentary, podcast series and upcoming Adam McKay/Jennifer Lawrence film. Some, like MoviePass, however, may have come close.

And for every Theranos, there are dozens of stories of hardworking founders with promising products that simply couldn’t make it to the finish line.

2. Huawei reportedly got by with a lot of help from the Chinese government

For those following Huawei’s substantial rise over the past several years, it’ll come as no surprise that the Chinese government played an important role in fostering the hardware maker. Even so, the actual numbers behind the ascent are still a bit jaw-dropping — at least according to a piece published by The Wall Street Journal.

3. Russia starts testing its own internal internet

Russia has begun testing a national internet system that would function as an alternative to the broader web, according to local news reports. Exactly what stage the country has reached is unclear, however.

4. Fintech’s next decade will look radically different

Nik Milanovic argues that in the next 10 years, fintech will become portable and ubiquitous, as it both moves into the background and creates a centralized place where our money is managed for us.

5. Wikimedia Foundation expresses deep concerns about India’s proposed intermediary liability rules

Wikimedia Foundation, the nonprofit group that operates Wikipedia, is urging the Indian government to rethink proposed changes to the nation’s intermediary liability rules. Under the proposal, the Indian Ministry of Electronics and IT requires “intermediary” apps — a category that includes any service with more than 5 million users — to set up a local office and have a senior executive in the nation who can be held responsible for any legal issues.

6. The FAA proposes remote ID technology for drones

According to the FAA, the “next exciting step in safe drone integration” aims to offer a kind of license plate analog to identify the approximately 1.5 million drones currently registered with the governmental body.

7. The year of the gig worker uprising

2019 was a momentous year for gig workers. While the likes of Uber, Lyft, Instacart and DoorDash rely on these workers for their respective core services, the pay does not match how much those workers are worth — which is a lot. It’s this issue that lies at the root of gig workers’ demands. (Extra Crunch membership required.)

Powered by WPeMatico

The nearly seven-year-old, New York-based fitness subscription app ClassPass is reportedly trying to raise $285 million in a new funding round that would push its valuation to more than $1 billion.

The company will issue 22.7 million Series E shares as part of the funding round, according to a securities filing obtained by Reuters from analytics firm Lagniappe Labs.

We’ve reached out to its press office for more information.

According to TC’s sources, ClassPass has been in fundraising mode since at least early fall.

The company began life as a way for people to book classes across different fitness studios but has more recently been pushing a corporate business that sees it adding ClassPass to employee benefit packages.

It is right now valued at $536.4 million, according to Reuters, which cites the Prime Unicorn Index. Its backers include the Singapore sovereign wealth fund Temasek and Alphabet, along with General Catalyst, Thrive Capital and Acequia Capital.

To date, the company has raised roughly $240 million from investors altogether, according to Crunchbase. It closed its most recent round of funding, an $85 million Series D round, in July 2018.

ClassPass was founded by Payal Kadakia, who is now the company’s executive chairman. She stepped aside in 2017 to make room for Fritz Lanman, the company’s former executive chairman and co-operator and now CEO.

Lanman acknowledged in an interview with Fortune earlier this year that ClassPass has endured some ups and downs in its time. Though it originally charged $99 per month for an unlimited number of fitness classes in New York, it was forced to raise prices before more recently instituting fluctuating class prices based on demand (and the availability of classes) of particular studios. The end result: Customers currently pay between $9 and $199 per month for credits that can be spent on classes.

As for its corporate memberships, it currently promises not just classes and a way to customize programs for employees but also streaming audio and video workouts. The last owes to an investment that ClassPass made in a broadcast studio, from which it built a library of on-demand video workouts. TC covered that development back in 2018.

Powered by WPeMatico

In September 2019, President Emmanuel Macron was about to wrap up a speech on late-stage investment in France. According to a press briefing and some discussions with a source, everything that he was supposed to announce had been announced.

But he dropped an unexpected number. “I’ll leave you with a goal: there should be 25 French unicorns by 2025,” Macron said. A unicorn is a private company with a valuation of $1 billion or more.

When you mention France in a conversation with foreigners, they don’t immediately think about startups. In December 2018, I covered a two-day roadshow of the French tech ecosystem with 40 partners of international venture capital firms, as well as limited partners, from Andreessen Horowitz to Greylock Partners, Khosla Ventures and more.

The same clichés came up again and again — taxes, labor law, long lunches… You name them. But it doesn’t matter if those clichés are true or not (hint: They aren’t), the French tech ecosystem has been thriving. And 2019 has been a remarkable year when it comes to reaching unicorn status and raising late-stage rounds of funding.

According to a recent report from VC firm Atomico, there are 11 unicorns in France. Some of them have been around for years, such as BlaBlaCar (a ride-sharing marketplace for long distance rides), OVHcloud (a cloud hosting company), Deezer (a music streaming service) and Veepee (an e-commerce company formerly known as Vente-privee.com).

But in 2019 alone, a handful of companies have reached unicorn status. Here are a few examples.

Powered by WPeMatico

December has been a strong month for Brazilian startups, bringing a big IPO and a new unicorn for local companies. Tech-driven investment firm XP Investimentos went public on the U.S. Stock Exchange in mid-December, raising $1.81 billion in the fourth-largest IPO of 2019. XP’s stock price jumped 30% on its first day of trading, from $27 per share to $34.50.

XP was founded in 2001 to provide brokerage training classes to Brazilians to help them invest in the international stock market. Today, it is a full-service brokerage firm, providing fund management and distribution to more than 1.5 million customers in Brazil.

Notably, XP has outlined a strategy for beating Brazilian banks, among the most profitable in the world, in its 354-page report to the SEC. Brazil’s banking market is highly concentrated, with the top five players dominating 93% of market share. This concentration has led to significant inefficiencies that XP tries to disrupt by offering a variety of financial products through an accessible online platform.

The heavy bureaucracy of these banks will prevent them from innovating quickly enough to compete with newer institutions like XP, whose debt products are attractive to frustrated Brazilian customers. The inefficiency of the Brazilian financial system has opened opportunities for companies like XP, or neobank Nubank, to rapidly attract customers who are disgruntled with the traditional system.

Brazil has seen a new unicorn emerge almost every month this year, and December was no exception. Gaming startup Wildlife raised a $60 million Series A round led by U.S.-investor Benchmark Capital at a $1.3 billion valuation to become the country’s eleventh unicorn. This round was big even for Silicon Valley standards, and it is uncommon for startups even in markets like the U.S. or Europe to hit a $1 billion-plus valuation in such an early round.

Wildlife has created more than 60 games since 2011, including Zooba and Tennis Clash, which have both reached global acclaim. Founded by brothers Victor and Arthur Lazarte, Wildlife operates on a freemium model that only charges users for in-app purchases. They plan to use the funding to double their employee base and grow to $2 billion in 2020, continuing the 80% yearly growth they have seen since 2011.

Konfio provides small business loans in Mexico through an online platform to help SMEs gain liquidity and grow their operations. These small businesses are often overlooked by banks in Mexico and Latin America, which do not know how to price risk for businesses that process less than $10 million per year.

Konfio recently raised $100 million from SoftBank’s Innovation Fund, the third investment that SoftBank has made into Mexico since launching the fund. The capital will go toward financing working capital loans, as well as creating new products for Konfio’s customers. Today, Konfio’s loans average around $12,000, while banks still struggle to loan less than $40,000. The tech-driven platform allows Konfio to disburse loans within 24 hours without requiring collateral.

Small business lending is a tremendous opportunity in Latin America, where banks are among the most profitable and the least competitive in the world. Brazil’s Creditas and Colombia’s OmniBnk are among the other startups providing innovative products that calculate risk more effectively than banks in Latin America’s complex lending environment.

The Albo team has raised $26.4 million to scale its leading neobank.

In an extension of a Series A round, Mexico’s albo raised a further $19 million from Valar Ventures to bring their newest round to $26.4 million in total. Albo previously raised $7.4 million from Mountain Nazca, Omidyar Network and Greyhound Capital in January 2019. Albo’s mission is to provide banking services to unbanked and underbanked clients in Mexico. More than half of albo’s customers claim that albo was their first-ever bank account.

Founded by Angel Sahagun in 2016, albo quickly became Mexico’s largest neobank, serving more than 200,000 customers and sending out thousands of new cards every day. The investment from Valar Ventures, founded by Peter Thiel (also an investor in N26 and TransferWise), is a vote of confidence for this Mexican fintech. Albo has also previously received investment from Arkfund, Magma Partners and Mexican angels.

Albo plans to use the capital to develop new products, including savings and credit services, in the coming year. Mexico will likely be a battleground for Latin American neobanks in 2020, as Klar, Nubank and potentially Argentina’s Uala will begin to grow in the region’s second-largest market. While there is room for several competitive neobanks to thrive in Mexico, this industry will be one to watch in 2020.

Goldman Sachs loaned $125 million to MercadoLibre to continue developing their credit product, MercadoCredito. MercadoLibre will use the capital to triple its $100 million debt facility for small business loans in Mexico. To date, MercadoCredito has loaned more than $610 million to 270,000 businesses around the region in Mexico, Brazil and Argentina.

Brazilian cloud-kitchen startup Mimic raised $9 million in a seed round led by Monashees to develop a more efficient food delivery model in Brazil. Mimic will exclusively manage the logistics of “dark kitchens,” which exist only for delivery and have no sit-down facilities, saving time and money for clients. Mimic will use the investment to grow its team.

An early-stage online lending startup in Brazil, Rebel, recently raised $10 million from Monashees and Fintech Collective to provide unsecured loans to middle-class Brazilians at affordable rates. Rebel has lowered rates to around 2.9% per month, compared to 40-400% at Brazil’s largest banks. The startup uses a proprietary algorithm to calculate risk for clients and provide loans rapidly through its online platform.

Colombia’s Rappi recently announced an expansion into Ecuador, where it has rapidly reached 100,000 users between Quito and Guayaquil, the country’s two largest cities. Rappi is now active in nine countries and more than 50 cities in Latin America.

Given the arrival of the SoftBank Innovation Fund, Latin American startup investment in 2019 will likely more than double the $2 billion invested in 2018. Here are a few of the highlights we saw this year:

Latin America’s startup and investment ecosystem has likely more than doubled this year as compared to 2019. As international investors like SoftBank, Andreessen Horowitz, Sequoia, Accel, Tencent and others are taking more bets on the region, more startups than ever have scaled and reached unicorn status. These startups will continue to scale in 2020, taking on a regional presence to provide services to Latin America’s 650 million population.

Powered by WPeMatico

It’s gotten to the point now where a handful of angel investors can put a space company on the map. But the same changes that have made the industry accessible have made it increasingly complex to track its trends. By default, all space startups are exciting, but companies vary widely in risk, capital intensity and maturity. Here’s what you need to know about the four main areas of the new space economy.

Perhaps simply the most exciting industry to be a part of today, orbital launch service has gone from a government-funded niche dominated by a handful of primes to a vibrant, growing community serving insatiable demand.

There’s a good reason why it was dominated for so long by the likes of ULA, whose Delta rockets took up a huge majority of missions for decades. The barrier to entry for launch is huge.

As such there are three ways to enter the sector: brute force, stealth, and novelty.

Brute force is how SpaceX and Blue Origin have managed to accomplish what they have. With billions in investment from people who don’t actually care whether money is made in the short term (or with Bezos, even in the long term), they can perform the research and engineering necessary to make a full-scale launch platform. Few of these can ever really exist, and participation is limited when they do. Fortunately we all reap the benefits when billionaires compete for space superiority.

Stealth, perhaps better described as smart positioning, is where you’ll find Rocket Lab. This New Zealand-based company didn’t appear out of nowhere — look at its timeline and you’ll see scaled-down tests being conducted more than a decade ago. But what founder Peter Beck and his crew did was anticipate the market and work doggedly towards a specific solution.

Rocket Lab is focused on small payloads, delivered with short turnaround time. This avoids the trouble of competing against billionaires and decades-old space dynasties because, really, this market didn’t exist until very recently.

“Responsive space, or launch on demand, is going to be increasingly important,” Beck said. “All satellites are vulnerable, be it from natural, accidental, or deliberate actions. As we see the growth and aging of small sat constellations, the need for replenishment will increase, leading to demand for single spacecraft to unique orbits. The ability to deploy new satellites to precise orbits in a matter of hours, not months or years, is critical to government and commercial satellite operators alike.”

Rocket Lab’s tenth launch, nicknamed “Running Out of Fingers.”

Investing in Rocket Lab early on would have seemed unexciting as for year after year they made measured progress but took on no cargo and made no money. Patience is the primary virtue here. But investors with foresight are looking back now on the company’s many successful launches and bright future and marveling that they ever doubted it.

The third category of launch is novelty: entirely new launch techniques like SpinLaunch or Leo Aerospace. The term may not inspire confidence, and that’s deliberate. Companies taking this approach are high-risk, high-reward propositions that often need serious funding before they can even prove the basic physical possibility of their launch technique. That’s not an investment everyone is comfortable making.

On the other hand, these are companies that, should they prove viable, may upend and collect a significant portion of the new and growing launch market. Here patience is not so much required as extra diligence and outside expertise to help separate the wheat from the chaff. Something like SpinLaunch may sound outlandish at first, but the Saturn V rocket still seems outlandish now, decades after it was built. Leaving the confines of established methods is how we move forward — but investors should be careful they don’t end up just blasting their cash into orbit.

Powered by WPeMatico