Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Extra Crunch community perks have a new offer from voice meeting notes service, Otter.ai. Starting today, annual and two-year Extra Crunch members can receive 25% off an annual plan for Otter Premium or Otter for Teams.

Otter.ai is an AI-powered assistant that generates rich notes from meetings, interviews, lectures and other voice conversations. You can record, review, search and edit the notes in real time, and organize the conversations from any device. We also use Otter.ai regularly here at TechCrunch to produce transcripts and voice notes from panels at our events, and it’s a great way to easily organize and search the conversations. Learn more about Otter.ai here.

To qualify for the Otter.ai community perk from Extra Crunch, you must be an annual or two-year Extra Crunch member. The 25% discount only applies to annual plans with Otter.ai, but it can be used for either the Premium or Teams plan. You can learn more about the pricing for Otter.ai here, and you can sign up for Extra Crunch here.

Extra Crunch is a membership program from TechCrunch that features how-tos and interviews on company building, intelligence on the most disruptive opportunities for startups, an experience on TechCrunch.com that’s free of banner ads, discounts on TechCrunch events and several community perks like the one mentioned in this article. Our goal is to democratize information about startups, and we’d love to have you join our community.

You can sign up for Extra Crunch here.

After signing up for an annual or two-year Extra Crunch membership, you’ll receive a welcome email with a link to sign up for Otter.ai and claim the discount. Otter.ai offers a free plan with capped minutes, and if you are interested in unlocking the full potential, you can purchase the annual plan with the 25% discount.

If you are already an annual or two-year Extra Crunch member, you will receive an email with the offer at some point over the next 24 hours. If you are currently a monthly Extra Crunch subscriber and want to upgrade to annual in order to claim this deal, head over to the “my account” section on TechCrunch.com and click the “upgrade” button.

This is one of several community perks we’ve launched for Extra Crunch annual members. Other community perks include a 20% discount on TechCrunch events, 100,000 Brex rewards points upon credit card sign up and an opportunity to claim $1,000 in AWS credits. For a full list of perks from partners, head here.

If there are other community perks you want to see us add, please let us know by emailing travis@techcrunch.com.

Sign up for an annual Extra Crunch membership today to claim this community perk. You can purchase an annual Extra Crunch membership here.

Disclaimer:

This offer is provided as a business partnership between TechCrunch and Otter.ai, but it is not an endorsement from the TechCrunch editorial team. TechCrunch’s business operations remain separate to ensure editorial integrity.

Powered by WPeMatico

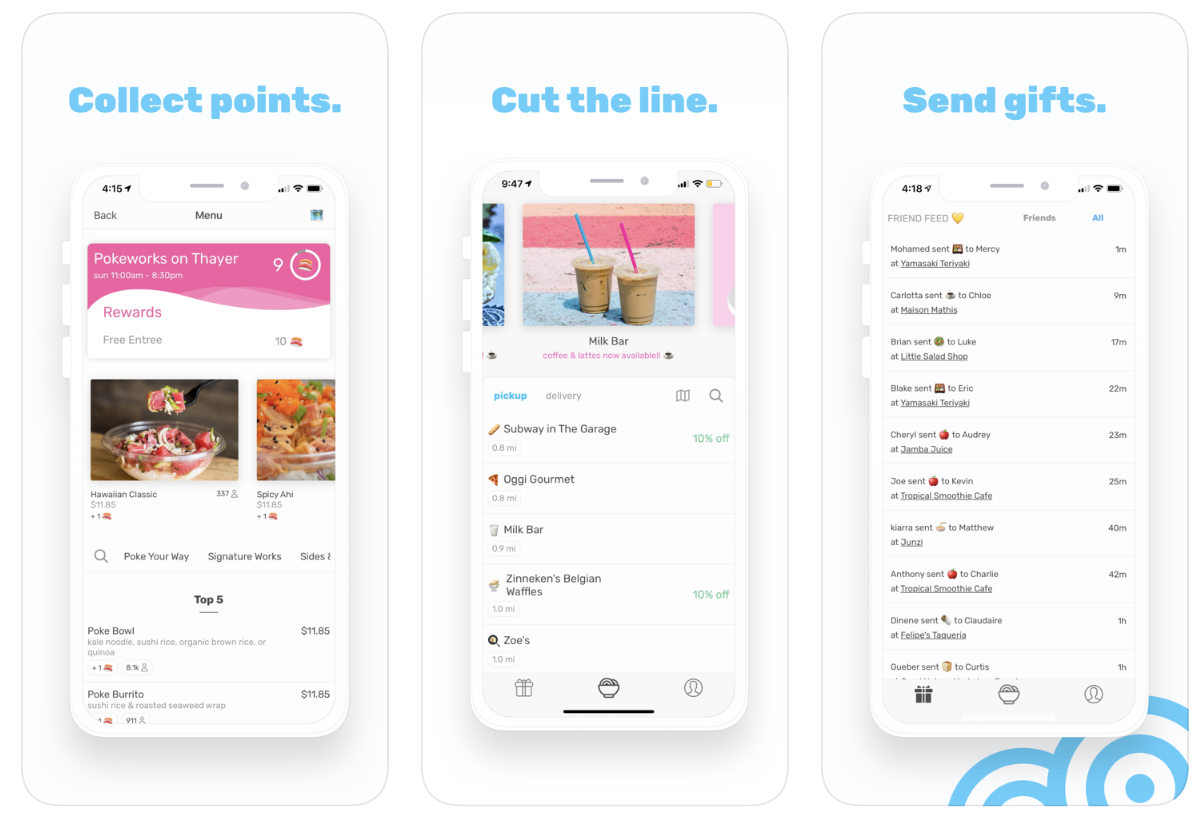

“We were in the back washing blenders so they could keep taking Snackpass orders,” recalls co-founder and CEO Kevin Tan. The team from order-ahead food startup Snackpass was willing to get their hands dirty to keep up with demand at one of their first restaurant partners, Tropical Smoothie Cafe on the Yale University campus.

Why were people so eager to pay for takeout through Snackpass? Because it lets them earn loyalty points to redeem for free food — both for themselves and as gifts for their friends. Sending people Snackpass rewards became a new way to flirt or show gratitude at Yale. And through the Venmo-esque Snackpass social feed, users could keep up with a fresh form of gossip while discovering restaurants.

“Anywhere someone is standing in line to order something, we can solve that with Snackpass,” says Tan. “Consumer spending will be social in the future.”

That future is already taking hold. Two years after launch, Snackpass is on 11 college campuses across the U.S., often boasting a 75% penetration rate amongst students within six months. It takes a cut of every order and keeps margins high because users pick up the food themselves rather than waiting for delivery. While other food ordering startups battle to offer discounts as marauding users deal-hop between apps, Snackpass keeps users coming back through its loyalty program.

Its momentum, retention and opportunity to expand from colleges to dense cities has now won Snackpass a $21 million Series A led by Andreessen Horowitz partner Andrew Chen. The round was joined by other heavy hitters, like Y Combinator, General Catalyst, Inspired Capital and First Round, plus angels, including musician Nas, NFL star Larry Fitzgerald and legendary talent agent Michael Ovitz. Building on Snackpass’ $2.7 million seed, the cash will go toward hiring up with the goal of reaching 100 campuses in two years.

Its momentum, retention and opportunity to expand from colleges to dense cities has now won Snackpass a $21 million Series A led by Andreessen Horowitz partner Andrew Chen. The round was joined by other heavy hitters, like Y Combinator, General Catalyst, Inspired Capital and First Round, plus angels, including musician Nas, NFL star Larry Fitzgerald and legendary talent agent Michael Ovitz. Building on Snackpass’ $2.7 million seed, the cash will go toward hiring up with the goal of reaching 100 campuses in two years.

“Takeout is an important market because it’s huge — also in the hundreds of billions — and fragmented,” writes Chen. “The opportunity complements the food delivery market in a big way: For the average restaurant, there are 6 takeout orders for every delivery order!”

Like many of the best startup ideas, Snackpass was born out of the founders’ own needs at Yale. Slow and expensive food delivery services didn’t make sense for smaller orders like a coffee, ice cream or a pepperoni slice on campuses small enough for customers to walk or bike to the restaurant. Tan says, “I was dabbling in several side projects, including helping a friend who managed a local pizza shop build a website to help better reach the local student community.” He realized how tough it was for restaurants around colleges to retain and reward customers, especially as regulars graduated.

Tan joined up with neuroscience student and Thiel Fellow Jamie Marshall, who became Snackpass’ COO. “I had grown up calling in every order,” Marshall tells me. “Waiting in line didn’t make sense for me. I used every order-ahead platform and thought this was the future.” Jonathan Cameron, a serial entrepreneur who’d built his own order-ahead app called Happy Hour, rounded out the founding team.

Snackpass founders (from left): Jamie Marshall and Kevin Tan

Snackpass offers users a list of nearby restaurants from which they can order ahead, with special tags for ones offering deals. Menu items include counts of how many people have ordered them and how many rewards points you’ll earn buying them. You pay in the app, skip the line at the restaurant and grab your order from the counter. Each restaurant can configure their own rewards system with how much items earn and cost, such as giving you a free coffee for every 10 you buy.

Users can then spend their points to get themselves free menu items, or send a virtual Snackpass gift card to any of their phone contacts or people they find via search. This gives Snackpass a way to grow virally that most food apps lack. Thankfully, you can block people on Snackpass if they get creepy showering you with gifts.

Each purchase and gift on Snackpass shows up in its social feed unless you make it private. “That’s become its own language. People use it to flirt with each other, or bond and connect with someone new,” Tan tells me. “There’s some drama or intrigue there seeing who’s sending gifts to who. People even look at the feed in the way they look at someone’s Instagram to see what’s going on with them.”

Snackpass has also done some integration work specifically for the college market that sets it apart from other order-ahead and delivery services. It can sync with students’ campus meal plans so they can spend them through the app. And student groups from clubs to fraternities can pre-load and replenish accounts for their members. Snackpass works with the same organizations to launch on new campuses. “We host parties, sponsor tailgates and make it feel like a student-led effort so it grows organically across campus communities,” Tan explains. “These efforts, combined with the social feed which would give anyone FOMO if they’re not in the app.”

With all the competition in the space, restaurants can be inundated with apps to manage, some of which just exacerbate spikes in demand that overwhelm kitchens. “There is certainly a risk that local restaurants will start to get platform fatigue, finding that using some apps will take too big of a bite out of their margins,” says Tan. That’s why Snackpass built features that let restaurants batch orders and control how many come in at a certain time so dine-in patients and non-app users aren’t stuck with unreasonable delays.

With all the competition in the space, restaurants can be inundated with apps to manage, some of which just exacerbate spikes in demand that overwhelm kitchens. “There is certainly a risk that local restaurants will start to get platform fatigue, finding that using some apps will take too big of a bite out of their margins,” says Tan. That’s why Snackpass built features that let restaurants batch orders and control how many come in at a certain time so dine-in patients and non-app users aren’t stuck with unreasonable delays.

Snackpass has recruited talent from Uber Eats and an advisor from Yelp’s executive team to help it navigate the tricky SMB sales process. One ace up its sleeve is that it can offer to send push notifications to announce recently signed partners or specials they’re launching, driving the new customers restaurants are desperate for. Tan says his startup is considering if it could charge for this kind of promotion down the line. Most customers who walk into restaurants are effectively in incognito mode, but Snackpass provides its partners with analytics to help them improve their own businesses.

“At the surface level there is a lot of competition in this space,” Tan admits. “The social aspect of the app has been the key differentiator for us. Other companies have been focused on creating the fastest, cheapest, most efficient delivery service, but it’s really hard to make those margins work and consumers are trained to shop around on different apps to get the best deal or fastest delivery time . . . Eating food is supposed to be fun and social, and our generation grew up online and in social networks. We’re combining the social aspect of eating with the utility of order ahead, which has helped us build loyalty and enable retention amongst our users.”

It will still be a battle to overtake long-running competitors like Allset, Level Up and Ritual, plus incumbents that offer takeout pickup like Uber and Grubhub. Logistics is a cut-throat business, and plenty of startups have already failed in the restaurant loyalty space.

Having Andreessen Horowitz’s support could give Snackpass some extra firepower. “A16z has better support and services for their portfolio companies than any other VC we’ve come across and they’ve delivered,” Tan tells me. “We knew that Andrew Chen understands growth and marketplaces from his blog and his Twitter.” That’s critical in a crowded space where such a precise balance of customer acquisition and lifetime value is necessary.

Snapchat, TikTok and Fortnite have all tapped into the youth market with a lighthearted nature that keeps users coming back until they develop network effect. Snackpass is managing to do the same, not with a messaging app or game, but a commerce platform. “We play up creativity, silliness and delight in areas where most companies focus on utility and convenience,” Tan concludes. “We built Snackpass for ourselves and our friends. We’ve carried on this philosophy: if something makes us laugh, we put it in the app.”

Powered by WPeMatico

One of the more notable startups using artificial intelligence to understand and fight cancer has raised $45 million more in funding to continue building out its operations and inch closer to commercialising its work.

Paige — which applies AI-based methods such as machine learning to better map the pathology of cancer, an essential component of understanding the origins and progress of a disease with seemingly infinite mutations (its name is an acronym of Pathology AI Guidance Engine) — says it will be use the funding to inch closer to FDA approvals for products it is developing in areas such as biomarkers and prognostic capabilities.

It also plans to use the funding to continue developing better ways of diagnosing and ultimately fighting the disease, as well as exploring further commercial opportunities for its work, specifically within the bio-pharmaceutical industry.

This round is being led by Healthcare Venture Partners, with previous investor Breyer Capital, Kenan Turnacioglu and other funds participating. The company is not disclosing its valuation, but PitchBook noted that a first close of this round (when it raised $33 million) put the valuation at $208 million. That would value Paige now at about $220 million with the $45 million close, more than three times its valuation in its previous round.

Paige first emerged from stealth back in 2018 — with a bang.

Paige.AI — as it was known at the time — was hatched inside the Memorial Sloan Kettering Cancer Center, one of the world’s foremost institutions both for working on cancer therapies and treating cancer patients, and along with a $25 million investment led by Jim Breyer, Paige had secured exclusive access to MSK’s 25 million pathology slides as well as its intellectual property related to the AI-based computational pathology that underpinned its work. These slides make up one of the biggest repositories of its kind in the world, and as all solutions and services built on machine learning are only as good as the data that’s fed into them, they were critical to the startup’s beginnings.

The startup also launched with some serious talent behind it.

Much of the computational pathology being used by Paige had been developed by Dr Thomas Fuchs, who is known as the “father of computational pathology” and is the director of Computational Pathology in The Warren Alpert Center for Digital and Computational Pathology at Memorial Sloan Kettering, as well as a professor of machine learning at the Weill Cornell Graduate School of Medical Sciences.

Fuchs co-founded Paige with Dr David Klimstra, chairman of the department of pathology at MSK, and Fuchs had originally started out as the CEO of Paige, but was replaced earlier this year by Leo Grady, who joined from another bio-startup, Heartflow (another company backed by Healthcare Venture Partners). Fuchs is still supporting the company, but no longer in an executive role.

In the nearly two years since it launched, there have been some milestones reached. The company, which has around 30 employees today, has been the first to get an FDA breakthrough designation (which helps expedite the long process of drug approvals in urgent areas where there are few or no other options for patients) for using AI in oncology pathology. It’s also the first to get a CE mark in the same category, which opens the door to working in Europe, too. Paige has so far ingested 1.2 million images into its slide database and is using them — in algorithms that also take in genomic data, drug response data and outcome data — to work on developing diagnostic solutions.

But as with all new medical products, progress is not measured in quarters as it might be with a more typical tech startup. Moving fast and breaking things is something to be avoided. So even with all of the above advances, there has yet to be any commercial products launched, nor is Grady giving any specific time frames for when they will. And when the company came out of stealth in 2018, it said it would be focusing on breast, prostate and other major cancers, although today it’s not as quick to specify what its targets will be when it does launch commercial products.

Similarly, it’s also expanding its remit from primarily clinical environments to pharmaceutical ones.

“The clinical side is still our focus, but this is an expansion and realisation that this has a broader impact, and that includes pharmaceutical customers,” Grady said.

And the dropping of the .AI in its name was also intentional, in part a reaction it seems to how much AI gets thrown around today.

“There is a fundamental misconception, which is thinking of AI as a product and not a technology,” said Grady. “It’s a technology set that can allow you to do many things that could not have been done in the past, but you need to apply it in a meaningful way. Developing a good AI and putting that on the market will not cut it in terms of clinical adoption.”

The funding round, Grady said, saw a lot of interest from strategic investors, although the company intentionally has stayed away from these.

“We were approached by all of the scanner vendors and some of the biopharmaceutical companies,” he said. “But we made the decision to not take a strategic investment with this round because we wanted to be neutral with hardware vendors and not be too tied with any one.”

He also pointed to the challenges of talking to investors when you are working in a cutting-edge area (a challenge that has foxed many an investor also into backing the wrong horses, too, such as Theranos).

“We’re at the intersection of three areas: tech, medical devices and clinical medicine, and life sciences and biotech,” he said. “Many investors sit squarely in one and don’t feel comfortable in others. That makes the conversations challenging and short. But there has been an increasing blend between those three sectors.”

That’s where Healthcare Venture Partners fits into the mix. “Paige exemplifies the benefits of digital pathology and represents the bright future of AI-driven medical diagnosis,” said Jeff Lightcap of Healthcare Venture Partners, in a statement. “As hospitals embark on digital transformations, they will face challenges associated with these transitions. We believe Paige addresses many of these issues by enhancing the ability of clinical teams and pathologists to collaborate. We’re confident in Paige’s future and believe they will continue to develop cutting-edge technologies that enable pathology departments to transform their practices, which have changed little in the last century.”

“We applaud Paige’s commitment to building clinical AI products that will improve the diagnostic process and patient care,” added Jim Breyer of Breyer Capital, in a statement. “This is a critical time for Pathology, as pathologists are carrying a heavier workload than ever before. Paige understands their needs and the team has built cutting-edge technologies to address them. Paige represents the future of computational pathology and we look forward to their continued growth and success.”

Powered by WPeMatico

Of all the startup jawns that could possibly come from Philadelphia, perhaps none is as unexpected as Jenzy, the startup that provides an online marketplace and virtual sizing tool for kids’ shoes.

The company, which has raised $1.25 million from Morgan Stanley’s Multicultural Innovation Lab, was born of desperation and grew up on two continents.

Co-founders Eve Ackerley and Carolyn Horner met five years ago in China while working as English language teachers in the remote corners of Yunnan province. Without much in the way of retail options, the two women resorted to doing much of their shopping online… and it was while searching for shoes that they realized one of the major pain points of the online retail experience was finding the right size.

Jenzy founders Carolyn Horner and Eve Ackerley

When they returned to the U.S. the idea stuck with them. So they set out to develop an application that would be able to size feet using nothing more than a smartphone, and worked with vendors to ensure that women could know their sizes and buy the right shoes.

As the idea evolved, the two first-time entrepreneurs realized that however annoying the buying process was for adults, the need for appropriately sized shoes and a marketplace to buy them was even more acute among children.

“The most proprietary part of what we do is standardize all the shoes on our platform,” says Horner.

The company works with brands like Converse, Saucony and Keds to send kids shoes that actually fit their feet. “A kid could be wearing a six in one shoe and a seven in another,” says Horner. Using Jenzy, the shoes will arrive in the right size for each foot. “We work with the suppliers to make sure that we’re sending the correct size to a parent when they check out on Jenzy.”

For retailers, it’s an opportunity to reduce what amounts to a huge cost. The industry average rate for returns is 30%, and Horner says that Jenzy reduces that figure to 15%. And those savings matter in what’s an $11 billion industry, according to Horner’s estimates.

The company launched the first version of its app in July 2017 and just released an update earlier this year. To date, Horner estimates the company has sized 25,000 feet and had 15,000 downloads since May.

“The plan was to see about if we still were interested when we got back from China,” Horner says of the company’s early days.

Initially, the two partners worked out of Ackerley’s parents’ house in California, but eventually moved to Philadelphia when the company pivoted to focus on children’s shoes to be close to their beta testers — Horner’s family, who had a lot of kids.

Powered by WPeMatico

Tusk Venture Partners, the venture capital firm led by Bradley Tusk and managing partner Jordan Nof, has secured $70 million for its second flagship fund, the firm has confirmed to TechCrunch following a report by Fortune this morning.

Fundraising for the effort began in January, when the pair filed paperwork with the U.S. Securities Exchange Commission for Tusk Venture Partners II. The firm, and affiliated political advisory outfit Tusk Ventures, is behind a number of high-profile startups, including e-scooter “unicorn” Bird, cryptocurrency exchange Coinbase and Ro, a direct-to-consumer healthcare business best known for selling erectile dysfunction medication.

The New York-based firm, founded in 2011, previously raised $36 million for its debut fund — capital it used to back fantasy sports company Fanduel, insurtech business Lemonade and D2C vitamin seller Care/of.

Tusk, before launching Tusk Ventures, served as campaign manager for Mike Bloomberg, as deputy governor of Illinois and as communications director for Senator Chuck Schumer. He also penned the book, The Fixer: My Adventures Saving Startups from Death by Politics, released in 2018.

Naturally, Tusk Ventures provides companies more than just checks. The politically savvy team lends its expertise to support companies plagued with regulatory barriers and communications issues, as well as help with grassroots organizing, opposition research and partnerships.

Powered by WPeMatico

Spotify did it. Slack did it. Many other late-stage private technology companies are reported to be seriously considering it. Should yours?

If you are a board member of a late-stage, venture-backed company or part of its management team, you likely have heard of the term “direct listing.” Or you may have attended one or all of the slew of recent conferences being hosted by big-name investment banks and others, including tech investor guru Bill Gurley, who recently debated the pros and cons of choosing a direct listing over a traditional IPO.

Before you decide what’s right for your company, here are a few things you need to know about direct listings.

For people not familiar with the term, a direct listing is an alternative way for a private company to “go public,” but without selling its shares directly to the public and without the traditional underwriting assistance of investment bankers.

In a traditional IPO, a company raises money and creates a public market for its shares by selling newly created stock to investors. In some instances, a select number of pre-IPO investors, usually very large stockholders or management, may also sell a portion of their holdings in the IPO. In an IPO, the company engages investment bankers to help promote, price and sell the stock to investors. The investment bankers are paid a commission for their work that is based on the size of the IPO—usually seven percent for a traditional technology company IPO.

In a direct listing, a company does not sell stock directly to investors and does not receive any new capital. Instead, it facilitates the re-sale of shares held by company insiders such as employees, executives and pre-IPO investors. Investors in a direct listing buy shares directly from these company insiders.

Does this mean that a company doing a direct listing doesn’t need investment banks? Not quite. Companies still engage investment banks to assist with a direct listing and those banks still get paid quite well (to the tune of $35 million in Spotify and $22 million in Slack).

However, the investment banks play a very different role in a direct listing. Unlike a traditional IPO, in a direct listing, investment banks are prohibited under current law from organizing or attending investor meetings and they do not sell stock to investors. Instead, they act purely in an advisory capacity helping a company to position its story to investors, draft its IPO disclosures, educate a company’s insiders on process and strategize on investor outreach and liquidity.

The concept of a direct listing is actually not a new one. Companies in a variety of industries have used similar structures for years. However, the structure has only recently received a lot of investor and media attention because high-profile technology companies have started to use it to go public. But why have technology companies only recently started to consider direct listings?

The rise of massive pre-IPO fundraising rounds

With an abundance of investor capital, especially from institutional investors that historically hadn’t invested in private technology companies, massive pre-IPO fundraising rounds have become the norm. Slack raised over $400 million in August 2018—just over a year prior to its direct listing. Because of this widespread availability of capital, some technology companies are now able to raise sufficient capital before their actual IPO to either become profitable or put them on a path to profitability.

Criticism of current IPO process

There has been increasing negative sentiment, especially amongst well-known venture capitalists, about certain aspects of the traditional IPO process—namely IPO lock-up agreements and the pricing and allocation process.

IPO lock-up agreements. In a traditional IPO, investment bankers require pre-IPO investors, employees and the company to sign a “lock-up agreement” restricting them from selling or distributing shares for a specified period of time following the IPO—usually 180 days. The bankers put these agreements in place in order to stabilize the stock immediately after the IPO. While the merits of a lock-up agreement can certainly be debated, by the time VCs (and other insiders) are allowed to sell following an IPO, oftentimes the stock price has fallen significantly from its highs (sometimes to below the IPO price) or the post lock-up flood of selling can have an immediate negative impact on the trading price.

In a direct listing, there is no lock-up agreement, which allows for equal access to the offering to all of the company’s pre-IPO investors, including rank-and-file employees and smaller pre-IPO stockholders.

IPO pricing and allocation: In a traditional IPO, shares are often allocated directly by a company (with the assistance of its underwriters) to a small number of large, institutional investors. Traditional IPOs are often underpriced by design to provide large institutional investors the benefit of an immediate 10-15% “pop” in the stock price. Over the last few years, some of these “pops” have become more pronounced. For example, Beyond Meat’s stock soared from $25 to $73 on its first day of trading, a 163% gain. This has fueled a concern, particularly shared amongst the VC community, that investment banks improperly price and allocate shares in an IPO in order to benefit these institutional investors, which are also clients of the same investment banks that are underwriting the IPO. While the merits of this concern can also be debated, in instances where there is a large price discrepancy between the trading price of the stock following the IPO and the price of the IPO, there is often a sense that companies have left money on the table and that pre-IPO investors have suffered unnecessary dilution. If the IPO had been priced “correctly,” the company would have had to sell fewer shares to raise the same amount of proceeds.

Because a company is not selling stock in a direct listing, the trading price after listing is purely market driven and is not “set” by the company and its investment bankers. Moreover, since no new shares are issued in a direct listing, insiders do not suffer any dilution.

The Spotify effect

Before Spotify’s direct listing, technology companies hadn’t used the direct listing structure to go public. Spotify was, in many ways, the perfect test case for a direct listing. It was well known, didn’t need any additional capital and was cash flow positive. In addition, prior to its direct listing, Spotify had entered into a debt instrument that penalized the company so long as it remained private. As a result, it just needed to go public. After clearing some regulatory hurdles, Spotify successfully executed its direct listing in April 2018. After Spotify’s direct listing, Slack (relatively) quickly followed suit. Slack’s direct listing was notable because it represented the first traditional Silicon Valley-based VC-backed company to use the structure. It was also an enterprise software company, albeit one with a consumer cult following.

While a direct listing offers many benefits, the structure does not make sense for every company. Below is a list of key benefits and drawbacks:

Powered by WPeMatico

The insurance industry, sleepy and ancient, is ripe for disruption. We’ve seen companies like Lemonade, Hippo and Rhino get in on that opportunity. Today, an insurtech company focused on small business insurance has raised $18 million to keep growing.

Meet Huckleberry, whose Series A was led by Tribe Capital, with participation from Amaranthine, Crosslink Capital and Uncork Capital.

Huckleberry launched in 2017 to offer business insurance, including workers’ compensation and general liability, all through an online portal.

Small business insurance coverage is not like car insurance or renters insurance. It’s not as simple as filling out a few forms and getting a quote. Even if a few platforms do have algorithms for providing quotes, you can’t really close the deal unless you get on the phone.

It’s an incredibly tedious and stressful process. In fact, Huckleberry co-founders Bryan O’Connell and Steve Au first came up with the idea for Huckleberry when they were seeking out their own small business coverage for a previous startup idea.

The industry itself is incredibly fragmented, which is caused in part by the fact that small business coverage underwriting varies wildly from business to business. For example, the policy for three or four restaurants might look relatively similar. However, a fast food restaurant might be identified as a higher risk with regards to workers’ compensation than a Michelin-star restaurant, where workers might be more eager to get back to work and take home their tip money. These differences come in the form of location, operations and many other factors, as well as business vertical.

Huckleberry has worked to build out myriad coverage verticals, including food and beverage, fitness, retail, legal, healthcare, hair and beauty and more.

The firm offers worker’s comp, as well as a package policy that includes general liability, property and business interruption insurance. Customers also can purchase add-ons like hired and non-owned auto insurance, employment practices liability insurance (EPLI), liquor liability insurance, employee dishonesty coverage, professional liability insurance, equipment breakdown coverage and spoilage coverage.

Huckleberry isn’t itself an insurance carrier, but does have the authority to underwrite and sell policies on behalf of the carrier. That said, Huckleberry’s expansion both by vertical and geography is more difficult than your average software startup. The regulatory landscape of insurance in the U.S. goes state by state.

“Our biggest challenge is navigating 50 states’ worth of extremely complicated regulations on something that is much more complicated than a software product,” said O’Connell. “We’re trying to protect individual workers and businesses all while staying fully compliant in every market.”

Powered by WPeMatico

Sapphire Ventures, the former corporate venture arm of SAP, has raised $1.4 billion for growth investments, including a $150 million opportunity fund to support larger deals.

The firm, which focuses primarily on enterprise tech companies in the U.S., Europe and Israel, writes checks to Series B through pre-IPO businesses. Its portfolio includes 23andMe, Sumo Logic and TransferWise.

The new funds brings Sapphire Ventures, which became independent from the German software company SAP in 2011, assets under management to north of $4 billion. Sapphire will write checks sized between $5 million and $100 million with the new funds, allowing the team “to do any financing we need to or want to,” chief executive officer and managing director Nino Marakovic tells TechCrunch. Sapphire’s fourth growth fund is the firm’s largest to date, at more than double the size of their $700 million Fund III.

“We need this fund because companies are staying private much longer because they want to get to a $200 million revenue run rate before they go public,” Sapphire Ventures president and co-founder Jai Das (pictured) tells TechCrunch. “We want to have the capital to support these companies as they keep growing.”

News of the fund comes nearly one year after Sapphire Ventures lassoed $115 million from new limited partners to invest at the intersection of tech, sports, media and entertainment. Sapphire Sport has ties to the sports industry, from City Football Group, which owns English Premier League team Manchester City, to Adidas, the owners of the Indiana Pacers, New York Jets, San Jose Sharks and Tampa Bay Lightning, among others.

Before that, the firm closed on $1 billion for its third flagship venture fund.

With seven check writers and another seven investment professionals focused on growth-stage investments, Sapphire has had a number of recent wins, counting a total of 21 initial public offerings and 55 exits since the firm’s inception.

“We’re excited to have now reached critical mass with $4 billion under management,” Marakovic said. “We are the right size to take advantage of our target area of early and later-stage enterprise software companies. We are innovating on the model by adding value-add LPs and trying to align our whole model of services to the target companies to serve them as best as possible.”

Powered by WPeMatico

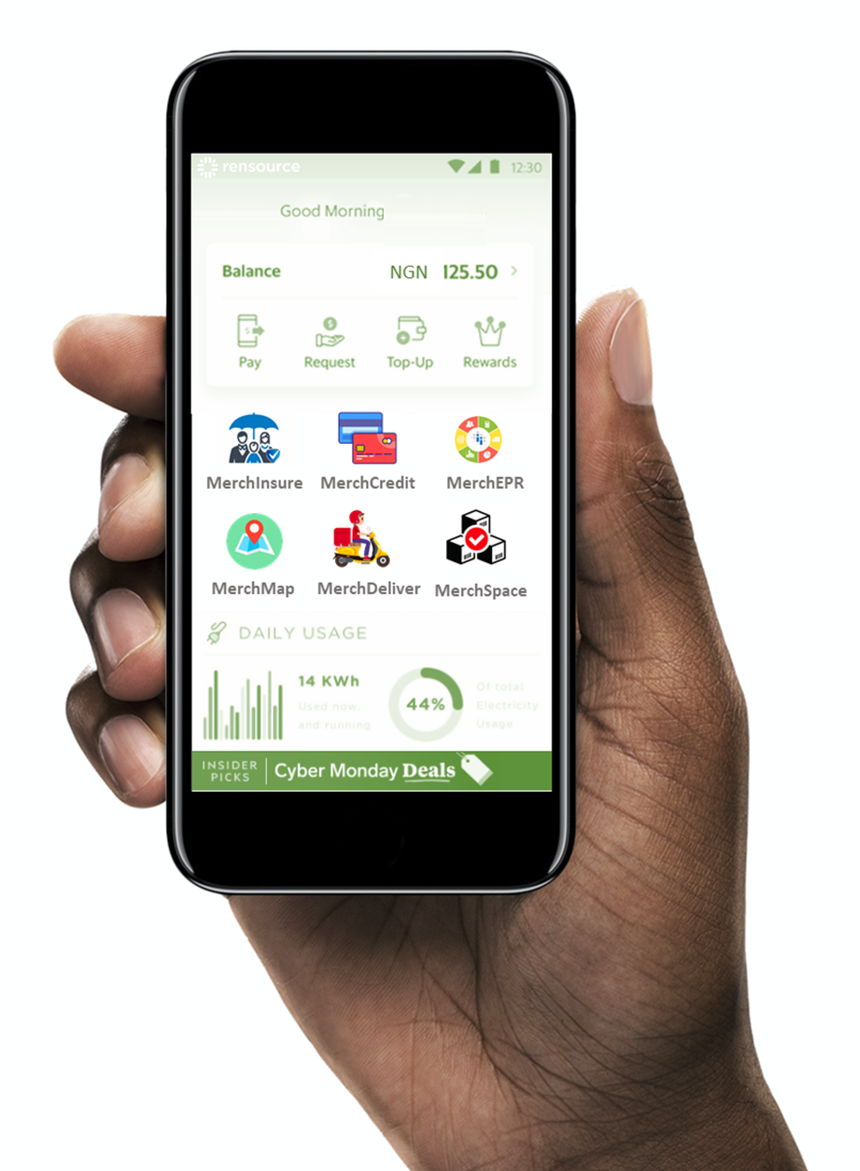

Nigerian startup Rensource Energy has raised a $20 million Series A round co-led by CRE Venture Capital and the Omidyar network.

The renewable energy company builds and operates solar-powered micro-utilities that provide electricity to commercial community structures, such as open-air trading bazaars.

Launched in 2016, the startup has shifted its operating strategy. “We’ve pivoted away from a residential focus…and we’re building much larger systems to become essentially the utility for these large urban markets we have a lot of in Nigeria,” Rensource co-founder Ademola Adesina told TechCrunch.

The company has a partnership with German manufacturer BOS AG, with whom it designs specialized panels for it use case. Rensource also has developer teams in Nigeria and Europe for its software-related programs.

In addition to becoming a micro-energy provider to Nigeria’s robust SME classes, the startup aims to offer them B2B services. With the $20 million round, Rensource is launching its Spaces Offline to Online platform for supply-chain services, including business-analytics and working capital options.

“It’s a mini-ERP tool. We’re trying to bring a universe of people who are banked, but…still offline — their products are offline, they don’t track anything, and there’s no data behind their business — online,” said Adesina.

The benefit Rensource seeks to deliver to Nigeria’s SMEs — at a profit for itself — is to lower overhead costs through better business practices and free them from the bane of generators.

Across marketplaces in West Africa, noisy, fuel-guzzling and pollution-producing generators are like an unwelcome, yet necessary business partner.

Lack of affordable and reliable electricity in Nigeria creates a massive real and opportunity cost to Africa’s largest economy.

For perspective, the West African country is roughly the size of Texas, with a 200 million population larger than Russia, and generates less gigawatt hours of electricity annually than the U.S. state of Connecticut.

Nigerian businesses (and citizens) adjust for these power deficiencies by spending on diesel fuel and generators.

The IMF’s 2019 Nigeria report quoted economic losses of $29 billion in Nigeria due to unreliable electricity supply. On global Doing Business rankings, Nigeria ranked 169 out of 190 countries in the category of “Getting Electricity.”

This difficulty and cost weighs particularly heavy on Nigeria (and the continent’s) SMEs, which often operate in Africa’s informal economy — projected to be one of the largest off-the grid commercial spaces in the world.

Rensource’s micro-utility model deploys power clusters — made up of solar-panels, batteries and a power management system — adjacent to markets and commercial hubs. The energy application isn’t totally clean, as the startup still uses its own diesel backup system.

Rensource’s micro-utility model deploys power clusters — made up of solar-panels, batteries and a power management system — adjacent to markets and commercial hubs. The energy application isn’t totally clean, as the startup still uses its own diesel backup system.

Rensourse has used this model to become an off-grid energy provider in six states in Nigeria, and powers the Sabon Gari market — one of the country’s largest, located in northern Kano State.

The company plans to expand to 100 markets within Nigeria and to additional African countries within 24 months, according to Adesina.

Rensource generates revenue from charging merchants daily, weekly or monthly fees. “In 2017, we did a few hundred thousand dollars in revenue. Last year we did about $7 million in revenue, and this year we’ll do better than that,” Adesina said.

The company doesn’t release official financials, but generated a small profit last year, according to Adesina. He named deploying more of its micro-utilities to new markets and diversifying services as the path to long-term profitability.

Rensource differentiates itself from many home-kit solar energy startups in Africa, such as M-Kopa, by becoming a renewable energy utility at scale.

The startup’s CEO sees the model as a classic leapfrog tech business, effectively bypassing Nigeria’s deficient electricity grid and providing a less capital intensive alternative to large (and often complicated) energy infrastructure projects.

The startup’s CEO sees the model as a classic leapfrog tech business, effectively bypassing Nigeria’s deficient electricity grid and providing a less capital intensive alternative to large (and often complicated) energy infrastructure projects.

Rensource is also following a trend by some Nigeria-based startups, such as trucking-logistics company Kobo360 and motorcycle ride-hail company Gokada, to shape a suite of additional services around the needs of core clients.

In Rensource’s case, those clients are SMEs and traders in the informal economy. “This informality of theirs is what we see as an opportunity in building this new business line and bringing these [merchants] into the online world,” said Adesina.

Powered by WPeMatico

No matter what your startup sells or who you’re selling it to, companies that survive — and grow — need big customers and lots of them. But how do you land million-dollar deals with limited resources and no credibility?

In more than 20 years of building companies and products, I’ve learned that in the grand scheme of the startup lifecycle, while you scale your way through growth to eventual sustainability and success, acquiring your first customer is relatively easy. Any good salesperson can sell a good product to the prospect of their choice. Hell, any mediocre salesperson, even when they’re hawking complete crap, can get lucky once. Your first customer is a great signal, but it’s just a signal, not a savior.

What actually matters is what we learn from that first signal and all the signals that follow.

The process starts way before the first sales pitch. Your chances of closing your first big sale are going to be directly related to how well you’re targeting your prospective customers. So let’s begin with a discussion of aggregation and targeting.

All product and service sales come down to usage and aggregated value. It doesn’t matter if your target customer is a consumer or a business. It makes no difference if your price point is dollars or thousands of dollars. It doesn’t matter if your transaction is completely frictionless or requires a six-month hand-hold by your sales team.

If your customer is a consumer, they’re going to have limited usage with your product or service and the value needs to be tightly wound into that small usage window. If your customer is a business, they’re likely going to have multiple users and almost continuous usage of the product or service, so the value will be delivered over time.

So a “lot of customers” for your product or service might be 100, or it might be a million. Either way, you’re offering the same value per dollar based on usage. You’re aggregating that value into the sale, so you need to be targeting those customer prospects with the highest expected usage.

A classic rookie mistake made by most entrepreneurs is spraying and praying at large prospect audiences for the sake of their largeness alone, hoping that those shards of value surface for the right people at the right time.

Don’t do that. Instead, for B2C sales, you’re going to need some intelligence about your prospect list, which means more than Facebook ad demographics — it’s being able to predict the usage based on the source of the prospect. For B2B sales, you need to determine the optimum type of business to sell into: their size, their industry, their appetite for innovation, and anything else you can use to narrow your focus.

Figure out who is going to get the most aggregate value for their usage and target them.

Targeting customer prospects based on value aggregation is not only going to increase the chances of closing, it’s also going to dictate the near future in terms of the growth of your startup. A targeted, good customer is going to make your life a lot easier. A random, poor customer is going to fill your world with complaints, support requests, change requests, feature requests, and ultimately severe changes to your product roadmap.

When you’re a startup, your customers are buying innovation. The tricky thing is, no one needs innovation. Rather, they need the derivatives of that innovation — time, simplification, throughput, security.

In order to close a big sale, in other words, the aggregation of many, many units of that usage and value, you’re going to have to consolidate that usage and find a champion of value on the customer side.

So the question becomes: Who benefits the most from the derivatives of innovation brought about by maximizing the usage of your product or service?

Powered by WPeMatico