Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Anyone who wants to eat a meatless burger has plenty of options — but what if you want to be a little healthier?

Daring Foods will soon be offering an alternative, in the form of plant-based chicken made from five non-genetically modified ingredients — water, soy, sunflower oil, salt and natural flavoring (a mix of paprika, pepper, ginger, nutmeg, mace, cardamom).

“We’re not here to be a gimmick, we’re here to be part of your life every day,” said Daring Foods co-founder and CEO Ross Mackay. “There’s a big need for plant-based food that’s actually healthy.”

The company started selling the first version of its Daring Pieces product in the United Kingdom at the beginning of this year.

Today, it announced that it has the backing of Rastelli Foods Group, a major U.S. food company supplying hotels, restaurants, retail markets and other commercial customers. In fact, Rastelli has committed $10 million to Daring, an investment that combines cash with infrastructure, sales and distribution support.

With Rastelli’s backing, Daring plans to launch in the United States in February, selling directly to consumers through its website, and also to restaurants and retailers. It sounds like the startup is committed to the U.S. market, and is shifting its headquarters from Glasgow to New York.

I had a chance to try Daring Pieces for myself, when Mackay cooked a light lunch for me earlier this month. He heated them on a pan with no extra seasoning, and they were ready in about eight minutes. He even encouraged me to eat it with my hands, to feel how Daring Pieces have the texture of real chicken.

As a vegetarian, I’m not exactly an authority on chicken, but I thought it tasted pretty close to the real thing. I even brought another portion home and cooked them for dinner a couple nights later.

Mackay is vegan himself, but he said his target audience is meat-eaters who are looking to a more plant-based diet. By focusing on chicken and white meat, he’s hoping to create what he calls a “second generation” of plant-based meat products — healthier than the first, and therefore a bigger part of everyday diets.

Plus, with Daring Pieces you don’t feel like you’ve had a heavy meal, and you can be comfortable knowing that there aren’t a bunch of artificial ingredients.

Powered by WPeMatico

Hiring the right people may be the most important thing you do when you start a new company. But how much time should founders spend on hiring when there are so many other competing demands?

Last week, we discussed team-building and several other issues during a panel on the Extra Crunch stage at Disrupt Berlin with Cloudflare CEO Matthew Prince and Red Points CEO Laura Urquizu.

“I was looking through early emails the other day,” said Prince . “I had forgotten how hard it was to hire people in the very beginning. I think that [Cloudflare co-founder] Michelle [Zatlyn] and I spent probably at least 70% of our time in the first two years just begging people to work for us.”

While it’s a hard job to get right, Prince said he didn’t believe that this was a job he should have outsourced to recruiters. “Fundamentally, as the founder and leader of an organization, your job is to attract and retain the best best possible people,” Prince argued. “And so even to this day, at least a third of my time is spent on recruiting.”

Red Points co-founder Urquizu agreed, noting that she also spends at least a third of her time on recruiting. But she also argued that as you grow as a company, your needs may change and you may need to let some people go.

“I usually say that what brought us here is not going to bring us to the next stage — and that includes people,” she said. “It’s not pleasant and it is very hard when you have to say ‘bye’ to people that have been with you in the journey for two years, or for one year, or three years, but then you need to find the next people that are gonna come along with you in the next stage.”

Powered by WPeMatico

We’re excited to announce a new community perk for Extra Crunch. Starting today, annual and two-year Extra Crunch members located in the United States can get free access to Avodocs from AXDRAFT.

Avodocs provides free legal documents for startups, including NDAs, privacy policies, founders’ agreements, employee onboarding documents, terms of service and more. Founders and startup teams often waste tons of time searching Google and asking friends for legal help. Avodocs provides the necessary documents for early-stage companies in minutes.

Avodocs is used by more than 4,000 startups, including alumni from Y Combinator, 500 Startups and Techstars. Users of Avodocs enjoy having documents ready for signature in less than 10 minutes, plain English description of the implications, a simple Q&A process for creating a document, the ease of editing and personalizing documents after download and the fact that Avodocs works on any device. Users of Avodocs also get access to extra content, such as a consulting agreement and advisory agreement, as well as document storage and DocuSign integration.

Extra Crunch is a membership program from TechCrunch that features how-tos and interviews on company building, intelligence on the most disruptive opportunities for startups, an experience on TechCrunch.com that’s free of banner ads, discounts on TechCrunch events and several community perks like the one mentioned in this article. Our goal is to democratize information about startups, and we’d love to have you join our community.

You can sign up for Extra Crunch here.

After signing up for an annual or two-year Extra Crunch membership (U.S. users only), you’ll receive a welcome email with a link to sign up for Avodocs. If you are already an annual or two-year Extra Crunch member, you will receive an email with the offer at some point today. If you are currently a monthly Extra Crunch subscriber and want to upgrade to annual in order to claim this deal, head over to the “my account” section on TechCrunch.com and click the “upgrade” button.

This is one of several community perks we’ve launched for Extra Crunch members. Other community perks include a 20% discount on TechCrunch events, 100,000 Brex rewards points upon credit card sign up and an opportunity to claim $1,000 in AWS credits. For a full list of community perks from partners, head here.

If there are other community perks you want to see us add, please let us know by emailing travis@techcrunch.com.

To sign up or learn more about all the benefits of Extra Crunch, head here.

Disclaimer:

Documents on Avodocs were created for startups operating in the United States. Avodocs provides self-help services at customer’s specific direction. Avodocs is not a law firm or a substitute for an attorney or law firm.

Communications between customer and Avodocs are protected by Avodocs Privacy Policy, but not by the attorney-client privilege. Avodocs does not provide any kind of advice, explanation, opinion, or recommendation about possible legal rights, remedies, defenses, options, selection of forms, or strategies.

Access to Avodocs is subject to its Terms of Service.

This offer is provided as a partnership between TechCrunch and Avodocs, but it is in no way an endorsement from the TechCrunch editorial team. TechCrunch’s business operations remain separate to ensure editorial integrity.

Powered by WPeMatico

In the wake of WeWork’s embarrassing IPO rout, you might imagine that startups working in similar markets would cool it for a bit. Perhaps they could work on cutting spending, improving their gross margins, and, say, shooting for profitability.

Not so, at least in one case. Instead of doing those things, China-based Ucommune filed to go public in America this month. The WeWork competitor is mostly a co-working business. It’s also a marketing company. And it has some of the worst economics we’ve seen in a company since WeWork.

Why this company is trying to go public isn’t hard to understand. It needs the cash. But at the same time, the chance of it debuting at a price it likes seems slim, given the market’s recent history — as well as Ucommune’s own.

Before we chat about the business fundamentals of Ucommune, a primer on the company itself.

Founded in 2015, according to Crunchbase data, Ucommune has raised over hundreds of millions. In 2018 alone the company raised a venture round and its Series C and its Series D. Prior investors include Gopher Asset Management, Aikang Group, Tianhong Asset Management, All-Stars Investment and Longxi Real Estate.

TechCrunch reported that its final private round valued Ucommune at $3 billion.

All that capital was put to work. According to is F-1 filing, Ucommune operates 197 co-working facilities in 42 cities. The company also claims more than 600,000 members and nearly 73,000 workstations.

The WeWork similarities continue: While discussing itself in its IPO filing, the firm touts an “asset-light model,” which it claims helps property owners “benefit from our professional capabilities and strong brand recognition” as well as allowing its “business to scale at a cost-efficient manner.”

Let’s see.

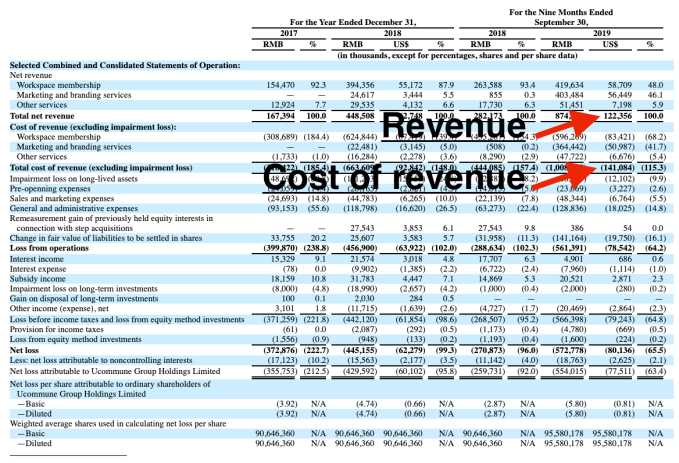

As a primer for all you non-accountants, here’s how you make money as a company: First, generate some revenue. Next, deduct the direct costs that that revenue engendered. What’s left is called “gross profit,” and the relative total of gross profit generated from revenue is called gross margin. From there, subtract your operating costs. If there’s anything left over, that’s operating profit. Now take your operating profit and remove taxes and other costs. What remains is net income.

As you can quickly see, the more gross profit a business generates from its revenue, the more money is has left over to pay for operating expenses. So, revenues that generate lots of gross profit — called high-margin revenue — are better than those that don’t.

Ucommune, our IPO hopeful, is unique in that its revenue doesn’t generate any gross profit at all. Its revenue doesn’t even pay for itself. The company is gross margin negative.

Here’s what that looks like:

If your cost of revenue is higher than your revenue, your gross profit is negative. And that means that you have no gross margin available to fund operating costs. In turn, that means that your company is super unprofitable.

Ucommune is unprofitable, unsurprisingly. (If it feels like we’re overly focused on gross margins, keep in mind that software companies are worth as much as they are in part because they have very high gross margins.)

Things get a bit worse when we look further.

Digging in, Ucommune operates two main businesses. The first enterprise is co-working, which generated just less than half of the company’s total revenue during the first three quarters of 2019. Its second largest business is a marketing effort. Ucommune acquired a company called “Shengguang Zhongshuo” in December of 2018, a deal that lets the company drive revenue by selling “branding services and online targeted marketing services.”

Ucommune is therefore a hybrid co-working and services business. Neither piece of the whole is attractive from a margin perspective. For example, the company’s $58.7 million in co-working revenue earned during the first nine months of 2019 was nearly entirely offset by lease costs ($49.6 million) alone, before the company staffed and otherwise managed the locations in question.

The company’s marketing business is slightly better. Its $56.5 million in revenue from the first three quarters of 2019 was nearly offset by $51.0 million in revenue costs. Ucommune’s services arm, therefore, was more lucrative in terms of generating gross margin for the co-working company than its actual co-working business.

(Bear in mind as we go along that this company wants to go public.)

Wrapping our discussion of yuck, let’s talk about cash. Ucommune had cash and equivalents of $23.4 million and short-term investments worth $11.0 million at the end of Q3 2019. That’s $33.4 million in total that the company can access, presuming that every short-term investment is unwindable into cash inside the window in which Ucommune would need to access it.

A window that is closing, mind. Ucommune’s operations burned through $32.4 million in the first three quarters of 2019. If the company kept consuming cash at its prior pace, we can estimate that it will not have enough cash to make it to the end of Q2 2020. Which is why Ucommune is going public.

The only counterargument to the mess that is Ucommune’s business is that it is growing quickly. That’s true. The company’s revenue grew from ¥282.2 million in the first three quarters of 2018 to ¥874.6 million over the same time period this year. That’s quick!

But instead of demonstrating operating leverage (losing less money as its revenue grew), the company lost more money this year than the last, making its business appear likely to keep burning acres of cash while it grows. And you have to ask yourself if it is a good business, why are its private investors pushing it onto the public markets instead of giving it more of their own money?

They must have known, landing this close to WeWork, how this was going to look. And that’s not confidence-inspiring.

Powered by WPeMatico

Airbnb has well and truly disrupted the world of travel accommodation, changing the conversation not just around how people discover and book places to stay, but what they expect when they get there, and what they expect to pay. Today, one of the startups riding that wave is announcing a significant round of funding to fuel its own contribution to the marketplace.

Domio, a startup that designs and then rents out apart-hotels with kitchens and other full-home experiences, has raised $100 million ($50 million in equity and $50 million in debt) to expand its business in the U.S. and globally to 25 markets by next year, up from 12 today. Its target customers are millennials traveling in groups or families swayed by the size and scope of the accommodation — typically five times bigger than the average hotel room — as well as the price, which is on average 25% cheaper than a hotel room.

The Series B, which actually closed in August of this year, was led by GGV Capital, with participation from Eldridge Industries, 3L Capital, Tribeca Venture Partners, SoftBank NY, Tenaya Capital and Upper90. Upper90 also led the debt round, which will be used to lease and set up new properties.

Domio is not disclosing its valuation, but Jay Roberts, the founder and CEO, said in an interview that it’s a “huge upround” and around 50x the valuation it had in its seed round and that the company has tripled its revenues in the last year. Prior to this, Domio had only raised around $17 million, according to data from PitchBook.

For some comparisons, Sonder — another company that rents out serviced apartments to the kind of travelers who have a taste for boutique hotels — earlier this year raised $225 million at a valuation north of $1 billion. Others like Guesty, which are building platforms for others to list and manage their apartments on platforms like Airbnb, recently raised $35 million with a valuation likely in the range of $180 million to $200 million. Airbnb is estimated to be valued around $31 billion.

Domio plays in an interesting corner of the market. For starters, it focuses its accommodations at many of the same demographics as Airbnb. But where Airbnb offers a veritable hodgepodge of rooms and homes — some are people’s homes, some are vacation places, some never had and never will have a private occupant, and across all those the range of quality varies wildly — Domio offers predictability and consistency with its (possibly more anodyne) inventory.

“We are competing with amateur hosts on Airbnb,” said Roberts, who previously worked in real estate investment banking. “This is the next step, a modern brand, the next Marriott but with a more tech-powered brain and operating model.” These are not to be confused with something like Hilton’s Homewood Suites, Roberts stressed to me. He referred to Homewood as “a soulless hotel chain.”

“Domio is the anti-hotel chain,” he added.

Roberts is also quick to describe how Domio is not a real estate company as much as it is a tech-powered business. For starters, it uses quant-style algorithms that it’s built in-house to identify regions where it wants to build out its business, basing it not just on what consumers are searching for, but also weather patterns, economic indicators and other factors. After identifying a city or other location, it works on securing properties.

It typically sets up its accommodations in newer or completely new buildings, where developers — at least up to now — are not usually constructing with short-term rentals in mind. Instead, they are considering an option like Domio as an alternative to selling as condominiums or apartments, something that might come up if they are sensing that there is a softening in the market. “We typically have 75%-78% occupancy,” Roberts said. He added that hotels on average have occupancy rates in the high 60% nationally.

As Domio lengthens its track record — its 12 U.S. markets include Miami, Los Angeles, Philadelphia and Phoenix — Roberts says that they’re getting a more select seat at the table in conversations.

“Investors are starting to go out to buy properties on our behalf and lease them to us,” he said. This gives the startup a much more favorable rate and terms on those deals. “The next step is that Domio will manage these directly.” The most recent property it signed, he noted, includes a Whole Foods at the ground level, and a gym.

Using technology to identify where to grow is not the only area where tech plays a role. Roberts said that the company is now working on an app — yet to be released — that will be the epicenter of how guests interact to book places and manage their experience once there.

“Everything you can do by speaking to a human in a traditional hotel you will be able to do with the Domio app,” he said. That will include ordering room service, getting more towels, booking experiences and getting restaurant recommendations. “You can book your Uber through the Domio app, or sync your Spotify account to play music in the apartment.

Ans there are plans to extend the retail experience using the app. Roberts says it will be a “shoppable” experience where, if you like a sofa or piece of art in the place where you’re staying, you can order it for your own home. You can even order the same wallpaper that’s been designed to decorate Domio apartments.

Although Airbnb has grown to be nearly as ubiquitous as hotels (and perhaps even more prominent, depending on who you are talking to), the wider travel and accommodation market is still ripe for the taking, estimated to reach $171 billion by 2023 and the highest growth sector in the travel industry.

“Airbnb has taught us that hotels are not the only place to stay,” said Hans Tung, GGV’s managing partner. “Domio is capitalizing on the global shift in short-term travel and the consumer demand for branded experiences. From my travels around the world, there is a large, underserved audience — millennials, families, business teams — who prefer the combined benefits of an apartment and hotel in a single branded experience.”

I mentioned to Roberts that the leasing model reminded me a little of WeWork, which itself does not own the property it curates and turns into office space for its tenants. (The SoftBank investor connection is interesting in that regard.) Roberts was very quick to say that it’s not the same kind of business, even if both are based around leased property re-rented out to tenants.

“One of the things we liked about Domio is that is very capital-efficient,” said Tung, “focusing on the model and payback period. The short-term nature of customer stays and the combination of experience/price required to maintain loyal customers are natural enforcers of efficient unit economics.”

“For GGV, Domio stands out in two ways,” he continued. “First, CEO Jay Roberts and the Domio team’s emphasis on execution is impressive, with expansion into 12 cities in just three years. They have the right combination of vision, speed and agility. Domio’s model can readily tap into the global opportunity as they have ambition to scale to new markets. The global travel and tourism spend is $2.8 trillion with 5 billion annual tourists. Global travelers like having the flexibility and convenience of both an apartment and hotel — with Domio they can have both.”

Powered by WPeMatico

In a world where ad rates are declining for traditional broadcast media, the corporations responsible for making the fictions that millions devour daily need to find a new business model.

Subscription services are on the rise — with every major broadcaster launching an on-demand service — and so are ad-supported video streaming services to replace the traditional networks.

But there’s another Holy Grail of the advertising industry, long thought to be too technologically difficult to achieve, that may finally be within reach. It’s the on-demand product placement of branded goods in a video, and it’s the technology that Ryff has been developing since it was founded in early 2018.

Product placement is an increasingly big business in the U.S., raking in some $11.44 billion in 2019, according to data collected by Statista. That figure is up from $4.75 billion in 2012. The same report indicated that roughly 49% of Americans took action after seeing product placement in media.

The effectiveness of product placement has even been proven by researchers from Indiana University and Emory University. They found that “prominent product placement embedded in television programming does have a net positive impact on online conversations and web traffic for the brand.”

And while streaming services enjoy the dollars their subscribers are throwing at them, they’re also looking at ways to diversify their revenue streams. Netflix and Hulu are both expanding their product marketing divisions and analysts like those from Forrester Research predict that product placement will be a huge moneymaker for the company as traditional ad rates decline.

There are companies that handle product placement already. Startups like Branded Entertainment Network, which works with brands and producers to place real brands into contextually relevant scenes in movies and television, and Mirriad, which adds branded billboards to scenes, are working to bring more money to platforms and producers.

Ryff takes the technology to the next level, using computer vision, machine learning and rendering technologies to identify objects in a scene and replace them with branded products that can be tailored based on customer data.

“The infusion of SVOD/streaming platforms into the market, combined with platforms like Netflix that are unsuccessfully trying to grow their subscriber base will force those same platforms to explore and embrace alternative revenue streams,” said Marlon Nichols, managing general partner at MaC Venture Capital, and a new director on the Ryff board. “In addition, consumers on paid platforms do not want their content consumption interrupted by ads. As such, product placement will be an important growth channel and Ryff’s new marketplace and unique technology set it up to be the unequivocal growth market leader.”

To continue its technology development and ramp up sales and marketing, the company has raised $5 million in financing. According to Crunchbase, Ryff had previously raised $3.6 million from investors, including a subsidiary of the Mahindra Group and undisclosed investors. The new financing came from Valor Siren Ventures, MaC Venture Capital, Moneta Ventures and Vulcan Capital.

“Ryff’s offering is well-timed with the rapidly increasing demand for solutions that extend the reach of a brand’s content and drive business results,” said Uday Ghare, vice president for media and entertainment at Tech Mahindra, in a statement at the time of the company’s investment. “We believe the market will continue to see a shift of brand dollars to both content marketing and programmatic advertising as brands increase their reliance on content-centric programs and look to scale those efforts.”

Ryff’s ads can be tailored to the viewer’s taste, the platform on which video is being distributed, the geography of the broadcast, the date and time of the broadcast and a broader demographic profile, according to the company. Basically it’s like AdWords for videos.

In a blog post writing about the rationale behind his investment firm’s capital commitment to the company, Marlon Nichols of MaC Ventures wrote:

Imagine a future where an IP owner can maximize the value of its content by putting it on the Ryff marketplace, where that content will be mapped for dozens if not hundreds of product placement opportunities and be layered with restrictions that comply with creative needs. Those opportunities will be ranked and priced by their effectiveness to drive marketing goals for brands. Brands can bid on in-video placement opportunities that fit their marketing strategies and budgets. 3D brand assets can be uploaded and inserted dynamically into content right before the moment of video delivery.

Ryff’s first disclosed partnership is with the “reality” television producer Endemol Shine.

“Ryff successfully takes the concept of product placement, the only advertising format that can’t be skipped by the viewer, and delivers a scalable and adaptable advertising solution that can be applied to any content, at any time and in any market,” said Roy Taylor, founder and CEO of Ryff, in a statement. “The result benefits all — content free from annoying distractions, audience-specific brand placement and delivering a new means towards monetizing video assets.”

Powered by WPeMatico

Trialjectory, which is developing a new technology service to match cancer patients with clinical trials, has raised $2.7 million to finance its continued growth.

Led by Contour Venture Partners, the new financing will be used to accelerate Trialjectory’s operations by adding more clinical trials for different cancer types and expanding the company’s outreach to caregivers, pharmaceutical companies and patients, the company said.

“As cancer is the second leading cause of death for Americans — with thousands of new cases diagnosed each year — having access to advanced treatment options is a necessity, not a privilege, as new trials provide better outcomes to patients,” said Tzvia Bader, Trialjectory chief executive and co-founder. “What’s more, one of the top obstacles that oncologists face today is the lack of clinical trial access for patients, which is due to the availability of more treatment options overall. Additionally, it is a very complex process to match the right patient with the right treatment, especially with the rise of personalized medicine.”

The company currently supports trials for breast cancer, colon cancer, bladder cancer, melanoma and myelodysplastic syndromes.

Trialjectory’s software was trained to seek out keywords in unstructured treatment descriptions and extracting relevant data. Its software then groups that information into clusters and standardizes the information to create a database that highlights patient attributes that would be appropriate for clinical trials.

Patients are then matched to the clinical trials after filling out a questionnaire.

“Trialjectory’s work — driven by a highly experienced management team, comprised of both oncology and technology experts — is disrupting and reshaping how we think about traditional cancer care today,” concluded Bob Greene, from Contour Venture Partners . “Even more important, it is empowering patients to take back control of their treatment, and we look forward to watching Trialjectory’s platform continue to grow quickly. We believe that the company has the potential to become a go-to resource for the global medical community to help doctors provide personalized, matched treatment options to patients in need everywhere.”

Powered by WPeMatico

Hugging Face has raised a $15 million funding round led by Lux Capital. The company first built a mobile app that let you chat with an artificial BFF, a sort of chatbot for bored teenagers. More recently, the startup released an open-source library for natural language processing applications. And that library has been massively successful.

A.Capital, Betaworks, Richard Socher, Greg Brockman, Kevin Durant and others are also participating in today’s funding round.

Hugging Face launched its original chatbot app back in early 2017. After months of work, the startup wanted to prove that chatbots don’t have to be a glorified command line interface for customer support.

With the app, you could generate a digital friend and text back and forth with your companion. And it wasn’t just about understanding what you meant — the app tried to detect your emotions to adapt answers based on your feelings.

It turns out that the technology behind that chatbot app is solid. As Brandon Reeves from Lux Capital wrote, there’s been a ton of progress when it comes to computer vision and image processing, but natural language processing has been lagging behind.

Hugging Face’s open-source framework Transformers has been downloaded over a million times. The GitHub project has amassed 19,000 stars, proving that the open-source community thinks this is a useful brick to build upon. Researchers at Google, Microsoft and Facebook have been playing around with it.

Some companies even use it in production, such as challenger bank Monzo for its customer support chatbot and Microsoft Bing. You can leverage Transformers for text classification, information extraction, summarization, text generation and conversational artificial intelligence.

With today’s funding round, the company plans to triple its headcount in New York and Paris.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re looking into Uber’s bike bet and what the push could mean for Lime and other micromobility companies working to find a sustainable business model. As profitability comes back into vogue among investors at the expense of growth, both Uber and a cadre of mobility-focused startups are hoping that electric- and pedal-powered transport pay off.

Let’s take a look.

Uber is most famous for its ride-hailing business, and the on-demand car-hire service that Uber was founded upon still generates the bulk of its revenue. In its most recent quarter, for example, Uber’s ride-hailing segment generated $2.86 billion in adjusted net revenue. The next-largest Uber business, its Uber Eats segment, generated a comparatively modest $392 million in adjusted net revenue.

Which brings us to the smaller Uber efforts. Freight, its aptly-named hauling business, brought in $218 million in adjusted net revenue in the same quarter (Q3 2019). And finally, Uber’s “Other Bets” segment was responsible for $38 million in adjusted net revenue. That was the smallest result, but also the fastest-growing, exploding from $3 million in adjusted net revenue in the year-ago quarter.

While Q3 2019 was better for Uber than its preceding periods regarding growth, the company’s slowing expansion and stiff losses (its net loss in the period came to $1.16 billion), have left the global transportation giant hunting for new revenue. And its Other Bets segment, which includes incomes from “dockless e-bikes and e-scooters,” is growing like heck.

This recent news item was therefore not surprising:

“We want to double down on micromobility,” Christian Freese, Jump’s head of EMEA, told CNBC in an interview. “We have seen how beautifully it works with our core business and ride sharing, and want to invest more and deeper, especially in Europe.”

Uber claims adoption of Jump’s bikes and scooters in Europe has outpaced that of the U.S. in the last eight months. It says more than 500,000 Europeans rode the vehicles in the last eight months alone, racking up 5 million trips in total.

The move by Uber makes good sense. The firm needs to grow, it has found a vein of consumer interest to mine, and it has the scale (financial, and in terms of an existing userbase) to pull off the scheme.

Of course, even if Uber quadrupled its Other Bets income (which includes more than just micromobility dollars), the segment would only add up to around 4% of its Rides adjusted net revenue (using the company’s Q3 figure for reference.) Growth, however, is growth, and investors love a story.

Uber is not the only company that wants to make bikes and scooters work at scale. There are a number of startups around the world that have raised rafts of capital to do just that. And they don’t want Uber to win.

Powered by WPeMatico

Entrepeneur First, the London-headquartered “talent investor” and company builder backed by Silicon Valley’s Greylock, is losing long-time employee Matt Wichrowski to a career in venture capital.

TechCrunch has learned that Wichrowski, who is currently running EF’s “Launch” programme in Europe and is an angel investor, is joining Berlin-based Fly Ventures, where he’ll be giving the enterprise and “deeptech” seed investor a bigger presence in London.

He’s expected to make the move officially in late February or early March and will split his time between Berlin and London. It is also thought that Wichrowski’s recruitment will coincide with Fly Venture beginning to invest out of its rumoured second fund.

Confirming that he is joining Fly Ventures, Wichrowski provided TechCrunch with the following statement:

I’m extremely excited to be joining the Fly team. While I haven’t started yet it does feel like the perfect partnership for me to join. Their investment focus (enterprise and deeptech seed) aligns very very well with the portfolio I worked with at Entrepreneur First/angel investments. And I’m really excited to build a lot of operational excellence within the fund like global network cultivation and platform support for our entrepreneurs. But for sure the most exciting element for me is the team I’ll be working with. I’ve worked with Fly via EF for a few years now and have always been impressed and now having gotten to know them more in depth over the past few months I’m thrilled to call them my (future) partners.

Meanwhile, I understand that Fly Ventures will still be headed up by partners Fredrik Bergenlid (tech lead) and Gabriel Matuschka (investment lead), and there are no plans to open a formal London office as such — Berlin will remain Fly’s home.

However, the VC firm has already made a number of deeptech investments in the U.K., including Wayve, Bloomsbury AI (exited to Facebook) and Scape. The latter two were co-investments with EF, while the broader thinking is that deeptech investing in Europe requires U.K. coverage, hence Wichrowski’s appointment.

To that end, Wichrowski has been actively involved with the U.K. early-stage tech scene for several years, including angel backing CloudNC, amongst others. He moved over to the U.K. in 2014 (from his home in Chicago), when he studied for an MBA at London Business School. He’s worked at Entrepreneur First since 2016 and built much of the company builder’s seed-stage funding product. Wichrowski also spent 18 months working for EF out of Boston, where he led U.S. investor relations and network building.

Sources at EF tell me Wichrowski is highly regarded amongst the leadership team, while EF itself has come a long way since 2016. A fun fact: He originally joined EF on a three-month contract but has ended up doing a four-year stint at the company builder. Not a bad run, I’d say.

Powered by WPeMatico