Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

All manner of startups fail for all manner of reasons. But there’s one constant: this is an incredibly difficult business. Launching a successful company isn’t just a matter of drive and finding the right people (though both, clearly, are important). Doing well in this business requires the stars to align perfectly on a billion different things.

A cursory look at this year’s batch of companies doesn’t find any story quite as spectacular as last year’s big Theranos flameout, which gave us a best-selling book, documentary, podcast series and upcoming Adam McKay/Jennifer Lawrence film. Some, like MoviePass, however, may have come close.

And for every Theranos, there are dozens of stories of hardworking founders with promising products that simply couldn’t make it to the finish line. There’s also room for debate about what is and isn’t a startup. For our purposes, we’re focusing here on independent startups, not digital initiatives from larger companies — though in at least one case, the startup was acquired by a larger company before shutting down.

So without further ado, here are some of the biggest and most fascinating startups that closed up shop in 2019.

Total raised: $182 million

In 2013, a promising young hardware startup showcased a new generation of slot cars onstage at the World Wide Developer Conference keynote. It was quite an honor for a young company. Apple was clearly impressed with how Overdrive pushed the limits of what could be done on the iPhone.

Three years later, Anki released Cozmo. The plucky little robot was the result of large investment, including the hiring of ex-Pixar and Dreamworks animators brought on board to craft a high range of emotions in the robot’s eyes. In late 2018, the company launched the similar but adult-focused Vector robot. By April 2019, Anki had shut its doors, in spite of selling 1.5 million robots and “hundreds of thousands” of Cozmo models.

Total raised: $3 million, acquired by Ford in 2017

Chariot was a shuttle startup hoping to reinvent mass transit with a fleet of vans for commuters. The routes, supposedly, were determined based on a “crowdsourced” vote.

After acquiring the service two years ago, Ford shut it down at the beginning of 2019. The company didn’t offer many details, except to say that “in today’s mobility landscape, the wants and needs of customers and cities are changing rapidly.”

Total raised: $132 million

Daqri, another high-flying, heavily funded AR headset business, shut its doors around September and completed an asset sale. The company is one of many in the sector that failed to succeed in its efforts to court enterprise customers, as well as in its efforts to compete with Magic Leap, Microsoft and others.

Daqri was, at one point, speaking with a large private equity firm about financing ahead of a potential IPO, but as the technical realities facing other AR companies came to light, the firm backed out and the deal crumbled, according to earlier TechCrunch reporting. Sadly, Daqri wasn’t the only AR business to crumble this year.

Total raised: $4.7 million

HomeShare tried to deal with the challenge of rapidly rising housing costs by matching roommates who shared apartments split into “micro-rooms.” The company said that as of March, it had about 1,000 active residents.

As part of the shutdown, HomeShare said residents would not be getting back the deposits for their partitions — but they would be able to keep the divider or sell it.

Total raised: $72.7 million

Between Anki and Jibo, you could say it was a tough year for consumer social robots. But then, there’s never been a great year for the category. Not yet, at least. Like the sad death of the original Aibo before it, Jibo’s end was punctuated by the incredibly depressing nature of watching an adorable robot friend draw its final breath. Jibo did just that in April, telling consumers, “I want to say I’ve really enjoyed our time together. Thank you very, very much for having me around.”

Jibo technically died in late-2018, but we’re making an exception due to the dramatic nature of its demise. The end came in spite of a successful crowdfunding campaign and a healthy amount of venture capital raised. In spite of it all, the startup was forced to lay off most of its staff and then, ultimately, send Jibo upstate to live on the robo-farm.

Total raised: $68.7 million, acquired by Helios and Matheson in 2017

Image: Bryce Durbin / TechCrunch

Holy hell. Where to even start with this one? When we were putting this list together, one TechCruncher remarked that he swore MoviePass shut down years ago. That’s because (not unlike some current political events), the ticket subscription service’s magnificent train wreck of a demise appeared to unfold over the course of several years, in excruciating slow motion. We wrote a lot about it. A lot, a lot.

In fact, there seemed to be a new disaster every week, as the company hemorrhaged money, limited its service, experience outages, borrowed even more money, was forced to enter a kind of zombie state and had a massive data breech. Oh, and then there was the John Gotti movie it financed that was arguably even worse. By the end of it all, MoviePass’ ultimate demise almost felt like an act of mercy.

Total raised: $125 million

One of the first startup scandals of 2019 involved a once well-known meal delivery startup, Munchery . After the business emailed its customers notifying them of its imminent shutdown, its vendors came forward with a slew of accusations. Namely, the food delivery startup took advantage of them in its final hours, knowingly allowing them to continue making deliveries it couldn’t pay for.

The company’s sudden demise sparked a debate around accountability. While the CEO and its venture capital investors stayed largely silent, its vendors cried out for an explanation and even protested outside the offices of Sherpa Capital, one of Munchery’s backers, in search of answers and payments.

Total raised: $145,000

One of the most recent additions to this list, Bay Area-based food startup Nomiku called it quits earlier this month. The company helped pioneer the consumer sous vide category, only to see the market flooded by competing devices. In multiple successful Kickstarter campaigns totaling $1.3 million, backing from Samsung Ventures and an attempted pivot into meal plans, the startup just couldn’t survive.

“The total climate for food tech is different than it used to be,” CEO Lisa Fetterman told TechCrunch. “There was a time when food tech and hardware were much more hot and viable. I think a company can survive a few hurdles, and a few challenges [ …] For me, it was the perfect storm of all these things.”

Total raised: $58 million

A pioneer in the AR glasses space, news emerged of Osterhout Design Group’s (ODG) demise in the first few weeks of January. Only a couple of years ago, the company raised a $58 million financing — less than a year later, it had burned through its funding and couldn’t pay employees. By early 2018, ODG had lost half of its workforce as it sought loans to pay back employees. By early 2019, only a skeleton crew awaited a patent sale after acquisitions from several large tech companies, including Facebook and Magic Leap, fell through.

“I hope Magic Leap is a huge success. I want everyone in AR to be a huge success,” Osterhout said in an interview with TechCrunch in 2017. “[Augmented reality] is going to be transformative.”

Total raised: $35.3 million

The startup began as a physical storage company, then tried to pivot after selling off its physical storage operations to competitor Clutter in May — it tried, unsuccessfully, to build a white-label software platform that would allow brick-and-mortar merchants to operate their own businesses for renting and selling products.

As part of the shutdown, roughly 10 Omni engineers were hired by Coinbase.

Scaled Inference (2014 – 2019)

Total raised: $17.6 million

Founded by former Googlers Olcan Sercinoglu and Dmitry Lepikhin, Scaled Inference made headlines in 2014 with a plan to build machine learning and artificial intelligence technology similar to what’s used internally by companies like Google, and making it available as a cloud service that can be used by anyone. The ambitions were grand and attracted investors like Felicis Ventures, Tencent and Khosla Ventures.

Unfortunately, the company was forced to call it quits recently. Former CEO Sercinoglu tells us the shutdown was a result of a lack of funding due to insufficient commercial traction. “We were working on various options until the last minute and retained the team as long as we could, but it did not work out. On the plus side, we were able to be transparent with the team throughout the process,” he said.

Total raised: $1.9 million

It was a rough year for MoviePass -style movie ticket subscription services in general. Sinemia seemed at first to be a more sustainable competitor, but it was plagued by subscriber complaints and even lawsuits around app issues, hidden charges and policies for shuttering accounts.

In April, the company announced that it was ending U.S. operations. To be clear, it did not say that it was shutting down entirely (much of its staff was based in Turkey), but the company’s website has since gone offline. If Sinemia survives in some form, it has disappeared from view.

Unicorn Scooters (2018 – 2019)

Total raised: $150,000

Unicorn Scooters was one of the first fatalities of the electric scooter craze of 2018, though certainly not the last. As the story goes, the business spent way too much money on Facebook and Google ads; the startup quickly shut down with no money left over to issue refunds for more than 300 of its $699 scooters that had been ordered.

The not-so-aptly named Unicorn had completed the Y Combinator startup accelerator only a few months before it called it quits, likely making it one of the fastest YC grads to shutter post-graduation. “Unfortunately, the cost of the ads were just too expensive to build a sustainable business,” Unicorn’s CEO Nick Evans wrote, according to The Verge. “And as the weather continued to get colder throughout the US and more scooters from other companies came on to the market, it became harder and harder to sell Unicorns, leading to a higher cost for ads and fewer customers.”

Total raised: $15 million

via @VrealOfficial twitter

Vreal was an ambitious game-streaming platform that aimed to let VR users explore the worlds in which live-streamers were playing. Those users could walk around streamers as avatars, or they could explore on their own as passive observers while listening to the live-streamer blast their way through zombies.

“Unfortunately, the VR market never developed as quickly as we all had hoped, and we were definitely ahead of our time,” the company said in a blog post. “As a result, Vreal is shutting down operations and our wonderful team members are moving on to other opportunities.”

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re peeking at what’s gone on in the world of altcoins recently, the other cryptocurrencies aside from bitcoin.

As 2016 came to a close, altcoins like ether and XRP saw their value soar. Toward the end of 2016 through early 2018, bitcoin’s relative share of the aggregate value of all cryptocurrencies fell to about a third.

Since then there’s been a reversal. Bitcoin is not only back over the 50% market share mark, it has effectively doubled its portion of crypto worth over the last two years.

What happened? Why altcoins have struggled isn’t something we can answer with a single data point or chart. But we can highlight a few reasons that help explain what happened. We’ll start with a look at the data and then we’ll highlight three ideas concerning what changed that pushed altcoins down, and bitcoin back up.

Over the past few weeks we’ve spent most of our time digging into IPOs, larger startups, stocks and revenue thresholds. Today we’re expanding our horizons a bit, looking at a market that sits somewhere to the side of our usual public-private divide. We’re having fun!

Let’s start with a few caveats to save tweets.

We all know that comparing the value of a cryptocurrency or token isn’t the only way to stack blockchains against one another. We also also know that comparing market caps isn’t a perfect way to examine the market. And, yes, there’s lots of development work that goes on behind the scenes that doesn’t show up in the data we are going to examine.

That said, we’re nearly 11 years into the bitcoin era. We care a bit more today than we did a half-decade ago about what is, versus what might be.

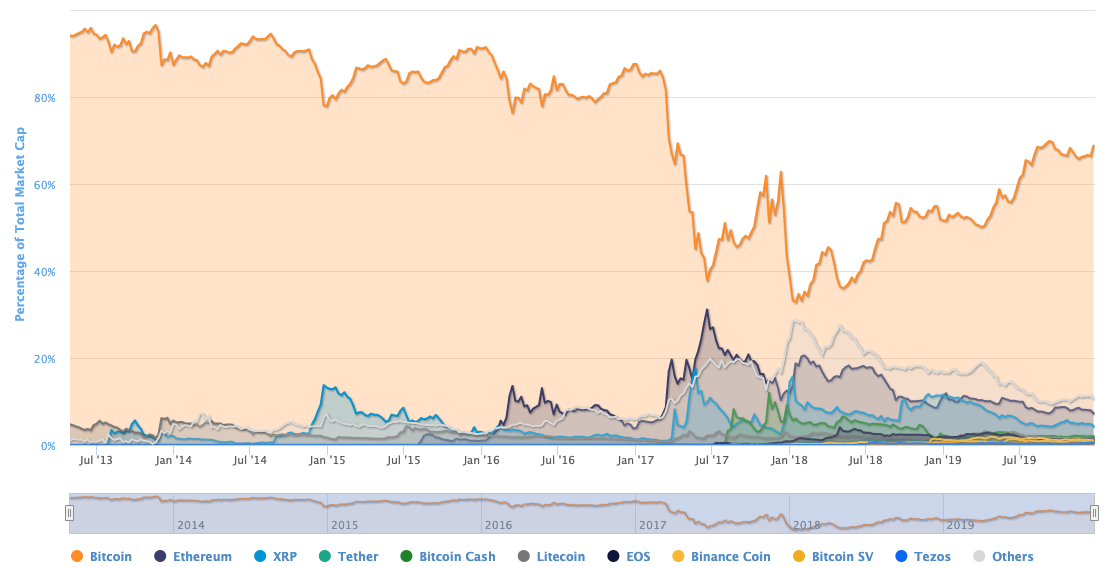

From the fine folks over at CoinMarketCap, the following set of data maps the relative value of the major cryptos, with smaller coins aggregated into a shared line:

I know it’s the day after a major holiday, so let’s help out. The big orange area is bitcoin. The 2017-2018 era is the period in which altcoins had their heyday. And since mid-2018 you can see bitcoin recapture most of its lost, relative prominence.

Bearing in mind that the value of bitcoin has traded as high as roughly $20,000 in late 2017, and is worth about $7,400 today, the chart does not merely show bitcoin recovering its former value. But it does show how over the last two years bitcoin’s share of the value of traded cryptos has doubled. Here are the key data points:

More simply, bitcoin’s share of the value of all cryptos held steady above 80% for a very long time. Then in early 2017 that same share began to fall. It continued to slip into the early days of 2018. Since then it recovered first to its December 2017 levels. And this year the relative value of bitcoin rose again, bringing it to twice its lowest ratings.

Why did that happen? Here are three reasons that form a part of the why.

For those of you with pie to eat, here’s our arguments upfront. Bitcoin bounced back due to:

Powered by WPeMatico

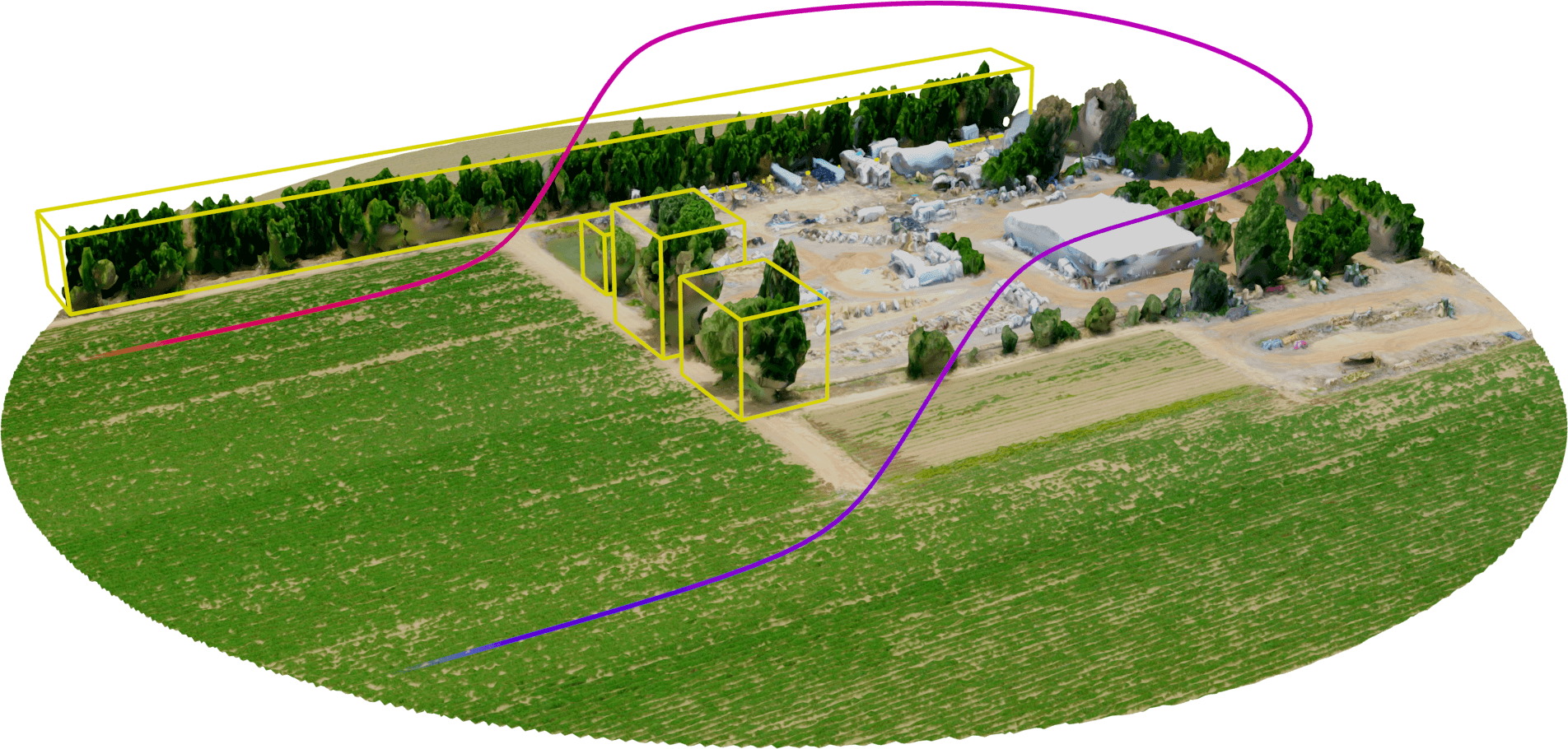

Modern agriculture involves fields of mind-boggling size, and spraying them efficiently is a serious operational challenge. Pyka is taking on the largely human-powered spray business with an autonomous winged craft and, crucially, regulatory approval.

Just as we’ve seen with DroneSeed, this type of flying is risky for pilots, who must fly very close to the ground and other obstacles, yet also highly susceptible to automation; That’s because it involves lots of repetitive flight patterns that must be executed perfectly, over and over.

Pyka’s approach is unlike that of many in the drone industry, which has tended to use multirotor craft for their maneuverability and easy take-off and landing. But those drones can’t carry the weight and volume of pesticides and other chemicals that (unfortunately) need to be deployed at large scales.

The craft Pyka has built is more traditional, resembling a traditional one-seater crop dusting plane but lacking the cockpit. It’s driven by a trio of propellers, and most of the interior is given over to payload (it can carry about 450 pounds) and batteries. Of course, there is also a sensing suite and onboard computer to handle the immediate demands of automated flight.

Pyka can take off or land on a 150-foot stretch of flat land, so you don’t have to worry about setting up a runway and wasting energy getting to the target area. Of course, it’ll eventually need to swap out batteries, which is part of the ground crew’s responsibilities. They’ll also be designing the overall course for the craft, though the actual flight path and moment-to-moment decisions are handled by the flight computer.

Example of a flight path accounting for obstacles without human input

All this means the plane, apparently called the Egret, can spray about a hundred acres per hour, about the same as a helicopter. But the autonomous craft provides improved precision (it flies lower) and safety (no human pulling difficult maneuvers every minute or two).

Perhaps more importantly, the feds don’t mind it. Pyka claims to be the only company in the world with a commercially approved large autonomous electric aircraft. Small ones like drones have been approved left and right, but the Egret is approaching the size of a traditional “small aircraft,” like a Piper Cub.

Of course, that’s just the craft — other regulatory hurdles hinder wide deployment, like communicating with air traffic management and other craft; certification of the craft in other ways; a more robust long-range sense and avoid system and so on. But Pyka’s Egret has already flown thousands of miles at test farms that pay for the privilege. (Pyka declined to comment on its business model, customers or revenues.)

The company’s founding team — Michael Norcia, Chuma Ogunwole, Kyle Moore and Nathan White — comes from a variety of well-known companies working in adjacent spaces: Cora, Kittyhawk, Joby Aviation, Google X, Waymo and Morgan Stanley (that’s the COO).

The $11 million seed round was led by Prime Movers Lab, with participation from Y Combinator, Greycroft, Data Collective and Bold Capital Partners.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

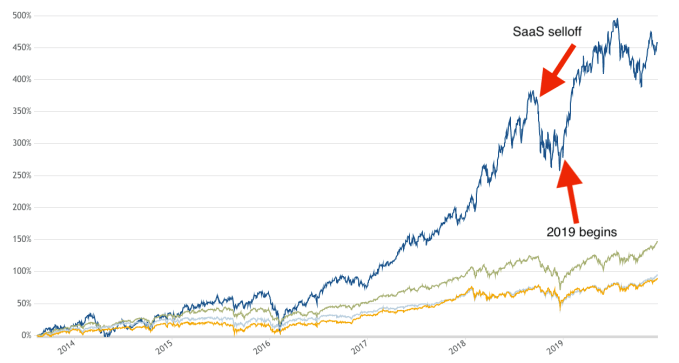

Today, something short. Continuing our loose collection of looks back of the past year, it’s worth remembering two related facts. First, that this time last year SaaS stocks were getting beat up. And, second, that in the ensuing year they’ve risen mightily.

If you are in a hurry, the gist of our point is that the recovery in value of SaaS stocks probably made a number of 2019 IPOs possible. And, given that SaaS shares have recovered well as a group, that the 2020 IPO season should be active as all heck, provided that things don’t change.

Let’s not forget how slack the public markets were a year ago for a startup category vital to venture capital returns.

We’re depending on Bessemer’s cloud index today, renamed the “BVP Nasdaq Emerging Cloud Index” when it was rebuilt in October. The Cloud Index is a collection of SaaS and cloud companies that are trackable as a unit, helping provide good data on the value of modern software and tooling concerns.

If the index rises, it’s generally good news for startups as it implies that investors are bidding up the value of SaaS companies as they grow; if the index falls, it implies that revenue multiples are contracting amongst the public comps of SaaS startups.*

Ultimately, startups want public companies that look like them (comps) to have sky-high revenue multiples (price/sales multiples, basically). That helps startups argue for a better valuation during their next round; or it helps them defend their current valuation as they grow.

Given that it’s Christmas Eve, I’m going to present you with a somewhat ugly chart. Today I can do no better. Please excuse the annotation fidelity as well:

Powered by WPeMatico

American automotive technology startup Rivian has raised $1.3 billion in new funding, the company announced today. The new investment is the fourth round of capital announced by the company in 2019 alone, following prior announcements of $700 million led by Amazon, $500 million from Ford (which includes a collaboration on electric vehicle technology) and $350 million from Cox Automotive.

That’s a lot of money, but Rivian’s not your typical startup, as it’s aiming to bring fully electric vehicles to market, including the R1T pickup truck and the R1S sport utility vehicle. Both of those are consumer cars, which the company aims to bring to market starting at the end of next year — and Rivian is also working with Amazon on all-electric delivery vans, of which the commerce giant has ordered 100,000, with a target of starting deliveries of the first of those in 2021.

Rivian’s new monster round includes participation from Amazon and Ford Motor Company, along with funds advised by T. Rowe Price Associates and BlackRock, the company said in a release. It’s not adding any new board seats attached to this funding, and it’s not sharing any further details on the specific funds involved in the investment at this time.

The company, founded in 2009, has R&D facilities in a number of cities globally, and also has a 2.6-million-square-foot manufacturing facility in Normal, Ill. It debuted its pickup and SUV at the LA Auto Show last November, and the vehicles will launch with higher-end trim levels first, including up to 410 miles of range on a single charge. Base prices for the R1T pickup start at $69,000 before any tax credits are applied, while the R1S SUV starts at $72,500; Rivian has been taking pre-order reservations, available with a $1,000 deposit.

For a company that in many ways has seemed to appear out of nowhere, Rivian’s capitalization and partnerships make it one of the better existing contenders to take on Tesla, especially in the truck and SUV categories, where Tesla has less presence, with only the high-end Model X actually available to purchase so far.

Powered by WPeMatico

Mastercard announced today that it is acquiring RiskRecon, a Salt Lake City startup that uses publicly available data to build security assessments of organizations. The companies did not share the purchase price.

It has become increasingly important for financial services companies like Mastercard to help customers navigate cybersecurity, and RiskRecon will give customers an objective score of a company’s risk profile.

“Through a powerful combination of AI and data-driven advanced technology, RiskRecon offers an exciting opportunity to complement our existing strategy and technology to secure the cyber space,” Ajay Bhalla, president of cyber and intelligence for Mastercard, said in a statement.

RiskRecon CEO Kelly White told TechCrunch in a 2016 interview after the company’s $3 million seed round that the company looks at information that is readily available on the internet and puts it together to measure a company’s overall security risk:

RiskRecon leverages information that is available on the web from companies operating there as part of the act of doing business. “If you stand up web servers and DNS servers, these are intentionally discoverable because they are providing services on the internet. Systems reveal the software being run and version information from which you can determine security performance.”

White sees joining Mastercard as an opportunity to be a part of a larger organization and all that that entails. “By becoming part of their team, we have an opportunity to scale our solution and help companies in new industries and geographies take steps to better manage their cybersecurity risk,” he said in a statement.

RiskRecon launched in 2015 and has raised $40 million, according to Crunchbase data. Investors included Accel, Dell Technologies Capital, General Catalyst and F-Prime Capital.

It’s worth noting that the company was not alone in the space, competing with New York City-based SecurityScoreCard, which launched in 2013 and has raised over $112 million, according to Crunchbase. The last investment came in June for $50 million.

Today’s deal is subject to standard regulatory approval, but is expected to close in the first quarter in 2020.

Powered by WPeMatico

Eddy Travels, an AI-powered travel assistant bot which can understand text and voice messages, has closed a pre-seed round of around $500,000 led by Techstars Toronto, Practica Capital and Open Circle Capital VC funds from Lithuania, with angel investors from the U.S., Canada, U.K.

Launched in November 2018, Eddy Travels claims to have more than 100,000 users worldwide.

Travelers can send voice and text messages to the Eddy Travels bot and get personalized suggestions for the best flights. Because of this ease of use, it now gets 40,000 flight searches per month — tiny compared to the major travels portals, but not bad for a bot that is available on Facebook Messenger, WhatsApp, Telegram, Rakuten Viber, Line and Slack chat apps.

The team is now looking to expand into accommodation, car rentals and other travel services. Eddy Travels search is powered by partnerships with Skyscanner and Emirates Airline.

The founders are from Lithuania: Edmundas Balcikonis, CEO, (previously founded and led as CEO TrackDuck startup, acquired by Invision), Pranas Kiziela and Adomas Baltagalvis. The company HQ is in Toronto, Canada.

Powered by WPeMatico

HomeLane, a Bangalore-based startup that helps people manage home renovations and interior design, today announced it has raised $30 million in a new financing round as it looks to expand its proprietary technology.

The financing round, dubbed Series D, was led by Evolvence India Fund (EIF), Pidilite Group and FJ Labs. Existing investors Accel Partners, Sequoia Capital and JSW Ventures also participated in the round, which pushes the five-year-old startup’s all-time raise to $46 million.

HomeLane helps property owners furnish and install fixtures in their new apartments and houses. Interior designers need to be local to customers and supply chain partners need to have the capacity to ship to a location. So HomeLane has established 16 experience centers in seven Indian cities so consumers can touch and see materials and furniture.

The startup plans to use the fresh capital to broaden its technology infrastructure and expand to eight to 10 additional cities.

HomeLane competes with other online furniture sellers such as Livspace and Urban Ladder, as well as brick-and-mortar stores. Founders Rama Harinath and Srikanth Iyer say their startup differentiates by offering a one-stop shop — it sells everything from fitted kitchens and wardrobes to entertainment units and shoe racks — and by providing guaranteed on-time delivery and after-sale services to help homeowners finish projects.

The site allows property owners to upload floor plans, which are reviewed by interior designers who provide product suggestions, price quotes and 3D pictures of how furnishings and fixtures will look after they are installed. The startup, which has worked with more than 900 design experts to deliver over 6,000 projects, pays to the designers a fraction of the money it charges customers.

Iyer, who serves as the chief executive of HomeLane, claimed that the startup is inching closer to being EBIDTA profitable (which does not include taxes and a range of other expenses). That would be a notable turnaround for HomeLane, which reported a net loss of $4.1 million on revenue of $5.6 million in the financial year that ended in March 2018.

Prashanth Prakash, a partner at Accel India, said, “We are very happy with HomeLane’s current growth trajectory and are believers in the long-term growth prospects of the home improvement consumer segment in India.”

Powered by WPeMatico

Artificial intelligence is a powerful tool, but it’s not a magic wand. Applying the technology requires thought and dedication, especially with legacy industries like law and insurance, which are being taken on in this way by Luminance and Omnius respectively. The companies’ founders, Emily Foges and Sofie Quidenus-Wahlforss, spoke with great insight on this on stage at Disrupt Berlin.

Luminance uses AI and natural language processing to help law firms process documents more quickly, not replacing the lawyer but providing additional intelligence and analysis of what may be hundreds or thousands of pages and saving time and money. Omnius applies AI not just to the text of insurance claims, but to the process of handling them, ensuring rapidity not only in documentation but in results like payouts.

Omnius has raised about $30 million in multiple small rounds and grants, while Luminance has raised some $23M mainly in its A and B rounds.

I’ve edited and contextualized our conversation here, but you can also watch the full panel below. I’ve made some slight changes for readability but left things mostly intact. Pull quotes belonging to Emily are on the left, Sofie’s are on the right.

The first thing I wanted to hear from the founders was why they chose these industries, and why now? After all, law and insurance are notoriously old-fashioned, some would even say backwards in many ways. How could they be sure this was an opportunity, and not a folly?

Emily Foges (Luminance): It had more to do with the capabilities of the technology, actually. We started with technology that can read a lot of language, and then we looked at what industry would benefit most from that. It was that way around.

I think the timing is 80 percent of the battle; The fact that the legal profession had got to a point of being ready to accept the use of that kind of technology was more luck than anything. But there’s been such an explosion in enterprise data that lawyers just can’t possibly cope with reading and all of the documentation that they need to — so the market was ready.

Sofie Quidenus-Wahlforss (Omnius): I think we come from a very similar background. We started on a horizontal level, with deep document understanding, and at some point we understood, if you really want to ship business value, you need to dive into one vertical.

We have different verticals to choose: manufacturing, legal, pharma… so then we were like, okay, which area is the biggest that is not transformed yet? And do we see decision makers aware of the of the need to do something? And do they have money?

The insuretech world is of course making a lot of pressure, all the new insurance companies like Lemonade, WeFox, Coya, because they claim to settle a claim in minutes. So the big guys like Alliance, they got nervous. And on the other hand you see, on the technology side, improvements in the areas of computing power, way more access to data, more flexible models. So we thought, the industry is ready, the technology’s ready, I was ready to build a big company. It’s my fourth company and I was like, this time I’ll build something huge. So everything fell into place.

They don’t call them legacy industries for nothing, though. These domains, and some companies, that have existed for decades or even a century or more. That means legacy systems and legacy people, to put it kindly, that may not be amenable to change. Emily had some surprising stats on that, while Sofie advocated an AI-like approach to classifying and selecting clients.

Emily: Some of them are more ready than others, and I think the ones who aren’t ready need to really catch up, because we got to critical mass really quickly. We’re only three and a half years old, but we’ve got 185 law firms around the world signed up. The interesting thing was the most ready people were the law firms outside of the UK, outside of the US. It was European law firms, APAC-based law firms, South and Central American law firms who got on board first. They were more ready because to be honest, the commercial pressure was greater. And then the pressure on the US and UK law firms came from them.

This is something I can really recommend for every startup trying to transform an industry from scratch: classifying your customers. We had 16-17 criteria, how we defined the companies we really want to spend time with.

Sofie: We thought, cool, the transformation is happening already. But after a while, 2018, we were like, okay, this market is not moving as fast as we thought . We looked at our proof of concept, our pilots we did with insurance companies and were like, wow, every big insurance company in Europe wants to have an AI pilot project but who’s really ready to start with AI full production?

And this is something I can really recommend for every startup trying to transform an industry from scratch: classifying your customers. Who is a laggard, who is an early adopter, who is early mainstream, is an innovator? Then we decided together with the board, okay, we’ll only focus on innovators and early adopters, and the rest should wait, or we can both wait for each other — but we cannot waste our time.

Powered by WPeMatico

Every once in a while on VC Twitter, a comment or statement seems so outlandish, so completely outrageous, that it must be — certainly has to be — false. Such as it was for Primary Ventures investor Jason Shuman, who commented on the recent prices for pitch deck advice in the Valley today:

Founder friend just told me that SF deck designers have quoted him between $20K to $40K + the right to invest up to $250K…my mind is officially blown

— Jason Shuman

(@BoatShuman) December 20, 2019

You can almost hear that plaintive scream, “My mind is officially blown” (Shuman doesn’t scream, mind you). And indeed, in a world where more and more founders are worried about a bubble; assets are more, let’s say, Notionally expensive than ever before; and everything just seems a little bit crazy these days, it seems downright, fucking insane to think that a PowerPoint file and some “thoughts” are worth tens of thousands of dollars, and a goddamn term sheet to boot.

But they are.

Or at the very least, they can be. And I say that as the guy who wrote an article last week entitled, “How to avoid the startup trap of the parasitic consultant.”

For sure, not every pitch deck consultant is worth top dollar, any more than not every croissant in New York’s West Village is worth $10. But some are, and certainly an elect chosen set of consultants are worth every penny they demand.

The best consultants are not luxuries to plaster on your WeWork’s walls, but critical tools to invest in your startup. Framing a startup’s thesis, product, team, and market exactly right is a qualitative skill that can’t be learned from reading a book or scanning through a founder friend’s deck or two. Get a single slide wrong, or hell, a single bullet point wrong and the whole thing can blow up in a pitch meeting in thirty seconds or less.

Trust me. As a former VC investor, I have gotten hung up on single sentences before. A founder has put their life’s work into a company, synoptically condensed it to a handful of slides, and I am stuck on eight words. But those eight words make no sense, and once something doesn’t make sense, the whole edifice of excitement and confidence comes crashing down. Eight words — one badly chosen verb and adjective.

A good pitch deck consultant may barely move the needle on a fundraise, while a superstar may not just get you a better term sheet, they may fundamentally transform the entire course of your startup’s trajectory. Those are the stakes.

And of course, it’s not just pitch deck consultants who can do this. The right PR consultants can potentially get you traction that no one else can. The right sales consultants may lock in those critical early design customers that represent the difference between an orderly liquidation and a massive Series A. The right product marketing specialists or pricing experts may be what drives conversions and eliminates churn.

What’s so hard today for founders is that the Valley has indeed matured, and all these consultants and more are available. There are the hucksters and the tricksters, the bon vivants thriving on naive capital, the idiot clowns cloaked in their own compelling pitch decks.

But as the market has expanded for these services, at least some superstars are emerging from the marketplace, people who can offer more value for you in a week or two than the mediocrities can in a year.

Your job as founder is to constantly probe and find those diamonds, and get them working on your idea at any cost — even costs that might at times seem insane.

The thing with tech startups today is that they are built upon strata of superstardom. Superstar talents lead to superstar products, superstar VC capital, and ultimately, superstar exits. Superstar momentum is real. Yes, yes, yes, not every time, and every stage in the pipeline is multiplied by a stochastic chance of failure, for sure. But idiocy has rarely been a path to success.

And so as with all parts of innovation, it’s all about making the right investments in the right people and the right ideas. $50K or even $500K for a consultant won’t do anything if they are the wrong person working on the wrong idea — parasites are parasites after all. But leverage that early seed capital into the right people working on the right problems, and that’s where the magic happens.

And so I can understand some of the outrage over these figures, as well as the lingering presumption behind them that VCs care more about a startup’s deck than the underlying startup itself. Those frustrations are palpable and not insane, but let’s not avoid the tough question: everything has some value attached to it. It shouldn’t surprise anyone that top experts in their fields, who understand their own leverage, would take advantage of their expertise and drive their own prices higher.

Paying tens of thousands of dollars for a pitch deck consultant isn’t a prerequisite for securing a venture capital round. There are founders whose entire skill is securing capital for their companies who have never paid a penny for this skill.

Yet ultimately, all early-stage startups face the same challenge: too many activities, too little time. Something, somewhere is going to have to get outsourced today and the quality of that external work is largely going to be determined by how much you are willing to pay for it. What you choose to spend whatever capital you have will determine the trajectory of your startup. So whether it is pitch decks or another activity, never blink from those top dollars. It may very well be what gets you the top dollar in the end.

Powered by WPeMatico