Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

Vimeo has raised $150 million in new equity funding, announced in conjunction with the third quarter earnings of its parent company IAC.

In a letter to shareholders, IAC CEO Joey Levin said the company has “begun contemplating spinning Vimeo off to our shareholders.”

“Given Vimeo’s success, and investor adulation for the Software-as-a-Service (SaaS) category generally, we expect Vimeo’s access to capital inside of IAC will be much more expensive than access to capital outside of IAC, and that capital will be helpful to enable Vimeo to achieve its highest ambitions,” Levin continued, adding, “We just tested Vimeo’s ability to access capital with a small private fundraise to bolster Vimeo’s balance sheet and to repay capital to IAC.”

Over the summer, Match Group (which owns a variety of dating services, including Tinder) completed its separation from IAC, with IAC’s ownership distributed to IAC shareholders.

Vimeo, meanwhile, has shifted its focus over the past couple years — instead of trying to compete with YouTube as a consumer video destination, it sells video tools to enterprises and other businesses. For example, it recently launched a free video messaging product called Vimeo Record.

The company says it has 1.5 million paying subscribers and more than 3,500 enterprise clients, including Amazon, Starbucks, Deloitte, Zendesk, Rite Aid and Siemens.

The new funding comes from Thrive Capital and GIC. According to the earnings report, in Q3, Vimeo grew revenue by 44% year-over-year, to $75.1 million. And it had its first quarter of positive EBITDA — $3.4 million.

“Our goal is to radically simplify how businesses create and share video, with tools that are far more intuitive and cost-effective than they’ve been historically,” said Vimeo CEO Anjali Sud in a statement. “We’re energized to access additional capital to pursue this enormous opportunity with the full focus and scale of the Vimeo platform.”

Powered by WPeMatico

No-code is the name of the game in enterprise software, and today a startup called Ushur that has built a platform for any business to create its own AI-based customer communication flows with no coding required is announcing some funding to help fuel its growth.

The startup has picked up $25 million in a Series B round of funding led by Third Point Ventures (the fund founded and led by activist investor and hedge fund supremo Daniel Loeb), with previous investor 8VC (Joe Lonsdale’s fund) also participating. It brings the total raised by Ushur to $36 million.

Ushur is not disclosing its valuation, but it’s growing fast. As a mark of how it is doing, the startup is currently focusing on the insurance sector (a big one when it comes to speaking with customers and amassing data during the conversation) and it counts Aetna, Irish Life, Tower Insurance and Unum among its customers building chatbots (dubbed Virtual Customer Assistants by Ushur), automated email response flows (branded SmartMail) and tools to help customer service agents serve people more quickly (FlowBuilder). It has APIs for those who need them, with integrations into Slack, ServiceNow, Salesforce and Jira, and works in 60 languages (not just English).

It’s now widening the net to also target financial services and telecoms companies, with the plan being to use the funding primarily to expand Ushur’s sales and marketing to keep growing its business after seeing a rise in demand during the COVID-19 pandemic, CEO and co-founder Simha Sadasiva said in an interview.

As companies — not just e-commerce or other online companies, but all companies — have turned to having more virtual interactions with their customers, solutions like Ushur’s have come into their own.

That’s been especially true for companies that are not “tech” at their core. They may lack the in-house talent and other resources to build and run tech-based services from the ground up, but at the same time also are looking for solutions that don’t involve the cost (and time) of working with third-party system integrators to implement them. This is the case, Sadasiva said, with RPA (robotic process automation) solutions, which he described as a competing approach that typically requires technical expertise or systems integrators to create and implement software.

Enter no-code: solutions — software platforms really — that are built with all the nitty gritty coding behind the scenes, and easy-to-use interfaces at the front for users to knit together programs, query databases and run calculations without needing to know how to do these at the coding level, at a typically lower cost.

“For every dollar you spend on RPA tool you have to spend $3-4 more to deploy it so we are very competitive,” Sadasiva said. One email service developed by Irish Life for its agents reduced typical enquiry processing times from between 3 hours – 2.5 days to “less than a second” with 40% fewer resources, the company claims.

To be clear, these are not off-the-shelf pieces of software, but flows that are customised by the customers based on what they need and then powered by natural language processing (which is also baked in behind the scenes).

“We have hundreds of templates already created,” Sadasiva said. “But the key thing is that they are like Lego pieces, or building blocks. We provide the assembly kit to make lots of new shapes and objects.”

Although there are a lot of companies marketing themselves as no-code and low-code, and indeed there is a big demand for more productivity and communication tools that don’t require you to be a programmer to use them but give you the flexibility of building what you need, not what a software company thinks you need, Ushur is finding a lot of traction with investors and customers.

“They’re right at the intersection of some of the biggest developments in enterprise software,” said Third Point Ventures Managing Partner Robert Schwartz in a statement. “Automation that feels personal yet delivers tremendous efficiencies to the enterprise. No-code design that allows customers to get to deployment and benefit easily and incredibly fast. Customer experiences that actually favor the customer. And they’re doing an incredible job with execution.”

Powered by WPeMatico

Yes, there is an election, but that’s getting pretty boring at this point. What’s far more interesting is the future of enterprise and cybersecurity startups, markets where companies are dumping billions of dollars in the wake of the largest change in office work in decades. Old notions are being discarded, new ideas are in — and all that portends huge potential opportunities for ambitious founders.

That’s why I am so excited to be hosting the next edition of our Extra Crunch Live interview series with the superlative enterprise venture capitalist Asheem Chandna of Greylock. We’re live in about two hours today at 3 p.m. EST/11 a.m. PST/8pm GMT. Details to join are below the fold, and if you don’t have an Extra Crunch membership, click through to signup in advance.

For nearly two decades, Asheem Chandna has been investing in enterprise and security startups at Greylock, with massive investment wins in Palo Alto Networks, AppDynamics and Sumo Logic. These days, he continues to invest in cybersecurity with companies like Awake Security and Abnormal Security, data platforms like Rubrik and Delphix, and the stealthy search engine company Neeva. As a leading early-stage investor and mentor in the space, he’s seen a multitude of companies transition from inception to product-market fit to IPO.

We’re going to be talking about the current landscape for enterprise and cybersecurity startups and then also talk about company building in these contexts, an area that Chandna has been particularly focused over his career. Plus, as always with ECL, we’ll be taking questions from you, our always inquisitive audience.

So come prepared for a great conversation, and join us shortly for another ECL live broadcast.

Powered by WPeMatico

When Alibaba entered the cloud infrastructure market in earnest in 2015 it had ambitious goals, and it has been growing steadily. Today, the Chinese e-commerce giant announced quarterly cloud revenue of $2.194 billion. With that number, it has passed IBM’s $1.65 billion revenue result (according to Synergy Research market share numbers), a significant milestone.

But while $2 billion is a large figure, it’s one worth keeping in perspective. For example, Amazon announced $11.6 billion in cloud infrastructure revenue for its most recent quarter, while Microsoft’s Azure came in second place with $5.9 billion.

Google Cloud has held onto third place, as it has for as long as we’ve been covering the cloud infrastructure market. In its most recent numbers, Synergy pegged Google at 9% market share, or approximately $2.9 billion in revenue.

While Alibaba is still a fair bit behind Google, today’s numbers puts the company firmly in fourth place now, well ahead of IBM . It’s doubtful it could catch Google anytime soon, especially as the company has become more focused under CEO Thomas Kurian, but it is still fairly remarkable that it managed to pass IBM, a stalwart of enterprise computing for decades, as a relative newcomer to the space.

The 60% growth represented a slight increase from the previous quarter’s 59%, but basically means it held steady, something that’s not easy to do as a company reaches a certain revenue plateau. In its earnings call today, Daniel Zhang, chairman and CEO at Alibaba Group, said that in China, which remains the company’s primary market, digital transformation driven by the pandemic was a primary factor in keeping growth steady.

“Cloud is a fast-growing business. If you look at our revenue breakdown, obviously, cloud is enjoying a very, very fast growth. And what we see is that all the industries are in the process of digital transformation. And moving to the cloud is a very important step for the industries,” Zhang said in the call.

He believes eventually that most business will be done in the cloud, and the growth could continue for the medium term, as there are still many companies that haven’t made the switch yet, but will do so over time.

John Dinsdale, an analyst at Synergy Research, says that while China remains its primary market, the company does have a presence outside the country too, and can afford to play the long game in terms of the current geopolitical situation with trade tensions between the U.S. and China.

“Alibaba has already made some strides outside of China and Hong Kong. While the scale is rather small compared with its Chinese operations, Alibaba has established a data center and cloud presence in a range of countries, including six more APAC countries, U.S., U.K. and UAE. Among these, it is the market leader in both Indonesia and Malaysia,” Dinsdale told TechCrunch.

In its most recent data released a couple of weeks ago, prior to today’s numbers, Synergy broke down the market this way: “Amazon 33%, Microsoft 18%, Google 9%, Alibaba 5%, IBM 5%, Salesforce 3%, Tencent 2%, Oracle 2%, NTT 1%, SAP 1% – to the nearest percentage point.”

Powered by WPeMatico

The race is on to build more efficient chip technology for faster and less power-intensive computing, and today an innovative startup that’s built one solution based on in-package optical interconnect (optical I/O) technology is announcing a round of growth funding from a number of strategic investors that speaks to how its approach is getting traction.

Ayar Labs, which makes chip solutions based on optical networking principals — architecture that promises both faster computing speeds and far less power consumption (and heat) in the process — has picked up $35 million in a Series B round of funding. Co-led by Downing Ventures and BlueSky Capital, the round also includes Applied Ventures (the VC arm of Applied Materials), Castor Ventures and SGInnovate (the Singaporean government’s deep tech fund), with participation also from existing investors Founders Fund, GLOBALFOUNDRIES, Intel Capital, Lockheed Martin Ventures and Playground Global.

Charles Wuischpard, CEO of Ayar Labs, style=”letter-spacing: -0.1px; font-size: 1.125rem;”> said that the funding will be used to continue developing its product as well as working on further commercialization. “The main application area for our technology is next-generation computing, anywhere that there is massive movement of data,” he said.

That includes aerospace and government applications, artificial intelligence and high-performance computing, telecoms and cloud applications, and lidar for self-driving car and other autonomous systems. Currently Wuischpard said that most of Ayar’s work is in the areas of AI and HPC — it’s a key partner of Intel’s in its work on AI computers for Darpa (see here and here) — and in telecoms/cloud.

Ayar’s focus on optical technology — specifically using silicon photonics and processing to build an optical communication device that can be built into a CPU — is emerging as a key area for chipmakers. Just last week, Marvell announced that it would buy Inphi, an optical networking specialist, for $10 billion.

As Wuischpard describes it, the big breakthrough that Ayar has brought to bear has been bringing down the size and scale of the technology to work within a computer’s core chip architecture, its CPU, which impacts and controls memory, control unit and processing/logic, helping to speed up computing for the most demanding applications.

(The company was co-founded by Mark Wade, Chen Sun, Vladimir Stojanovic and Alexandra Wright-Gladstein based on work at MIT, and they brought in Wuischpard, an engineer by training and also a veteran exec from Intel, to help figure out how to build a commercialised business around that.)

“Optics has been around for a long time,” he points out, first in subsea cabling, then between data centers and then inside the data center. “We think of ourselves as the last or first mile, bringing optical tech into the CPU.”

As he describes it, the company has devised a new type of modulator to turn electrons into photons, a “microing modulator” as he calls it. “There have been 1,000 research papers on this, but it’s typically difficult to manufacture and operate over a wide range of temperatures, and this is where a lot of our patents come in, to develop that into a single chiplet,” he said. The amount of bandwidth the tech can handle, 2 terabits/second, “would fill a whole server, but we are doing it in 5×9 millimeters.”

He adds that the opportunities here are such that there are others also working on the same kind of technology. “There are bigger companies and one or two smaller ones, but they are all still a couple of years behind us in commercialization,” he said. “It’s one thing to build one, versus a million.” Having GLOBALFOUNDRIES as an investor — it’s also fabricating hardware for Ayar — is key in this regard.

The company seems like it would be a key acquisition target, I pointed out, not least because of the race for having ownership of technology that can give a company a leading edge over another, but also because of the trend of consolidation in the chip industry. (Intel’s acquisition of Habana Labs also underscores the interest it has in optical tech.)

Wuischpard laughs a little ironically and says that COVID-19 has been a “help” in this regard: acquisitions have slowed down, giving the startup more time and less pressure to sell up.

“Ayar Labs represents the future of interconnects which have eventual applicability to every electronic device on earth”, said Warren Rogers, partner and head of Ventures at Downing Ventures, in a statement. “We have the highest confidence that when their optical I/O technology is applied to computing, the industry will finally break away from Moore’s Law and redefine the boundaries of computing.”

“We’ve been an investor in Ayar Labs since the beginning and have been looking for opportunities to increase our ownership in the company” added Madison Hamman, managing director of BlueSky Capital. “We are very excited about Ayar Labs and believe in their patented technology and execution of a plan that makes it a core building block of future computing systems.”

Powered by WPeMatico

Intel continues to snap up startups to build out its machine learning and AI operations. In the latest move, TechCrunch has learned that the chip giant has acquired Cnvrg.io, an Israeli company that has built and operates a platform for data scientists to build and run machine learning models, which can be used to train and track multiple models and run comparisons on them, build recommendations and more.

Intel confirmed the acquisition to us with a short note. “We can confirm that we have acquired Cnvrg,” a spokesperson said. “Cnvrg will be an independent Intel company and will continue to serve its existing and future customers.” Those customers include Lightricks, ST Unitas and Playtika.

Intel is not disclosing any financial terms of the deal, nor who from the startup will join Intel. Cnvrg, co-founded by Yochay Ettun (CEO) and Leah Forkosh Kolben, had raised $8 million from investors that include Hanaco Venture Capital and Jerusalem Venture Partners and PitchBook estimates that it was valued at around $17 million in its last round.

It was only a week ago that Intel made another acquisition to boost its AI business, also in the area of machine learning modeling: it picked up SigOpt, which had developed an optimization platform to run machine learning modeling and simulations.

While SigOpt is based out of the Bay Area, Cnvrg is in Israel and joins an extensive footprint that Intel has built in the country specifically in the area of artificial intelligence research and development, banked around its Mobileye autonomous vehicle business (which it acquired for more than $15 billion in 2017) and its acquisition of AI chipmaker Habana (which it acquired for $2 billion at the end of 2019).

Cnvrg.io’s platform works across on-premise, cloud and hybrid environments and it comes in paid and free tiers (we covered the launch of the free service, branded Core, last year). It competes with the likes of Databricks, Sagemaker and Dataiku as well as smaller operations like H2O.ai that are built on open source frameworks.

While Intel is not saying much about the deal, it seems that some of the same logic behind last week’s SigOpt acquisition applies here as well: Intel has been refocusing its business around next-generation chips to better compete against the likes of Nvidia and smaller players like GraphCore. So it makes sense to also provide/invest in AI tools for customers, specifically services to help with the compute loads that they will be running on those chips.

It’s notable that in our article about the Core free tier last year, Frederic noted that those using the platform in the cloud can do so with Nvidia-optimized containers that run on a Kubernetes cluster. It’s not clear if that will continue to be the case, or if containers will be optimized instead for Intel architecture, or both. Cnvrg’s other partners include Red Hat and NetApp.

Intel’s focus on the next generation of computing aims to offset declines in its legacy operations. In the last quarter, Intel reported a 3% decline in its revenues, led by a drop in its data center business. It said that it’s projecting the AI silicon market to be bigger than $25 billion by 2024, with AI silicon in the data center to be greater than $10 billion in that period.

In 2019, Intel reported some $3.8 billion in AI-driven revenue, but it hopes that tools like SigOpt’s will help drive more activity in that business, dovetailing with the push for more AI applications in a wider range of businesses.

Powered by WPeMatico

When Quibi announced it was shutting its doors recently after raising $1.75 billion, it begged an obvious question: If the original idea didn’t work, why not adjust its model or do something completely different while it still had capital? It wouldn’t have been the first company to decide to shift gears. Perhaps because of the unusually large amount of money it burned through in just six months of public operation, pivoting wasn’t an option for Quibi, but it has been for countless other successful companies over the years. Sometimes an original idea simply doesn’t pan out, a market gets too crowded or a company’s founders stumble onto something they have built that is actually a better business than the original idea.

There are many such examples:

These examples — and many more — show that when your first approach doesn’t work, pivoting may be the the only logical course, but it takes courage from founders and patience from investors.

We spoke to several founders and VCs who have been through this to find out how pivots happen, and how all the parties involved adjust to shifting priorities.

A big part of founding a company is having vision. You need to believe in your idea of course, but that doesn’t mean it’s the right way to go. Sometimes it pays to move on. The king of pivots might be the aptly named Pivotal, which changed direction several times and even swapped owners before it went public and got acquired, all in the span of about 20 years. Ed Sim, co-founder at boldstart ventures was part of Dawntreader Ventures in the late 90s when his firm invested in an early version of the company called Metapa. Sim had a front row seat to every twist and turn in the company’s long and intricate history.

“Greenplum, which was sold to EMC and eventually became Pivotal Software, was initially called Metapa. Metapa was in the Akamai space and as the markets cratered in 2001 for funding infrastructure projects, Scott Yara (the company’s founder) and team bought a small company called Didera and turned it into Greenplum, the first petabyte scale data warehouse built on top of open-source technology,” Sim told TechCrunch. It didn’t end there though as Sim continued, “Once again, years later, Scott recruited his replacement CEO, Bill Cook, and they paired together to sell Greenplum to EMC and eventually spin back out and take the company public as Pivotal Software.”

It’s worth noting that Pivotal eventually ran into financial problems when its stock tanked last year, but fellow Dell/EMC family member VMware saved the day by acquiring it for $2.7 billion.

Segment, the customer-data platform company that was recently sold to Twilio for $3.2 billion was originally a college lecture sentiment platform, according to CEO and co-founder Peter Reinhardt. “Our first idea was a classroom lecture tool, ClassMetric, which gave students a button they could press in class to let professors know, in real-time, that they were confused. I like to think of it like a pulse monitor for class confusion,” Reinhardt told TechCrunch

That idea quickly failed when professors testing it found that inviting students to open their laptops to test their sentiment just led them to start playing Solitaire or checking Facebook. Professors weren’t thrilled and they moved on. The founders, who were MIT students at the time, decided they wanted to build an analytics tool instead, but it turned out that competition from Google Analytics and Mixpanel at the time proved too steep.

“We spent a year on development, but it was a crowded market and we struggled to carve out our own niche. We were rapidly running out of capital and the pressure was on to find something new,” he said. They were actually considering simply packing it in, but they had developed a tiny open-source tool called analytics.js, which they used to get data into their failed analytics product. At that point, desperate for an idea, one of the founders suggested posting the open-source tool on Hacker News.

Powered by WPeMatico

Online education tools continue to see a surge of interest boosted by major changes in work and learning practices in the midst of a global health pandemic. And today, one of the early pioneers of the medium is announcing some funding as it tips into profitability on the back of a pivot to enterprise services, targeting businesses and governments that are looking to upskill workers to give them tech expertise more relevant to modern demands.

Udacity, which provides online courses and popularized the concept of “Nanodegrees” in tech-related subjects like artificial intelligence, programming, autonomous driving and cloud computing, has secured $75 million in the form of a debt facility. The funding will be used to continue investing in its platform to target more business customers.

Udacity said that part of the business is growing fast, with Q3 bookings up by 120% year-over-year and average run rates up 260% in H1 2020.

Udacity said that customers in the segment include “five of the world’s top seven aerospace companies, three of the Big Four professional services firms, the world’s leading pharmaceutical company, Egypt’s Information Technology Industry Development Agency, and three of the four branches of the United States Department of Defense”, which work with Udacity to build tailor-made courses for their specific needs, as well as use off-the-shelf content from its catalogue.

Udacity also works with companies to build programs as part of their CSR remits, and with tech companies like Microsoft to build programs to get more developers using their tools.

“We’re seeing tremendous demand on the enterprise and government side,” said Gabe Dalporto, Udacity’s CEO who joined the company in 2019. “But to date it’s mostly been inbound, with enterprises, Fortune 500 companies and government organizations coming in and wanting to work with us. Now it’s time to build out a sales team to go after them.”

The news today is a welcome turn of events for a company that has been in the spotlight over the years for less rosy reasons, partly because it found it challenging to land on a profitable business model.

Founded nearly a decade ago by three robotics specialists, including Sebastian Thrun, the Stanford professor who at the time was instrumental in building and running Google’s self-driving car and larger moonshot programs, Udacity initially saw an opportunity to partner with colleges and universities to build online tech courses (Thrun’s academic standing, and the vogue for MOOCs, were possibly two fillips for that strategy).

After that proved to be too challenging and costly, Udacity pivoted to positioning itself as a vocational learning provider targeting adults, specifically those who didn’t have the hours or money to embark on full-time courses but wanted to learn tech skills that could help them land better jobs.

That resulted in some substantial user growth, but still no profit. Eventually, the company faced multiple rounds of layoffs as it restructured and gravitated closer to its current form.

Currently, the company still provides direct-to-consumer (direct-to-learner?) courses, but it won’t be long, Dalporto said, before enterprise and government customers account for about 80% of the company’s business.

Previously, Udacity had raised nearly $170 million from a pretty illustrious group of investors that include Andreessen Horowitz, Ballie Gifford, CRV, Emerson Collective and more. This latest tranche is coming in the form of a debt facility from a single company, Hercules Capital.

Dalporto said the decision to take the debt route came after initially getting a number of term sheets for an equity round.

“We had multiple term sheets on the equity side, but then we received an unsolicited debt term sheet,” he said. That led to the company modelling out the cost of capital and dilution, he said, and “it turned out it was the better option.” For now, he added, equity was “off the table” but it may consider revisiting the idea en route to a public listing. “For the foreseeable future, we are cash flow positive so there is no compelling reason right now, but we might do something closer to an IPO.”

Being a debt facility, this funding does not mean a revisiting of Udacity’s valuation. The company was last capitalized five years ago at $1 billion, but Dalporto would not comment on how that had changed in the (uncompleted) equity term sheets it had received.

The interest Udacity is seeing — both from investors and as a company — is part of the bigger spotlight that online education companies have had in the last year. In K-12 and university education, the focus has been on building better technology and content to help students stay engaged and continue learning even when they cannot be in their normal physical classrooms as schools, districts, governments and public health officials implement social distancing to slow the spread of COVID-19.

But that’s not the only classroom where online education is getting called on. In the world of business, organizations that have also gone remote because of the pandemic are facing a matrix of challenges. How can they keep employees productive and feeling like part of a team when they no longer work next to each other? How do they make sure their workforces have the skills they need to work in the new environment? How do they make sure their own businesses are equipped with the right technology, and the expertise of people to run it, for this latest and future iterations of “work”? And how can governments make sure their economies don’t fall off a cliff as a result of the pandemic?

Online education has been seen as something of a panacea for all of these questions, and that has spelled a lot of opportunity for tech companies building online learning tools and other infrastructure — with others including the likes of Coursera, LinkedIn, Pluralsight, Treehouse and Springboard in the area of tech-related courses and learning platforms for workers.

As with other market segments like e-commerce, this isn’t about a trend emerging out of the blue, but about it accelerating much faster than people projected it would.

“Given Udacity’s growth, focus on sustainable business practices, and expanding reach across multiple industries, we are excited to provide this investment. We look forward to working with the company to help them sustain their impressive global growth, and continued innovation in upskilling and reskilling,” said Steve Kuo, senior MD and Technology Group head at Hercules Capital, in a statement.

In the areas of enterprise and government, Dalporto described a number of scenarios where Udacity is already active, which are natural progressions of the kind of vocational learning it was already offering.

They include, for example, the energy company Shell retraining structural and geological engineers “who had good math skills but no machine learning expertise” to be able to work in data science, needed as the company builds more automation into its operation and moves into new kinds of energy technology.

And he said that Egypt and other nations — looking to the success that India has had — have been providing technology expertise training to residents to help them find jobs in the “outsourcing economy.” He said that the program in Egypt has seen an 80% graduation rate and 70% “positive outcomes” (resulting in jobs).

“If you take just AI and machine learning, demand for these skills is growing at a rate of 70% year-over-year, but there is a shortage of talent to fill those roles,” Dalporto said.

Udacity is for now not looking at any acquisitions, he added, for another 6-12 months. “We have so much demand and work to do internally that there is no compelling reason to do that. At some point we will look at that but it needs to be linked to our strategy.”

Powered by WPeMatico

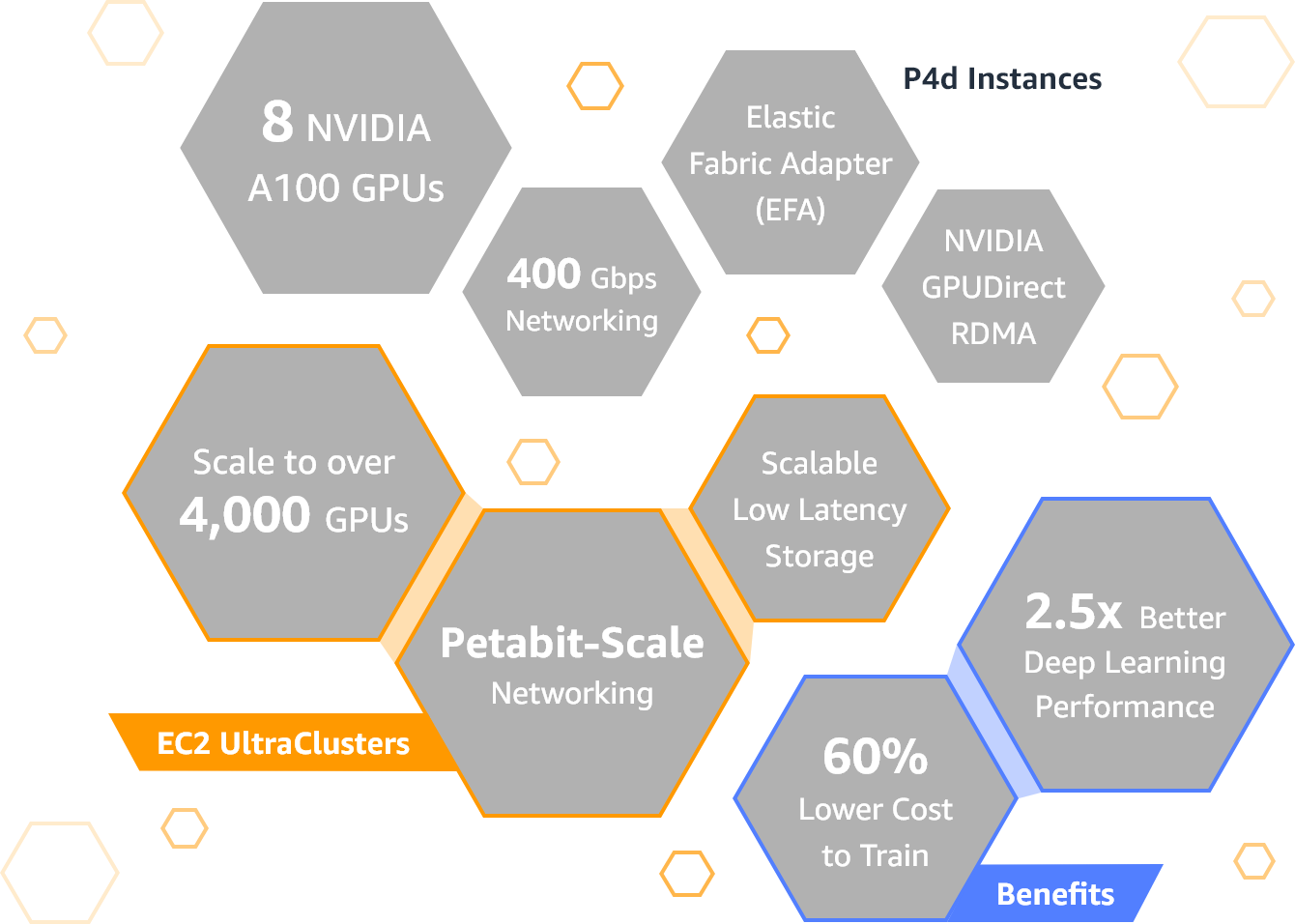

AWS today announced the launch of its newest GPU-equipped instances. Dubbed P4, these new instances are launching a decade after AWS launched its first set of Cluster GPU instances. This new generation is powered by Intel Cascade Lake processors and eight of Nvidia’s A100 Tensor Core GPUs. These instances, AWS promises, offer up to 2.5x the deep learning performance of the previous generation — and training a comparable model should be about 60% cheaper with these new instances.

Image Credits: AWS

For now, there is only one size available, the p4d.12xlarge instance, in AWS slang, and the eight A100 GPUs are connected over Nvidia’s NVLink communication interface and offer support for the company’s GPUDirect interface as well.

With 320 GB of high-bandwidth GPU memory and 400 Gbps networking, this is obviously a very powerful machine. Add to that the 96 CPU cores, 1.1 TB of system memory and 8 TB of SSD storage and it’s maybe no surprise that the on-demand price is $32.77 per hour (though that price goes down to less than $20/hour for one-year reserved instances and $11.57 for three-year reserved instances.

Image Credits: AWS

On the extreme end, you can combine 4,000 or more GPUs into an EC2 UltraCluster, as AWS calls these machines, for high-performance computing workloads at what is essentially a supercomputer-scale machine. Given the price, you’re not likely to spin up one of these clusters to train your model for your toy app anytime soon, but AWS has already been working with a number of enterprise customers to test these instances and clusters, including Toyota Research Institute, GE Healthcare and Aon.

“At [Toyota Research Institute], we’re working to build a future where everyone has the freedom to move,” said Mike Garrison, Technical Lead, Infrastructure Engineering at TRI. “The previous generation P3 instances helped us reduce our time to train machine learning models from days to hours and we are looking forward to utilizing P4d instances, as the additional GPU memory and more efficient float formats will allow our machine learning team to train with more complex models at an even faster speed.”

Powered by WPeMatico

Coupa Software, a publicly traded company that helps large corporations manage spending, announced that it was buying Llamasoft, an 18-year-old Michigan company that helps large companies manage their supply chain. The deal was pegged at $1.5 billion.

This year Llamasoft released its latest tool, an AI-driven platform for managing supply chains intelligently. This capability in particular seemed to attract Coupa’s attention, as it was looking for a supply chain application to complement its spend management capabilities.

Coupa CEO and chairman Rob Bernshteyn says when you combine that supply chain data with Coupa’s spending data, it can produce a powerful combination.

“Llamasoft’s deep supply chain expertise and sophisticated data science and modeling capabilities, combined with the roughly $2 trillion of cumulative transactional spend data we have in Coupa, will empower businesses with the intelligence needed to pivot on a dime,” Bernshteyn said in a statement.

The purchase comes at a time when companies are focusing more and more on digitizing processes across enterprise, and when supply chains can be uncertain, depending on the location of COVID hotspots at any particular time.

“With demand uncertainty on one hand, and supply volatility on the other, companies are in need of supply chain technology that can help them assess alternatives and balance trade-offs to achieve desired business results. LLamasoft provides these capabilities with an AI-powered cloud platform that empowers companies to make smarter supply chain decisions, faster,” the company wrote in a statement.

Llamasoft was founded in 2002 in Ann Arbor, Michigan and has raised more than $56 million, according to Crunchbase data. Its largest raise was a $50 million Series B in 2015 led by Goldman Sachs .

The company generated more than $100 million in revenue and has 650 big customers, including Boeing, DHL, Kimberly-Clark and GM, according to company data.

Coupa has been extremely acquisitive over the years, buying 17 companies, according to Crunchbase data. This deal represents the fourth acquisition this year for the company. So far the stock market is not enamored with the acquisition; the company’s stock price is down 5.20% at publication.

Powered by WPeMatico