Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

In 2017, Ironclad founder and CEO Jason Boehmig was looking to raise a Series A. As a former lawyer, Boehmig had a specific process for fundraising and an ultimate goal of finding the right investors for his company.

Part of Boehmig’s process was to ask people in the San Francisco Bay Area about their favorite place to work. Many praised RelateIQ, a company founded by Steve Loughlin who had sold it to Salesforce for $390 million and was brand new to venture at the time.

“I wanted to meet Steve and had kind of put two and two together,” said Boehmig. “I was like, ‘There’s this founder I’ve been meaning to connect with anyways, just to pick his brain, about how to build a great company, and he also just became an investor.’”

On this week’s Extra Crunch Live, the duo discussed how the Ironclad pitch excited Loughlin about leading the round. (So excited, in fact, he signed paperwork in the hospital on the same day his child was born.) They also discussed how they’ve managed to build trust by working through disagreements and the challenges of pricing and packaging enterprise products.

As with every episode of Extra Crunch Live, they also gave feedback on pitch decks submitted by the audience. (If you’d like to see your deck featured on a future episode, send it to us using this form.)

We record Extra Crunch Live every Wednesday at 12 p.m. PST/3 p.m. EST/8 p.m. GMT. You can see our past episodes here and check out the March slate right here.

When Boehmig came in to pitch Accel, Loughlin remembers feeling ambivalent. He had heard about the company and knew a former lawyer was coming in to pitch a legal tech company. He also trusted the reference who had introduced him to Boehmig, and thought, “I’ll take the meeting.”

Then, Boehmig dove into the pitch. The company had about a dozen customers that were excited about the product, and a few who were expanding use of the product across the organization, but it wasn’t until the ultimate vision of Ironclad was teased that Loughlin perked up.

Loughlin realized that the contract can be seen as a core object that could be used to collaborate horizontally across the enterprise.

“That was when the lightbulb went off and I realized this is actually much bigger,” said Loughlin. “This is not a legal tech company. This is core horizontal enterprise collaboration in one of the areas that has not been solved yet, where there is no great software yet for legal departments to collaborate with their counterparts.”

He listed all the software that those same counterparts had to let them collaborate: Salesforce, Marketo, Zendesk. Any investor would be excited to hear that a potential portfolio company could match the likes of those behemoths. Loughlin was hooked.

“There was a slide that I’m guessing Jason didn’t think much of, as it was just the data around the business, but I got pretty excited about it,” said Loughlin. “It said, for every legal user Ironclad added, they added nine other users from departments like sales, marketing, customer service, etc. It was evidence that this theory of collaboration could be true at scale.”

Powered by WPeMatico

SailPoint, an identity management company that went public in 2017, announced it was going to be acquiring Intello, an early-stage SaaS management startup. The two companies did not share the purchase price.

SailPoint believes that by helping its customers locate all of the SaaS tools being used inside a company, it can help IT make the company safer. Part of the problem is that it’s so easy for employees to deploy SaaS tools without IT’s knowledge, and Intello gives them more visibility and control.

In fact, the term “shadow IT” developed over the last decade to describe this ability to deploy software outside of the purview of IT pros. With a tool like Intello, they can now find all of the SaaS tools and point the employees to sanctioned ones, while shutting down services the security pros might not want folks using.

Grady Summers, EVP of product at SailPoint, says that this problem has become even more pronounced during the pandemic as many companies have gone remote, making it even more challenging for IT to understand what SaaS tools employees might be using.

“This has led to a sharp rise in ungoverned SaaS sprawl and unprotected data that is being stored and shared within these apps. With little to no visibility into what shadow access exists within their organization, IT teams are further challenged to protect from the cyber risks that have increased over the past year,” Summers explained in a statement. He believes that with Intello in the fold, it will help root out that unsanctioned usage and make companies safer, while also helping them understand their SaaS spend better.

Intello has always seen itself as a way to increase security and compliance and has partnered in the past with other identity management tools like Okta and OneLogin. The company was founded in 2017 and raised $5.8 million according to Crunchbase data. That included a $2.5 million extended seed in May 2019.

Yesterday, another SaaS management tool, Torii, announced a $10 million Series A. Other players in the SaaS management space include BetterCloud and Blissfully, among others.

Powered by WPeMatico

When Wendell Brooks stepped down as managing partner and head of Intel Capital last August, Anthony Lin was named to replace him on an interim basis. At the time, it wasn’t clear if he would be given the role permanently, but today, six months later, the answer is known.

In a letter to the firm’s portfolio CEOs published on the company website, Lin mentioned, almost casually, that he had taken on the two roles on a permanent basis. “Personally, I want to share that I have been appointed to managing partner and head of Intel Capital. I have been a member of the investment committee for the past several years and am humbly awed by the talent of our entrepreneurs and our team,” he wrote.

Lin takes over in a time of turmoil for Intel as the company struggles to regain its place in the semiconductor business that it dominated for decades. Meanwhile, Intel itself has a new CEO with Pat Gelsinger returning in January from VMware to lead the organization.

As the corporate investment arm of Intel, it looks for companies that can help the parent company understand where to invest resources in the future. If that is its goal, perhaps it hasn’t done a great job, as Intel has lost some of its edge when it comes to innovation.

Lin, who was formerly head of mergers and acquisitions and international investing at the firm, can use the power of the firm’s investment dollars to try to help point the parent company in the right direction and help find new ways to build innovative solutions on the Intel platform.

Lin acknowledged how challenging 2020 was for everyone, and his company was no exception, but the firm invested in 75 startups, including 35 new deals and 40 deals involving companies in which it had previously invested. It has also made a commitment to invest in companies with more diverse founders. To that end, 30% of new venture-stage dollars went to startups led by diverse leaders, according to Lin.

What’s more, the company made a five-year commitment that 15% of all its deals would go to companies with Black founders. It made some progress toward that goal, but there is still a ways to go. “At the end of 2020, 9% of our new venture deals and 15% of our venture dollars committed were in companies led by Black founders. We know there is more progress to be made and we will continue to encourage, foster and invest in diverse and inclusive teams,” he wrote.

Lin faces a big challenge ahead as he takes over a role that had the same leader for the first 28 years in Arvind Sodhani. His predecessor, Brooks, was there for five years. Now it passes to Lin, and he needs to use the firm’s investment might to help Gelsinger advance the goals of the broader firm, while making sound investments.

Powered by WPeMatico

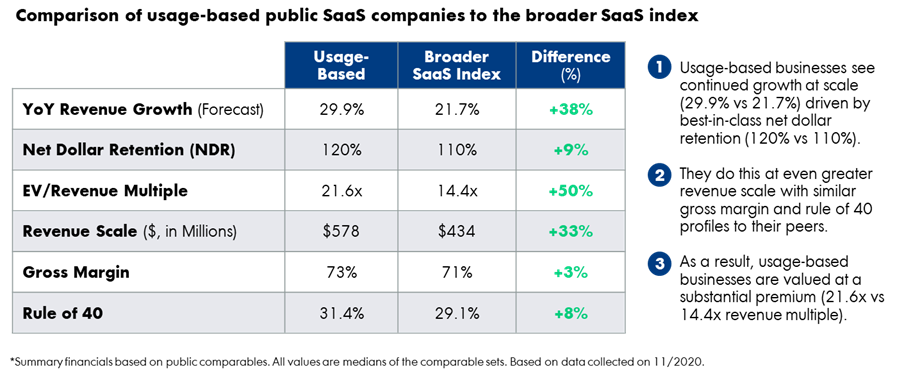

Today we know of HubSpot — the maker of marketing, sales and service software products — as a preeminent public company with a market cap above $17 billion. But HubSpot wasn’t always on the IPO trajectory.

For its first five years in business, HubSpot offered three subscription packages ranging in price from $3,000 to $18,000 per year. The company struggled with poor churn and anemic expansion revenue. Net revenue retention was near 70%, a far cry from the 100%+ that most SaaS companies aim to achieve.

Something needed to change. So in 2011, they introduced usage-based pricing. As customers used the software to generate more leads, they would proportionally increase their spend with HubSpot. This pricing change allowed HubSpot to share in the success of its customers.

In a usage-based model, expansion “just happens” as customers are successful.

By the time HubSpot went public in 2014, net revenue retention had jumped to nearly 100% — all without hurting the company’s ability to acquire new customers.

HubSpot isn’t an outlier. Public SaaS companies that have adopted usage-based pricing grow faster because they’re better at landing new customers, growing with them and keeping them as customers.

Image Credits: Kyle Poyar

In a usage-based model, a company doesn’t get paid until after the customer has adopted the product. From the customer’s perspective, this means that there’s no risk to try before they buy. Products like Snowflake and Google Cloud Platform take this a step further and even offer $300+ in free usage credits for new developers to test drive their products.

Many of these free users won’t become profitable — and that’s okay. Like a VC firm, usage-based companies are making a portfolio of bets. Some of those will pay off spectacularly — and the company will directly share in that success.

Top-performing companies open up the top of the funnel by making it free to sign up for their products. They invest in a frictionless customer onboarding experience and high-quality support so that new users get hooked on the platform. As more new users become active, there’s a stronger foundation for future customer growth.

Powered by WPeMatico

Census, a startup that helps businesses sync their customer data from their data warehouses to their various business tools like Salesforce and Marketo, today announced that it has raised a $16 million Series A round led by Sequoia Capital. Other participants in this round include Andreessen Horowitz, which led the company’s $4.3 million seed round last year, as well as several notable angles, including Figma CEO Dylan Field, GitHub CTO Jason Warner, Notion COO Akshay Kothari and Rippling CEO Parker Conrad.

The company is part of a new crop of startups that are building on top of data warehouses. The general idea behind Census is to help businesses operationalize the data in their data warehouses, which was traditionally only used for analytics and reporting use cases. But as businesses realized that all the data they needed was already available in their data warehouses and that they could use that as a single source of truth without having to build additional integrations, an ecosystem of companies that operationalize this data started to form.

The company argues that the modern data stack, with data warehouses like Amazon Redshift, Google BigQuery and Snowflake at its core, offers all of the tools a business needs to extract and transform data (like Fivetran, dbt) and then visualize it (think Looker).

Tools like Census then essentially function as a new layer that sits between the data warehouse and the business tools that can help companies extract value from this data. With that, users can easily sync their product data into a marketing tool like Marketo or a CRM service like Salesforce, for example.

Image Credits: Census

“Three years ago, we were the first to ask, ‘Why are we relying on a clumsy tangle of wires connecting every app when everything we need is already in the warehouse? What if you could leverage your data team to drive operations?’ When the data warehouse is connected to the rest of the business, the possibilities are limitless,” Census explains in today’s announcement. “When we launched, our focus was enabling product-led companies like Figma, Canva, and Notion to drive better marketing, sales, and customer success. Along the way, our customers have pulled Census into more and more scenarios, like auto-prioritizing support tickets in Zendesk, automating invoices in Netsuite, or even integrating with HR systems.“

Census already integrates with dozens of different services and data tools and its customers include the likes of Clearbit, Figma, Fivetran, LogDNA, Loom and Notion.

Looking ahead, Census plans to use the new funding to launch new features like deeper data validation and a visual query experience. In addition, it also plans to launch code-based orchestration to make Census workflows versionable and make it easier to integrate them into an enterprise orchestration system.

Powered by WPeMatico

A couple of weeks ago SentinelOne announced it was acquiring high-speed logging platform Scalyr for $155 million. Just this morning CrowdStrike struck next, announcing it was buying unlimited logging tool Humio for $400 million.

In Humio, CrowdStrike gets a company that will provide it with the ability to collect unlimited logging information. Most companies have to pick and choose what to log and how long to keep it, but with Humio, they don’t have to make these choices, with customers processing multiple terabytes of data every single day.

Humio CEO Geeta Schmidt writing in a company blog post announcing the deal described her company in similar terms to Scalyr, a data lake for log information:

“Humio had become the data lake for these enterprises enabling searches for longer periods of time and from more data sources allowing them to understand their entire environment, prepare for the unknown, proactively prevent issues, recover quickly from incidents, and get to the root cause,” she wrote.

That means with Humio in the fold, CrowdStrike can use this massive amount of data to help deal with threats and attacks in real time as they are happening, rather than reacting to them and trying to figure out what happened later, a point by the way that SentinelOne also made when it purchased Scalyr.

“The combination of real-time analytics and smart filtering built into CrowdStrike’s proprietary Threat Graph and Humio’s blazing-fast log management and index-free data ingestion dramatically accelerates our [eXtended Detection and Response (XDR)] capabilities beyond anything the market has seen to date,” CrowdStrike CEO and co-founder George Kurtz said in a statement.

While two acquisitions don’t necessarily make a trend, it’s clear that security platform players are suddenly seeing the value of being able to process the large amounts of information found in logs, and they are willing to put up some cash to get that capability. It will be interesting to see if any other security companies react with a similar move in the coming months.

Humio was founded in 2016 and raised just over $31 million, according to Pitchbook Data. Its most recent funding round came in March 2020, a $20 million Series B led by Dell Technologies Capital. It would appear to be a decent exit for the startup.

CrowdStrike was founded in 2011 and raised over $480 million before going public in 2019. The deal is expected to close in the first quarter, and is subject to typical regulatory oversight.

Powered by WPeMatico

The rise of “Zoom University” was only possible because edtech wasn’t ready to address the biggest opportunity of the past year: remote learning at scale. Of course, the term encapsulates more than just Zoom, it’s a nod to how schools had to rapidly adopt enterprise video conferencing software to keep school in session in the wake of closures brought on by the virus’ rapid spread.

Now, nearly a year since students were first sent home because of the coronavirus, a cohort of edtech companies is emerging, emboldened with millions in venture capital, ready to take back the market.

The new wave of startups are slicing and dicing the same market of students and teachers who are fatigued by Zoom University, which — at best — often looks like a gallery view with a chat bar. Four of the companies that are gaining traction include Class, Engageli, Top Hat and InSpace. It signals a shift from startups playing in the supplemental education space and searching to win a spot in the largest chunk of a students day: the classroom.

While each startup has its own unique strategy and product, the founders behind them all need to answer the same question: Can they make digital learning a preferred mode of pedagogy and comprehension — and not merely a backup — after the pandemic is over?

Answering that question begins with deciding whether videoconferencing is what online, live learning should look like.

“This is completely grounds up; there is no Zoom, Google Meets or Microsoft Teams anywhere in the vicinity,” said Dan Avida, co-founder of Engageli, just a few minutes into the demo of his product.

Engageli, a new startup founded by Avida, Daphne Koller, Jamie Nacht Farrell and Serge Plotkin, raised $14.5 million in October to bring digital learning to college universities. The startup wants to make big lecture-style classes feel more intimate, and thinks digitizing everything from the professor monologues to side conversations between students is the way to go.

Engageli is a videoconferencing platform in that it connects students and professors over live video, but the real product feature that differentiates it, according to Avida, is in how it views the virtual classroom.

Upon joining the platform, each student is placed at a virtual table with another small group of students. Within those pods, students can chat, trade notes, screenshot the lecture and collaborate, all while hearing a professor lecture simultaneously.

“The FaceTime session going on with friends or any other communication platform is going to happen,” Avida said. “So it might as well run it through our platform.”

The tables can easily be scrambled to promote different conversation or debates, and teachers can pop in and out without leaving their main screen. It’s a riff on Zoom’s breakout rooms, which let participants jump into separate calls within a bigger call.

There’s also a notetaking feature that allows students to screenshot slides and live annotate them within the Engageli platform. Each screenshot comes with a hyperlink that will take the student back to the live recording of that note, which could help with studying.

“We don’t want to be better than Zoom, we want to be different than Zoom,” Avida said. Engageli can run on a variety of products of differing bandwidth, from Chromebooks to iPads and PCs.

Engageli is feature-rich to the point that it has to onboard teachers, its main customer, in two phases, a process that can take over an hour. While Avida says that it only takes five minutes to figure out how to use the platform to hold a class, it does take longer to figure out how to fully take advantage of all the different modules. Teachers and students need to have some sort of digital savviness to be able to use the platform, which is both a barrier to entry for adoption but also a reason why Engageli can tout that it’s better than a simple call. Complexity, as Avida sees it, requires well-worth-it time.

The startup’s ambition doesn’t block it from dealing with contract issues. Other video conferencing platforms can afford to be free or already have been budgeted into. Engageli currently charges $9.99 or less per student seat for its platform. Avida says that with Zoom, “it’s effectively free because people have already paid for it, so we have to demonstrate why we’re much better than those products.”

Engageli’s biggest hurdle is another startup’s biggest advantage.

Class, launched less than a year ago by Blackboard co-founder Michael Chasen, integrates exclusively with Zoom to offer a more customized classroom for students and teachers alike. The product, currently in private paid beta, helps teachers launch live assignments, track attendance and understand student engagement levels in real time.

While positioning an entire business on Zoom could lead to platform risk, Chasen sees it as a competitive advantage that will help the startup stay relevant after the pandemic.

“We’re not really pitching it as pandemic-related,” Chasen said. “No school has only said that we’re going to plan to use this for a month, and very few K-12 schools say we’re only looking at this in case a pandemic comes again.” Chasen says that most beta customers say online learning will be part of their instructional strategy going forward.

Investors clearly see the opportunity in the company’s strategy, from distribution to execution. Earlier this month, Class announced it had raised $30 million in Series A financing, just 10 weeks after raising a $16 million seed round. Raising that much pre-launch gives the startup key wiggle room, but it also gives validation: a number of Zoom’s earliest investors, including Emergence Capital and Bill Tai, who wrote the first check into Zoom, have put money into Class.

“At Blackboard, we had a six to nine month sales cycle; we’d have to explain that e-learning is a thing,” Chasen said, who was at the LMS business for 15 years. “[With Class] we don’t even have to pitch. It wraps up in a month, and our sales cycle is just showing people the product.

Unlike Engageli, Class is selling to both K-12 institutions and higher-education institutions, which means its product is more focused on access and ease of use instead of specialized features. The startup has over 6,000 institutions, from high schools to higher education institutions, on the waitlist to join.

Image Credits: Class

Right now, Class software is only usable on Macs, but its beta will be available on iPhone, Windows and Android in the near future. The public launch is at the end of the quarter.

“K-12 is in a bigger bind,” he said, but higher-ed institutions are fully committed to using synchronous online learning for the “long haul.”

“Higher-ed has already been taking this step towards online learning, and they’re now taking the next step,” he said. “Whereas with a lot of K-12, I’m actually seeing that this is the first step that they’re taking.”

The big hurdle for Class, and any startup selling e-learning solutions to institutions, is post-pandemic utility. While institutions have traditionally been slow to adopt software due to red tape, Chasen says that both of Class’ customers, higher ed and K-12, are actively allocating budget for these tools. The price for Class ranges between $10,000 to $65,000 annually, depending on the number of students in the classes.

“We have not run into a budgeting problem in a single school,” he said. “Higher ed has already been taking this step towards online learning, and they’re now taking the next step, whereas K-12, this is the first step they’re taking.”

Engageli and Class are both trying to innovate on the live learning experience, but Top Hat, which raised $130 million in a Series E round this past week, thinks that the future is pre-recorded video.

Top Hat digitizes textbooks, but instead of putting a PDF on a screen, the startup fits features such as polls and interactive graphics in the text. The platform has attracted millions of students on this premise.

“We’re seeing a lot of companies putting emphasis on creating a virtual classroom,” he said. “But replicating the same thing in a different medium is never a good idea…nobody wants to stare at a screen and then have the restraint of having to show up at a previous pre-prescribed time.”

In July, Top Hat launched Community to give teachers a way to make class more than just a YouTube video. Similar to ClassDojo, Community provides a space for teachers and students to converse and stay up to date on shared materials. The interface also allows students to create private channels to discuss assignments and work on projects, as well as direct message their teachers.

CEO Mike Silagadze says that Top Hat tried a virtual classroom tool early on, and “very quickly learned that it was fundamentally just the wrong strategy.” His mindset contrasts with the demand that Class and Engageli have proven so far, to which Silagadze says might not be as long-term as they think.

“There’s definitely a lot of interest that’s generated in people signing up to beta lists and like wanting to try it out. But when people really get into it, everyone pretty much drops off and focuses more on asynchronous, small and in-person groups.”

Instead, the founder thinks that “schools are going to double down on the really valuable in-person aspects of higher education that they couldn’t provide before” and deliver other content, like large lecture-style classes or meetings, through asynchronous content delivery.

This is similar to what Jeff Maggioncalda, the CEO of Coursera, told TechCrunch in November: Colleges are going to re-invest in their in-person and residential experiences, and begin offering credentials and content online to fill in the gaps.

“We’ve been on the journey to create a more and more complete platform that our customers can use since almost day one,” Silagadze said. “What the pandemic has brought is much more comprehensive testing functionality that Top Hat has rolled out and better communication tooling so basically better chat and communication tooling for professors.”

TopHat costs $30 per semester, per student. Currently Top Hat has most of its paying customers coming in through its content offering, the digital textbooks, instead of this learning platform.

InSpace, a startup spinning out of Champlain college, is similarly focused on making the communication between professors and students more natural. Dr. Narine Hall, the founder of the startup, is a professor herself who just wanted class to “feel more natural” when it was being conducted.

InSpace is similar to some of the virtual HQ platforms that have popped up over the past few months. The platforms, which my colleague Devin Coldewey aptly dubbed Sims for Enterprise, are trying to create the feel of an office or classroom online but without a traditional gallery view or conference call vibe. The potential success of inSpace and others could signal how the future of work will blend gaming and socialization for distributed teams.

InSpace is using spatial gaming infrastructure to create spontaneity. The technology allows users to only hear people within their nearby proximity, and get quieter as they walk, or click, away. When applied to a virtual world, spatial technology can give the feeling of a hallway bump-in.

Similar to Engageli, inSpace is rethinking how an actual class is conducted. In inSpace, students don’t have to leave the main call to have a conversation during inSpace, which they do in Zoom. Students can just toggle over to their own areas and a professor can see teamwork being done in real time. When a student has a question, their bubble becomes bigger, which is easier to track than the hand-raise feature, says Hall.

InSpace has a different monetization strategy than other startups. It charges $15 a month per-educator or “host” versus per-student, which Hall says was so educators could close contracts “as fast as possible.” Hall agrees with other founders that schools have a high demand for the product, but she says that the decision-making process around buying new tooling continues to be difficult in schools with tight budgets, even amid a pandemic. There are currently 100 customers on the platform.

So far, Hall sees inSpace working best with classes that include 25 people, with a max of 50 people.

The company was born out of her own frustrations as a teacher. In grad school, Hall worked on research that combined proximity-based interactions with humans. When August rolled around and she needed a better solution than WebEx or Zoom, she turned to that same research and began building code atop of her teachings. It led to inSpace, which recently announced that it has landed $2.5 million in financing led by Boston Seed Capital.

The differences between each startup, from strategy to monetization to its view of the competition, are music to Zoom’s ears. Anne Keough Keehn, who was hired as Zoom’s Global Education Lead just nine months ago, says that the platform has a “very open attitude and policy about looking at how we best integrate…and sometimes that’s going to be a co-opetition.”

“In the past there has been too much consolidation and therefore it limits choices,” Keehn said. “And we know everybody in education likes to have choices.” Zoom will be used differently in a career office versus a class, and in a happy hour versus a wedding; the platform sees opportunity in it all beyond the “monolithic definition” that video-conferencing has had for so long.

And, despite the fact that this type of response is expected by a well-trained executive at a big company in the spotlight, maybe Keehn is onto something here: Maybe the biggest opportunity in edtech right now is that there is opportunity and money in the first place, for remote learning, for better video-conferencing and for more communication.

Editor’s note: A previous version of this story claims that TopHat’s community platform cost $30 per student, per month. TopHat has clarified since that the community platform is free, but its core product is sold for this cost. An update has been made to reflect this clarification.

Powered by WPeMatico

Today, that software is offered as a cloud service should be pretty much considered a given. Certainly any modern tooling is going to be SaaS, and as companies and employees add services, it becomes a management nightmare. Enter Torii, an early-stage startup that wants to make it easier to manage SaaS bloat.

Today, the company announced a $10 million Series A investment led by Wing Venture Capital, with participation from prior investors Entree Capital, Global Founders Capital, Scopus Ventures and Uncork Capital. The investment brings the total raised to $15 million, according to the company. Under the terms of the deal, Wing partner Jake Flomenberg is joining the board.

Uri Haramati, co-founder and CEO, is a serial entrepreneur who helped launch Houseparty and Meerkat. As a serial founder, he says that he and his co-founders saw firsthand how difficult it was to manage their companies’ SaaS applications, and the idea for Torii developed from that.

“We all felt the changes around SaaS and managing the tools that we were using. We were all early adopters of SaaS. We all [took advantage of SaaS] to scale our companies and we felt the same thing: The fact is that you just can’t add more people who manage more software, it just doesn’t scale,” Haramati told me.

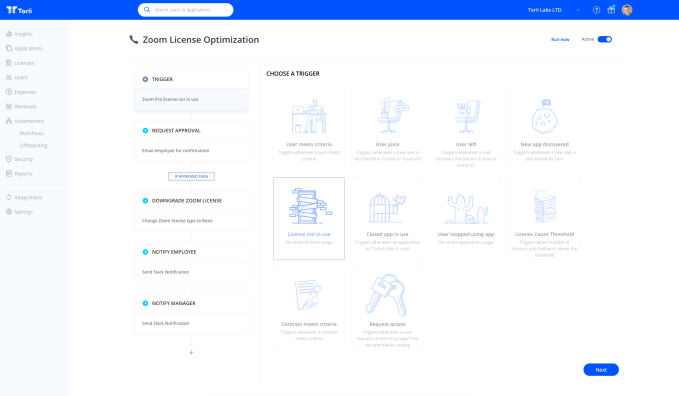

He said they started Torii with the idea of using software to control the SaaS sprawl they were experiencing. At the heart of the idea was an automation engine to discover and manage all of the SaaS tools inside an organization. Once you know what you have, there is a no-code workflow engine to create workflows around those tools for key activities like onboarding or offboarding employees.

Torii Workflow Engine. Image Credits: Torii

The approach seems to be working. As the pandemic struck in 2020, more companies than ever needed to control and understand the SaaS tooling they had, and revenue grew 400% YoY last year. Customers include Delivery Hero, Chewy, Monday.com and Palo Alto Networks.

The company also doubled its employees from a dozen with which they started last year, with plans to get to 60 people by the end of this year. As they do that, as experienced entrepreneurs, Haramati told me they already understood the value of developing a diverse and inclusive workforce, certainly around gender. Today, the team is 25 people with 10 being women and they are working to improve those ratios as they continue to add new people.

Flomenberg invested in Torii because he was particularly impressed with the automation aspect of the company and how it took a holistic approach to the SaaS management problem, rather than attempting to solve one part of it. “When I met Uri, he described this vision. It was really to become the operating system for SaaS. It all starts with the right data. You can trust data that is gathered from [multiple] sources to really build the right picture and pull it together. And then they took all those signals and they built a platform that is built on automation,” he said.

Haramati admits that it’s challenging to scale in the midst of a pandemic, but the company is growing and is already working to expand the platform to include product recommendations and help with compliance and cost control.

Powered by WPeMatico

The only people who truly understand a relationship are the ones who are in it. Luckily for us, we’re going to have a candid conversation with both parties in the relationship between Ironclad CEO and cofounder Jason Boehmig and his investor and board member Accel partner Steve Loughlin.

Loughlin led Ironclad’s Series A deal back in 2017, making it one of his first Series A deals after returning to Accel.

This episode of Extra Crunch Live goes down on Wednesday at 3pm ET/12pm PT, just like usual.

We’ll talk to the duo about how they met, what made them ‘choose’ each other, and how they’ve operated as a duo since. How they built trust, maintain honesty, and talk strategy are also on the table as part of the discussion.

Loughlin was an entrepreneur before he was an investor, founding RelateIQ (an Accel-backed company) in 2011. The company was acquired by Salesforce in 2014 for $390 million and later became Salesforce IQ. Loughlin then “came back home” to Accel in 2016, and has led investments in companies like Airkit, Ascend.io, Clockwise, Ironclad, Monte Carlo, Nines, Productiv, Split.io, and Vivun.

Not entirely unsurprising for a man who has dominated the legal tech sphere, Jason Boehmig is a California barred attorney who practiced law at Fenwick & West and was also an adjunct professor of law at Notre Dame Law School. Ironclad launched in 2014 and today the company has raised more than $180 million and, according to reports, is valued just under $1 billion.

Not only will we peel back the curtain on how this investor/founder relationship works, but we’ll also hear from these two tech leaders on their thoughts around bigger enterprise trends in the ecosystem.

Then, it’s time for the Pitch Deck Teardown. On each episode of Extra Crunch Live, we take a look at pitch decks submitted by the audience and our experienced guests give their live feedback. If you want to throw your hat pitch deck in the ring, you can hit this link to submit your deck for a future episode.

As with just about everything we do here at TechCrunch, audience members can also ask their own questions to our guests.

Extra Crunch Live has left room for you to network (you gotta network to get work, amirite?). Networking is open starting at 2:30pm ET/11:30am PT and stays open a half hour after the episode ends. Make a friend!

As a reminder, Extra Crunch Live is a members-only series that aims to give founders and tech operators actionable advice and insights from leaders across the tech industry. If you’re not an Extra Crunch member yet, what are you waiting for?

Loughlin and Boehmig join a stellar cast of speakers on Extra Crunch Live, including Lightspeed’s Gaurav Gupta and Grafana’s Raj Dutt, as well as Felicis’ Aydin Senkut and Guideline’s Kevin Busque. Extra Crunch members can catch every episode of Extra Crunch Live on demand right here.

You can find details for this episode (and upcoming episodes) after the jump below.

See you on Wednesday!

Powered by WPeMatico

Typically when we talk about tech and security, the mind naturally jumps to cybersecurity. But equally important, especially for global companies with large, multinational organizations, is physical security — a key function at most medium-to-large enterprises, and yet one that to date, hasn’t really done much to take advantage of recent advances in technology. Enter Base Operations, a startup founded by risk management professional Cory Siskind in 2018. Base Operations just closed their $2.2 million seed funding round and will use the money to capitalize on its recent launch of a street-level threat mapping platform for use in supporting enterprise security operations.

The funding, led by Good Growth Capital and including investors like Magma Partners, First In Capital, Gaingels and First Round Capital founder Howard Morgan, will be used primarily for hiring, as Base Operations looks to continue its team growth after doubling its employe base this past month. It’ll also be put to use extending and improving the company’s product and growing the startup’s global footprint. I talked to Siskind about her company’s plans on the heels of this round, as well as the wider opportunity and how her company is serving the market in a novel way.

“What we do at Base Operations is help companies keep their people in operation secure with ‘Micro Intelligence,’ which is street-level threat assessments that facilitate a variety of routine security tasks in the travel security, real estate and supply chain security buckets,” Siskind explained. “Anything that the chief security officer would be in charge of, but not cyber — so anything that intersects with the physical world.”

Siskind has firsthand experience about the complexity and challenges that enter into enterprise security since she began her career working for global strategic risk consultancy firm Control Risks in Mexico City. Because of her time in the industry, she’s keenly aware of just how far physical and political security operations lag behind their cybersecurity counterparts. It’s an often overlooked aspect of corporate risk management, particularly since in the past it’s been something that most employees at North American companies only ever encounter periodically when their roles involve frequent travel. The events of the past couple of years have changed that, however.

“This was the last bastion of a company that hadn’t been optimized by a SaaS platform, basically, so there was some resistance and some allegiance to legacy players,” Siskind told me. “However, the events of 2020 sort of turned everything on its head, and companies realized that the security department, and what happens in the physical world, is not just about compliance — it’s actually a strategic advantage to invest in those sort of services, because it helps you maintain business continuity.”

The COVID-19 pandemic, increased frequency and severity of natural disasters, and global political unrest all had significant impact on businesses worldwide in 2020, and Siskind says that this has proven a watershed moment in how enterprises consider physical security in their overall risk profile and strategic planning cycles.

“[Companies] have just realized that if you don’t invest [in] how to keep your operations running smoothly in the face of rising catastrophic events, you’re never going to achieve the profits that you need, because it’s too choppy, and you have all sorts of problems,” she said.

Base Operations addresses this problem by taking available data from a range of sources and pulling it together to inform threat profiles. Their technology is all about making sense of the myriad stream of information we encounter daily — taking the wash of news that we sometimes associate with “doom-scrolling” on social media, for instance, and combining it with other sources using machine learning to extrapolate actionable insights.

Those sources of information include “government statistics, social media, local news, data from partnerships, like NGOs and universities,” Siskind said. That data set powers their Micro Intelligence platform, and while the startup’s focus today is on helping enterprises keep people safe, while maintaining their operations, you can easily see how the same information could power everything from planning future geographical expansion, to tailoring product development to address specific markets.

Siskind saw there was a need for this kind of approach to an aspect of business that’s essential, but that has been relatively slow to adopt new technologies. From her vantage point two years ago, however, she couldn’t have anticipated just how urgent the need for better, more scalable enterprise security solutions would arise, and Base Operations now seems perfectly positioned to help with that need.

Powered by WPeMatico