Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Japanese startup FPV Robotics is leveraging drone technology to address a growing global need: inspecting aging infrastructure in an effort to avoid major issues like unexpected bridge collapses. FPV Robotics CEO and founder Masaki Komagata showed me his company’s production Waver drone, which is debuting for the first time ever at CES 2020 in Las Vegas this week.

Waver is an amphibious drone, which can fly thanks to eight rotors, and also speed along the surface of bodies of water using its floats. This dual nature makes it particularly well-suited to solving a very specific task — a problem Komagata set out specifically to solve after observing that Japan Railways (JR) needed this addressed.

This specific problem was rail bridge collapse, including damaged and destroyed bridges along the Tadami River in 2011 due to floods in Niigata and Fukushima. Many of the spans that JR relies upon for its Shinkansen and other local trains in Japan are considerably old, and beginning to show their age. That wear can be further exasperated by environmental disasters — which are occurring with greater frequency as a result of climate change.

FPV Robotics can’t magically repair this aging infrastructure or prevent natural disasters, but it can deliver on-demand, flexible monitoring and inspection at a greatly reduced cost compared to current methods. Komagata partnered with JR and with sensor company OKI on development of the Waver to custom-design it specifically for this use, which is where it got its amphibious abilities and attached multibeam sensor array.

This multibeam technology, provided by OKI, is installed on the bottom of the Waver drone and provides sonar imaging capabilities that allow the drone to accurately map the bottom of a river or seabed from the water’s surface. This information, Komagata tells me, can be used to help predict when infrastructure, including bridges and roads, might need to be replaced or reinforced, prior to any actual collapse or damage.

This multibeam technology, provided by OKI, is installed on the bottom of the Waver drone and provides sonar imaging capabilities that allow the drone to accurately map the bottom of a river or seabed from the water’s surface. This information, Komagata tells me, can be used to help predict when infrastructure, including bridges and roads, might need to be replaced or reinforced, prior to any actual collapse or damage.

Waver can autonomously map a predetermined section of riverbed, moving like a Roomba across the water in segment sweeps to build the full picture. It’s also equipped with eight rotors, more than your average VTOL drone, which Komagata tells me is for added redundancy so that it can continue to operate effectively even in the unlikely event that it loses power to multiple rotors at once.

In addition to the sea and river bed inspection, the Waver can do a visual inspection of the bridge itself from up close using a more traditional camera, as well as the supporting land from which it extends. Komagata points out that this kind of multi-part inspection can require specialized boats, many hours of trained personnel time, things like temporary scaffolding for a close-up eyes-on approach and a lot more. He estimates based on studies FPV has done that their drone could reduce inspection costs to as little as 1/20th the cost of existing methods. That means it would be possible to monitor much more frequently than can be done currently, and in circumstances where risk to human inspectors on the ground might be a necessary component of using more traditional means.

Waver estimates that just taking into account bridges alone, there’s a roughly $25 million per year total addressable market, and it’s aiming to acquire around 4% of that (roughly $1 million in revenue) in 2020, and then to grow that by about $2 million per year in the next two fiscal years. It’s currently mostly bootstrapped, with 90% of the startup’s existing ¥30,700,000 ($300,000) in seed funding coming from Komagata himself. With that capital, the company has already gone from working prototype (which you can see in the GIF above) to the much more polished production version debuted at CES.

Komagata, an engineer with a focus in drone development, envisions Waver being able to address challenges with aging infrastructure not just in Japan, but globally, though FPV’s initial focus is on the market opportunity at home. Ultimately, he hopes that Waver and other drone technology FPV Robotics brings to market helps to “make the world a better place,” and addressing challenges like infrastructure inspection is definitely a good place to start.

Powered by WPeMatico

Weber is deepening its partnership with smart cooking startup June, with a new product debuting at CES 2020 today that can turn any grill into a smart grill — and providing expert guidance and grilling advice to even novice home cooks.

The new Weber Connect Smart Grilling Hub includes a small device with ports for connecting wired thermometers that you can use to monitor the temperature of your meats or other foods as they cook. The Hub supports use of up to four temperature sensors at once, so you can monitor the temperature of different dishes all at the same time; you connect to the hub with your smartphone via Weber’s dedicated app to receive up-to-date info about the current internal temperature of whatever you’re cooking. The app will alert you when your meats reach the proper temperature for whatever level of doneness you’re shooting for.

The app also provides step-by-step cooking instructions, notifications for things like when it’s time to flip food if that’s part of the cooking process and tips and tricks culled from actual expert grillers about how best to cook your stuff. Weber also says it plans to add Alexa support to the Hub later in the year, as well as provide other new features via software updates.

The app also provides step-by-step cooking instructions, notifications for things like when it’s time to flip food if that’s part of the cooking process and tips and tricks culled from actual expert grillers about how best to cook your stuff. Weber also says it plans to add Alexa support to the Hub later in the year, as well as provide other new features via software updates.

Weber previously partnered with June on their forthcoming Weber SmokeFire pellet grill, the first pellet grill made by Weber, which also has smart cooking technology similar to what the Smart Grilling Hub provides, but built-in.

The Smart Grilling Hub will launch in more than 30 countries initially starting in “early 2020,” and will sell for $129.99 in the U.S.

Powered by WPeMatico

CES is a magical place full of gizmos, gadgets and communicable diseases.

TechCrunch is hosting another pitch-off event this year. Called Pitch Night, select early-stage companies will take the stage and have 60 seconds to present their wares to TechCrunch editorial and industry experts.

This event is free. Obtain a ticket here. Want to pitch at the event? Apply below.

This Vegas Pitch Night isn’t a polished show with massive screens, celebrity guests and life-changing cash prizes. This event is quick and efficient, held in a co-working event space outside of downtown Vegas. There will be coolers of beer, sodas and whatever snacks we can find at a 7-Eleven.

We’ve held these events for years and they’re among our favorite to host. There are countless startups in town for CES and we just want to hang out away from the noise of the Vegas strip.

Space is very limited. Register as soon as possible.

Loading…

Powered by WPeMatico

Almost exactly 4 months to the day after BigID announced a $50 million Series C, the company was back today with another $50 million round. The Series C extension came entirely from Tiger Global Management. The company has raised a total of $144 million.

What warrants $100 million in interest from investors in just four months is BigID’s mission to understand the data a company has and manage that in the context of increasing privacy regulation including GDPR in Europe and CCPA in California, which went into effect this month.

BigID CEO and co-founder Dimitri Sirota admits that his company formed at the right moment when it launched in 2016, but says he and his co-founders had an inkling that there would be a shift in how governments view data privacy.

“Fortunately for us, some of the requirements that we said were going to be critical, like being able to understand what data you collect on each individual across your entire data landscape, have come to [pass],” Sirota told TechCrunch. While he understands that there are lots of competing companies going after this market, he believes that being early helped his startup establish a brand identity earlier than most.

Meanwhile, the privacy regulation landscape continues to evolve. Even as California privacy legislation is taking effect, many other states and countries are looking at similar regulations. Canada is looking at overhauling its existing privacy regulations.

Sirota says that he wasn’t actually looking to raise either the C or the D, and in fact still has B money in the bank, but when big investors want to give you money on decent terms, you take it while the money is there. These investors clearly see the data privacy landscape expanding and want to get involved. He recognizes that economic conditions can change quickly, and it can’t hurt to have money in the bank for when that happens.

That said, Sirota says you don’t raise money to keep it in the bank. At some point, you put it to work. The company has big plans to expand beyond its privacy roots and into other areas of security in the coming year. Although he wouldn’t go into too much detail about that, he said to expect some announcements soon.

For a company that is only four years old, it has been amazingly proficient at raising money with a $14 million Series A and a $30 million Series B in 2018, followed by the $50 million Series C last year, and the $50 million round today. And Sirota said, he didn’t have to even go looking for the latest funding. Investors came to him — no trips to Sand Hill Road, no pitch decks. Sirota wasn’t willing to discuss the company’s valuation, only saying the investment was minimally diluted.

BigID, which is based in New York City, already has some employees in Europe and Asia, but he expects additional international expansion in 2020. Overall the company has around 165 employees at the moment and he sees that going up to 200 by mid-year as they make a push into some new adjacencies.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

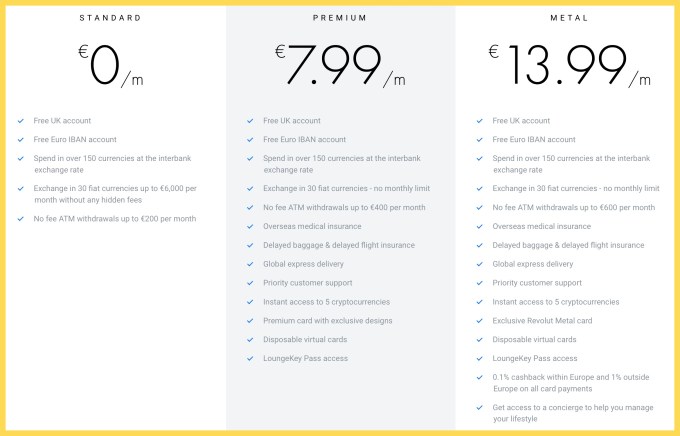

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

One Medical, a San Francisco-based primary care startup with tech-infused, concierge services filed for an IPO with the Securities and Exchange Commission today.

Internal medicine doctor Tom Lee founded the startup, now valued at well-over $1 billion dollars, in 2007. Lee exited his company in 2017, leaving it in the hands of former UnitedHealth group executive Amir Rubin.

The startup currently operates 72 health clinics in nine major cities throughout the U.S., with three more markets expected to open in 2020 and has raised just over $500 in venture capital from it’s biggest investor, the Carlyle Group (which owns just over a quarter of shares), Alphabet’s GV, J.P. Morgan and others. Google also incorporates One Medical into its campuses and accounts for about 10% of the company revenue, according to the SEC filing. The filing also mentions the company, which is officially incorporated as 1Life Healthcare Inc. ONEM, now plans to raise about $100 million.

Presumably, this money will help the company improve upon its technology and expand to more markets. We’ve reached out to One Medical for more and so far have only been referred to its wire statement.

According to that statement, One Medical has applied for a listing as ticker symbol, ONEM under its common stock on the Nasdaq Global Select Market.

Powered by WPeMatico

The world’s forests are ablaze, under threat from illegal logging and disappearing due to the less dramatic environmental degradation wrought by drought and other signs of climate change.

It’s part of the negative feedback loop that seems to be accelerating climate change as greenhouse gases accumulate in the atmosphere, but one startup company is trying to facilitate reforestation by supporting carbon offsets that specifically target the world’s flora.

Pachama has raised $4.1 million to create a marketplace where companies can support carbon offset projects. The company is backed by some big names in tech investment, like former Uber executive Ryan Graves, through his private investment firm, Saltwater, and Chris Sacca, a prominent early investor in Uber, through his Lowercase Capital firm.

Founded by Diego Saez-Gil, a serial entrepreneur whose last company was a startup selling a “smart-suitcase,” Pachama is aiming to bring reforestation projects to the carbon markets whose impacts can be independently verified by the company’s monitoring software to ensure their ability to offset emissions.

“We were making a smart connected suitcase which got banned,” says Saez-Gil. “After that I decided to take some time off and I was quite burnt out. I wanted to do some soul searching and tried to decide what I wanted to put my efforts [into].”

He traveled to South America and did a trip through the Amazon rain forest in Peru. It was there that Saez-Gil saw the effects of deforestation in an area that represents a huge carbon dioxide offset for the planet.

“There are about 1 billion hectares on the planet that could be reforested,” says Saez-Gil.

That opportunity — to contribute to the perpetuation of independently validated carbon markets around the world — is what convinced investors like Paul Graham, Justin Kan, Daniel Kan, Gustaf Alströmer, Peter Reinhardt, Jason Jacobs and Chris Sacca from Lowercase Capital, as well as funds such as Social+Capital, Global Founders Capital and Atomico, to contribute to the company’s $4.1 million funding.

It’s a pretty big consortium to finance what amounts to a small capital commitment (given the size of the funds under management that these investors have at their disposal), but investors are right to be a little wary.

Carbon markets are driven by policy, and policymakers have been reluctant to draft legislation that would put a high enough price on carbon emissions to make those markets viable.

“Pachama’s carbon credit marketplace is launching at a pivotal moment when awareness of the climate crisis is reaching an all-time high, and businesses are increasingly looking to become carbon neutral,” said Ryan Graves, Pachama’s lead investor and new director said in a statement. “What attracted me to Pachama was the company’s use of technology to bring trust to an industry that desperately needs it, and gives the verifiable results to the purchasers of carbon credits.”

Awareness doesn’t equal political action, however, and Pachama needs the political will of both governments and consumers to move the needle on creating viable carbon trading markets.

Pachama’s business becomes profitable only when the price of carbon moves beyond $15 per ton of carbon dioxide (or similar emissions) offset. Currently, there are only two markets in the world where that threshold has been reached — the California market and Europe, according to Saez-Gil.

For Pachama’s founder, forest preservation and reforestation projects can have outsized benefits. “There are only 500 forest projects that are certified today… we need tens of thousands,” says Saez-Gil. “There are one billion hectares on the planet available for reforestation without competing with agriculture.”

The restoration of native forests can contribute to replenishing global biodiversity, and captures more carbon than cultivating forests for industrial use, but both are better than destruction to grow row crops or support animal husbandry, Saez-Gil says.

Pachama sources projects that are approved by existing certification bodies, but offers its customers monitoring and management services through access to satellite imagery and sensors that provide information on emissions and carbon capture on reforested land.

It’s a potential solution to the problem of deforestation that’s plaguing countries like Brazil. “The government in Brazil, they want to generate income for the country,” says Saez-Gil. If carbon markets paid as much as ranching, it would reduce the need for animal husbandry and plantation farming in Brazil, Indonesia or places like Peru.

Today, most investments in reforestation projects are done through middlemen, which increases opacity and the chance that projects are being double-counted or sold, according to Saez-Gil. Pachama has a person who is contacting forest project developers so that they can list the projects independently. Then the company verifies the offsets with satellite imaging systems.

The company currently has 23 forest projects — three in the Amazon rain forest in Brazil and Peru and projects in the U.S. in California, Vermont, New Jersey, Connecticut and Maine .

Saez-Gil has high hopes for the future of carbon markets based on demand coming, in part, from new regulations like those imposed on the airline industry.

“Airlines will have to offset part of their emissions as part of CORSIA,” says Saez-gil. That’s an offset of 160 million tons of emission per year. “There is all this demand coming for different offsets for different markets that will make the price go up.”

Powered by WPeMatico

Pitch the wrong reporter or publication, and your story won’t see the light of day.

Before you start seeking press, you’ll need to look for reporters who have reach, respect and expertise when you choose who to talk to. You’ll also need to be prepared to accept the truth about your business, even if it hurts. It’s critical that you find a writer who’s a good fit for the business you’re building and the audience you’re seeking.

If you don’t use a strategic approach when reaching out to journalists, you’ll get few responses, fewer meetings, and articles that either misrepresent you, shortchange you, or blow up in your face. The goal isn’t just to secure positive coverage, because no one will believe it; startups are tough. There are challenges and setbacks and scary looming questions. But an honest article from a respected voice with a big enough audience can legitimize a business as it tries to turn vision into impact.

Here we’ll discuss how to find the publication and reporter who understands you and can tell the story that aligns with your objectives. In part one of this series, we detailed why you should (or shouldn’t) want press coverage and how to know what’s newsworthy enough to pitch.

In future ExtraCrunch posts, I’ll explore how to hire PR help, formulate a pitch, deliver it to reporters, prepare for interviews and conduct an announcement. If you have more questions or ideas for ExtraCrunch posts, feel free to reach out to me via Twitter or elsewhere.

Why should you believe me? I’m editor-at-large for TechCrunch, where I’ve written 4,000 articles about early-stage startups and tech giants. For 10 years, I’ve reviewed startup pitches via email and Twitter, at demo days for accelerators like Y Combinator and on stage as a judge of startup competitions. From warm introductions to cold calls, I’ve seen what gets reporters’ attention and why stories become enduring narratives supporting companies as they grow.

Which publications do you currently read and respect?

Starting here ensures that you’re approaching PR from a place of knowledge with personal context rather than going by what someone else tells you. But you also have to consider which publications appeal in that way to your target demographic. For example, if you’re aiming to reach teens, parents, or Chief Information Officers, you’ll have very different target publications.

If you appeal to a niche audience aligned with a specific publication, you can definitely score some leads and installs, priming the pump so when users hear about you again, they already have a positive association for your brand. You can score SEO to help your get discovered when people search for keywords related to your business, but if you’re looking for user growth or SEO, be sure to work with a publication that links to the websites and apps they write about, as many don’t. But if you’re hoping for ‘the servers are on fire we’ve got so much traffic’ attention, you need to first build network effects and viral loops directly into your product.

Once you identify a realistic objective for gaining press coverage, you can figure out which reporters and outlets will best help you achieve your goals.

Typically, you’ll aim to work with more prestigious publications and writers first, as they can inspire other outlets to write up follow-on coverage. It rarely works the other way around, since top publishers want to be seen as first to a story and forging trends rather than following them with late coverage. These outlets often have greater reach in terms of home page traffic, social following, SEO and shareability.

The exception to this strategy: if there’s a specific writer at a less-prestigious publisher who’s renowned as the expert in your space whose word has more weight, or if that publication better aligns with your overall goals. For example, you might want to work with a transportation expert like Kirsten Korosec if you’re an electric car company, or a publication focused on startups like TechCrunch if you’re trying to stoke fundraising. If you’re a more general mainstream consumer business or are seeking maximum growth, you might instead choose a popular national newspaper with a big circulation.

After you’ve set goals and have an idea regarding the kind of publication or journalist you want to work with, it’s time to build a ranked list of specific reporters. Here, expertise is key.

Powered by WPeMatico

Trussle, the online mortgage broker backed by the likes of Goldman Sachs, LocalGlobe, Finch Capital and Seedcamp, has lost its founding CEO.

Ishaan Malhi, who co-founded the fintech startup five years ago, has resigned with “immediate effect,” according to a rather brief press release issued by Trussle this morning.

The company is now searching for Malhi’s replacement and in the interim says it will be led by Chairman Simon Williams and others in the senior leadership team. “Williams will be supported by co-founder Jonathan Galore who helped establish Trussle in 2015 and remains closely involved in the business,” reads the press release.

Williams joined Trussle’s board in April 2019, and has had a long stint in financial services. He spent nine years at Citigroup, heading up its International Retail Bank, and more recently served as head of HSBC’s Wealth Management group until 2014.

Meanwhile, the departure of Malhi seems rather abrupt, not least as he doesn’t appear to be involved in the recruitment of his successor. As well as resigning from the role of CEO, the Trussle co-founder has resigned from the startup’s board.

Trussle itself declined to provide further detail, with a spokesperson for the company advising that any questions with regards to why Malhi has resigned should be put to him. I pinged Malhi for comment but he declined to take my call having committed to spending the day with family.

However, he did give a statement to The Telegraph newspaper, telling reporter James Cook: “it was my decision to step down.”

More broadly, the story appears to be being spun as a young first-time founder growing a business to a size where more experienced leadership is needed to take it to the next stage. And it’s certainly true that the company has been staffing up in recent months, growing to 120 staff members (as of late November 2019) and bolstering the leadership team.

Along with Williams, Trussle announced in November that it had recruited ex-Wallaby Financial co-founder Todd Zino as CTO, and ex-head of Zoopla content strategy Sebastian Anthony as head of Organic Growth and Product Manager.

At the time of the announcement, Malhi said in a statement that “culture remains to be our competitive advantage” — a culture that has since seen its founding CEO depart abruptly before a replacement has been found.

Although, as one person with inside knowledge of Malhi’s departure framed it, Trussle has been attempting to diversify the startup’s leadership team for a while now and make the company “less of a one-man show.”

What’s also clear is that the online mortgage broker space is a tough one and pretty capital-intensive due to high customer acquisition costs compared to traditional brokers where cross-selling is the norm but cost of operations is greater and less scalable. The promise of the online broker model is that once scale is achieved, lower operational costs will start to offset those higher and fiercely competitive acquisition costs.

In other words, a classic venture/digitisation bet, but one that is yet to pan out definitively.

As another reference point, one source tells me that Trussle is projected to make a £10 million loss in 2019 based on £2 million in revenue. I also understand from sources that the startup recently closed an internal funding round from existing investors — separate from its £13.6 million Series B in May 2018, and that its backers remain bullish. As always, watch this space.

Powered by WPeMatico