india

Auto Added by WPeMatico

Auto Added by WPeMatico

Does the overcrowded and cut-throat music streaming business have room for an additional player? The world’s most valuable startup certainly thinks so.

Chinese conglomerate ByteDance, valued at more than $75 billion, is working on a music streaming service, two sources familiar with the matter told TechCrunch. The company, which operates popular app TikTok, has held discussions with music labels in recent months to launch the app as soon as the end of this quarter, one of the sources said.

The app will offer both a premium and an ad-supported free tier, one of the sources said. Bloomberg, which first wrote about the premium app, reported that ByteDance is targeting emerging markets with its new music app. A ByteDance spokesperson declined to comment.

For ByteDance, interest in a music app does not come as a surprise. Snippets of pop songs from movies and albums intertwined with videos shot by its humongous user base is part of the service’s charm. The company already works with music labels worldwide to licence usage of their tracks on its platform. In China, where ByteDance claims to have tie-ups with more than 800 labels, it has been aggressively expanding efforts to find music talents and urge them to make their own tracks.

Besides, ByteDance has been expanding its app portfolio in recent months. Earlier this year, the company released Duoshan, a video chat app that appears to be a mix of TikTok and Snap. This week, it launched Feiliao, another chat app that is largely focused on text-driven conversations. At some point, the company may have realized the need for a standalone music consumption app.

When asked about TikTok’s partnership with music labels last month, Todd Schefflin, TikTok’s head of global music business development, told WSJ that music is part of the app’s “creative DNA” but it is “ultimately for short video creation and viewing, not a product for music consumption.”

The private Chinese company is likely eyeing India as a key market for its music app. The company has been in discussion with local music labels T Series and Times Music for rights. Moreover, its apps are estimated to have more than 300 million monthly active users in the nation, though there could be significant overlaps among them.

India may have also inspired ByteDance to consider a free, ad-supported version of its music app. Even as more than 150 million users in India listen to music online, only a tiny portion of this user base is willing to pay for it.

This has made India a unique battleground for local and international music giants, most of which offer an ad-supported, free version of their apps in the market. Even premium offerings from Apple and Spotify cost less than $1.2 a month. India is the only market where Spotify offers a free version of its app that has access to the entire catalog on demand.

The launch of the app could put the spotlight again on ByteDance in India, where its TikTok app recently landed in hot water. An Indian court banned the app for roughly a week after expressing concerns over questionable content on the platform. Ever since the nation lifted the ban on TikTok, the company has become visibly cautious about its movement.

Powered by WPeMatico

As we swing into the summer tourist season, a company poised to capitalise on that has raised a huge round of funding. GetYourGuide — a Berlin startup that has built a popular marketplace for people to discover and book sightseeing tours, tickets for attractions and other experiences around the world — is today announcing that it has picked up $484 million, a Series E round of funding that will catapult its valuation above the $1 billion mark.

The funding is a milestone for a couple of reasons. GetYourGuide says it is the highest-ever round of funding for a company in the area of “travel experiences” (tours and other activities) — a market estimated to be worth $150 billion this year and rising to $183 billion in 2020. And this Series E is also one of the biggest-ever growth rounds for any European startup, period.

The company has now sold 25 million tickets for tours, attractions and other experiences, with a current catalog of some 50,000 experiences on offer. That’s a sign of strong growth: in 2017 it sold 10 million tickets, and its last reported catalog number was 35,000. It will be using the funding to build more of its own “Originals” tour experiences — which have now passed the 40,000 tickets sold mark — as well as to build up more activities in Asia and the U.S., two fast-growing markets for the startup.

The funding is being led by SoftBank, via its Vision Fund, with Temasek, Lakestar, Heartcore Capital (formerly Sunstone Capital) and Swisscanto Invest among others also participating. (Swisscanto is part of Zürcher Kantonalbank: GetYourGuide was originally founded in Zurich, where the founders had studied, and it still runs some R&D operations there.) The company has now raised well over $600 million.

It’s notable how SoftBank — which is on the hunt for interesting opportunities to invest its $100 billion superfund — has been stepping up a gear in Germany to tap into some of the bigger tech players that have emerged out of that market, which today is the biggest in Europe. Other big plays have included €460 million into Auto1 and €900 million into payments provider Wirecard. Other companies it has backed, such as hotel company Oyo out of India, are using its funding to break into Europe (and buy German companies in the process).

There had been reports over the last several months that GetYouGuide was in the process of raising anywhere between $300 million and more than $500 million. In late April, we were told by sources that the round hadn’t yet closed, and that numbers published in the media up to then had been inaccurate, even as we nailed down that SoftBank was indeed involved in the round.

The valuation in this round is not being disclosed, but CEO Johannes Reck (who co-founded the app with Martin Sieber, Pascal Mathis, Tobias Rein and Tao Tao) said in an interview with TechCrunch that it was definitely “now a unicorn” — meaning that its valuation had passed the $1 billion mark. For additional context, the rumor last month was that GetYourGuide’s valuation was up to €1.6 billion ($1.78 billion), but I have not been able to get firm confirmation of that number.

GetYourGuide’s growth — and investor interest in it — has closely followed the rise of new platforms like Airbnb that have changed the face of how we travel, and what we do when we get somewhere. We have moved far beyond the days of visiting a travel agent that books everything, from flight to hotel to all your activities, as you sit on the other side of a desk from her or him. Now with the tap of a finger or the click of a mouse, we have thousands of choices.

Within that, GetYourGuide thinks that it has jumped on an interesting opportunity to rethink the activity aspect of tourism. Tour packages and other highly organized travel experiences are often associated with older people, or those with families — essentially people who need more predictability when they are not at home.

Reck noted that the earliest users of GetYourGuide in 2010 were precisely those people — or at least those who were more inclined to use digital platforms to begin with: the demographic, he said, was 40-50 year olds, most likely travelling with family.

That is one thing that has really started to change, in no small part because of GetYourGuide itself. Making the experience of booking experiences mobile-friendly, GetYourGuide has played into the culture of doing and showing, which has propelled the rise of social media.

“They want to do things, to have something to post on Instagram,” he said. The average age of a GetYourGuide user now, he said, is 25-40.

This has even evolved into what GetYourGuide provides to users. “At some point, staff in Asia had the idea of crafting a ‘GetYourGuide Instagram Tour of Bali.’ That really took off, and now this is the number-one tour booked in the region.” It has since expanded the concept to 50 destinations.

Not by coincidence, today the company is also announcing that Ameet Ranadive is joining as the company’s first chief product officer. Ranadive comes from Instagram, where he led the Well-being product team (the company’s health and safety team). He’d also been VP and GM of Revenue Product at Twitter. Nils Chrestin is also coming on as CFO, having recently been at Rocket Internet-incubated Global Fashion Group.

That has also led GetYourGuide to conclude it has a ways to go to continue developing its model and scope further, expanding into longer sightseeing excursions, beyond one or two-hour tours into day trips and even overnight experiences.

As it continues to play around with some of these offerings, it’s also increasingly taking a more direct role in the branding and the provision of the content. Initially, all tickets and tours were posted on GetYourGuide by third parties. Now, GetYourGuide is building more of what Reck calls “Originals” — which it might develop in partnership with others but ultimately handles as its own first-party content. (That Instagram tour was one of those Originals.)

It’s worth noting that others are closing in on the same “experiences” model that forms the core of GetYourGuide’s business: Airbnb, to diversify how it makes revenues and to extend its touchpoints with guests beyond basic accommodation bookings, has also started to sell experiences. Meanwhile, daily deals pioneer Groupon has also positioned itself as a destination for purchasing “experiences” as a way to offset declines in other areas of its business. Similarly, travel portals that sell plane tickets regularly default to pushing more activities on you.

Reck pointed out that the area of business where GetYourGuide is active is becoming increasingly attractive to these players as other aspects of the travel industry become increasingly commoditised. Indeed, you can visit dozens of sites to compare pricing on plane tickets, and if you are flexible, pick up even more of a bargain at the last minute. And the rise of multiple Airbnb-style platforms offering private accommodation has made competition among those supplying those platforms — as well as hotels — increasingly fierce.

All of that leaves experiences — for now at least — as the place where these companies can differentiate themselves from the pack. Reck believes that focusing on this, however, means you just do it much better than companies that have added experiences on to a platform that is not a native destination for discovering or buying that kind of content or product. (That doesn’t mean there aren’t others natively tackling “experiences” from the world of startups. Klook is one also funded by SoftBank.)

“Consumers, especially millennials, are spending an increasing portion of their disposable income on travel experiences. We believe GetYourGuide is leading this seismic shift by consolidating the fragmented global supply base of tour operators and modernizing access for travelers globally,” said Ted Fike, partner at SoftBank Investment Advisers, in a statement. “This combination creates powerful network effects for their business that is fueling their strong growth. We are excited to partner with their passionate and talented leadership team.” Fike is joining the board with this round.

Powered by WPeMatico

A day after India’s largest wallet app Paytm entered the credit card business, local ride-hailing giant Ola is following suit. Ola has inked a deal with state-run SBI and Visa to issue as many as 10 million credit cards in the next three and a half years, it said today.

The move will help Visa and SBI (State Bank of India) acquire more customers in India, where most transactions are still bandied out over cash. For Ola, which rivals Uber in India, the foray into credit cards represents a new avenue to monetize its customers, as TechCrunch previously reported.

With about 150 million users availing more than 2 million rides on its platform each day, Ola is sitting on a mountain of data about its users’ financial power and spends. With the card, dubbed Ola Money-SBI Credit Card, the mobility firm is also offering several discounts and savings to retain its loyal customer base.

Ola, which is nearing $6 billion in valuation and counts SoftBank and Naspers among its investors, said it will offer its credit card holders “highest cashback and rewards” in the form of Ola Money that could be redeemed for Ola rides, as well as flight and hotel bookings. There will be 7% percent cashback on cab spends, 5% on flight bookings, 20% on domestic hotel bookings (6% on international hotel bookings), 20% on more than 6,000 restaurants and 1% on all other spends.

In an interview with TechCrunch, Nitin Gupta, CEO of Ola financial services, claimed that the company was offering “five times rewards to customers” in comparison to average credit card companies. “Also, the card is a first of its kind offering that can be managed digitally through the Ola App. We are committed to creating an inclusive ecosystem where mobility and financial services go hand in hand in leading growth and development,” he said. Ola said it has already rolled out the card to some users and will invite other eligible customers to avail it.

“Mobility spends form a significant wallet share for users and we see a huge opportunity to transform their payments experience with this solution. With over 150 million digital-first consumers on our platform, Ola will be a catalyst in driving India’s digital economy with cutting edge payment solutions,” Bhavish Aggarwal, co-founder and CEO of Ola, said in a statement.

Ola appears to be following the playbook of Grab and Go-Jek, two ride-hailing services in Southeast Asian markets that have ventured into a number of businesses in recent years. Both Grab and Go-Jek offer loans, remittance and insurance to their riders, while the former also maintains its own virtual credit card. Interestingly, Uber, which also offers a credit card in some markets, has no such play in India.

The move will allow Ola to look beyond ride-hailing and food delivery, two businesses that appear to have hit a saturation point in India, said Satish Meena, an analyst with research firm Forrester.

In recent years, Ola has started to explore financial services. It offers riders “micro-insurance” that covers a range of risks, including loss of baggage and medical expenses. The company said earlier this year, it has sold more than 20 million insurances to customers. Using Ola Money to facilitate cashbacks also underscores Ola’s push to increase the adoption of its mobile wallet, which, according to estimates, lags Paytm and several other wallet and UPI payment apps.

The company has also made a major push in the electric vehicles business, which it spun off as a separate company earlier this year. In March, its EV business raised $300 million from Hyundai and Kia. The company has said that it plans to offer one million EVs by 2022. Its other EV programs include a pledge to add 10,000 rickshaws for use in cities.

Powered by WPeMatico

Paytm, India’s largest mobile wallet app, has branched out to several businesses in recent years as threat from Google and Facebook grows. On Tuesday, it added another category to the list: credit cards.

The firm, operated by One97 Communications, today unveiled Paytm First Credit Card with lofty benefits as it races to bulk up its financial offerings. The cards, issued by Citi Bank, will be the first in the country to offer unlimited, one percent cashback on purchases, Paytm claimed in a statement. The company is hoping to rope in about 25 million credit card customers in the coming months.

The penetration of credit cards remains very low in India with under 50 million people possessing one. With people conducting most of their businesses through cash in the nation, banks have little understanding of a customer’s credit history and score. And it also doesn’t help that banks in India are still wary of issuing credit cards to those who don’t perfectly fit the traditional blue collar job.

But why is a company that made its name through a mobile payment wallet open to its customers engaging with credit card companies? Paytm itself is struggling to grow its business and retain existing customers. Some of its recent major bets haven’t exactly paid off. Its ecommerce business Paytm Mall remains tiny despite bleeding money.

Yo! The First. Paytm First. pic.twitter.com/5kAxozc2IH

— Vijay Shekhar (@vijayshekhar) May 13, 2019

But more importantly, payments itself has become a commoditized space. Users park their money in Paytm and do transactions from there. Paytm makes money from this accumulated sum. This business flourished for years, especially in the months after the Indian government invalidated much of the cash in the nation. But then the government launched its own payment infrastructure called UPI, which removes the need for a middleman.

This has made payments more convenient for users, who are increasingly jumping ship. UPI apps such as PhonePe that have emerged in the last two and a half years now see more transactions than wallet apps. To make matter worse for Paytm, Google and Facebook — two companies that have larger userbase in India — have entered the payments space. Google Pay reached 100 million installs on Google Play Store recently, and WhatsApp plans a nation-wide roll out of its payment feature in India later this year.

So Paytm is now expanding its financial offerings and credit card play fits well in it. With more than 200 million active users, Paytm rivals banks on both the number of customers and volume of transaction it processes.

“Our new offering is designed to bring utmost flexibility to our customers in their digital payment options and will help spur large-ticket cashless payments,” Vijay Shekhar Sharma, chairman and CEO of One97 Communications said in a statement.

Backed by SoftBank, Alibaba, and most recently Warren Buffett’s Berkshire Hathaway, Paytm has the capital to spur the adoption of its new credit card. As part of the package, Paytm’s credit card holders will be able to avail dining, shopping, travel and other offers that Citi Bank provides to its privilege customers. In the first four months of issuing a card, the company will offer its customers discounts worth Rs 10,000 ($142) on spending of Rs 10,000.

Paytm First Credit Card will work both in India and elsewhere and support contactless transactions. Like any other credit card, customers will be able to pay back a sum in multiple monthly instalments. Paytm First Credit Card will charge users a nominal fee of Rs 500 ($7.1) that will be waived off if their spendings through the card exceeds Rs 50,000 ($710) in a year.

If the gamble works, Paytm will be able to retain some customers and convince many to do big-ticket transactions. For Citi Bank, this partnership is just an easy ploy to acquire some customers.

In the meantime, Paytm continues to aggressively expand its financial offerings. In recent years, it has launched a digital payments bank, and has started to offer prepaid Forex cards for international purchases. It also lets customers buy gold, and employers issue food allowance wallets for their staff. Last year, the company announced Paytm Money to facilitate purchase of mutual funds.

Earlier this year, the company launched Paytm First, a subscription bundle that includes access to subscriptions from other services such as Zomato, Uber, Gaana, and Eros Now. In an interview with TechCrunch late last month, Paytm’s Sharma said payments is the moat around which you can build a number of services. “Now that’s a business model… payment itself can’t make you money.”

Powered by WPeMatico

Locus, an Indian startup that uses AI to help businesses map out their logistics, has raised $22 million in Series B funding to expand its operations in international markets.

The financing round for the four-year-old startup was led by Falcon Edge Capital and Tiger Global. Existing investors Exfinity Venture Partners and Blume Ventures also participated in the round. The startup has raised $29 million to date, Nishith Rastogi, co-founder and CEO of Locus, told TechCrunch in an interview.

Locus works with companies that operate in FMCG, logistics and e-commerce spaces. Some of its clients include Tata Group companies, Myntra, BigBasket, Lenskart and Bluedart. It helps these clients automate their logistics workload — tasks such as planning, organizing, transporting and tracking of inventories, and finding the best path to reach a destination — that have traditionally required intensive human labor.

“Say a Lenskart representative is visiting a house or an office to offer an eye checkup, and suddenly two more people there are interested in getting their eyes checked. The representative could attend these two new potential clients, or wrap things up with the first client and take care of his or her next appointment,” said Rastogi.

Locus looks at a client’s past data, identifies patterns and automates these kind of decisions on a large scale. In an example shared earlier with TechCrunch, Rastogi talked about how Locus had built a scanner for e-commerce companies for measuring products.

Rastogi said he will use the fresh capital to develop products and expand Locus in Southeast Asian and North American markets. The startup says half of its 110-person workforce is outside of India. Half of the IP it has built and the revenue it generates comes from its team outside of India.

He said the startup has spent the recent quarters studying these international markets, and has secured some anchor clients to expand the business. Locus is operationally profitable already and any additional capital goes into expanding its business, he added.

The logistics market in India has long been riddled with challenges. A growing number of startups, including BlackBuck — which raised $150 million last week — have emerged in recent years to tackle these problems.

The new funding also illustrates Tiger Global’s new strategy for the Indian market. The VC fund, which has invested in B2C businesses Flipkart and Ola in India, has made a number of investments in B2B startups in recent months. Last month, it invested $90 million in agritech supply chain startup Ninjacart, and weeks later, it gave cloud-based solutions provider Zenoti $50 million. It also participated in customer marketing service ClearTap’s $26 million round.

Powered by WPeMatico

Indian video streaming giant Hotstar, owned by Disney, today set a new global benchmark for the number of people an OTT service can draw to a live event.

Some 18.6 million users simultaneously tuned into Hotstar’s website and app to watch the deciding game of the 12th edition of the Indian Premier League (IPL) cricket tournament. The streaming giant, which competes with Netflix and Amazon in India, broke its own “global best” 10.3 million concurrent views milestone that it had set last year.

Hotstar topped the 10 million concurrent viewership mark a number of times during this year’s 51-day IPL season. More than 12.7 million viewers huddled to watch an earlier game in the tournament (between Royal Challengers Bangalore and Mumbai Indians), a spokesperson for the four-year-old service said. In mid-April, Hotstar said that the cricket series had already garnered a 267 million overall viewership, creating a new record for the streamer. (Last year’s IPL had clocked a 202 million overall viewership.)

Fans of Mumbai Indians celebrate their team’s victory against Chennai Super Kings in IPL cricket tournament in India.

These figures coming out of India, the fastest-growing internet market, are astounding to say the least. In comparison, a 2012 live stream of skydiver Felix Baumgartner jumping from near-space to the Earth’s surface, remains the most concurrently viewed video on YouTube. It amassed about 8 million concurrent viewers. The live viewership of the royal wedding between Prince Harry and Meghan Markle was also a blip in comparison.

As Netflix and Amazon scramble to find the right content strategy to lure Indians, Hotstar and its local parent firm Star India have aggressively focused on securing broadcast and streaming rights to various cricket series. Cricket is almost followed like a religion in India.

In 2017, Star India, then owned by 21st Century Fox, secured the rights to broadcast and stream the IPL cricket tournament for five years for a sum of roughly $2.5 billion. Facebook had also participated in the bidding, offering north of $600 million for streaming. (Star India was part of 21st Century Fox’s business that Disney acquired for $71.3 billion earlier this year.)

That bet has largely paid off. Hotstar said last month that its service has amassed 300 million monthly active users, up from 150 million it had reported last year. In comparison, both Netflix and Amazon Prime Video have less than 30 million subscribers in India, according to industry estimates.

In the last two years, Hotstar has expanded to three international markets — the U.S., Canada, and most recently, the UK — to chase new audiences. The streaming service is hoping to attract Indians living overseas and anyone else who is interested in Bollywood movies and cricket, Ipsita Dasgupta, president of Hotstar’s international operations, told TechCrunch in an interview.

The streaming service plans to enter Sri Lanka, Pakistan, Nepal, Middle East, Australia, and New Zealand in the next few quarters, Dasgupta said.

That’s not to say that Hotstar has a clear path ahead. According to several estimates, the streaming service typically sees a sharp decline in its user base after the conclusion of an IPL season. Despite the massive engagement it generates, it remains operationally unprofitable, people familiar with Hotstar’s finances said.

The ad-supported streaming service offers about 80 percent of its content catalog — which includes titles produced by Star India, and shows and movies syndicated from international partners HBO, ABC, and Showtime among others — for no cost to users. One of the most watched international shows on the platform, “Game of Thrones,” will be ending soon, too.

The upcoming World Cup cricket tournament, which Hotstar will stream in India, should help it avoid the major headache for sometime. In the meantime, the service is aggressively expanding its slate of original shows in the nation. One of the shows is a remake of BBC/NBC’s popular “The Office.”

Powered by WPeMatico

Truecaller, an app that helps users screen strangers and robocallers, will soon allow users in India, its largest market, to borrow up to a few hundred dollars.

The crediting option will be the fourth feature the nine-year-old app adds to its service in the last two years. So far it has added to the service the ability to text, record phone calls and mobile payment features, some of which are only available to users in India. Of the 140 million daily active users of Truecaller, 100 million live in India.

The story of the ever-growing ambition of Truecaller illustrates an interesting phase in India’s internet market that is seeing a number of companies mold their single-functioning app into multi-functioning so-called super apps.

This may sound familiar. Truecaller and others are trying to replicate Tencent’s playbook. The Chinese tech giant’s WeChat, an app that began life as a messaging service, has become a one-stop solution for a range of features — gaming, payments, social commerce and publishing platform — in recent years.

WeChat has become such a dominant player in the Chinese internet ecosystem that it is effectively serving as an operating system and getting away with it. The service maintains its own “app store” that hosts mini apps. This has put it at odds with Apple, though the iPhone-maker has little choice but to make peace with it.

For all its dominance in China, WeChat has struggled to gain traction in India and elsewhere. But its model today is prominently on display in other markets. Grab and Go-Jek in Southeast Asian markets are best known for their ride-hailing services, but have begun to offer a range of other features, including food delivery, entertainment, digital payments, financial services and healthcare.

The proliferation of low-cost smartphones and mobile data in India, thanks in part to Google and Facebook, has helped tens of millions of Indians come online in recent years, with mobile the dominant platform. The number of internet users has already exceeded 500 million in India, up from some 350 million in mid-2015. According to some estimates, India may have north of 625 million users by year-end.

This has fueled the global image of India, which is both the fastest growing internet and smartphone market. Naturally, local apps in India, and those from international firms that operate here, are beginning to replicate WeChat’s model.

Founder and chief executive officer (CEO) of Paytm Vijay Shekhar Sharma speaks during the launch of Paytm payments Bank at a function in New Delhi on November 28, 2017 (AFP PHOTO / SAJJAD HUSSAIN)

Leading that pack is Paytm, the popular homegrown mobile wallet service that’s valued at $18 billion and has been heavily backed by Alibaba, the e-commerce giant that rivals Tencent and crucially missed the mobile messaging wave in China.

In recent years, the Paytm app has taken a leaf from China with additions that include the ability to text merchants; book movie, flight and train tickets; and buy shoes, books and just about anything from its e-commerce arm Paytm Mall . It also has added a number of mini games to the app. The company said earlier this month that more than 30 million users are engaging with its games.

Why bother with diversifying your app’s offering? Well, for Vijay Shekhar Sharma, founder and CEO of Paytm, the question is why shouldn’t you? If your app serves a certain number of transactions (or engagements) in a day, you have a good shot at disrupting many businesses that generate fewer transactions, he told TechCrunch in an interview.

At the end of the day, companies want to garner as much attention of a user as they can, said Jayanth Kolla, founder and partner of research and advisory firm Convergence Catalyst.

“This is similar to how cable networks such as Fox and Star have built various channels with a wide range of programming to create enough hooks for users to stick around,” Kolla said.

“The agenda for these apps is to hold people’s attention and monopolize a user’s activities on their mobile devices,” he added, explaining that higher engagement in an app translates to higher revenue from advertising.

Paytm’s Sharma agrees. “Payment is the moat. You can offer a range of things including content, entertainment, lifestyle, commerce and financial services around it,” he told TechCrunch. “Now that’s a business model… payment itself can’t make you money.”

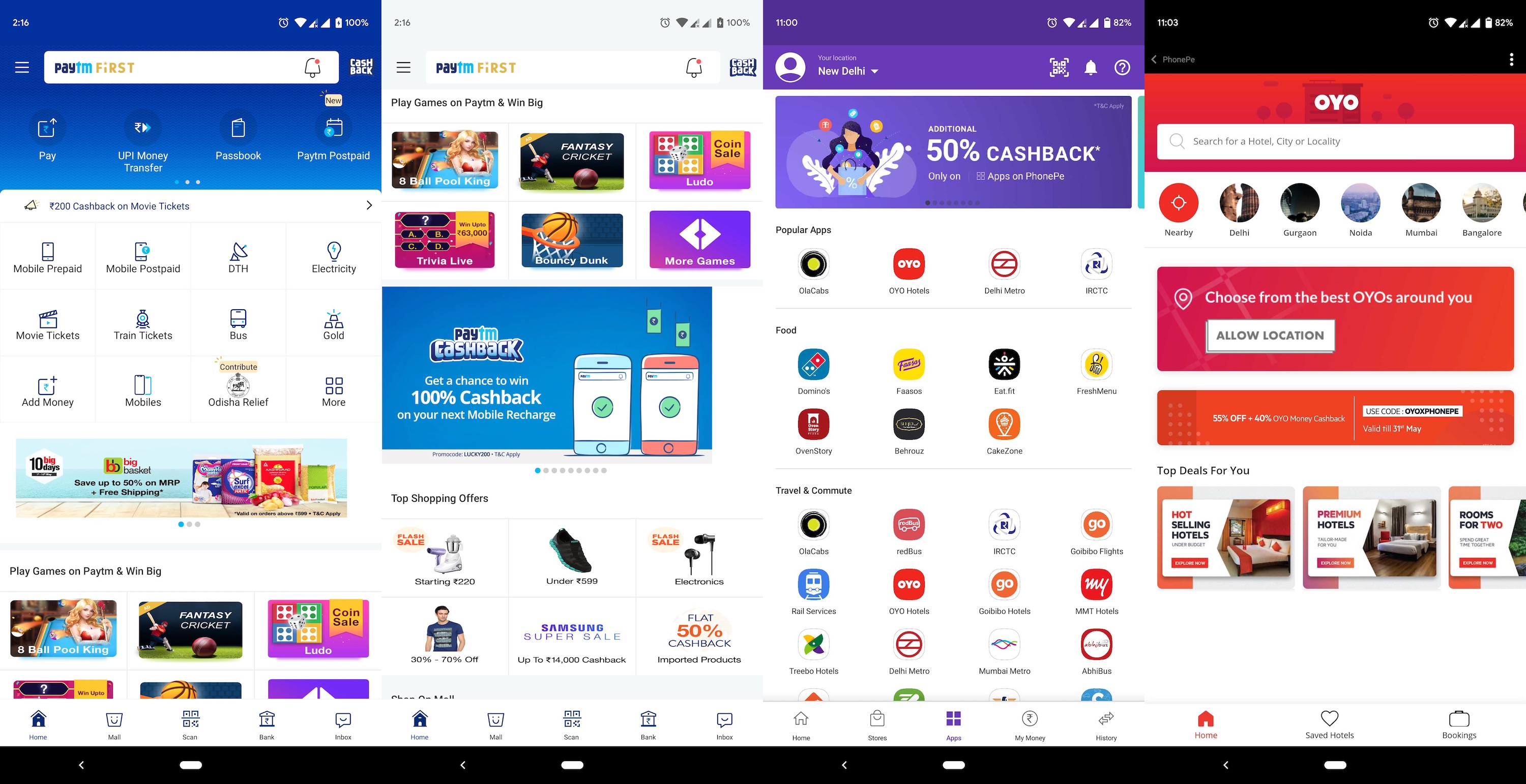

Other businesses have taken note. Flipkart -owned payment app PhonePe, which claims to have 150 million active users, today hosts a number of mini apps. Some of those include services for ride-hailing service Ola, hotel booking service Oyo and travel booking service MakeMyTrip.

Paytm (the first two images from left) and PhonePe offer a range of services that are integrated into their payments apps

What works for PhonePe is that its core business — payments — has amassed enough users, Himanshu Gupta, former associate director of marketing and growth for WeChat in India, told TechCrunch. He added that unlike e-commerce giant Snapdeal, which attempted to offer similar offerings back in the day, PhonePe has tighter integration with other services, and is built using modern architecture that gives users almost native app experiences inside mini apps.

When you talk about strategy for Flipkart, the homegrown e-commerce giant acquired by Walmart last year for a cool $16 billion, chances are arch rival Amazon is also hatching similar plans, and that’s indeed the case for super apps.

In India, Amazon offers its customers a range of payment features such as the ability to pay phone bills and cable subscription through its Amazon Pay service. The company last year acquired Indian startup Tapzo, an app that offers integration with popular services such as Uber, Ola, Swiggy and Zomato, to boost Pay’s business in the nation.

Another U.S. giant, Microsoft, is also aboard the super train. The Redmond-based company has added a slew of new features to SMS Organizer, an app born out of its Microsoft Garage initiative in India. What began as a texting app that can screen spam messages and help users keep track of important SMSs recently partnered with education board CBSE in India to deliver exam results of 10th and 12th grade students.

This year, the SMS Organizer app added an option to track live train schedules through a partnership with Indian Railways, and there’s support for speech-to-text. It also offers personalized discount coupons from a range of companies, giving users an incentive to check the app more often.

Like in other markets, Google and Facebook hold a dominant position in India. More than 95% of smartphones sold in India run the Android operating system. There is no viable local — or otherwise — alternative to Search, Gmail and YouTube, which counts India as its fastest growing market. But Google hasn’t necessarily made any push to significantly expand the scope of any of its offerings in India.

India is the biggest market for WhatsApp, and Facebook’s marquee app too has more than 250 million users in the nation. WhatsApp launched a pilot payments program in India in early 2018, but is yet to get clearance from the government for a nationwide rollout. (It isn’t happening for at least another two months, a person familiar with the matter said.) In the meanwhile, Facebook appears to be hatching a WeChatization of Messenger, albeit that app is not so big in India.

Ride-hailing service Ola too, like Grab and Go-Jek, plans to add financial services such as credit to the platform this year, a source familiar with the company’s plans told TechCrunch.

“We have an abundance of data about our users. We know how much money they spend on rides, how often they frequent the city and how often they order from restaurants. It makes perfect sense to give them these valued-added features,” the person said. Ola has already branched out of transport after it acquired food delivery startup Foodpanda in late 2017, but it hasn’t yet made major waves in financial services despite giving its Ola Money service its own dedicated app.

The company positioned Ola Money as a super app, expanded its features through acquisition and tie ups with other players and offered discounts and cashbacks. But it remains behind Paytm, PhonePe and Google Pay, all of which are also offering discounts to customers.

Super apps indeed come in all shapes and sizes, beyond core services like payment and transportation — the strategy is showing up in apps and services that entertain India’s internet population.

MX Player, a video playback app with more than 175 million users in India that was acquired by Times Internet for some $140 million last year, has big ambitions. Last year, it introduced a video streaming service to bolster its app to grow beyond merely being a repository. It has already commissioned the production of several original shows.

In recent months, it has also integrated Gaana, the largest local music streaming app that is also owned by Times Internet. Now its parent company, which rivals Google and Facebook on some fronts, is planning to add mini games to MX Player, a person familiar with the matter said, to give it additional reach and appeal.

Some of these apps, especially those that have amassed tens of millions of users, have a real shot at diversifying their offerings, analyst Kolla said. There is a bar of entry, though. A huge user base that engages with a product on a daily basis is a must for any company if it is to explore chasing the super app status, he added.

Indeed, there are examples of companies that had the vision to see the benefits of super apps but simply couldn’t muster the requisite user base. As mentioned, Snapdeal tried and failed at expanding its app’s offerings. Messaging service Hike, which was valued at more than $1 billion two years ago and includes WeChat parent Tencent among its investors, added games and other features to its app, but ultimately saw poor engagement. Its new strategy is the reverse: to break its app into multiple pieces.

“In 2019, we continue to double down on both social and content but we’re going to do it with an evolved approach. We’re going to do it across multiple apps. That means, in 2019 we’re going to go from building a super app that encompasses everything, to Multiple Apps solving one thing really well. Yes, we’re unbundling Hike,” Kavin Mittal, founder and CEO of Hike, wrote in an update published earlier this year.

It remains unclear how users are responding to the new features on their favorite apps. Some signs suggest, however, that at least some users are embracing the additional features. Truecaller said it is seeing tens of thousands of users try the payment feature for the first time each day. It’s also being used to send 3 billion texts a month.

Regardless, the race is still on, and there are big horses waiting to enter to add further competition.

Reliance Jio, a subsidiary of conglomerate Reliance Industry that is owned by India’s richest man, Mukesh Ambani, is planning to introduce a super app that will host more than 100 features, according to a person familiar with the matter. Local media first reported the development.

It will be fascinating to see how that works out. Reliance Jio, which almost single-handedly disrupted the telecom industry in India with its low-cost data plans and free voice calls, has amassed tens of millions of users on the bouquet of apps that it offers at no additional cost to Jio subscribers.

Beyond that diverse selection of homespun apps, Reliance has also taken an M&A-based approach to assemble the pieces of its super app strategy.

It bought music streaming service Saavn last year and quickly integrated it with its own music app JioMusic. Last month, it acquired Haptik, a startup that develops “conversational” platforms and virtual assistants, in a deal worth more than $100 million. It already has the user bases required. JioTV, an app that offers access to over 500 TV channels; and JioNews, an app that additionally offers hundreds of magazines and newspapers, routinely appear among the top apps in Google Play Store.

India’s super app revolution is in its early days, but the trend is surely one to keep an eye on as the country moves into its next chapter of internet usage.

Powered by WPeMatico

Indian edtech startup CollegeDekho, which helps students connect with prospective colleges and keep track of exams, has raised $8 million in a Series B round.

The new financing round for the four-year-old Gurgaon-based startup was led by its parent company GirnarSoft Education and London-based private equity investor Man Capital, which also participated in the startup’s Series A round last year.

Ruchir Arora, founder and CEO of CollegeDekho, told TechCrunch in an interview that the startup will use the capital to expand its presence in more schools and also begin connecting students with international educational institutions. The startup, which has raised $13 million to date, will also ramp up its research and development efforts.

CollegeDekho, Hindi for search for college, maintains a website that helps students identify the right career choices for them. The website has a chatbot that answers some of the questions students have while logging their responses, and other activities such as the kind of colleges they are searching for, their preferred location and budget.

Arora said the startup, which also has about 3,000 call center representatives and counselors, builds profiles of students to make college recommendations. He said each month the site observes more than five million sessions from students. Last year, more than 8,000 students used CollegeDekho to take admission in a college.

Parents in India, a country of 1.3 billion people with not the best literacy record, see education as an upward mobility for their children. Each year, more than six to seven million students go to a college. But because of a range of factors that can include cultural stigma, many students end up choosing the wrong path and thus don’t excel in college. Indeed, many students ultimately don’t pursue the subject they are best suited for, Arora said, and that’s where CollegeDekho aims to make an impact.

Most high school students in India often gravitate toward engineering or medical college, as a result of which, each year India produces many engineers and doctors who struggle for years to find a job. Arora said his startup looks at more than 2,000 career paths a student could pursue.

What works in favor of Arora is that the country will continue to turn out millions of students each year who will be looking to go to a college soon. It also helps that CollegeDekho is operationally profitable, Arora said, adding that it generates about $3.2 million in revenue in a year. Any additional cash the startup raises will go into its expansion, he said.

CollegeDekho charges a nominal fee from students, and also takes a cut when they join a college. More than 36,000 educational institutes are listed on CollegeDekho. The startup also works with more than 400 colleges to conduct an exam for direct admission, and there too it earns a cut.

India’s education market, estimated to grow to $5.7 billion by next year, has emerged as a lucrative opportunity for startups and VCs alike. Bangalore-based Byju’s, which helps millions of students in India prepare for competitive exams, raised $540 million from Naspers and others late last year. Unacademy, which like Byju’s offers online tutoring to students, has raised more than $38.5 million to date.

A legion of other education startups today are vying for the attention of students in the nation. Noida-based AskIITians, not too far from the offices of CollegeDekho, aims to help school-going students prepare for medical and engineering exams. Extramarks, also based in Noida, operates in the same space as AskIITians. Reliance Industries, owned and controlled by India’s richest man, Mukesh Ambani, bought a 38.5% stake in the startup three years ago.

Powered by WPeMatico

India has a new unicorn after BigBasket, a startup that delivers groceries and perishables across the country, raised $150 million for its fight against rivals Walmart’s Flipkart, Amazon and hyperlocal startups Swiggy and Dunzo.

The new financing round — a Series F — was led by Mirae Asset-Naver Asia Growth Fund, the U.K.’s CDC Group and Alibaba, BigBasket said on Monday. The closing of the round has officially helped the seven-year-old startup surpass $1 billion valuation, co-founder Vipul Parekh, who heads marketing and finances for the company, told TechCrunch in an interview. Chinese giant Alibaba, which also led the Series E round in BigBasket last year, is the largest investor in the company, with about 30% stake, a person familiar with the matter said.

The company, which offers more than 20,000 products from 1,000 brands in more than two dozen cities, will deploy the fresh capital into expanding its supply-chain network, adding more cold storage centers and distribution centers to serve customers faster, Parekh said. The company also plans to add about 3,000 vending machines that offer daily eatable items, such as vegetables, snacks and cold drinks in residential apartments and offices by next month, he added.

Infusion of $150 million for BigBasket, which raised $300 million last year, comes at a time when both Walmart’s Flipkart and Amazon are increasingly expanding their grocery businesses in India.

Amazon Retail India, which operates Amazon Pantry and Prime Now services and has a presence in mire than 100 cities, is reportedly planning to expand its business in India. Flipkart Group CEO Kalyan Krishnamurthy said in an interview with the Economic Times last month that the e-commerce giant may pilot a fresh foods business soon. Last week, Flipkart was said to be in talks to acquire grocery chain Namdhari’s Fresh.

Parekh largely brushed off the challenge his company faces from Flipkart and Amazon at this stage, saying that “it is a very large market, and it is unlikely to be dominated by one single company for the simple reason of its complex nature.” Flipkart and Amazon may eventually get serious about this space, but so far their play with groceries is mostly an additional differentiation checkpoint, he said.

“The success in this business requires having the ability to build and manage a very complex supply chain across multiple categories such as vegetables, meat and beauty products among others. Our focus has been on building the supply chain, and also ensuring that we are able to deliver a very large assortment of products to consumers,” he added. He said BigBasket today offers the largest catalog and fastest delivery among any of its rivals.

Besides, BigBasket, which is increasingly growing its subscription business to supply milk and other daily eatables, is also inching closer to becoming financially stronger. Parekh said BigBasket expects to become operationally profitable in six to eight months. “The idea is that business by itself does not consume cash. If we use cash, it will be for investment in new businesses or scaling of existing businesses,” he said.

India’s retail market, valued at mire than $900 billion, is increasingly attracting the attention of VC funds. Since 2014, online retailers alone have participated in more than 163 financing rounds, clocking over $1.38 billion, analytics firm Tracxn told TechCrunch. More than 882 players are operational in the market, the firm said.

The challenge for BigBasket remains fighting a growing army of rivals, including hyperlocal delivery startups including Grofers, which raised $60 million earlier this year, unicorn Swiggy and Google-backed Dunzo, which is increasingly becoming a verb in urban Indian cities.

Powered by WPeMatico

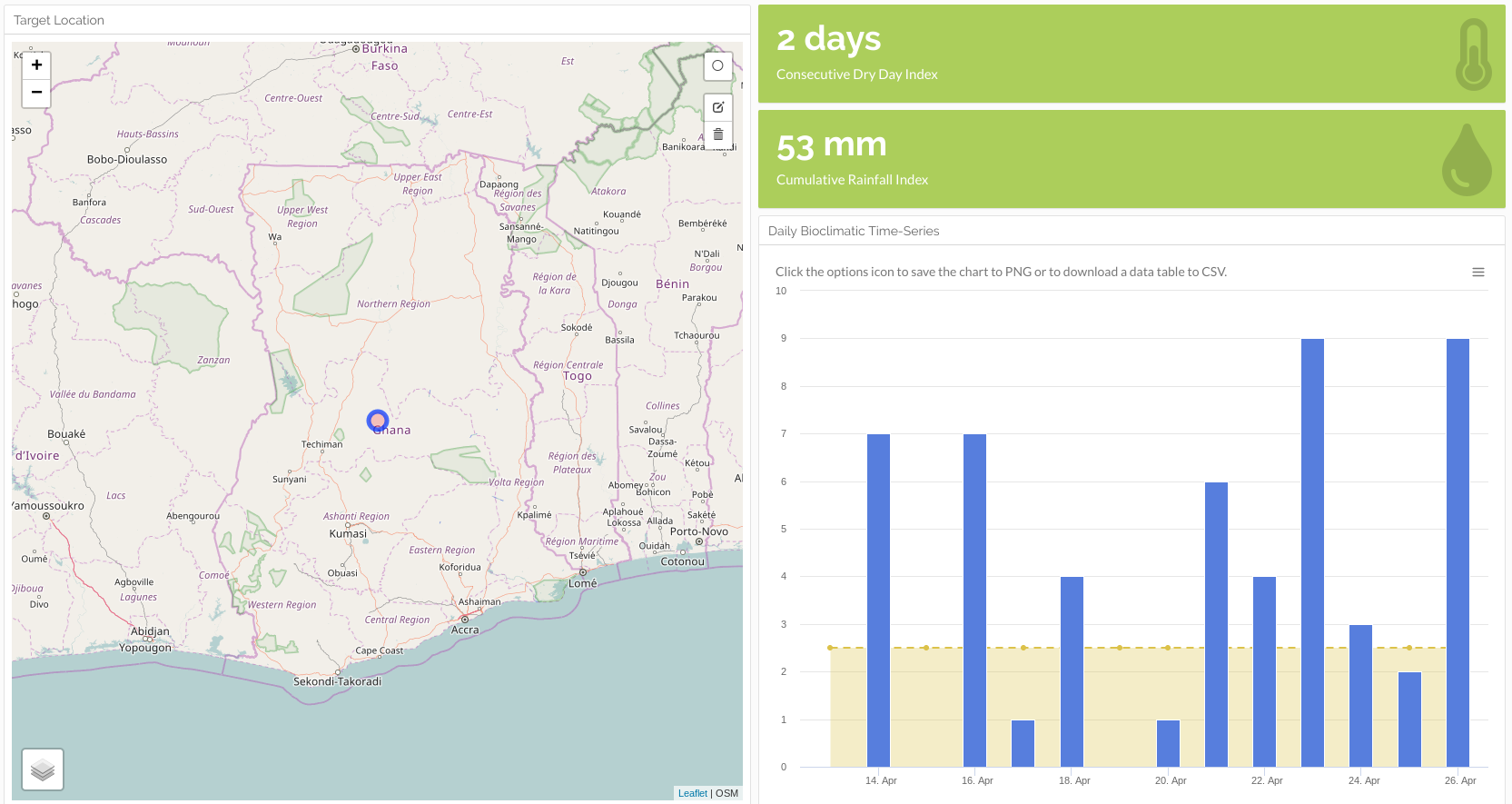

WorldCover, a New York and Africa-based climate insurance provider to smallholder farmers, has raised a $6 million Series A round led by MS&AD Ventures.

Y Combinator, Western Technology Investment and EchoVC also participated in the round.

WorldCover’s platform uses satellite imagery, on-ground sensors, mobile phones and data analytics to create insurance options for farmers whose crop yields are affected adversely by weather events — primarily lack of rain.

The startup currently operates in Ghana, Uganda and Kenya . With the new funding, WorldCover aims to expand its insurance offerings to more emerging market countries.

“We’re looking at India, Mexico, Brazil, Indonesia. India could be first on an 18-month timeline for a launch,” WorldCover co-founder and chief executive Chris Sheehan said in an interview.

The company has served more than 30,000 farmers across its Africa operations. Smallholder farmers are those earning all or nearly all of their income from agriculture, farming on 10-20 acres of land and earning around $500 to $5,000, according to Sheehan.

Farmers connect to WorldCover by creating an account on its USSD mobile app. From there they can input their region and crop type and determine how much insurance they would like to buy and use mobile money to purchase a plan. WorldCover works with payments providers such as M-Pesa in Kenya and MTN Mobile Money in Ghana.

The service works on a sliding scale, where a customer can receive anywhere from 5x to 15x the amount of premium they have paid. If there is an adverse weather event, namely lack of rain, the farmer can file a claim via mobile phone. WorldCover then uses its data-analytics metrics to assess it, and, if approved, the farmer will receive an insurance payment via mobile money.

Common crops farmed by WorldCover clients include maize, rice and peanuts. It looks to add coffee, cocoa and cashews to its coverage list.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

The startup’s founder clarified that WorldCover’s model does not assess or provide insurance payouts specifically for climate change, though it does directly connect to the company’s business.

“We insure for adverse weather events that we believe climate change factors are exacerbating,” Sheehan explained. WorldCover also resells the risk of its policyholders to global reinsurers, such as Swiss Re and Nephila.

On the potential market size for WorldCover’s business, he highlights a 2018 Lloyd’s study that identified $163 billion of assets at risk, including agriculture, in emerging markets from negative, climate change-related events.

“That’s what WorldCover wants to go after…These are the kind of micro-systemic risks we think we can model and then create a micro product for a smallholder farmer that they can understand and will give them protection,” he said.

With the round, the startup will look to possibilities to update its platform to offer farming advice to smallholder farmers, in addition to insurance coverage.

WorldCover investor and EchoVC founder Eghosa Omoigui believes the startup’s insurance offerings can actually help farmers improve yield. “Weather-risk drives a lot of decisions with these farmers on what to plant, when to plant, and how much to plant,” he said. “With the crop insurance option, the farmer says, ‘Instead of one hector, I can now plant two or three, because I’m covered.’ ”

Insurance technology is another sector in Africa’s tech landscape filling up with venture-backed startups. Other insurance startups focusing on agriculture include Accion Venture Lab-backed Pula and South Africa based Mobbisurance.

With its new round and plans for global expansion, WorldCover joins a growing list of startups that have developed business models in Africa before raising rounds toward entering new markets abroad.

In 2018, Nigerian payment startup Paga announced plans to move into Asia and Latin America after raising $10 million. In 2019, South African tech-transit startup FlexClub partnered with Uber Mexico after a seed raise. And Lagos-based fintech startup TeamAPT announced in Q1 it was looking to expand globally after a $5 million Series A round.

Powered by WPeMatico