Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

Almost exactly 4 months to the day after BigID announced a $50 million Series C, the company was back today with another $50 million round. The Series C extension came entirely from Tiger Global Management. The company has raised a total of $144 million.

What warrants $100 million in interest from investors in just four months is BigID’s mission to understand the data a company has and manage that in the context of increasing privacy regulation including GDPR in Europe and CCPA in California, which went into effect this month.

BigID CEO and co-founder Dimitri Sirota admits that his company formed at the right moment when it launched in 2016, but says he and his co-founders had an inkling that there would be a shift in how governments view data privacy.

“Fortunately for us, some of the requirements that we said were going to be critical, like being able to understand what data you collect on each individual across your entire data landscape, have come to [pass],” Sirota told TechCrunch. While he understands that there are lots of competing companies going after this market, he believes that being early helped his startup establish a brand identity earlier than most.

Meanwhile, the privacy regulation landscape continues to evolve. Even as California privacy legislation is taking effect, many other states and countries are looking at similar regulations. Canada is looking at overhauling its existing privacy regulations.

Sirota says that he wasn’t actually looking to raise either the C or the D, and in fact still has B money in the bank, but when big investors want to give you money on decent terms, you take it while the money is there. These investors clearly see the data privacy landscape expanding and want to get involved. He recognizes that economic conditions can change quickly, and it can’t hurt to have money in the bank for when that happens.

That said, Sirota says you don’t raise money to keep it in the bank. At some point, you put it to work. The company has big plans to expand beyond its privacy roots and into other areas of security in the coming year. Although he wouldn’t go into too much detail about that, he said to expect some announcements soon.

For a company that is only four years old, it has been amazingly proficient at raising money with a $14 million Series A and a $30 million Series B in 2018, followed by the $50 million Series C last year, and the $50 million round today. And Sirota said, he didn’t have to even go looking for the latest funding. Investors came to him — no trips to Sand Hill Road, no pitch decks. Sirota wasn’t willing to discuss the company’s valuation, only saying the investment was minimally diluted.

BigID, which is based in New York City, already has some employees in Europe and Asia, but he expects additional international expansion in 2020. Overall the company has around 165 employees at the moment and he sees that going up to 200 by mid-year as they make a push into some new adjacencies.

Powered by WPeMatico

A few days before Christmas, TechCrunch caught up with CrowdStrike CEO George Kurtz to chat about his company’s public offering, direct listings and his expectations for the 2020 IPO market. We also spoke about CrowdStrike’s product niche — endpoint security — and a bit more on why he views his company as the Salesforce of security.

The conversation is timely. Of the 2019 IPO cohort, CrowdStrike’s IPO stands out as one of the year’s most successful debuts. As 2020’s IPO cycle is expected to be both busy and inclusive of some of the private market’s biggest names, Kurtz’s views are useful to understand. After all, his SaaS security company enjoyed a strong pricing cycle, a better-than-expected IPO fundraising haul and strong value appreciation after its debut.

Notably, CrowdStrike didn’t opt to pursue a direct listing; after chatting with the CEO of recent IPO Bill.com concerning why his SaaS company also decided on a traditional flotation, we wanted to hear from Kurtz as well. The security CEO called the current conversation around direct listings a “great debate,” before explaining his perspective.

Pulling from a longer conversation, what follows are Kurtz’s four tips for companies gearing up for a public offering, why his company elected chose a traditional public offering over a more exotic method, comments on endpoint security and where CrowdStrike fits inside its market, and, finally, quick notes on upcoming debuts.

The following interview has been condensed and edited for clarity.

What’s most important is the fact that when we IPO’d in June of 2019, we started the process three years earlier. And that is the number one thing that I can point to. When [CrowdStrike CFO Burt Podbere] and I went on the road show everybody knew us, all the buy side investors we had met with for three years, the sell side analysts knew us. The biggest thing that I would say is you can’t go on a road show and have someone not know your company, or not know you, or your CFO.

And we would share — as a private company, you share less — but we would share tidbits of information. And we built a level of consistency over time, where we would share something, and then they would see it come true. And we would share something else, and they would see it come true. And we did that over three years. So we built, I believe, trust with the street, in anticipation of, at some point in the future, an IPO.

We spent a lot of time running the company as if it was public, even when we were private. We had our own earnings call as a private company. We would write it up and we would script it.

You’ve seen other companies out there, if they don’t get their house in order it’s very hard to go [public]. And we believe we had our house in order. We ran it that way [which] allowed us to think and operate like a public company, which you want to get out of the way before you come become public. If there’s a takeaway here for folks that are thinking about [going public], run it and act like a public company before you’re public, including simulated earnings calls. And once you become public, you already have that muscle memory.

The third piece is [that] you [have to] look at the numbers. We are in rarified air. At the time of IPO we were the fastest growing SaaS company to IPO ever at scale. So we had the numbers, we had the growth rate, but it really was a combination of preparation beforehand, operating like a public company, […] and then we had the numbers to back it up.

One last point, we had the [total addressable market, or TAM] as well. We have the TAM as part of our story; security and where we play is a massive opportunity. So we had that market opportunity as well.

On this topic, Kurtz told TechCrunch two interesting things earlier in the conversation. First that what many people consider as “endpoint security” is too constrained, that the category includes “traditional endpoints plus things like mobile, plus things like containers, IoT devices, serverless, ephemeral cloud instances, [and] on and on.” The more things that fit under the umbrella of endpoint security, CrowdStrike’s focus, the bigger its market is.

Kurtz also discussed how the cloud migration — something that builds TAM for his company’s business — is still in “the early innings,” going on to say that in time “you’re going to start to see more critical workloads migrate to the cloud.” That should generate even more TAM for CrowdStrike and its competitors, like Carbon Black and Tanium.

Powered by WPeMatico

It would be hard to top the 2018 enterprise M&A total of a whopping $87 billion, and predictably this year didn’t come close. In fact, the top 10 enterprise M&A deals in 2019 were less than half last year’s, totaling $40.6 billion.

This year’s biggest purchase was Salesforce buying Tableau for $15.7 billion, which would have been good for third place last year behind IBM’s mega deal plucking Red Hat for $34 billion and Broadcom grabbing CA Technologies for $18.8 billion.

Contributing to this year’s quieter activity was the fact that several typically acquisitive companies — Adobe, Oracle and IBM — stayed mostly on the sidelines after big investments last year. It’s not unusual for companies to take a go-slow approach after a big expenditure year. Adobe and Oracle bought just two companies each with neither revealing the prices. IBM didn’t buy any.

Microsoft didn’t show up on this year’s list either, but still managed to pick up eight new companies. It was just that none was large enough to make the list (or even for them to publicly reveal the prices). When a publicly traded company doesn’t reveal the price, it usually means that it didn’t reach the threshold of being material to the company’s results.

As always, just because you buy it doesn’t mean it’s always going to integrate smoothly or well, and we won’t know about the success or failure of these transactions for some years to come. For now, we can only look at the deals themselves.

Powered by WPeMatico

Back in 2013, Dropbox was scaling fast.

The company had grown quickly by taking advantage of cloud infrastructure from Amazon Web Services (AWS), but when you grow rapidly, infrastructure costs can skyrocket, especially when approaching the scale Dropbox was at the time. The company decided to build its own storage system and network — a move that turned out to be a wise decision.

In a time when going from on-prem to cloud and closing private data centers was typical, Dropbox took a big chance by going the other way. The company still uses AWS for certain services, regional requirements and bursting workloads, but ultimately when it came to the company’s core storage business, it wanted to control its own destiny.

Storage is at the heart of Dropbox’s service, leaving it with scale issues like few other companies, even in an age of massive data storage. With 600 million users and 400,000 teams currently storing more than 3 exabytes of data (and growing) if it hadn’t taken this step, the company might have been squeezed by its growing cloud bills.

Controlling infrastructure helped control costs, which improved the company’s key business metrics. A look at historical performance data tells a story about the impact that taking control of storage costs had on Dropbox.

In March of 2016, Dropbox announced that it was “storing and serving” more than 90% of user data on its own infrastructure for the first time, completing a 3-year journey to get to this point. To understand what impact the decision had on the company’s financial performance, you have to examine the numbers from 2016 forward.

There is good financial data from Dropbox going back to the first quarter of 2016 thanks to its IPO filing, but not before. So, the view into the impact of bringing storage in-house begins after the project was initially mostly completed. By examining the company’s 2016 and 2017 financial results, it’s clear that Dropbox’s revenue quality increased dramatically. Even better for the company, its revenue quality improved as its aggregate revenue grew.

Powered by WPeMatico

In Marc Benioff’s book, Trailblazer, he tells the tale of how Steve Jobs planted the seeds of the idea that would become the first enterprise app store, and how Benioff eventually paid Jobs back with the gift of the AppStore.com domain.

While Salesforce did truly help blaze a trail when it launched as an enterprise cloud service in 1999, it took that a step further in 2006 when it became the first SaaS company to distribute related services in an online store.

In an interview last year around Salesforce’s 20th anniversary, company CTO and co-founder Parker Harris told me that the idea for the app store came out of a meeting with Steve Jobs three years before AppExchange would launch. Benioff, Harris and fellow co-founder Dave Moellenhoff took a trip to Cupertino in 2003 to meet with Jobs. At that meeting, the legendary CEO gave the trio some sage advice: to really grow and develop as a company, Salesforce needed to develop a cloud software ecosystem. While that’s something that’s a given for enterprise SaaS companies today, it was new to Benioff and his team in 2003.

As Benioff tells it in his book, he asked Jobs to elucidate on what he meant by an application ecosystem. Jobs replied that how he implemented the idea was up to him. It took some time for that concept to bake, however. Benioff wrote that the notion of an app store eventually came to him as an epiphany at dinner one night a few years after that meeting. He says that he sketched out that original idea on a napkin while sitting in a restaurant:

One evening over dinner in San Francisco, I was struck by an irresistibly simple idea. What if any developer from anywhere in the world could create their own applications for the Salesforce platform? And what if we offered to store these apps in an online directory that allowed any Salesforce user to download them?

Whether it happened like that or not, the app store idea would eventually come to fruition, but it wasn’t originally called the AppExchange, as it is today. Instead, Benioff says he liked the name AppStore.com so much that he had his lawyers register the domain the next day.

When Benioff talked to customers prior to the launch, while they liked the concept, they didn’t like the name he had come up with for his online store. He eventually relented and launched in 2006 with the name AppExchange.com instead. Force.com would follow in 2007, giving programmers a full-fledged development platform to create applications, and then distribute them in AppExchange.

Meanwhile, AppStore.com sat dormant until 2008, when Benioff was invited back to Cupertino for a big announcement around iPhone. As Benioff wrote, “At the climactic moment, [Jobs] said [five] words that nearly floored me: ‘I give you App Store.”

Benioff wrote that he and his executives actually gasped when they heard the name. Somehow, even after all that time had passed since that the original meeting, both companies had settled upon the same name. Except Salesforce had rejected it, leaving an opening for Benioff to give a gift to his mentor. He says that he went backstage after the keynote and signed over the domain to Jobs.

In the end, the idea of the web domain wasn’t even all that important to Jobs in the context of an app store concept. After all, he put the App Store on every phone, and it wouldn’t require a website to download apps. Perhaps that’s why today the domain points to the iTunes store, and launches iTunes (or gives you the option of opening it).

Even the App Store page on Apple.com uses the sub-domain “app-store” today, but it’s still a good story of how a conversation between Jobs and Benioff would eventually have a profound impact on how enterprise software was delivered, and how Benioff was able to give something back to Jobs for that advice.

Powered by WPeMatico

InsightFinder, a startup from North Carolina based on 15 years of academic research, wants to bring machine learning to system monitoring to automatically identify and fix common issues. Today, the company announced a $2 million seed round.

IDEA Fund Partners, a VC out of Durham, N.C., led the round, with participation from Eight Roads Ventures and Acadia Woods Partners. The company was founded by North Carolina State University professor Helen Gu, who spent 15 years researching this problem before launching the startup in 2015.

Gu also announced that she had brought on former Distil Networks co-founder and CEO Rami Essaid to be chief operating officer. Essaid, who sold his company earlier this year, says his new company focuses on taking a proactive approach to application and infrastructure monitoring.

“We found that these problems happen to be repeatable, and the signals are there. We use artificial intelligence to predict and get out ahead of these issues,” he said. He adds that it’s about using technology to be proactive, and he says that today the software can prevent about half of the issues before they even become problems.

If you’re thinking that this sounds a lot like what Splunk, New Relic and Datadog are doing, you wouldn’t be wrong, but Essaid says that these products take a siloed look at one part of the company technology stack, whereas InsightFinder can act as a layer on top of these solutions to help companies reduce alert noise, track a problem when there are multiple alerts flashing and completely automate issue resolution when possible.

“It’s the only company that can actually take a lot of signals and use them to predict when something’s going to go bad. It doesn’t just help you reduce the alerts and help you find the problem faster, it actually takes all of that data and can crunch it using artificial intelligence to predict and prevent [problems], which nobody else right now is able to do,” Essaid said.

For now, the software is installed on-prem at its current set of customers, but the startup plans to create a SaaS version of the product in 2020 to make it accessible to more customers.

The company launched in 2015, and has been building out the product using a couple of National Science Foundation grants before this investment. Essaid says the product is in use today in 10 large companies (which he can’t name yet), but it doesn’t have any true go-to-market motion. The startup intends to use this investment to begin to develop that in 2020.

Powered by WPeMatico

The Daily Crunch is TechCrunch’s roundup of our biggest and most important stories. If you’d like to get this delivered to your inbox every day at around 9am Pacific, you can subscribe here.

1. VMware completes $2.7 billion Pivotal acquisition

VMware is closing the year with a significant new weapon in its arsenal. (I restrained myself from using a “pivotal” pun here. You’re welcome.)

The acquisition — first announced in August — helps the company in its transformation from a pure virtual machine supplier into a cloud native vendor that can manage infrastructure wherever it lives. It fits alongside the acquisitions of Heptio and Bitnami, two other deals that closed this year.

2. Spotify to ‘pause’ running political ads, citing lack of proper review

The company told us that starting early next year, it will stop selling political ads: “At this point in time, we do not yet have the necessary level of robustness in our processes, systems and tools to responsibly validate and review this content.”

3. ‘The Mandalorian’ returns for Season 2 on Disney+ in fall 2020

The last episode of the first season of “The Mandalorian” went live on Disney+ on Friday, and showrunner Jon Favreau wasted very little time confirming when we can expect season two of the smash hit to land: next fall.

4. 2019 Africa Roundup: Jumia IPOs, China goes digital, Nigeria becomes fintech capital

The last 12 months served as a grande finale to 10 years that saw triple-digit increases in startup formation and VC on the continent. Here’s an overview of the 2019 market events that capped off a decade in African tech.

5. Maxar is selling space robotics company MDA for around $765 million

Maxar’s goal in selling the business is to help alleviate some of its considerable debt. The purchasing entity is a consortium of companies led by private investment firm Northern Private Capital, which will acquire the entirety of MDA’s Canadian operations — responsible for the development of the Canadarm and Canadarm2 robotic manipulators used on the Space Shuttle and the International Space Station, respectively.

6. Cloud gaming is the future of game monetization, not gameplay

Lucas Matney argues that as is so often the case with the next big thing in tech, cloud streaming is much more likely to become the next big feature of a more traditional platform, rather than the entire platform itself. (Extra Crunch membership required.)

7. This week’s TechCrunch podcasts

Equity took the week off, but we kept Original Content going with a review of Netflix’s new fantasy show “The Witcher.”

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

It’s the second to last day of 2019, meaning we’re very nearly out of time this year; our space for repretrospection is quickly coming to a close. Before we do run out of hours, however, I wanted to peek at some data that former Kleiner Perkins investor and Packagd founder Eric Feng recently compiled.

Feng dug into the changing ratio between enterprise-focused Seed deals and consumer-oriented Seed investments over the past decade or so, including 2019. The consumer-enterprise split, a loose divide that cleaves the startup world into two somewhat-neat buckets, has flipped. Feng’s data details a change in the majority, with startups selling to other companies raising more Seed deals than upstarts trying to build a customer base amongst folks like ourselves in 2019.

The change matters. As we continue to explore new unicorn creation (quick) and the pace of unicorn exits (comparatively slow), it’s also worth keeping an eye on the other end of the startup lifecycle. After all, what happens with Seed deals today will turn into changes to the unicorn market in years to come.

Let’s peek at a key chart from Feng, talk about Seed deal volume more generally, and close by positing a few reasons (only one of which is Snap’s IPO) as to why the market has changed as much as it has for the earliest stage of startup investing.

Feng’s piece, which you can read here, tracks the investment patterns of startup accelerator Y Combinator against its market. We care more about total deal volume, but I can’t recommend the dataset enough if you have the time.

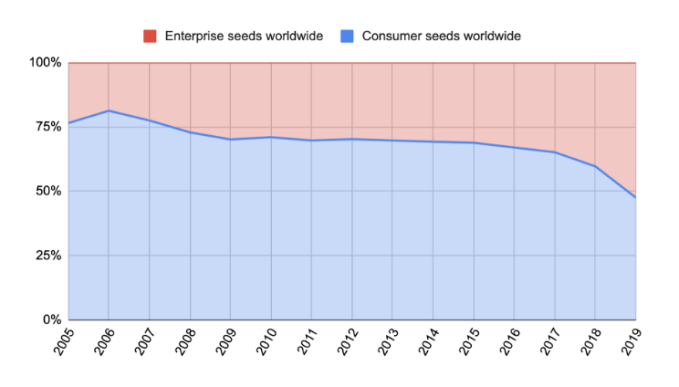

Concerning the universe of Seed deals, here’s Feng’s key chart:

Chart via Eric Feng / Medium

As you can see, the chart shows that in the pre-2008 era, Seed deals were amply skewed towards consumer-focused Seed investments. A new normal was found after the 2008 crisis, with just a smidge under 75% of Seed deals focused on selling to the masses for nearly a decade.

In 2016, however, a new trend emerged: a gradual decline in consumer Seed deals and a shift towards enterprise investments.

This became more pronounced in 2017, sharper in 2018, and by 2019 fewer than half of Seed deals focused on consumers. Now, more than half are targeting other companies as their future customer base. (Y Combinator, as Feng notes, got there first, making a majority of investments into enterprise startups since 2010, with just a few outlying classes.)

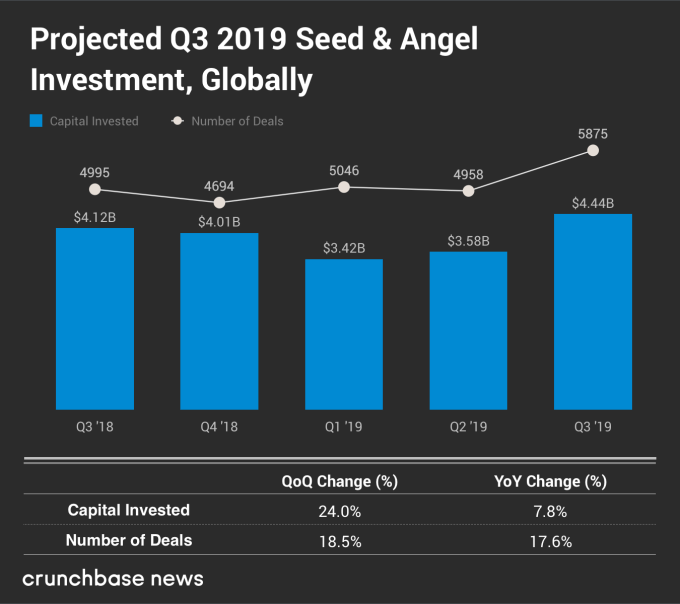

This flip comes as Seed deals sit at the 5,000-per-quarter mark. As Crunchbase News published as Q3 2019 ended, global Seed volume is strong:

So, we’re seeing a healthy number of deals as the consumer-enterprise ratio changes. This means that the change to more enterprise deals as a portion of all Seed investments isn’t predicated on their number holding steady while Seed deals dried up. Instead, enterprise deals are taking a rising share while volume appears healthy.

Now we get to the fun stuff; why is this happening?

As with many trends long in the making, there is no single reason why Seed investors have changed up their investing patterns. Instead, there are likely a myriad that added up to the eventual change. I’m going to ping a number of Seed investors this week to get some more input for us to chew on, but there are some obvious candidates that we can discuss today.

In no particular order, here are a few:

Powered by WPeMatico

VMware is closing the year with a significant new component in its arsenal. Today it announced it has closed the $2.7 billion Pivotal acquisition it originally announced in August.

The acquisition gives VMware another component in its march to transform from a pure virtual machine company into a cloud native vendor that can manage infrastructure wherever it lives. It fits alongside other recent deals like buying Heptio and Bitnami, two other deals that closed this year.

They hope this all fits neatly into VMware Tanzu, which is designed to bring Kubernetes containers and VMware virtual machines together in a single management platform.

“VMware Tanzu is built upon our recognized infrastructure products and further expanded with the technologies that Pivotal, Heptio, Bitnami and many other VMware teams bring to this new portfolio of products and services,” Ray O’Farrell, executive vice president and general manager of the Modern Application Platforms Business Unit at VMware, wrote in a blog post announcing the deal had closed.

Craig McLuckie, who came over in the Heptio deal and is now VP of R&D at VMware, told TechCrunch in November at KubeCon that while the deal hadn’t closed at that point, he saw a future where Pivotal could help at a professional services level, as well.

“In the future when Pivotal is a part of this story, they won’t be just delivering technology, but also deep expertise to support application transformation initiatives,” he said.

Up until the closing, the company had been publicly traded on the New York Stock Exchange, but as of today, Pivotal becomes a wholly owned subsidiary of VMware. It’s important to note that this transaction didn’t happen in a vacuum, where two random companies came together.

In fact, VMware and Pivotal were part of the consortium of companies that Dell purchased when it acquired EMC in 2015 for $67 billion. While both were part of EMC and then Dell, each one operated separately and independently. At the time of the sale to Dell, Pivotal was considered a key piece, one that could stand strongly on its own.

Pivotal and VMware had another strong connection. Pivotal was originally created by a combination of EMC, VMware and GE (which owned a 10% stake for a time) to give these large organizations a separate company to undertake transformation initiatives.

It raised a hefty $1.7 billion before going public in 2018. A big chunk of that came in one heady day in 2016 when it announced $650 million in funding led by Ford’s $180 million investment.

The future looked bright at that point, but life as a public company was rough, and after a catastrophic June earnings report, things began to fall apart. The stock dropped 42% in one day. As I wrote in an analysis of the deal:

The stock price plunged from a high of $21.44 on May 30th to a low of $8.30 on August 14th. The company’s market cap plunged in that same time period falling from $5.828 billion on May 30th to $2.257 billion on August 14th. That’s when VMware admitted it was thinking about buying the struggling company.

VMware came to the rescue and offered $15.00 a share, a substantial premium above that August low point. As of today, it’s part of VMware.

Powered by WPeMatico

Salesforce turned 20 this year, and the most successful pure enterprise SaaS company ever showed no signs of slowing down. Consider that the company finished the year on an $18 billion run rate, rushing toward its 2022 revenue goal of $20 billion. Oh, and it also spent a tidy $15.7 billion to buy Tableau this year in the most high-profile and expensive acquisition it’s ever made.

Co-founder, chairman and CEO Marc Benioff published a book called Trailblazer about running a socially responsible company, and made the rounds promoting it. In fact, he even stopped by TechCrunch Disrupt in San Francisco in September, telling the audience that capitalism as we know it is dead. Still, the company announced it was building two more towers in Sydney and Dublin.

It also promoted Bret Taylor just last week, who could be in line as heir apparent to Benioff and co-CEO Keith Block whenever they decide to retire. The company closed the year with a bang with a $4.5 billion quarter. Salesforce, for the most part, has somehow been able to balance Benioff’s vision of responsible capitalism while building a company makes money in bunches, one that continues to grow and flourish, and that’s showing no signs of slowing down anytime soon.

The company just keeps churning out good quarters. Here’s what this year looked like:

Powered by WPeMatico