Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

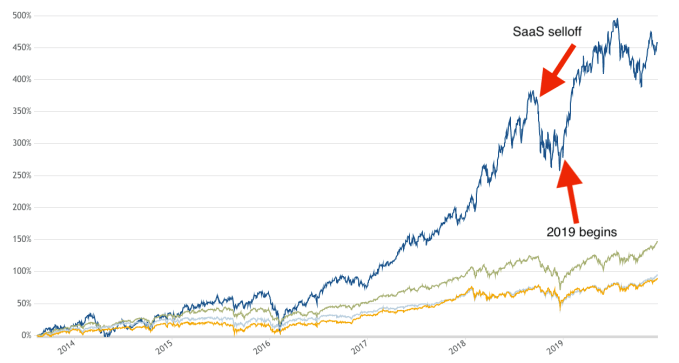

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today, something short. Continuing our loose collection of looks back of the past year, it’s worth remembering two related facts. First, that this time last year SaaS stocks were getting beat up. And, second, that in the ensuing year they’ve risen mightily.

If you are in a hurry, the gist of our point is that the recovery in value of SaaS stocks probably made a number of 2019 IPOs possible. And, given that SaaS shares have recovered well as a group, that the 2020 IPO season should be active as all heck, provided that things don’t change.

Let’s not forget how slack the public markets were a year ago for a startup category vital to venture capital returns.

We’re depending on Bessemer’s cloud index today, renamed the “BVP Nasdaq Emerging Cloud Index” when it was rebuilt in October. The Cloud Index is a collection of SaaS and cloud companies that are trackable as a unit, helping provide good data on the value of modern software and tooling concerns.

If the index rises, it’s generally good news for startups as it implies that investors are bidding up the value of SaaS companies as they grow; if the index falls, it implies that revenue multiples are contracting amongst the public comps of SaaS startups.*

Ultimately, startups want public companies that look like them (comps) to have sky-high revenue multiples (price/sales multiples, basically). That helps startups argue for a better valuation during their next round; or it helps them defend their current valuation as they grow.

Given that it’s Christmas Eve, I’m going to present you with a somewhat ugly chart. Today I can do no better. Please excuse the annotation fidelity as well:

Powered by WPeMatico

F5 got an expensive holiday present today, snagging startup Shape Security for approximately $1 billion.

What the networking company gets with a shiny red ribbon is a security product that helps stop automated attacks like credential stuffing. In an article earlier this year, Shape CTO Shuman Ghosemajumder explained what the company does:

We’re an enterprise-focused company that protects the majority of large U.S. banks, the majority of the largest airlines, similar kinds of profiles with major retailers, hotel chains, government agencies and so on. We specifically protect them against automated fraud and abuse on their consumer-facing applications — their websites and their mobile apps.

F5 president and CEO François Locoh-Donou sees a way to protect his customers in a comprehensive way. “With Shape, we will deliver end-to-end application protection, which means revenue generating, brand-anchoring applications are protected from the point at which they are created through to the point where consumers interact with them—from code to customer,” Locoh-Donou said in a statement.

As for Shape, CEO Derek Smith said that it wasn’t a huge coincidence that F5 was the buyer, given his company was seeing F5 consistently in its customers. Now they can work together as a single platform.

Shape launched in 2011 and raised $183 million, according to Crunchbase data. Investors included Kleiner Perkins, Tomorrow Partners, Norwest Venture Partners, Baseline Ventures and C5 Capital. In its most recent round in September, the company raised $51 million on a valuation of $1 billion.

F5 has been in a spending mood this year. It also acquired NGINX in March for $670 million. NGINX is the commercial company behind the open-source web server of the same name. It’s worth noting that prior to that, F5 had not made an acquisition since 2014.

It was a big year in security M&A. Consider that in June, four security companies sold in one three-day period. That included Insight Partners buying Recorded Future for $780 million and FireEye buying Verodin for $250 million. Palo Alto Networks bought two companies in the period: Twistlock for $400 million and PureSec for between $60 and $70 million.

This deal is expected to close in mid-2020, and is of course, subject to standard regulatory approval. Upon closing Shape’s Smith will join the F5 management team and Shape employees will be folded into F5. The company will remain in its Santa Clara headquarters.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week Kate was in SF, Alex was in Providence and there was a mountain of news to shovel through. If you’re here because we mentioned linking to a certain story in the show notes, that’s here. For everyone else, let’s get into the agenda.

We kicked off with a look at three new venture funds. In order:

From there we turned to the gender imbalance in the world of venture capital. This year, companies founded by women raised only 2.8% of capital. These not-so-stellar statistics are always worth digging into.

We then took a quick look at two different venture rounds, including ProdPerfect’s $13 million Series A and Pepper’s smaller $5.6 million round. ProdPerfect’s round was led by Anthos Capital (known for investing in Honey, which sold for $4 billion). The company has $2 million in ARR and is growing quickly. Pepper, formed by former Snap denizens, is working to help other startups lower their CAC costs in-channel. Smart.

And finally, Alex wanted to bring up his series on startups that reach the $100 million ARR threshold (Extra Crunch membership required). A first piece looking into the idea led to a few more submissions. There seem to be enough companies to name the grouping with something nice. Centurion? Centipede? Centaur? We’re working on it.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Extra Crunch community perks have a new offer from voice meeting notes service, Otter.ai. Starting today, annual and two-year Extra Crunch members can receive 25% off an annual plan for Otter Premium or Otter for Teams.

Otter.ai is an AI-powered assistant that generates rich notes from meetings, interviews, lectures and other voice conversations. You can record, review, search and edit the notes in real time, and organize the conversations from any device. We also use Otter.ai regularly here at TechCrunch to produce transcripts and voice notes from panels at our events, and it’s a great way to easily organize and search the conversations. Learn more about Otter.ai here.

To qualify for the Otter.ai community perk from Extra Crunch, you must be an annual or two-year Extra Crunch member. The 25% discount only applies to annual plans with Otter.ai, but it can be used for either the Premium or Teams plan. You can learn more about the pricing for Otter.ai here, and you can sign up for Extra Crunch here.

Extra Crunch is a membership program from TechCrunch that features how-tos and interviews on company building, intelligence on the most disruptive opportunities for startups, an experience on TechCrunch.com that’s free of banner ads, discounts on TechCrunch events and several community perks like the one mentioned in this article. Our goal is to democratize information about startups, and we’d love to have you join our community.

You can sign up for Extra Crunch here.

After signing up for an annual or two-year Extra Crunch membership, you’ll receive a welcome email with a link to sign up for Otter.ai and claim the discount. Otter.ai offers a free plan with capped minutes, and if you are interested in unlocking the full potential, you can purchase the annual plan with the 25% discount.

If you are already an annual or two-year Extra Crunch member, you will receive an email with the offer at some point over the next 24 hours. If you are currently a monthly Extra Crunch subscriber and want to upgrade to annual in order to claim this deal, head over to the “my account” section on TechCrunch.com and click the “upgrade” button.

This is one of several community perks we’ve launched for Extra Crunch annual members. Other community perks include a 20% discount on TechCrunch events, 100,000 Brex rewards points upon credit card sign up and an opportunity to claim $1,000 in AWS credits. For a full list of perks from partners, head here.

If there are other community perks you want to see us add, please let us know by emailing travis@techcrunch.com.

Sign up for an annual Extra Crunch membership today to claim this community perk. You can purchase an annual Extra Crunch membership here.

Disclaimer:

This offer is provided as a business partnership between TechCrunch and Otter.ai, but it is not an endorsement from the TechCrunch editorial team. TechCrunch’s business operations remain separate to ensure editorial integrity.

Powered by WPeMatico

What’s the most successful pure SaaS company of all time? The answer is Salesforce, and it’s no contest — the company closed the year on an $18 billion run rate, placing it in a category no other company born in the cloud can touch.

That Salesforce is on such an impressive run rate might suggest that reaching a billion in revenue is a fairly easy proposition for an enterprise SaaS company, but firms in this category grow or drive revenue like Salesforce. Some, in fact, find themselves growing much more slowly than anyone thought, but keep slugging it out as they inch steadily toward the $1 billion mark. This happens to public and private SaaS companies alike, which means that we can look at few public ones thanks to their regular earnings disclosures.

It’s a good time to look back at the year and analyze a few firms that should reach the mythical $1 billion in revenue at some point. Today we’re examining Zuora, a SaaS player focused on building and managing subscription-based services. GuideWire, a company transitioning to SaaS with big ambitions and Box, a well-known SaaS player caught somewhere between big and a billion.

We’ll start with the smallest company that caught our eye, Zuora . We’ll proceed from here going up in revenue terms.

Zuora is as pure a SaaS company as you can imagine. The San Mateo-based company raised nearly a quarter billion dollars while private to build out the technology that other companies use to help build their own subscription-based businesses. To some degree, Zuora’s success can be viewed as a proxy for SaaS as a whole.

However, while SaaS has chugged along admirably, Zuora has seen its share price fall by more than half in recent quarters.

At issue is the firm’s slowing growth:

Why is Zuora’s growth slowing? There’s no single reason to point out. Reading through coverage of the firm’s earnings report reveals a number of issues that the company has dealt with this year, including slow sales rep ramp and some technology complaints. Add in Stripe’s meteoric rise (the unicorn added tools for subscription billing in 2018, expanding the product to Europe earlier this year) and you can see why Zuora has had a tough year.

Adding to its difficulties, the company has lost more money while its growth has slowed. Zuora’s net loss expanded from $53.6 million in the three calendar quarters of 2018. That rose to $59.9 million over the same period in 2019. But the news is not all bad.

In spite of these numbers, Zuora is still growing; the company expects around $276 to $278 million in revenue in its current fiscal year and between $206 and $207 million in subscription top-line revenue over the same period.

At the revenue growth pace set in its most recent quarter (17% in the third quarter of its fiscal 2020) the company is eight years from reaching $1 billion in revenue. However, Zuora’s rising subscription growth rate in the same period is very encouraging. And, the company’s cash burn is declining. Indeed, in the most recent quarter Zuora’s operations generated cash. That improvement led to the firm’s free cash flow improving by half in the first three calendar quarters of 2019.

It also has pedigree on its side. Founder and CEO Tien Tzuo was employee number 11 at Salesforce when the company launched in 1999. He left the company in 2007 to start Zuora after realizing that traditional accounting methods designed to account for selling a widget wouldn’t work in the subscription world.

Zuora’s subscription revenue is high-margin, but the rest of its revenue (services, mostly) is not. So, with less thirst for cash and modestly improving subscription revenue growth, Zuora is still on the path towards the next revenue threshold despite a rough past year.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re exploring the 2019 IPO cohort from a capital-in perspective. How much did tech companies going public in 2019 raise before they went public, and what impact that did that have on their valuation when they debuted?

Looking ahead, the tech startups and other venture-backed companies expected to go public in 2020 will include a similar mix of mid-sized offerings, unicorn debuts and perhaps a huge direct listing. What we’ve seen in 2019 should be a good prelude to the 2020 IPO market.

With that in mind, let’s examine how much money tech companies that went public this year raised before their IPO. Spoiler: It’s a lot more than was normal just a few years ago. Afterwards, I have a question regarding what to call companies in the $100 million ARR club (more here) that we’ve been exploring lately. Let’s go!

According to CBInsights’ recent IPO 2020 IPO report, there’s a sharp, upward swing in the amount of capital that tech companies raise before they go public. It’s so steep that the data draw a nearly linear breakout from a preceding, comfortable normal.

Here’s the chart:

There are two distinct periods; from 2012 to 2015, raising up to $100 million was the norm (median) for tech companies going public. That’s still a lot of cash, mind.

The second period is more exciting. From 2016 on we can see a private capital arms race in which tech companies going public stacked ever-greater sums under their mattresses before debuting. This is generally consistent with a different trend that you are also aware of, namely the rise of $100 million financings.

Before we turn back to the CBInsights data, let’s observe a chart from Crunchbase News that underscores the simply astounding rise of $100 million financings that was published just a few weeks ago. As you look at this chart, remember that prior to 2016, more than half of venture-backed technology companies going public had raised less than $100 million total:

Now, compare the two data sets.

Powered by WPeMatico

The insurance industry, sleepy and ancient, is ripe for disruption. We’ve seen companies like Lemonade, Hippo and Rhino get in on that opportunity. Today, an insurtech company focused on small business insurance has raised $18 million to keep growing.

Meet Huckleberry, whose Series A was led by Tribe Capital, with participation from Amaranthine, Crosslink Capital and Uncork Capital.

Huckleberry launched in 2017 to offer business insurance, including workers’ compensation and general liability, all through an online portal.

Small business insurance coverage is not like car insurance or renters insurance. It’s not as simple as filling out a few forms and getting a quote. Even if a few platforms do have algorithms for providing quotes, you can’t really close the deal unless you get on the phone.

It’s an incredibly tedious and stressful process. In fact, Huckleberry co-founders Bryan O’Connell and Steve Au first came up with the idea for Huckleberry when they were seeking out their own small business coverage for a previous startup idea.

The industry itself is incredibly fragmented, which is caused in part by the fact that small business coverage underwriting varies wildly from business to business. For example, the policy for three or four restaurants might look relatively similar. However, a fast food restaurant might be identified as a higher risk with regards to workers’ compensation than a Michelin-star restaurant, where workers might be more eager to get back to work and take home their tip money. These differences come in the form of location, operations and many other factors, as well as business vertical.

Huckleberry has worked to build out myriad coverage verticals, including food and beverage, fitness, retail, legal, healthcare, hair and beauty and more.

The firm offers worker’s comp, as well as a package policy that includes general liability, property and business interruption insurance. Customers also can purchase add-ons like hired and non-owned auto insurance, employment practices liability insurance (EPLI), liquor liability insurance, employee dishonesty coverage, professional liability insurance, equipment breakdown coverage and spoilage coverage.

Huckleberry isn’t itself an insurance carrier, but does have the authority to underwrite and sell policies on behalf of the carrier. That said, Huckleberry’s expansion both by vertical and geography is more difficult than your average software startup. The regulatory landscape of insurance in the U.S. goes state by state.

“Our biggest challenge is navigating 50 states’ worth of extremely complicated regulations on something that is much more complicated than a software product,” said O’Connell. “We’re trying to protect individual workers and businesses all while staying fully compliant in every market.”

Powered by WPeMatico

Sapphire Ventures, the former corporate venture arm of SAP, has raised $1.4 billion for growth investments, including a $150 million opportunity fund to support larger deals.

The firm, which focuses primarily on enterprise tech companies in the U.S., Europe and Israel, writes checks to Series B through pre-IPO businesses. Its portfolio includes 23andMe, Sumo Logic and TransferWise.

The new funds brings Sapphire Ventures, which became independent from the German software company SAP in 2011, assets under management to north of $4 billion. Sapphire will write checks sized between $5 million and $100 million with the new funds, allowing the team “to do any financing we need to or want to,” chief executive officer and managing director Nino Marakovic tells TechCrunch. Sapphire’s fourth growth fund is the firm’s largest to date, at more than double the size of their $700 million Fund III.

“We need this fund because companies are staying private much longer because they want to get to a $200 million revenue run rate before they go public,” Sapphire Ventures president and co-founder Jai Das (pictured) tells TechCrunch. “We want to have the capital to support these companies as they keep growing.”

News of the fund comes nearly one year after Sapphire Ventures lassoed $115 million from new limited partners to invest at the intersection of tech, sports, media and entertainment. Sapphire Sport has ties to the sports industry, from City Football Group, which owns English Premier League team Manchester City, to Adidas, the owners of the Indiana Pacers, New York Jets, San Jose Sharks and Tampa Bay Lightning, among others.

Before that, the firm closed on $1 billion for its third flagship venture fund.

With seven check writers and another seven investment professionals focused on growth-stage investments, Sapphire has had a number of recent wins, counting a total of 21 initial public offerings and 55 exits since the firm’s inception.

“We’re excited to have now reached critical mass with $4 billion under management,” Marakovic said. “We are the right size to take advantage of our target area of early and later-stage enterprise software companies. We are innovating on the model by adding value-add LPs and trying to align our whole model of services to the target companies to serve them as best as possible.”

Powered by WPeMatico

Over the years, Google’s various whitepapers, detailing how the company solves specific problems at scale, have regularly spawned new startup ecosystems and changed how other enterprises think about scaling their own tools. Today, the company is publishing a new security whitepaper that details how it keeps its cloud-native architecture safe.

The name, BeyondProd, already indicates that this is an extension of the BeyondCorp zero trust system the company first introduced a few years ago. While BeyondCorp is about shifting security away from VPNs and firewalls on the perimeter to the individual users and devices, BeyondProd focuses on Google’s zero trust approach to how it connects machines, workloads and services.

Unsurprisingly, BeyondProd is based on pretty much the same principles as BeyondCorp, including network protection at the end, no mutual trust between services, trusted machines running known code, automated and standardized change rollout and isolated workloads. All of this, of course, focuses on securing cloud-native applications that generally communicate over APIs and run on modern infrastructure.

“Altogether, these controls mean that containers and the microservices running inside can be deployed, communicate with each other, and run next to each other, securely; without burdening individual microservice developers with the security and implementation details of the underlying infrastructure,” Google explains.

Google, of course, notes that it is making all of these features available to developers through its own services like GKE and Anthos, its hybrid cloud platform. In addition, though, the company also stresses that a lot of its open-source tools also allow enterprises to build systems that adhere to the same platforms, including the likes of Envoy, Istio, gVisor and others.

“In the same way that BeyondCorp helped us to evolve beyond a perimeter-based security model, BeyondProd represents a similar leap forward in our approach to production security,” Google says. “By applying the security principles in the BeyondProd model to your own cloud-native infrastructure, you can benefit from our experience, to strengthen the deployment of your workloads, how your their communications are secured, and how they affect other workloads.”

You can read the full whitepaper here.

Powered by WPeMatico

Belgium-based all-in-one business software maker Odoo, which offers an open source version as well as subscription-based enterprise software and SaaS, has taken in $90 million led by a new investor: Global growth equity investor Summit Partners.

The funds have been raised via a secondary share sale. Odoo’s executive management team and existing investor SRIW and its affiliate Noshaq also participated in the share sale by buying stock — with VC firms Sofinnova and XAnge selling part of their shares to Summit Partners and others.

“Odoo is largely profitable and grows at 60% per year with an 83% gross margin product; so, we don’t need to raise money,” a spokeswoman told us. “Our bottleneck is not the cash but the recruitment of new developers, and the development of the partner network.

“What’s unusual in the deal is that existing managers, instead of cashing out, purchased part of the shares using a loan with banks.”

The 2005-founded company — which used to go by the name of OpenERP before transitioning to its current open core model in 2015 — last took in a $10M Series B back in 2014, per Crunchbase.

Odoo offers some 30 applications via its Enterprise platform — including ERP, accounting, stock, manufacturing, CRM, project management, marketing, human resources, website, eCommerce and point-of-sale apps — while a community of ~20,000 active members has contributed 16,000+ apps to the open source version of its software, addressing a broader swathe of business needs.

It focuses on the SME business apps segment, competing with the likes of Oracle, SAP and Zoho, to name a few. Odoo says it has in excess of 4.5 million users worldwide at this point, and touts revenue growth “consistently above 50% over the last ten years”.

Summit Partners told us funds from the secondary sale will be used to accelerate product development — and for continued global expansion.

“In our experience, traditional ERP is expensive and frequently fails to adapt to the unique needs of dynamic businesses. With its flexible suite of applications and a relentless focus on product, we believe Odoo is ideally positioned to capture this large and compelling market opportunity,” said Antony Clavel, a Summit Partners principal who has joined the Odoo board, in a supporting statement.

Odoo’s spokeswoman added that part of the expansion plan includes opening an office in Mexico in January, and another in Antwerpen, Belgium, in Q3.

This report was updated with additional comment

Powered by WPeMatico