Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Applications networking company F5 announced today that it is acquiring Volterra, a multi-cloud management startup, for $500 million. That breaks down to $440 million in cash and $60 million in deferred and unvested incentive compensation.

Volterra emerged in 2019 with a $50 million investment from multiple sources, including Khosla Ventures and Mayfield, along with strategic investors like M12 (Microsoft’s venture arm) and Samsung Ventures. As the company described it to me at the time of the funding:

Volterra has innovated a consistent, cloud-native environment that can be deployed across multiple public clouds and edge sites — a distributed cloud platform. Within this SaaS-based offering, Volterra integrates a broad range of services that have normally been siloed across many point products and network or cloud providers.

The solution is designed to provide a single way to view security, operations and management components.

F5 president and CEO François Locoh-Donou sees Volterra’s edge solution integrating across its product line. “With Volterra, we advance our Adaptive Applications vision with an Edge 2.0 platform that solves the complex multi-cloud reality enterprise customers confront. Our platform will create a SaaS solution that solves our customers’ biggest pain points,” he said in a statement.

Volterra founder and CEO Ankur Singla, writing in a company blog post announcing the deal, says the need for this solution only accelerated during 2020 when companies were shifting rapidly to the cloud due to the pandemic. “When we started Volterra, multi-cloud and edge were still buzzwords and venture funding was still searching for tangible use cases. Fast forward three years and COVID-19 has dramatically changed the landscape — it has accelerated digitization of physical experiences and moved more of our day-to-day activities online. This is causing massive spikes in global Internet traffic while creating new attack vectors that impact the security and availability of our increasing set of daily apps,” he wrote.

He sees Volterra’s capabilities fitting in well with the F5 family of products to help solve these issues. While F5 had a quiet 2020 on the M&A front, today’s purchase comes on top of a couple of major acquisitions in 2019, including Shape Security for $1 billion and NGINX for $670 million.

The deal has been approved by both companies’ boards, and is expected to close before the end of March, subject to regulatory approvals.

Powered by WPeMatico

RedHat today announced that it’s acquiring container security startup StackRox . The companies did not share the purchase price.

RedHat, which is perhaps best known for its enterprise Linux products has been making the shift to the cloud in recent years. IBM purchased the company in 2018 for a hefty $34 billion and has been leveraging that acquisition as part of a shift to a hybrid cloud strategy under CEO Arvind Krishna.

The acquisition fits nicely with RedHat OpenShift, its container platform, but the company says it will continue to support StackRox usage on other platforms including AWS, Azure and Google Cloud Platform. This approach is consistent with IBM’s strategy of supporting multicloud, hybrid environments.

In fact, Red Hat president and CEO Paul Cormier sees the two companies working together well. “Red Hat adds StackRox’s Kubernetes-native capabilities to OpenShift’s layered security approach, furthering our mission to bring product-ready open innovation to every organization across the open hybrid cloud across IT footprints,” he said in a statement.

CEO Kamal Shah, writing in a company blog post announcing the acquisition, explained that the company made a bet a couple of years ago on Kubernetes and it has paid off. “Over two and half years ago, we made a strategic decision to focus exclusively on Kubernetes and pivoted our entire product to be Kubernetes-native. While this seems obvious today; it wasn’t so then. Fast forward to 2020 and Kubernetes has emerged as the de facto operating system for cloud-native applications and hybrid cloud environments,” Shah wrote.

Shah sees the purchase as a way to expand the company and the road map more quickly using the resources of Red Hat (and IBM), a typical argument from CEOs of smaller acquired companies. But the trick is always finding a way to stay relevant inside such a large organization.

StackRox’s acquisition is part of some consolidation we have been seeing in the Kubernetes space in general and the security space more specifically. That includes Palo Alto Networks acquiring competitor TwistLock for $410 million in 2019. Another competitor, Aqua Security, which has raised $130 million, remains independent.

StackRox was founded in 2014 and raised over $65 million, according to Crunchbase data. Investors included Menlo Ventures, Redpoint and Sequoia Capital. The deal is expected to close this quarter subject to normal regulatory scrutiny.

Powered by WPeMatico

Roblox is now one of the world’s most valuable private companies in the world after a monster Series H raise brings the social gaming platform a stratospheric $29.5 billion valuation. The company won’t be private for long, though.

The $520 million raise led by Altimeter Capital and Dragoneer Investment Group is a significant cash influx for Roblox, which had previously raised just over $335 million from investors according to Crunchbase. The Investment Group of Santa Barbara, Warner Music Group, and a number of current investors, also participated in this round.

In February of 2020, the company closed a $150 million Series G led by Andreessen Horowitz which valued the company at $4 billion.

The gaming startup had initially planned an IPO in 2020, but after the major first-day pops of DoorDash and Airbnb, the company leadership reconsidered their timeline, according to a report in Axios. Those major day-one share price pops left significant money on the table for the companies selling those shares, an outcome Roblox is likely looking to avoid. Today, the company also announced that it plans to enter the public markets via a direct listing.

Roblox’s 7x valuation multiple signals just how feverish public and private markets are for tech stocks. The valuation also highlights how investors foresee the company benefiting from pandemic trends which pushed more users online and toward social gaming platforms. In a 2019 prospectus, the company shared that it had 17.6 million users, now Roblox claims to have 31 million daily active users on its platform.

Powered by WPeMatico

The popular news app News Break is announcing that it has raised $115 million in new funding.

The press release claims this round makes News Break “one of the first new unicorns of 2021,” but the startup declined to disclose its actual valuation.

Founder and CEO Jeff Zheng said that when he started the company in 2015, the goal was to differentiate itself from other news aggregation apps by focusing on local news, and to “help or empower these local content creators.”

To be clear, you can find similar stories in News Break that you’d see in other news apps (there’s a whole section for coronavirus news, for example, and this morning you’ll see plenty of headlines about yesterday’s violent takeover of the U.S. Capitol), but you’ll also see plenty of stories that are highlighted specifically based on your location.

“Technology is interweaving with every aspect of the company — in how we empower local publishers and local journalists to generate content more effectively and to reach an online audience more effectively,” Zheng said. “We have AI tools to help provide all these relevant articles … We have location profiles and what you’re most interested in, which we basically match against the content.”

Jeff Zheng. Image Credits: News Break

The local focus may be increasingly valuable given the broader economic challenges facing the local news business — as Zheng put it, there’s “strong user demand” for local news but “weak supply.” And the strategy seems to have paid off for News Break so far, with the app reaching the top spot in the News category of Apple’s U.S. App Store multiple times (it’s currently ranked No. 4), and in Google Play as well. The startup says it’s currently reaching 12 million daily active users.

Zheng said that while News Break already shares ad revenue with publishers, he’s hopeful that the value it provides those publishers will only grow over time: “We want to give as much money back to the creators as possible.”

When I suggested that publishers and journalists may be leery about relying too much on a third-party platform to reach their audience, Zheng argued that News Break’s incentives are very different from the big internet and social media platforms.

“We are local-centric,” he said. “If local publishers are struggling, if the newspapers are diminishing every year, then sooner or later we are out of business.”

And while Zheng previously led Yahoo Labs in Beijing and was also founding CEO at Chinese news startup Yidian Zixun — plus, the startup has team members in Beijing and Shanghai — he emphasized that this is a “U.S. high-tech company incorporated in Delaware, headquartered in Mountain View,” with the majority of its workforce in the United States and a focus on the U.S. market. The distinction could become important if News Break continues to grow, given the U.S. government’s current attempts to ban some Chinese companies.

News Break previously raised $36 million in funding. The new round was led by Francisco Partners, which is taking a seat on the News Break board. IDG Capital also participated.

In a statement, Francisco Partners Principal Alan Ni said:

News Break’s breakout multi-year successes in the local news space is what first brought them to our attention. We are inspired by their mission and extremely impressed by the work they have done to bring local-news distribution into the 21st Century through cutting-edge machine learning and media savvy. We are thrilled to be partnering with News Break’s talented leadership team as they continue to drive local news innovations while also rapidly expanding their business into adjacent local verticals beyond news.

Powered by WPeMatico

The ongoing push for social distancing to slow the spread of COVID-19 has meant that more people than ever are using internet-based services to get things done. And that is having a direct impact on digital customer service, which is seeing unprecedented traffic and demands when things are not running smoothly. Today, one of the startups that’s built an interesting, very “hands-on” approach to addressing that problem is announcing a round of funding to expand its business.

Glia, which has built a platform that not only integrates and helps manage different customer support channels, but also provides tools to help agents proactively get into a customer’s app or web page to help them find things or fix issues, is today announcing that it has picked up $78 million in a Series C round of funding. Dan Michaeli, the co-founder and CEO who is based out of New York (the company has a substantial operation in Estonia too), said it will be used to continue developing its technology and expanding to address inbound interest for its services after seeing its revenues grow by 150% in 2020.

The company’s original focus was around financial services and it counts a large base of customers in that area, but it is also seeing a lot of activity in adjacent industries like insurance, as well as education, retail and other categories Michaeli said.

“We’ve had overwhelming demand and it’s incredible to see how businesses want to adopt us right now,” he said in an interview. “The plan is to significantly scale up and continue to define and meet that demand for digital customer service.” The company is likely also to use some of the funding for acquisitions in what appears to be a rapidly consolidating market.

The round is being led by Insight Partners, with Don Brown (an entrepreneur in the world of customer service, with his company Interactive Intelligence acquired by Genesys for $1.4 billion) also participating.

Glia isn’t disclosing other investors, but past backers include Tola Capital, Temerity Capital, Grassy Creek and Wildcat Capital, as well as Insight. Prior to this, the company, which has been around since 2012 and was previously known as SaleMove, had raised just $28 million and its valuation was a modest $69 million according to PitchBook data (and it’s not disclosing valuation today).

There are a lot of customer service startups in the market today, and a number of them are seeing huge boosts in their business, and even some consolidation as others snap up tech to make sure they have their own customer service strategies going in the right direction. (Witness Facebook of all companies acquiring omnichannel customer support and CRM leader Kustomer for $1 billion in November.)

Glia is not unlike many of the new guard of these companies, in that its focus is very squarely on providing a platform to be able to manage and interact across whatever digital channel a customer happens to be using. Glia, I should point out, means “glue” in Greek.

What makes Glia quite interesting and different from these are some of the twists it uses to engage with users. One of these involves being able to give agents the ability to actually get on the screen of the user in question, in order to both guide the user around the screen, and to see what the user is doing on that screen.

To be clear, the connection and ability to track what the user is doing is just on the screen in question, and it’s done with the user’s awareness of what is going on. In the demo of the service that I went through, it’s a very smooth service, which reminded me just a little of things like Clippy on Microsoft Word.

Alongside this, Glia provides tools to agents to coach them on questions to ask, phrasing to use and links for answers, and Glia also develops virtual customer service assistants, to help with more basic questions. These also have the ability to interact with people’s screens when they make contact with a company. This in effect sees the company combining a number of technologies in one place, from natural language to suggest (and in some cases run) customer service responses, through to computer vision to help detect what is going on on the remote screen, through to more fundamental CRM technology to run those services across multiple platforms.

While screen sharing has been a well-used tool in other areas — for example in workforce collaboration environments, or for presenting online — Glia is seen as one of the pioneers in leveraging that for customer service. For investors, the interest in Glia has been to tap into that.

“We are proud to expand our investment in Glia as the company continues to lead the evolution of Digital Customer Service for businesses across the globe,” said Lonne Jaffe, managing director at Insight Partners, in a statement. “Glia’s platform provides the modern technology necessary for businesses to meet customers in their digital journeys and communicate through the customer’s channel of choice. With this capital, the company will continue to scale and keep up with skyrocketing demand.”

We are in a key moment of digital transformation in customer services. Surprisingly, there are still many who opt for calling in to ask questions, but as Michaeli noted, these days, even when they are still using phones, customers will do so with “their screens in front of them.”

Brown believes that this is the other opportunity to seize. “Many companies are still focused on moving antiquated, on-premises telephony systems to cloud contact centers that essentially offer the same functionality,” he said in a statement. “Instead, businesses can leapfrog this process and move directly to a digital-first cloud approach by partnering with Glia. If I were to build Interactive Intelligence for today’s contact center, I would take Glia’s approach.”

Powered by WPeMatico

As the pandemic took hold in 2020, companies accelerated their move to cloud services. Lacework, the cloud security startup, was in the right place at the right time as customers looked for ways to secure their cloud native workloads. The company reported that revenue grew 300% year over year for the second straight year.

It was rewarded for that kind of performance with a $525 million Series D today. It did not share an exact valuation, only saying that it exceeded $1 billion, which you would expect on such a hefty investment. Sutter Hill and Altimeter Capital led the round with help from D1 Capital Management, Coatue, Dragoneer Investment Group, Liberty Global Ventures, Snowflake Ventures and Tiger Global Management. The company has now raised close to $600 million.

Lacework CEO Dan Hubbard says one of the reasons for such widespread interest from investors is the breadth of the company’s security solution. “We enable companies to build securely in the cloud, and we span across multiple different categories of markets, which enable the customers to do that,” he said.

He says that encompasses a range of services, including configuration and compliance, security for infrastructure as code, build time and runtime vulnerability scanning and runtime security for cloud native environments like Kubernetes and containers.

As the company has grown revenue, it has been adding employees quickly. It started the year with 92 employees and closed with more than 200, with plans to double that by the end of this year. As he looks at hiring, Hubbard is aware of the need to build a diverse organization, but acknowledges that tech in general hasn’t done a great job so far.

He says they are working with the various teams inside the company to try and change that, while also working to support outside organizations that are helping educate underrepresented groups to get the skills they need and then building from that. “If you can help solve the problem at an earlier stage, then I think you’ve got a bigger opportunity [to have a base of people to hire] there,” he said.

The company was originally nurtured inside Sutter Hill and is built on top of the Snowflake platform. It reports that $20 million of today’s total comes from Snowflake’s new venture arm, which is putting some money into an early partner.

“We were an alpha Snowflake customer, and they were an alpha customer of ours. Our platform is built on top of the Snowflake data cloud and their new venture arm has also joined the round with an investment to further strengthen the partnership there,” Hubbard said.

As for Sutter Hill, investor Mike Speiser sees Lacework as one of his firm’s critical investments. “[Much] like Snowflake at a similar point in its evolution, Lacework is growing revenue at over 300% per year making Lacework one of Sutter Hill Ventures’ most important and promising portfolio companies,” he said in a statement.

Powered by WPeMatico

Revenue-based investing (RBI), also known as revenue-based financing, or revenue-share investing,1 is a natural next step for the private equity and early-stage venture investment industry. However, due to RBI being a relatively new model, publicly available data is limited.

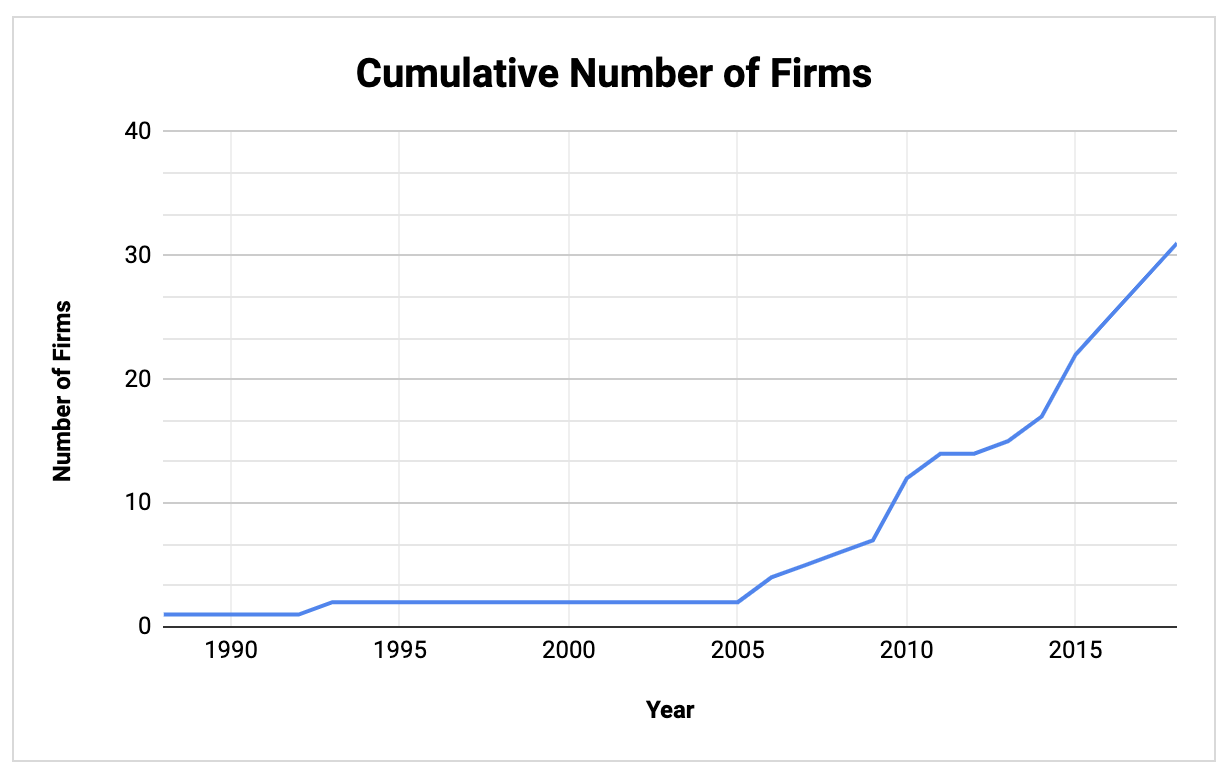

To address this foundational gap in market information, we have developed a proprietary data set of 32 RBI investment firms, 57 distinct funds and 134 companies that have secured revenue-based investing.

Bootstrapp developed this extensive analysis on revenue-based investing for the purpose of accelerating the shift toward greater transparency and standardization within the industry.

Upon thoroughly analyzing the data, we’ve been able to identify the total number of investment firms and amount of capital that comprise the RBI industry, the specific verticals and business models that are most actively leveraging RBI, and the typical profile of companies that access this form of capital.

These findings are summarized below; a full industry-spanning report that defines the overall revenue-based investing market as it stands today is available to download here.

As context, the financial structures used by VCs haven’t evolved much since they first emerged in 1957. Today, the model is almost precisely the same, with only incremental changes such as more efficient capital markets and industry standards for structuring deals, pricing companies and more.

More recently, we have seen numerous new investment models and financing instruments, including shared earnings agreements and point-of-sale capital. One of the most prominent and popular new models for investors is revenue-based investing (RBI).

However, because the model is new, there is a lack of publicly available data, industry standards have not yet been fully established, and similarly to the equity investment market, there is little transparency into the cost of capital that investees truly pay in exchange for taking on a revenue-based investment.

Thankfully, there have been some notable efforts to drive transparency in the RBI market. For example, Bigfoot Capital open-sourced its RBI model, outlining it in a blog post and sharing their RBI financial model and anonymized term sheet, but a thorough, quantitative, industry-wide analysis has not been conducted until now.

In order to raise RBI, the company must normally be generating revenue, but is not necessarily required to be profitable, although profitability, or at least a near-term path to profitability, is often an important criteria for many investors. “For startups with revenue, RBI may be a good option because, even though the startup may not be profitable, it can reduce dilution — especially for founders,” said Emily Campbell of The Campbell Firm PLLC, a law firm that represents serial entrepreneurs and venture-backed businesses.

“Taking in some smart equity or convertible debt and balancing that money with other financing can be a good strategy for a startup,” she said. Profitability decreases the risk of default and assures that the investee has the ability to service the debt.

In regards to the applications that are best suited to RBI, B2B software-as-a-service (SaaS) companies rise to the top of the list primarily because one is able to — in essence — securitize the revenue being generated by a company and then lend capital against that theoretical security. In addition to SaaS companies, RBI is being used quite frequently in the impact investing community as it solves the problem of a lack of normal M&A or IPO exit paths for impact-driven companies and are sometimes marketed as a nonextractive form of investment structure.

Beyond B2B SaaS and impact investing, many other verticals are adopting the model as well, including e-commerce/D2C, consumer software, food and beverage, and more. It ought to be noted, however, that regardless of the specific business model a company employs, the investee is typically required to have repeatable sales and a track record that demonstrates a strong revenue stream, and therefore a clear ability to return the capital to the investors.

We have identified 32 U.S.-based firms actively investing via a revenue-based investing instrument, with those firms managing 57 distinct funds representing an estimated $4.31 billion in capital. Through our analysis of those firms, funds and investees, we found that:

Firms were included in the data set (and by extension, determined to be actively making revenue-based investments) if they:

The specific number of firms we believe to be quite accurate, representing only active, U.S.-based revenue-based investing firms. The number of funds, however, may be underestimated. This is due to the fact that, although each firm is associated with at least one fund, we did not include additional funds beyond that unless they were confirmed through other sources, such as the firms’ public communications, their SEC Form D or other sources as outlined in the methodology section at the conclusion of the full report.

The total amount of RBI capital that has already been allocated to companies across all firms and all years is $2.1 billion. However, it should be noted that this includes the outliers in our dataset, namely Kapitus, Clearbanc, Braavo and United Capital Source. Once we remove those firms, the remaining 28 firms, representing 51 funds, have allocated $592.8 million.

This figure of $592.8 million is almost certainly an underestimate due to the fact that only 19 of 32 firms had a known “amount of allocated capital,” whereas the remaining 13 firms have unknown values (i.e., zeros) for the amount of capital they have allocated thus far. Therefore, if all 32 firms had a valid and confirmed amount of allocated capital, we can logically conclude that the number would rise dramatically from the current figure of $592.8 million.

New RBI firms have been founded every year since 2013. In 2010, five firms were founded and in 2015 four additional firms were founded, then from 2014-2019, two or more firms were founded each year.

Image Credits: Bootstrapp (opens in a new window)

Clearly, there has been a major uptick in RBI firms being founded since 2005, with a relatively consistent number of new firms being founded over the 15 years since then. In the last 10 years alone, 25 RBI firms have been founded.

Powered by WPeMatico

In 2020, venture capitalists unceremoniously broke up with D2C brands and product-based businesses.

Many watched as the consumer brands in their portfolios rushed to make hefty layoffs and eke out more runway and grew more concerned with their business models.

Some simply monitored the “lackluster” Casper IPO or skimmed articles about Brandless and others “imploding” and started pulling a slow fade on D2C brands — not taking pitches, not following up.

Many product-based brands, as it turns out, are no longer interested in chasing venture capital.

Last year, investors adopted a wait-and-see approach to all new investments and prayed portfolio brands could cut their burn significantly enough, stay relevant and ride things out.

Product-based businesses fell out of favor and venture capitalists, if they did invest last year, mainly focused on AI startups, or companies focused on data collaboration, data privacy and healthcare (mostly founded by men, might I add).

From a distance, it sounds like direct-to-consumer founders were left destitute and desperate for financing, wounded by every slow fade or hard pass, beholden as ever to the whims of Silicon Valley.

But as Hal Koss so eloquently shared in his “DTC playbook” post-mortem, this wasn’t a one-way breakup; this parting of ways is actually mutual. Many product-based brands, as it turns out, are no longer interested in chasing venture capital, playing the “grow-at-all-costs” game and relinquishing partial control to investors, despite the pandemic and the uncertain circumstances many founders find themselves facing.

Through my work running and scaling Bulletin, I’ve followed thousands of product-based businesses ranging from indie beauty brands selling clean serums and cleansers to sex tech companies making couples’ vibrators and foreplay accessories. I’ve followed them on Instagram, in the press and across various platforms, and in many cases, I’ve spoken to their founders directly.

Over the past two years, I interviewed executives at more than 30 women-owned businesses for my upcoming book, “How to Build a Goddamn Empire,” and had long phone calls with dozens of independent brands and makers as Bulletin got a handle on how the pandemic was impacting customers. And I noticed something new and remarkable about what founders want now, in 2021, compared to what they wanted in years past.

Back then, I’d get dozens of cold emails and DMs asking how I successfully raised VC and what the unspoken rules might be. I’d hear from business owners who were considering a raise or gearing up for one. Product-based entrepreneurs approached me at panels or Bulletin events and say they wanted to be the “Glossier for X” or the “Away for Y.” Many younger founders didn’t even know what venture capital really was, but they saw it as symbolic validation for the business, or the only way to get “big.”

Now, brands would rather scrape by than pursue an injection of funding on someone else’s terms; just ask the Gorjana founders or Scott Sternberg. Many brands that saw astronomical growth in 2020, like Rosen, Golde, Entireworld and others that spurred similar growth for Etsy and Shopify are fully bootstrapped businesses, and proudly so.

Some founders I’ve spoken to have even outright rejected offers for investment. A lot of D2C brands are interested in learning about alternative forms of financing like bank loans, lines of credit and crowdfunding, and ask about iFundWomen or Kickstarter, observing the success of other fully crowdfunded brands like Dame and Pepper.

Venture capital, from my vantage point, has lost its sheen for a lot of product-based brands. They’re not destitute and desperate for financing. They’re actually scoffing at the prospect and trusting they can succeed, scale and maintain long-term profitability without swapping equity for cash. They’re tripped up by what they’ve been reading in the media, or they’ve survived or even thrived during COVID, as a fully bootstrapped company, and feel more conviction than ever that the “grow slow” approach is the right move.

They’re reading the same stories about layoffs and tenuous unit economics at massive D2C companies and agreeing with Sam Kaplan that the old playbook — pricey customer acquisition practices, rapid scale, endless rounds of funding — is out of date. It’s 2021 and we’re midpandemic. These brands want to turn a profit.

Powered by WPeMatico

The new year is off to a busy IPO start. As The Exchange reported a few weeks ago, investors anticipate a busy Q1 IPO cycle, followed by a slower Q2 and a busy Q3 and Q4.

With Affirm releasing an initial IPO price range last night and Poshmark repeating the feat this morning, private-market investor expectations are holding up thus far.

Secondhand fashion marketplace Poshmark anticipates its IPO could price between $35 and $39 per share. Using its simple share count, the former startup could be worth nearly $3 billion. So, we’ve seen two multiunicorns set early pricing terms this week. That’s comfortably busy.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

As we did with Affirm, we’ll dig into Poshmark’s new pricing interval, calculate valuations for the company using both simple and fully diluted share counts, and figure out how they compare to its most-recent financial results and final private valuation. For the last bit, we’ll pull from PitchBook data and the S-1/A filing itself.

But for those of you in a hurry, the short gist is that for Mayfield, GGV, Menlo Ventures, Inventus Capital and Temasek, the company’s first pricing estimate looks like a win.

But for those of you in a hurry, the short gist is that for Mayfield, GGV, Menlo Ventures, Inventus Capital and Temasek, the company’s first pricing estimate looks like a win.

If you want to read our first dig into the company’s IPO filing that is more focused on performance than pricing, head here. Let’s go!

Poshmark’s $35 to $39 per-share IPO price interval could change, but even if it fails to rise, the company’s implied valuation is a dramatic step up from prior rounds.

For example, the company’s S-1 filings note that during its 2017 venture round — the last that it raised per the IPO filing and PitchBook data — Poshmark sold shares at $8.37 per share. That’s a fraction of the price that the company now expects public-market investors to pay.

As with Affirm, let’s calculate Poshmark’s valuation using both simple and fully diluted share counts. The latter takes into account shares that have been earned, but not yet exercised or converted.

Here’s the company’s valuation range using a simple share count, inclusive of its underwriters’ option to purchase 990,000 shares at its IPO price:

If we expand the company’s share count to include vested options and RSUs, the numbers go up. Again, the following math is inclusive of the underwriters’ option:1

So, are those good numbers? Yes.

Powered by WPeMatico

In April 2020, when the entire world was laser-focused on the coronavirus pandemic, we realized that startupland was in unprecedented territory. How should startups navigate fundraising, operations, and better understand the market?

In a matter of a couple weeks, we spun up a little series called Extra Crunch Live, giving Extra Crunch members the chance to hear from and connect with leaders across the industry. We brought on some of the biggest names in tech and VC, including the likes of Roelof Botha, Kirsten Green, Zach Perret, Charles Hudson, Aileen Lee, Mark Cuban, Howard Lerman, Niko Bonatsos and Alexa Von Tobel — and the list could go on and on and on.

Somehow, we did 44 episodes of the show in 2020, the year of our Lord.

By any measure, it’s been a huge success. But we’re not ones to rest on our laurels here at TechCrunch. Which is why I’m thrilled to announce Extra Crunch Live 2.0.

In 2021, we’ll be tweaking the format of ECL to provide even more interactivity between founders and audience members and the speakers we host on the show. You’re going to love it.

What’s New:

We’re super excited about our ECL plans for 2021 and we hope you are, too. More on upcoming speakers soon.

Remember, Extra Crunch Live events are for EC members only, so if you haven’t joined Extra Crunch, get over here!

Powered by WPeMatico