india

Auto Added by WPeMatico

Auto Added by WPeMatico

Indian fintech startup BharatPe has raised $370 million in a new round of financing as it looks to aggressively scale its business in the next two years. It’s the nineteenth Indian startup to become a unicorn this year (up from 11 last year) as several high-profile global investors double down in the South Asian market.

The new round — a Series E — was led by Tiger Global and valued the New Delhi-based startup at $2.85 billion (post-money), it said in a statement Tuesday evening. Dragoneer Investor Group and Steadfast Capital also participated in the new round, which brings the startup’s to-date raise to over $580 million against equity.

Tuesday’s news confirms a TechCrunch scoop from June in which we reported that the four-year-old startup was looking to raise about $250 million at a pre-money valuation of $2.5 billion. BharatPe was valued at about $900 million in its Series D round in February this year, and $425 million last year.

BharatPe co-founder Ashneer Grover confirmed that the startup was indeed looking to raise $250 million until inbound requests from investors prompted an oversubscription. The new investment also includes some secondary transactions.

BharatPe, which counts Coatue, Ribbit Capital and Sequoia Capital India among its existing investors, operates an eponymous service to help offline merchants accept digital payments and secure working capital.

Even as India has already emerged as the second-largest internet market, with more than 650 million users, much of the country remains offline.

Among those outside of the reach of the internet are merchants running small businesses, such as roadside tea stalls and neighborhood stores. To make these merchants comfortable with accepting digital payments, BharatPe relies on QR codes and point of sale machines that support government-backed UPI payments infrastructure.

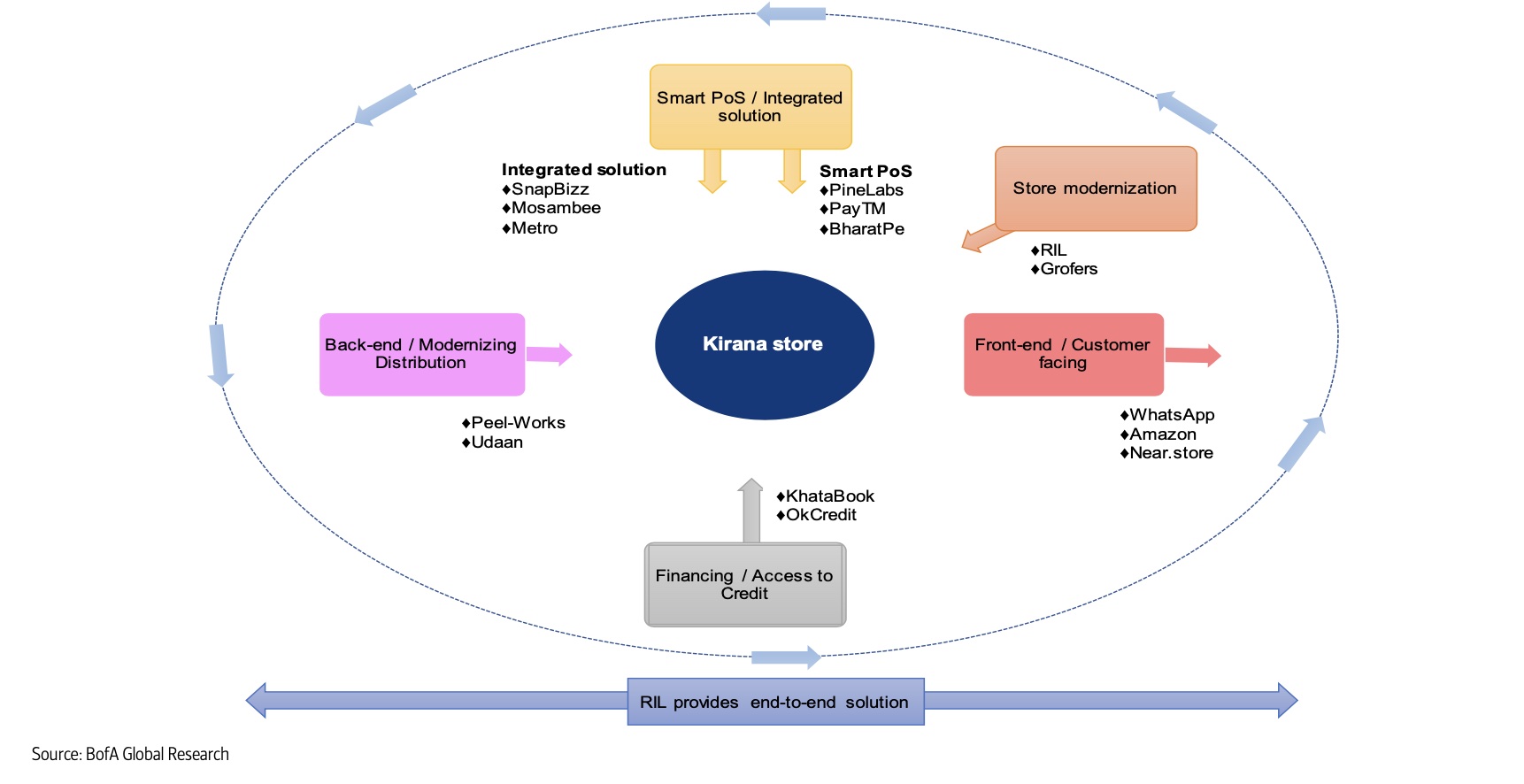

Scores of giants and startups are attempting to serve neighborhood stores in India. Image Credits: Bank of America Research

The startup, which serves more than 7 million merchants in over 130 Indian cities, said it has disbursed close to $300 million to merchant partners. It does not charge merchants for universal QR code access, but is looking to make money by lending.

The startup plans to expand its product offerings as well as work with Centrum Financial Services, with which it was recently granted the license by India’s central bank (Reserve Bank of India) to set up a small finance bank. (Centrum Financial Services has collaborated with BharatPe for the license, and the Indian startup says the two are “equal” partners.)

Tuesday’s development further illustrates the growing interest of Tiger Global in India. The New York-headquartered firm has backed dozens of Indian startups, including social commerce startup DealShare, edtech Classplus, Apna (an app that helps blue-collar workers connect with recruiters) and home services platform Urban Company in recent months.

On Tuesday, Infra.Market, an Indian startup that helps construction and real estate companies procure materials and handle logistics for their projects, said it had raised $125 million in a round led also by Tiger Global.

Powered by WPeMatico

Gupshup, a business messaging platform that began its journey in India 15 years ago, surprised many when it raised $100 million in April this year, roughly 10 years after its last financing round, and attained the coveted unicorn status. Now just three months later, the San Francisco-headquartered startup has secured even more capital from high-profile investors.

On Wednesday, Gupshup said it had raised an additional $240 million as part of the same Series F financing round. The new investment was led by Fidelity Management, Tiger Global, Think Investments, Malabar Investments, Harbor Spring Capital, certain accounts managed by Neuberger Berman Investment Advisers and White Oak.

Neeraj Arora, formerly a high-profile executive at WhatsApp who played an instrumental role in helping the messaging platform sell to Facebook, also wrote a significant check to Gupshup in the new tranche of investment, which continues to value the startup at $1.4 billion as in April.

In an interview with TechCrunch earlier this week, Beerud Sheth, co-founder and chief executive of Gupshup, said he extended the financing round after receiving too many inbound requests from investors. The new investors will provide the startup with crucial insight and expertise, he said. The round is now closed, he continued.

The startup, which operates a conversational messaging platform that is used by over 100,000 businesses and developers today to build their own messaging and conversational experiences to serve their users and customers, is beginning to consider exploring the public markets by next year, said Sheth, though he cautioned a final decision is yet to be made.

“Conversation is becoming a bigger part of doing business and it has partly been driven by the pandemic,” he said over a phone call. “Second, we have always been the leader in this space, but the product innovation we have focused on in the last two to three years has worked in our favor.”

The new investment, which includes some secondary buyback (some early investors and employees are selling their stakes), will be deployed into broadening the product offerings of Gupshup, he said. The startup is also eyeing some M&A opportunities and may close some deals this year, he added.

Some of the notable customers of Gupshup, which leads the business messaging market. Image Credits: Gupshup

Before Gupshup became so popular with businesses, it existed in a different avatar. For the first six years of its existence, Gupshup was best known for enabling users in India to send group messages to friends. (These cheap texts and other clever techniques enabled tens of millions of Indians to stay in touch with one another on phones a decade ago.)

That model eventually became unfeasible to continue, Sheth told TechCrunch in an earlier interview.

“For that service to work, Gupshup was subsidizing the messages. We were paying the cost to the mobile operators. The idea was that once we scale up, we will put advertisements in those messages. Long story short, we thought as the volume of messages increases, operators will lower their prices, but they didn’t. And also the regulator said we can’t put ads in the messages,” he said earlier this year.

That’s when Gupshup decided to pivot. “We were neither able to subsidize the messages, nor monetize our user base. But we had all of this advanced technology for high-performance messaging. So we switched from a consumer model to an enterprise model. So we started to serve banks, e-commerce firms and airlines that need to send high-level messages and can afford to pay for it,” said Sheth, who also co-founded freelance workplace Elance in 1998.

Over the years, Gupshup has expanded to newer messaging channels, including conversational bots and it also helps businesses set up and run their WhatsApp channels to engage with customers.

Sheth said scores of major firms worldwide in banking, e-commerce, travel and hospitality and other sectors are among the clients of Gupshup. These firms are using Gupshup to send their customers transaction information and authentication codes, among other use cases. “These are not advertising or promotional messages. These are core service information,” he said.

“We have followed Gupshup’s progress for a long while and believe that they are the most evolved customer communications platform In India and increasingly in other emerging markets, with a leadership position in the most attractive and fastest growing subsegments of the market,” said Sumeet Nagar, managing director of Malabar Investments, in a statement.

“We believe that Beerud and team have the unique opportunity to expand the addressable market on the back of new offerings and scale the business up significantly, which is a perfect recipe for massive value creation. I have known Beerud for over three decades, and all of us at Malabar are delighted to partner with Gupshup in the next stage of their journey.”

Powered by WPeMatico

The global pandemic highlighted inefficiencies and inconsistencies in healthcare systems around the world. Even co-founders Mayank Banerjee, Matilde Giglio and Alessandro Ialongo say nowhere is this more evident than in India, especially after the COVID death toll reached 4 million this week.

The Bangalore-based company received a fresh cash infusion of $5 million in seed funding in a round led by Khosla Ventures, with participation from Founders Fund, Lachy Groom and a group of individuals including Palo Alto Networks CEO Nikesh Arora, CRED CEO Kunal Shah, Zerodha founder Nithin Kamath and DST Global partner Tom Stafford.

Even, a healthcare membership company, aims to cover what most insurance companies in the country don’t, including making going to a primary care doctor as easy and accessible as it is in other countries.

Banerjee grew up in India and said the country is similar to the United States in that it has government-run and private hospitals. Where the two differ is that private health insurance is a relatively new concept for India, he told TechCrunch. He estimates that less than 5% of people have it, and even though people are paying for the insurance, it mainly covers accidents and emergencies.

This means that routine primary care consultations, testings and scans outside of that are not covered. And, the policies are so confusing that many people don’t realize they are not covered until it is too late. That has led to people asking doctors to admit them into the hospital so their bills will be covered, Ialongo added.

Banerjee and Giglio were running another startup together when they began to see how complicated health insurance policies were. About 50 million Indians fall below the poverty line each year, and many become unable to pay their healthcare bills, Banerjee said.

They began researching the insurance industry and talking with hospital executives about claims. They found that one of the biggest issues was incentive misalignment — hospitals overcharged and overtreated patients. Instead, Even is taking a similar approach to Kaiser Permanente in that the company will act as a service provider, and therefore, can drive down the cost of care.

Even became operational in February and launched in June. It is gearing up to launch in the fourth quarter of this year with more than 5,000 people on the waitlist so far. Its health membership product will cost around $200 per year for a person aged 18 to 35 and covers everything: unlimited consultations with primary care doctors, diagnostics and scans. The membership will also follow as the person ages, Ialongo said.

The founders intend to use the new funding to build out their operational team, product and integration with hospitals. They are already working with 100 hospitals and secured a partnership with Narayana Hospital to deliver more than 2,000 COVID vaccinations so far, and more in a second round.

“It is going to take a while to scale,” Banerjee said. “For us, in theory, as we get better pricing, we will end up being cheaper than others. We have goals to cover the people the government cannot and find ways to reduce the statistics.”

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture-capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday Tuesday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here.

What a busy weekend we missed while mostly hearing distant explosions and hugging our dogs close. Here’s a sampling of what we tried to recap on the show:

It’s going to be a busy week! Chat tomorrow.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Shares of Chinese ride-hailing provider Didi are sharply lower this morning after news broke that its domestic regulators are investigating the newly public company. A loose translation of the probe’s official notice indicates that the cybersecurity review is “in order to prevent national data security risks, maintain national security and protect the public interest.”

Yesterday, regulators ordered Didi to stop registering new users during the investigation.

The move comes amid a larger reset of relations between China’s burgeoning technology sector and its autocratic government. Other fallouts from the campaign included the effective silencing of Jack Ma, the embarrassing cancellation of the Ant IPO and a crackdown on data collection from technology companies more broadly.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

China is not the only nation grappling with its technology sector; India has made consistent noise in recent months regarding tech firms inside its borders, for example. And there is effort inside the U.S. Congress to put some cap on Big Tech’s scale and power, though of the trio, the United States appears the least likely to take a real swipe at technology companies’ market influence.

That Didi has run afoul of China’s regulatory bodies is not a surprise; it’s a well-known tech company in the country with lots of consumer data. Similar data-rich tech shops in the country have come under increased scrutiny as well.

But to see Didi get taken to task mere days after its U.S. debut puts a bad taste in our mouths.

The way that this saga reads from the cynical perspective is that the Chinese Communist Party was willing to let the company go public in the United States, allowing it to raise billions of dollars from foreign sources. And that the ruling party was then content to leave them holding a midsized bag by announcing its cybersecurity probe.

Hanlon’s Razor is at play in this situation, naturally.

Didi has not published a new SEC filing since June 30, and, as of the time of writing, its investor relations page is devoid of any information regarding today’s news.

While going public, it’s worth noting that Didi did warn investors that it faces a host of risks relating to its status as a Chinese company, namely its government, and as a Chinese company going public in the United States. Observe the following risk factors that it shared while going public (emphasis added) that dealt with the company’s business operations:

- Our business is subject to numerous legal and regulatory risks that could have an adverse impact on our business and future prospects.

- Our business is subject to a variety of laws, regulations, rules, policies and other obligations regarding privacy, data protection and information security. Any losses, unauthorized access or releases of confidential information or personal data could subject us to significant reputational, financial, legal and operational consequences.

Powered by WPeMatico

For most people in India, having to engage with banks doesn’t instill a sense of joy. Banks in the South Asian market are notorious for making unannounced spam calls to upsell customers loans and credit cards, even when they have been explicitly asked not to do so.

Moreover, when a customer does reach out to a bank with a query, it can take forever to get the job done. Take ICICI Bank, India’s third largest bank and until recently my only banking partner for over six years, for an example.

It is now in its third month in figuring out who exactly in its relationship with Amazon is supposed to re-issue me a credit card. I have moved on with my life, and it looks like they did, too, likely before they even looked at my query.

Small and medium-sized businesses aren’t a big fan of banks, either. If you operate an early-stage startup, it’s anyone’s guess if you will ever be able to convince a bank to issue you a corporate account. So of course, startups — Razorpay and Open — took it upon themselves to fix this experience.

For consumers, too, in recent years, scores of startups have arrived on the scene to improve this banking experience. Whether you are a teenager, or just out of college, or a working professional, or don’t have a credit score, there are firms that can get you a credit card and loan.

But even these services have a ceiling limit of some sort. And customers aren’t loyal to any startup.

“A customer’s relationship is always with the entity where they park their savings deposit,” said Jitendra Gupta, a high-profile entrepreneur who has spent a decade in the fintech world. Since these customers are not parking their money with fintech, “the startups have been unable to disrupt the bank. That’s the hard reality.”

So what’s the alternative? Gupta, who co-founded CitrusPay (sold to Naspers’ PayU) and served as managing director of PayU, has been thinking about these challenges for more than two years.

“If you really want to change the banking industry, you cannot operate from the side. You have to fight from the centre, where they deposit their money. It’s a very time-consuming process and requires a lot of initial capital and experience with banks,” he told TechCrunch in an interview.

After more than a year and a half of raising about $24 million — from Sequoia Capital India, 3one4 Capital, Amrish Rau, Kunal Shah, Kunal Bahl, Tanglin Venture Partners, Rainmatter and others — Gupta is ready to launch what he believes will address a lot of the issues individuals face with their banks.

His new startup, called Jupiter, wants to bring “delight” to the banking experience, and it will launch in India on Thursday.

“We believe that a bank account should be a smart account, where it gives you insight, shares personalized tips and guides you through attaining some financial discipline,” he said.

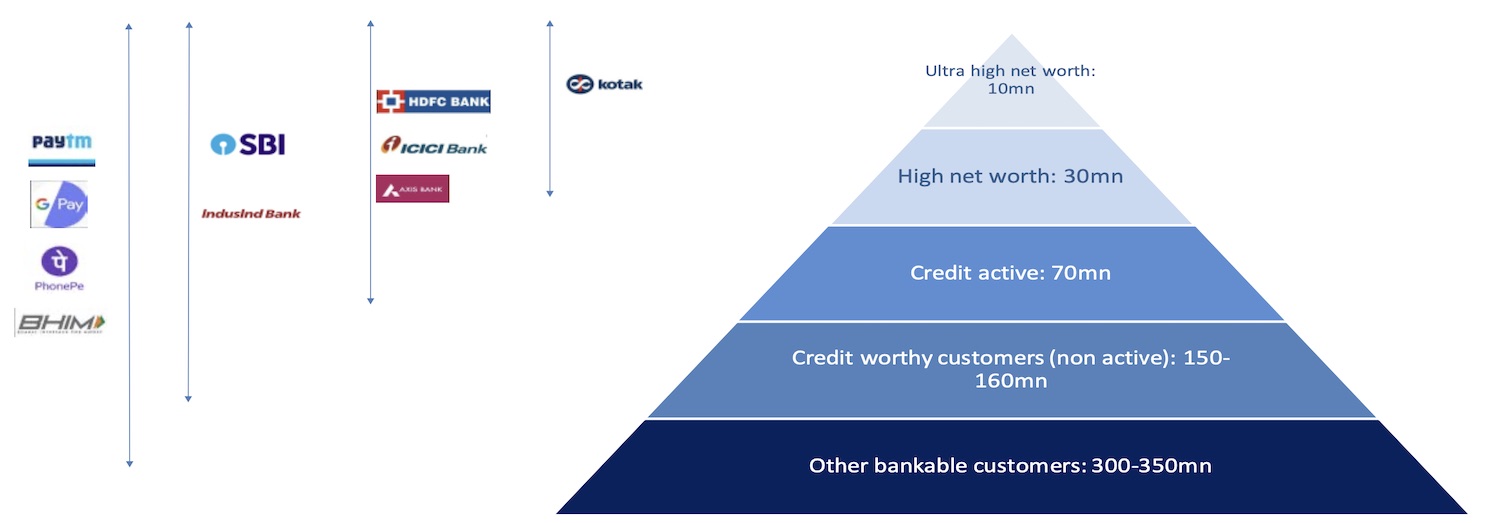

A snapshot of the reach of banks and fintech startups in India. Data: CIBIL, Statista, BofA Global Research. Image: BofA

To be sure, Jupiter, too, will offer loans and other financial services to customers. But instead of making irrelevant calls to customers, it will assess which of its customers are running short on money and give the option to take a credit line from its app itself, he said. “The upsell doesn’t need to happen by way of spam. It needs to happen by way of contextualization and personalization.”

“Jupiter has been built in a deep integration with the underlying bank, allowing the consumer to have a frictionless experience for all their banking needs,” said Amrish Rau, chief executive of Pine Labs, co-founder of CitrusPay and longtime friend of Gupta.

The startup, which employs 115 people, has developed a number of products for customers joining on day one. The products include the ability to buy now and pay later on UPI, a feature first offered in the market by Jupiter, and a mutual fund portfolio analyzer. A debit card, in-app chat with a customer service agent, expense categorisation, finding the right card, determining the existing health insurance coverage, and more are ready to ship, the startup said.

Jupiter is currently working on providing zero mark-up on forex transactions, and frictionless two-factor authentication. The startup has published a public Trello page where it has outlined the features it is working on and when it expects to ship them, as well as features suggested by its beta-testing customers. “I want to establish full transparency in what we are working on to build trust with customers,” said Gupta.

Jupiter will have its own customer relationship team that will engage with the startup’s users. The startup, which last month opened a waiting list for customers to sign up, had amassed more than 25,000 applications as of two weeks ago.

Even Jupiter, which one day wishes to disrupt the banking sector, currently has to partner with banks. Its partners are Federal Bank and Axis Bank.

I asked Gupta about the excitement his investors see in Jupiter. “Everyone believes, as you see with fintech giants such as Nubank globally, that we will become a full bank,” he said.

But for the time being, Gupta said he is not looking to partner with more banks. “I don’t want Jupiter to attract customers because they want to bank with Federal or Axis. I want them to come to Jupiter because they want to bank with Jupiter,” he said.

In the next 12 months, the startup hopes to serve more than 1 million customers.

Powered by WPeMatico

Krafton, which filed for an IPO earlier this week, has built a gigantic gaming empire. If the firm is able to raise the target $5 billion from the IPO it will be the largest public offering in its home country, South Korea. The firm has something to celebrate elsewhere in the world, too.

On Thursday, it pulled off another feat that no other firm has been able to achieve: Its sleeper hit title, PUBG Mobile, has made a return to India, which banned the title more than nine months ago.

The world’s second-largest internet market banned over 200 apps last year citing national security concerns. All the apps New Delhi blocked in the nation had links to China. The move was seen by many as retaliation as tension between the two nuclear-armed neighboring nations escalated last year.

Every other app that has been banned by India — and pulled by Google and Apple from their respective app stores in the country in compliance with local government orders — remains in that state. ByteDance, whose TikTok app identified India as its largest market, has significantly downsized its team in the country. (ByteDance runs several businesses in India and many remain operational. Employees have been instructed to stay off the radar.)

Which is what makes PUBG Mobile’s return to India all the more interesting. The game, which has been rebranded to Battlegrounds Mobile India in the South Asia market, is available to download from the Play Store for any user in the country — provided they sign up for an early access before the imminent launch.

Even as PUBG Mobile is now using a different moniker, the game follows the same plot, and the identical home screen greets users with the familiar ecstatic background score.

Moreover, users are offered a quick and straightforward option to migrate their PUBG Mobile accounts to the new app.

Rishi Alwani, the quintessential gaming reporter in India who edits IGN India, told TechCrunch that the new game is “essentially PUBG Mobile with data compliance, green blood, and a constant reminder that you’re in a ‘virtual world’ with such messaging present as you start a game and when you’re in menus.”

The changes are likely Krafton’s attempt to assuage previous concerns from the local authorities, some of whom had expressed concerns about the game’s affect on youngsters.

Image Credits: TechCrunch / screen capture

But these on-the-surface changes raise a set of bigger questions that have been a topic of discussion among several startup founders and policy executives in India in recent months:

Neither the Indian government nor Krafton have publicly said anything on this subject. Krafton, on its part, has taken steps to assuage India’s concerns. For instance, last year the South Korean firm cut ties with its publishing partner Tencent, the only visible Chinese affiliation — if the Indian government was indeed banning just Chinese apps. Krafton also publicly announced that it will be investing $100 million in India’s gaming ecosystem.

The Indian government’s order and the communication and compliance mechanism for concerned entities have been so opaque on this subject that it is unclear on what grounds Krafton has been able to bring the game back.

One explanation — albeit admittedly full of speculation — is that it’s a new app in the sense that it has a new app ID. In this instance, it happens to have a new developer account, too. Remember, India banned apps, and not the firms themselves. Several Tencent and Alibaba apps, for instance, remain available in India.

This would also explain how BIGO has been able to launch a new app — Tiki Video — under a new developer account and plenty of effort to conceal its connection. That app, which was launched in late February, has amassed over 16 million monthly active users, according to mobile insight firm App Annie. The app’s existence and affiliation with BIGO have not been previously reported.

But the question remains, are these simple workarounds enough to escape the ban? To be sure, some apps, including Battlegrounds Mobile India, are also hosting their data in the country now, and have agreed for periodic audits. So is that enough? And if it is, why aren’t most — if not all — apps making a return to India?

Regardless, the return of PUBG Mobile India is a welcome move for tens of millions of users in the country, many of whom — about 38 million last month, according to App Annie — were using workarounds themselves to continue to play the game.

Powered by WPeMatico

Indian cities are home to hundreds of millions of low-skilled workers who hail from villages in search of work. Many of them have lost their jobs amid the coronavirus pandemic that has slowed several economic activities in the world’s second-largest internet market.

Apna, a startup by an Apple alum, is helping millions of such blue and gray-collar workers upskill themselves, find communities and land jobs. On Wednesday it announced its acceptance by the market has helped it raise $70 million in a new financing round as the startup prepares to scale the 16-month-old app across India.

Insight Partners and Tiger Global co-led Apna’s $70 million Series B round, which valued the startup at $570 million. Existing investors Lightspeed India, Sequoia Capital India, Greenoaks Capital and Rocketship VC also participated in the round, which brings Apna’s to-date raise to over $90 million.

The startup, whose name is inspired from a 2019 Bollywood song, at its core is solving the network gap issue for workers. “Someone born in a privileged family goes to the best school, best college and makes acquaintance with influential people. Many born just a few kilometres away are dealt with a whole different kind of life and never see such opportunities,” said Nirmit Parikh, founder and chief executive of Apna, in an interview with TechCrunch.

Apna is building a scalable networking infrastructure, something that doesn’t currently exist in the market, so that these workers can connect to the right employers and secure jobs. “Apna’s focus on digitizing the process of job discovery, application and employer candidate interaction has the potential to revolutionize the hiring process,” said Griffin Schroeder, a partner at Tiger Global, in a statement.

The workers in India “already have a champion in them, we are just helping them find opportunities,” said Nirmit Parikh, founder and chief executive of Apna. (Apna)

The startup’s eponymous Android app, available in multiple languages, features more than 70 communities today for skilled professionals such as carpenters, painters, field sales agents and many others.

On the app, users connect to each other and help with leads and share tips to improve at their jobs. The app also offers people the opportunity to upskill themselves, practice with their interview performance, and become eligible for even more jobs. The startup said it’s building Masterclass-like skilling modules, outcome or job based skilling, and also enabling peer-to-peer learning via its vertical communities. It plans to launch career counselling and resume building feature.

And that bet is working. The startup has amassed over 10 million users and just last month it facilitated more than 15 million job interviews, said Parikh. All jobs listed on the Apna platform are verified by the startup and free of cost for the candidates.

Apna has partnered with some of India’s leading public and private organizations and is providing support to the Ministry of Minority Affairs of India, National Skill Development Corporation and UNICEF YuWaah to provide better skilling and job opportunities to candidates.

Apna app (Apna)

More than 100,000 recruiters — including Byju’s, Unacademy, Flipkart, Zomato, Licious, Burger King, Dunzo, Bharti-AXA, Delhivery, Teamlease, G4S Global and Shadowfax — in the country today use Apna’s platform, where they have to spend less than five minutes to post job posts and are connect to hyperlocal candidates with relevant skills in within two days.

Apna has built the “market leading platform for India’s workforce to establish digital professional identity, network, access skills training, and find high quality jobs,” said Nikhil Sachdev, managing director, Insight Partners, in a statement.

“Employers are engaging with Apna at a rapid pace to help find high quality talent with low friction which is leading to best in class customer satisfaction scores. We believe that our investment will enable Apna to continue their steep growth trajectory, scale up their operations, and improve access to opportunities for India’s workforce.”

The startup plans to deploy the fresh capital to scale across India and eventually take the app to international markets, said Parikh. Apna, which has recently seen high-profile individuals from firms such as Uber, BCG and Swiggy join the firm, is also actively hiring for several tech roles in the South Asian market.

Apna has built the infrastructure and brand awareness in the market that it can launch in a new city within two days and drive over 10,000 interviews there in less than two days, it said.

“Our first goal is to restart India’s economy in the next couple of months and do whatever we can to help,” said Parikh, who was part of the iPhone product-operations team at Apple.

Powered by WPeMatico

Tiger Global is in talks to lead a $30 million round in Indian edtech startup Classplus, according to sources familiar with the matter.

The new round, which includes both primary investment and secondary transactions, values the five-year-old Indian startup at over $250 million, two sources told TechCrunch.

The new round follows another ~$30 million investment that was led by GSV recently, one of the sources said. The new round hasn’t closed, so terms may change.

Classplus — which has built a Shopify-like platform for coaching centers to accept fees digitally from students and deliver classes and study material online — also raised $10.3 million in September last year from Falcon Edge’s AWI, cricketer Sourav Ganguly and existing investors RTP Global and Blume Ventures. That round had valued Classplus at about $73 million, according to research firm Tracxn.

Classplus didn’t respond to a request for comment. Sources requested anonymity, as the matter is private.

As tens of millions of students — and their parents — embrace digital learning apps, Classplus is betting that hundreds of thousands of teachers and coaching centers that have gained reputation in their neighborhoods are here to stay.

The startup is serving these hyperlocal tutoring centers that are present in nearly every nook and cranny in India. “Anyone who was born in a middle-class family here has likely attended these tuition classes,” Mukul Rustagi, co-founder and chief executive of Classplus, told TechCrunch last year.

“These are typically small and medium setups that are run by teachers themselves. These teachers and coaching centers are very popular in their locality. They rarely do any marketing and students learn about them through word-of-mouth buzz,” he said then.

Rustagi had described Classplus as “Shopify for coaching centers.” Like Shopify, Classplus does not serve as a marketplace that offers discoverability to these teachers or coaching centers and instead it offers a way for these teachers to leverage its tech platform to engage with customers.

This year, Tiger Global has backed — or in talks to back — about two dozen startups in India.

Powered by WPeMatico