india

Auto Added by WPeMatico

Auto Added by WPeMatico

A 22-month-old startup that is helping millions of blue- and gray-collar workers in India learn new skills and find jobs has become the youngest firm to join the coveted unicorn status in the world’s second-largest internet market.

Apna announced on Thursday that it has raised $100 million in a round led by Tiger Global. The new round — a Series C — valued Apna at $1.1 billion. TechCrunch reported last month that Tiger Global, an existing investor in Apna, was in talks to lead a $100 million financing round in the startup at the unicorn valuation.

Owl Ventures, Insight Partners, Sequoia Capital India, Maverick Ventures and GSV Ventures also participated in the new round, which is the third investment secured by Apna this year. Apna was valued at $570 million in its Series B round in June this year.

The investors’ excitement comes as Apna has demonstrated an impressive growth in recent months. The startup has amassed over 16 million users on its 15-month-old eponymous Android app, up from 10 million in June this year.

Indian cities are home to hundreds of millions of low-skilled workers who hail from villages in search of work. Many of them have lost their jobs amid the coronavirus pandemic that has slowed several economic activities in the South Asian market.

Apna has built a platform that provides a community to these workers. In the community, they engage with each other, exchange notes to perform better at interviews and share tips to negotiate better compensation.

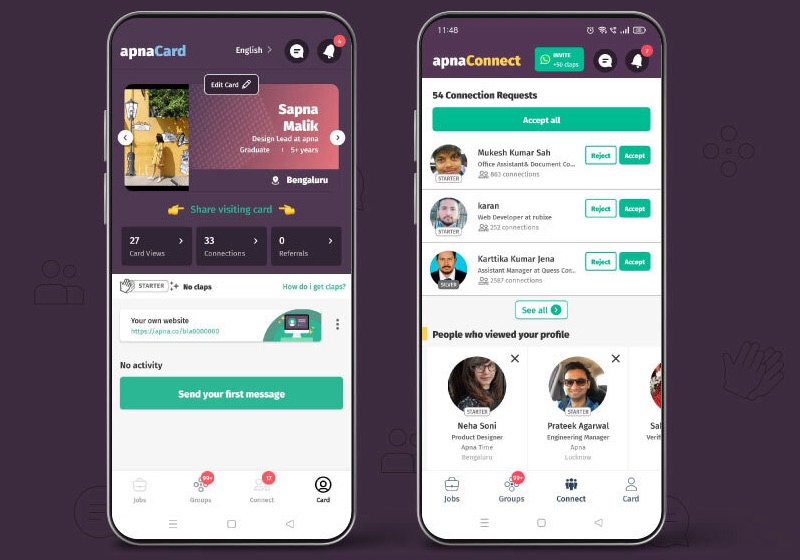

Image Credits: Apna

On top of this, Apna connects these workers to potential employers. In an interview with TechCrunch, Apna founder and chief executive Nirmit Parikh said more than 150,000 employers — including Zomato, Bharti AXA, Urban Company, BYJU’S, PhonePe, Burger King, Delhivery, Teamlease and G4S Global — are on the platform, and over 5 million jobs are active.

The startup, whose name is inspired from a cheerful 2019 Bollywood song, has facilitated over 18 million job interviews in the past 30 days, he said. Apna is currently operational in 28 Indian cities.

The idea for Apna came, Parikh has said, after he was puzzled to find that even as there are hundreds of millions of blue- and gray-collar workers in India, locating them when you need assistance with a task often proves very difficult.

Prior to starting Apna, Parikh, who previously worked at Apple, met these workers and went undercover as an electrician and floor manager to understand the problems they were facing. The problem, he found, was the disconnect. Workers had no means to find who needed them for jobs, and they were also not connected with one another. The community aspect of Apna, which now has over 70 such groups, is aimed at addressing this challenge.

The Apna app allows these workers to learn new skills to become eligible for more work opportunities. Apna has emerged as one of the fastest growing upskilling platforms — and that would explain why GSV Ventures and Owl Ventures, two high-profile firms known to back edtech startups, are investing in the Bangalore-based firm.

“Apna’s viral adoption is driven by a novel social and interactive approach to connecting employers with job seekers. We expect job seekers in search of meaningful connections and vetted opportunities to drive Apna’s continued explosive growth across India — and the world,” said Griffin Schroeder, partner at Tiger Global, in a statement.

Now the startup, which has started to monetize the platform, is ready to aggressively expand. Parikh said Apna will continue to expand to more cities in India and by early next year, Apna will begin its global expansion. Parikh said the startup is eyeing expansion in the USA, South East Asia and Middle East and Africa.

“We have already created a dent. Now we want to impact the lives of 2.3 billion,” he said. “We will require crazy amounts of resources and a world-class team to deliver. It’s a herculean task, and is going to take a village. But somebody has to solve it.”

Powered by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

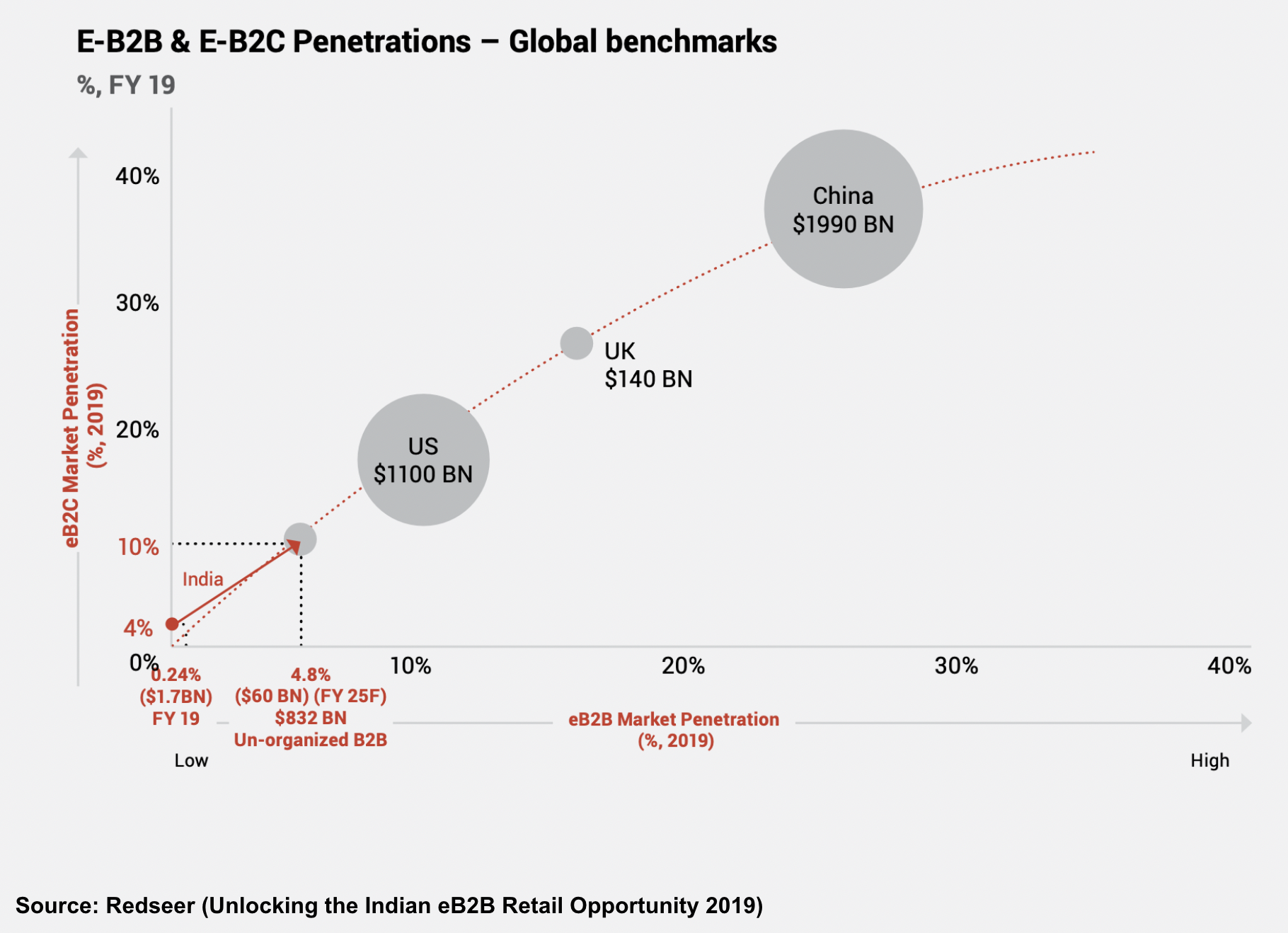

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

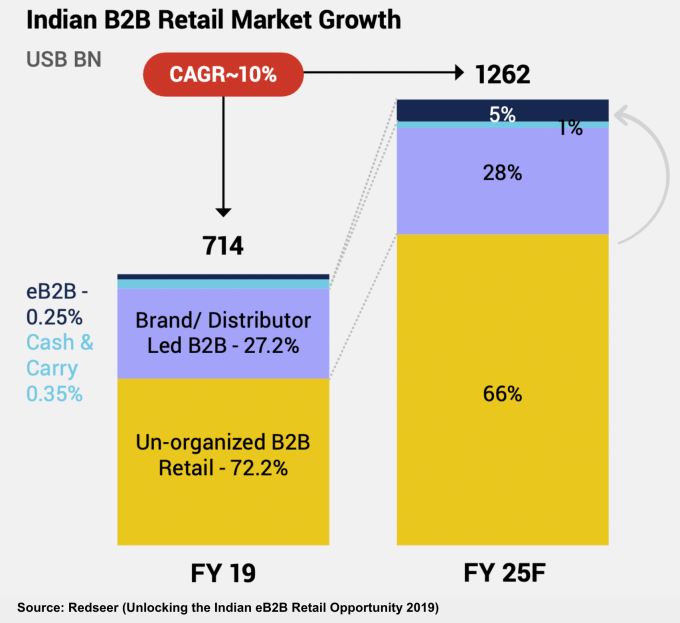

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

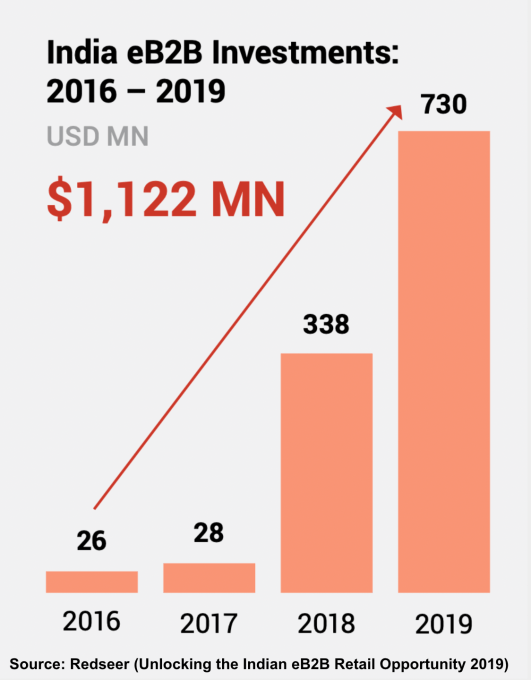

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

Media technology company Amagi announced Friday $100 million to further develop its cloud-based SaaS technology for broadcast and connected televisions.

Accel, Avataar Ventures and Norwest Venture Partners joined existing investor Premji Invest in the funding round, which included buying out stakes held by Emerald Media and Mayfield Fund. Nadathur Holdings continues as an existing investor. The latest round gives Amagi total funding raised to date of $150 million, Baskar Subramanian, co-founder and CEO of Amagi, told TechCrunch.

Bangalore-based Amagi provides cloud broadcast and targeted advertising software so that customers can create content that can be created and monetized to be distributed via broadcast TV and streaming TV platforms like The Roku Channel, Samsung TV Plus and Pluto TV. The company already supports more than 2,000 channels on its platform across over 40 countries.

“Video is a complex technology to manage — there are large files and a lot of computing,” Subramanian said. “What Amagi does is enable a content owner with zero technology knowledge to simplify that complex workflow and scalable infrastructure. We want to make it easy to plug in and start targeting and monetizing advertising.”

As a result, Amagi customers see operational cost savings on average of up to 40% compared to traditional delivery models and their ad impressions grow between five and 10 times.

The new funding comes at a time when the company is experiencing rapid growth. For example, Amagi grew 30 times in the United States alone over the past few years, Subramanian said. Amagi commands an audience of over 2 billion people, and the U.S. is its largest market. The company also sees growth potential in both Latin America and Europe.

In addition, in the last year, revenue grew 136%, while new customer year over year growth was 44%, including NBCUniversal — Subramanian said the Tokyo Olympics were run on Amagi’s platform for NBC, USA Today and ABS-CBN.

As more of a shift happens with video content being developed for connected television experiences, which he said is a $50 billion market, the company plans to use the new funding for sales expansion, R&D to invest in the company’s product pipeline and potential M&A opportunities. The company has not made any acquisitions yet, Subramanian added.

In addition to the broadcast operations in New Delhi, Amagi also has an innovation center in Bangalore and offices in New York, Los Angeles and London.

“Consumer behavior and infrastructure needs have reached a critical mass and new companies are bringing in the next generation of media, and we are a large part of that growth,” Subramanian said. “Sports will come on quicker, while live news and events are going to be one of the biggest growth areas.”

Shekhar Kirani, partner at Accel, said Amagi is taking a unique approach to enterprise SaaS due to that $50 billion industry shift happening in video content, where he sees half of the spend moving to connected television platforms quickly.

Some of the legacy players like Viacom and NBCUniversal created their own streaming platforms, where Netflix and Amazon have also been leading, but not many SaaS companies are enabling the transition, he said.

When Kirani met Subramanian five years ago, Amagi was already well funded, but Kirani was excited about the platform and wanted to help the company scale. He believes the company has a long tailwind because it is saving people time and enabling new content providers to move faster to get their content distributed.

“Amagi is creating a new category and will grow fast,” Kirani added. “They are already growing and doubling each year with phenomenal SaaS metrics because they are helping content providers to connect to any audience.

Powered by WPeMatico

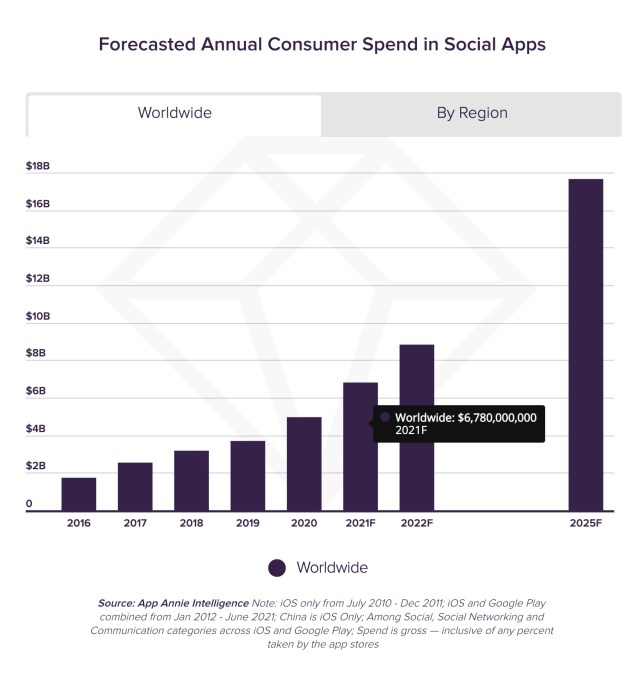

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

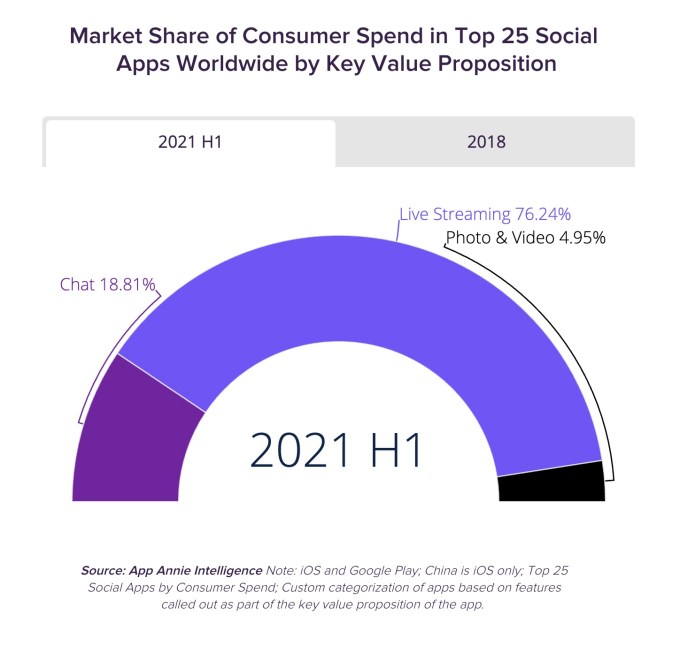

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

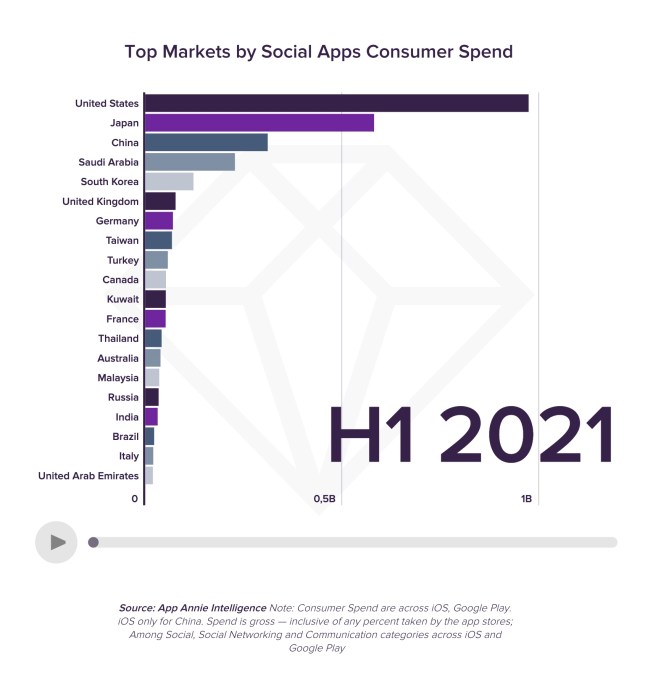

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

One top app that’s significantly gaining here is TikTok.

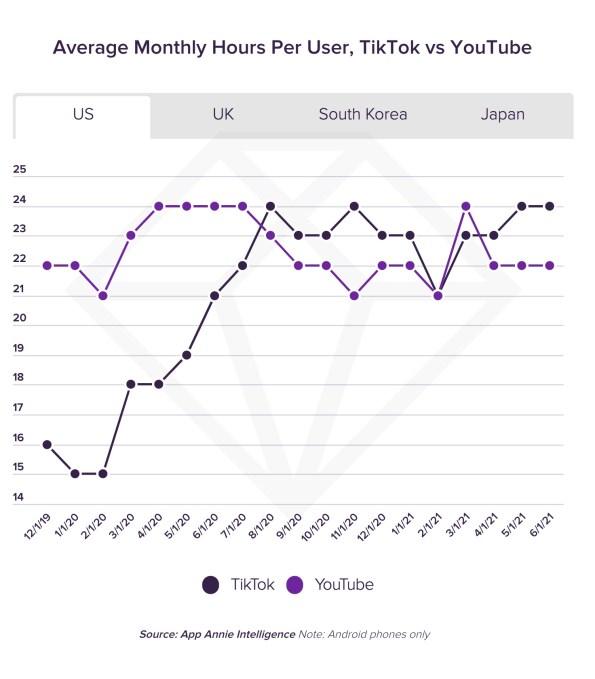

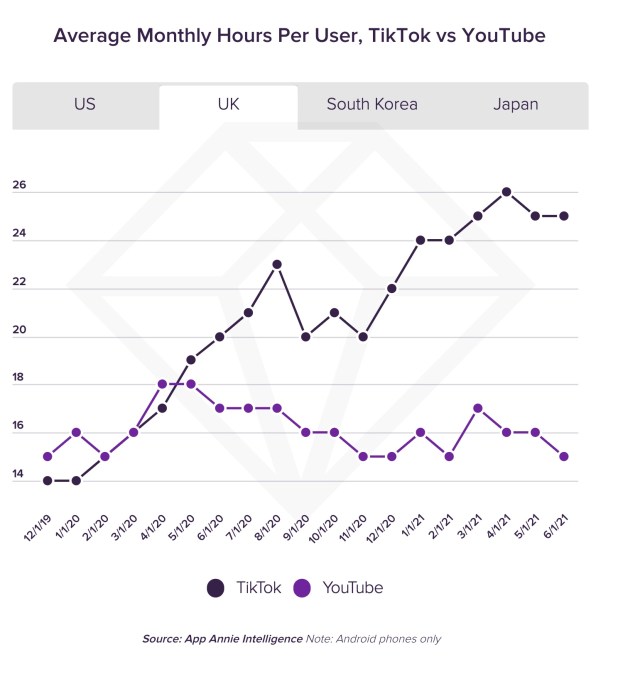

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

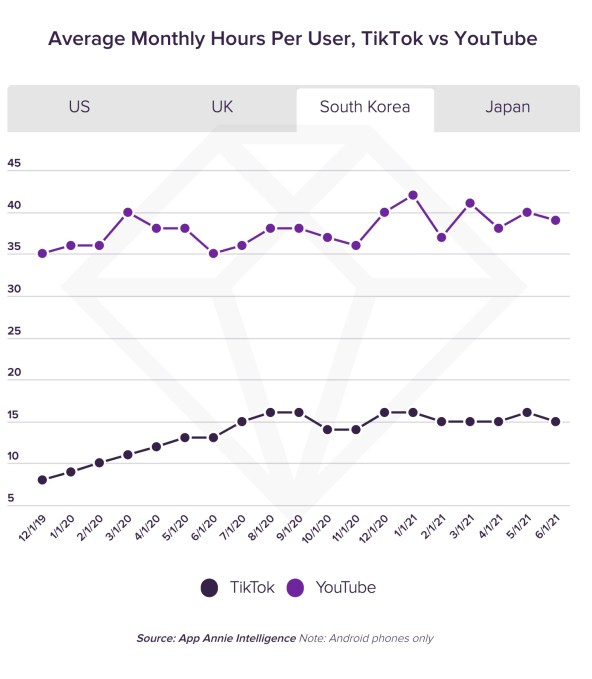

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

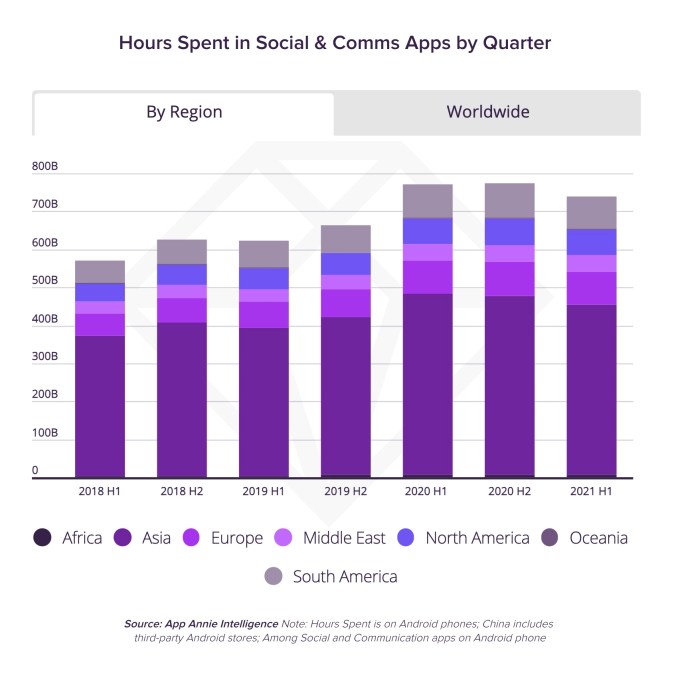

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

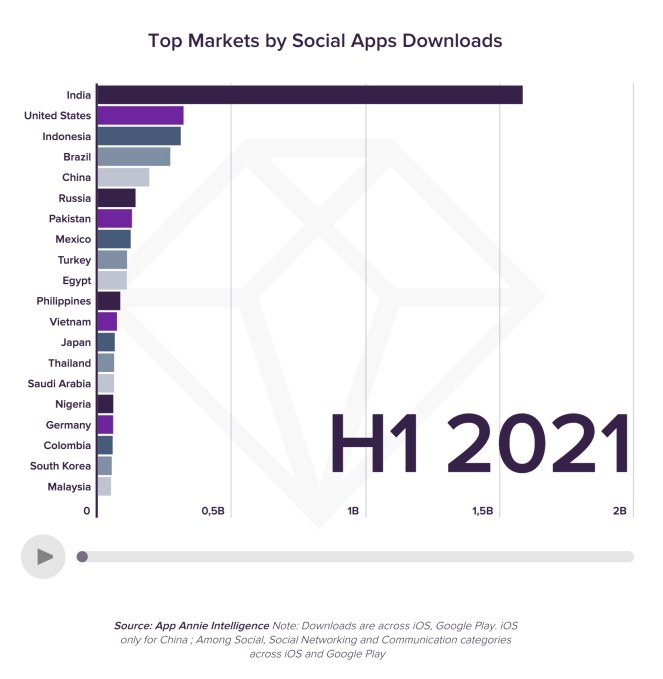

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

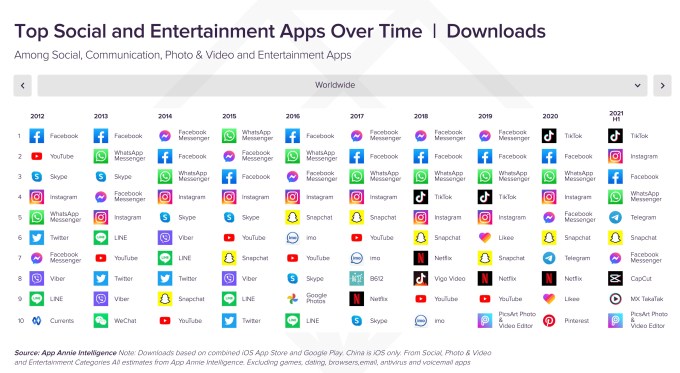

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

Summer is still technically in session, but a snowball is slowly developing in the world of apps, and specifically the world of in-app payments. A report in Reuters today says that the Competition Commission of India, the country’s monopoly regulator, will soon be looking at an antitrust suit filed against Apple over how it mandates that app developers use Apple’s own in-app payment system — thereby giving Apple a cut of those payments — when publishers charge users for subscriptions and other items in their apps.

The suit, filed by an Indian nonprofit called “Together We Fight Society”, said in a statement to Reuters that it was representing consumer and startup interests in its complaint.

The move would be the latest in what has become a string of challenges from national regulators against app store operators — specifically Apple but also others like Google and WeChat — over how they wield their positions to enforce market practices that critics have argued are anti-competitive. Other countries that have in recent weeks reached settlements, passed laws or are about to introduce laws include Japan, South Korea, Australia, the U.S. and the European Union.

And in India specifically, the regulator is currently working through a similar investigation as it relates to in-app payments in Android apps, which Google mandates use its proprietary payment system. Google and Android dominate the Indian smartphone market, with the operating system active on 98% of the 520 million devices in use in the country as of the end of 2020.

It will be interesting to watch whether more countries wade in as a result of these developments. Ultimately, it could force app store operators, to avoid further and deeper regulatory scrutiny, to adopt new and more flexible universal policies.

In the meantime, we are seeing changes happen on a country-by-country basis.

Just yesterday, Apple reached a settlement in Japan that will let publishers of “reader” apps (those for using or consuming media like books and news, music, files in the cloud and more) to redirect users to external sites to provide alternatives to Apple’s proprietary in-app payment provision. Although it’s not as seamless as paying within the app, redirecting previously was typically not allowed, and in doing so the publishers can avoid Apple’s cut.

South Korean legislators earlier this week approved a measure that will make it illegal for Apple and Google to make a commission by forcing developers to use their proprietary payment systems.

And last week, Apple also made some movements in the U.S. around allowing alternative forms of payments, but, relatively speaking, the concessions were somewhat indirect: app publishers can refer to alternative, direct payment options in apps now, but not actually offer them. (Not yet at least.)

Some developers and consumers have been arguing for years that Apple’s strict policies should open up more. Apple however has long said in its defense that it mandates certain developer policies to build better overall user experiences, and for reasons of security. But, as app technology has evolved, and consumer habits have changed, critics believe that this position needs to be reconsidered.

One factor in Apple’s defense in India specifically might be the company’s position in the market. Android absolutely dominates India when it comes to smartphones and mobile services, with Apple actually a very small part of the ecosystem.

As of the end of 2020, it accounted for just 2% of the 520 million smartphones in use in the country, according to figures from Counterpoint Research quoted by Reuters. That figure had doubled in the last five years, but it’s a long way from a majority, or even significant minority.

The antitrust filing in India has yet to be filed formally, but Reuters notes that the wording leans on the fact that anti-competitive practices in payments systems make it less viable for many publishers to exist at all, since the economics simply do not add up:

“The existence of the 30% commission means that some app developers will never make it to the market,” Reuters noted from the filing. “This could also result in consumer harm.”

Powered by WPeMatico

After a 17-hour marathon through nearly 200 startup pitches, the Equity team was fired up to get back on Twitter and chat through some early trends and favorites from the first day of Y Combinator’s demo party. We’ll be back on the air tomorrow, so make sure you’re following the show on Twitter so you don’t miss out.

What did Natasha and Alex chat about? The following:

TechCrunch has extensive coverage of the day on the site, so there’s lots to dig into if you are in the mood. More tomorrow!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Even as hundreds of millions of people in India have a bank account, only a tiny fraction of this population invests in any financial instrument.

Fewer than 30 million people invest in mutual funds or stocks, for instance. In recent years, a handful of startups have made it easier for users — especially the millennials — to invest, but the figure has largely remained stagnant.

Now, an Indian startup believes that it has found the solution to tackle this challenge — and is already seeing good early traction.

Nishchay AG, former director of mobility startup Bounce, and Misbah Ashraf, co-founder of Marsplay (sold to Foxy), founded Jar earlier this year.

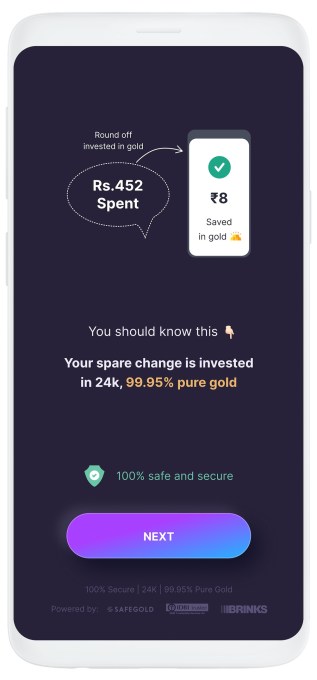

The startup’s eponymous six-month-old Android app enables users to start their savings journey for as little as 1 Indian rupee.

Users on Jar can invest in multiple ways and get started within seconds. The app works with Paytm (PhonePe support is in the works) to set up a recurring payment. (The startup is the first to use UPI 2.0’s recurring payment support.) They can set up any amount between 1 Indian rupee to 500 for daily investments.

The Jar app can also glean users’ text messages and save a tiny amount based on each monetary transaction they do. So, for instance, if a user has spent 31 rupees in a transaction, the Jar app rounds that up to the nearest tenth figure (40, in this case) and saves nine rupees. Users can also manually open the app and spend any amount they wish to invest.

Once users have saved some money in Jar, the app then invests that into digital gold.

The startup is using gold investment because people in the South Asian market already have an immense trust in this asset class.

India has a unique fascination for gold. From rural farmers to urban working class, nearly everyone stashes the yellow metal and flaunts jewelry at weddings.

Indian households are estimated to have a stash of over 25,000 tons of the precious metal whose value today is about half of the country’s nominal GDP. Such is the demand for gold in India that the South Asian nation is also one of the world’s largest importers of this precious metal.

Jar’s Android app (Image Credits: Jar)

“When you’re thinking about bringing the next 500 million people to institutional savings and investments, the onus is on us to educate them on the efficacies of the other instruments that are in the market,” said Nishchay.

“We want to give them the instrument they trust the most, which is gold,” he said. The startup plans to eventually offer several more investment opportunities, he said.

The founders met several years ago when they were exploring if MarsPlay and Bounce could have any synergies. They stayed in touch and, last year during one of their many conversations, realized that neither of them knew much about investments.

“That’s when the dots started to connect,” said Misbah, drawing stories from his childhood. “I come from a small town in Bihar called Bihar Sharif. During my childhood days, I saw my family deeply troubled with debt because of poor financial decisions and no savings,” he said.

“We both understand what a typical middle class family goes through. Someone who comes from this background never had any means in the past but their aspirations are never-ending. So when you start earning, you immediately start to spend it all,” said Nishchay.

“The market needs products that will help them get started,” he said.

That idea, which is similar to Acorn and Stash’s play in the U.S. market, is beginning to make inroads. The app has already amassed about half a million downloads, the founders said. Investors have taken notice, too.

On Wednesday, Jar announced it has raised $4.5 million from a clutch of high-profile investors, including Arkam Ventures, Tribe Capital, WEH Ventures, and angels including Kunal Shah (founder of CRED), Shaan Puri (formerly with Twitch), Ali Moiz (founder of Stonks), Howard Lindzon (founder of Social Leverage), Vivekananda Hallekere (co-founder of Bounce), Alvin Tse (of Xiaomi) and Kunal Khattar (managing partner at AdvantEdge).

“Over 400 million Indians are about to embrace digital financial services for the first time in their lives. Jar has built an app that is poised to help them — with several intuitive ways including gamification — start their investment journey. We love the speed at which the team has been executing and how fast they are growing each week,” said Arjun Sethi, co-founder of Tribe Capital, in a statement.

Transactions and AUM on the Jar app are surging 350% each month, said Nishchay. The startup plans to broaden its product offerings in the coming days, he said.

Powered by WPeMatico

Apna, a 21-month-old startup that is helping millions of blue- and gray-collar workers in India upskill themselves, find communities and land jobs, is inching closer to becoming the fastest tech firm in the world’s second-largest internet market to become a unicorn.

Tiger Global is in advanced stages of talks to lead a $100 million round in Apna, according to four sources familiar with the matter. The proposed terms value the startup at over $1 billion, the sources said.

The round hasn’t closed yet, so terms of the deal may change, some of the sources cautioned.

If the round materializes, Apna will become the youngest Indian startup to attain the much-coveted unicorn status. The startup, which launched its app in December 2019, was valued at $570 million in its Series B financing round in June this year. It will also be the third financing round Apna would have secured in a span of less than seven months.

Tiger Global, an existing investor in Apna, didn’t respond to a request for comment earlier this month. Apna founder and chief executive Nirmit Parikh, an Apple alum, declined to comment on Tuesday.

Indian cities are home to hundreds of millions of low-skilled workers who hail from villages in search of work. Many of them have lost their jobs amid the coronavirus pandemic that has slowed several economic activities in the world’s second-largest internet market.

Apna, whose name is inspired from a 2019 Bollywood song, is building a scalable networking infrastructure so that these workers can connect to the right employers and secure jobs. On its eponymous Android app, users also upskill themselves, review their interview skills and become eligible for more jobs.

As of June this year, Apna had amassed over 10 million users and was facilitating more than 15 million job interviews each month. All jobs listed on the Apna platform are verified by the startup and free of cost for the candidates.

The startup has also partnered with some of India’s leading public and private organizations and is providing support to the Ministry of Minority Affairs of India, National Skill Development Corporation and UNICEF YuWaah to provide better skilling and job opportunities to candidates.

The investment talks further illustrate Tiger Global’s growing interest in India. The New York-headquartered firm has made several high-profile investments in India this year, including in BharatPe, Gupshup, DealShare, Classplus, Urban Company, CoinSwitch Kuber and Groww.

More than two dozen Indian startups have become a unicorn this year, up from 11 last year, as several high-profile investors, including Tiger Global, SoftBank and Falcon Edge, have increased the pace of their investments in the world’s second most populous nation.

Apna also counts Insight Partners, Lightspeed and Sequoia Capital among its existing investors.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here. I also tweet.

Today’s show was good fun to put together. Here’s what we got to:

Woo! And that’s the start to the week. Hugs from here, and we’ll chat you on Wednesday!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Our beloved Danny was back, joining Natasha and Alex and Grace and Chris to chat through yet another incredibly busy week. As a window into our process, every week we tell one another that the next week we’ll cut the show down to size. Then the week is so interesting that we end up cutting a lot of news, but also keeping a lot of news. The chaotic process is a work in progress, but it means that the end result is always what we decided we can’t not talk about.

Here’s what we got into:

Powered by WPeMatico