Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

Today Intercom announced that it has hired a chief financial officer (CFO) as it ramps toward an IPO. The unicorn also promoted its COO to the CEO role earlier this year.

The company’s recent CEO, Karen Peacock, told TechCrunch that her new CFO Dan Griggs was a strong candidate thanks to his experience helping take Rocket Fuel public, and for helping execute a “whole business transformation” at Sitecore, where he worked immediately before coming to Intercom.

Intercom is a software startup that sells customer-chat software that works with support and marketing teams. Different tiers of its service allow for automated “conversational” campaigns, and custom bots. The company has raised a hair over $240 million, according to PitchBook data.

Griggs told TechCrunch that he was not in the market for a new role, but conversations with Peacock drew him in.

Peacock took over the CEO role after around three years as the company’s COO, during which time it became known that the preceding CEO had made “unwanted advances” on employees. Intercom also underwent layoffs before Peacock took over the helm. According to reporting, the firm cut around 6% of its staff in May, a time when many tech companies were trimming personnel due to market uncertainties surrounding COVID-19 and its economic disruptions. (Update: Following publication, Intercom stressed that co-founder Eoghan McCabe earned support from its board after an investigation into the allegations in 2019. During a call, the company also emphasized that an external party had executed the investigation.)

Now Intercom has a refreshed C-suite, and is at IPO scale.

According to TechCrunch reporting at the time Peacock took over as CEO, Intercom had around $150 million in annual recurring revenue (ARR). The company clarified to TechCrunch that the ARR milestone was reached at the end of its last fiscal year, or the conclusion of January of 2020.

Dan Griggs, via the company.

Intercom, Griggs said, is near profitability and is growing in the “strong” double digits. We read that as meaning between 50% and 99% growth, implying the company could close its current fiscal year (January 2021) with $225 million to $298.5 million in ARR, with a bias — thanks to the laws of large numbers — toward the smaller figure.

With a CFO with IPO experience on hand, a new CEO, a material revenue base and good growth, when is the IPO? Not soon, sadly. The CFO said his company doesn’t need to raise new capital, and that it has enough liquidity today to invest. That’s financial-speak for “no rush.”

The CEO is on the same page, saying during the same call that Intercom is not in a hurry to go public, and wants to build out some internal infrastructure before executing the transaction. There won’t be an IPO for at least 12 months, she estimated.1 (Update: Intercom reached out after publication to clarify that the timeline discussed in our call was imprecise. The IPO is at least two years away.)

Intercom hit some market chop in 2020 and had to spend parts of the last year or so cleaning up internal issues. Now, in theory, it has sorted house, and is operating in a market that has greatly rewarded software startups in recent quarters, especially those helping other companies operate digitally.

Let’s see how fast Intercom can grow. We’ll get the full retrospective with its eventual S-1.

Powered by WPeMatico

“Marketing cloud” has become an increasingly popular concept in the world of marketing technology — used by the likes of Salesforce, Adobe, Oracle and others to describe their digital tool sets for organizations to identify and connect with customers. Now, a startup that is building its own take on the idea aimed specifically at e-commerce companies is announcing some funding after seeing a surge of business in the last few months.

Yotpo, which provides a suite of tool to help direct-to-consumer and other e-commerce players build better relationships with customers, is today announcing that it has raised $75 million in funding, money it will use to continue growing its suite of products, as well as to acquire more customers and build out more integration partnerships.

The Series E included a number of Yotpo’s existing investors, namely Bessemer Venture Partners, Access industries (the owner of Warner Music Group, among a number of other holdings) and Vertex Ventures (a subsidiary of Temasek), new investor Hanaco (which focuses on Israeli startups — Yotpo is co-headquartered in Tel Aviv and New York) and other unnamed investors.

It brings the total raised by the startup to $176 million, and while it’s not disclosing valuation, its CEO Tomer Tagrin — who co-founded the company with COO Omri Cohen — describes it as “nearly a unicorn.”

“I like to call what we’re building a flamingo, which is also a rare and beautiful animal but also a real thing, and we are a proper business,” he said in an interview, adding that Yotpo is on target for ARR next year to be $100 million.

The company had its start as an app in Shopify’s App Store, providing tools to Shopify customers to help with customer engagement by way of user-generated content, and while it has outgrown that single relationship — it now has some 500 additional strategic partners, including Salesforce, Adobe, BigCommerce and others — Yotpo’s CEO still likes to describe his company in Shopify-ish terms.

“Just as Shopify manages your business, we manage your customers end to end,” Tagrin said. He said that while it’s great to see the bigger trend of consolidation around marketing clouds, it’s not a one-size-fits-all problem. He believes Yotpo’s e-commerce-specific approach to that stands apart from the pack because it addresses issues unique to D2C and other e-commerce companies.

Yotpo’s services today include SMS and visual marketing, loyalty and referral services and reviews and ratings, which are used by a range of e-commerce companies, spanning from newer direct-to-consumer brands like Third Love and Away, to more established names like Patagonia and 1-800-Flowers. Some of these have been built in-house, and some by way of acquisition — most recently, SMSBump, in January. The plan is to use some of the funding to continue that acquisition strategy.

“Since our first investment more than three years ago, Tomer and Omri have executed flawlessly, expanding the product suite, serving a wider range of customers, and continually hiring strong talent across the organization,” says Adam Fisher, a partner at BVP, in a statement. “Yotpo is singularly focused on helping direct-to-consumer eCommerce brands solve the dual challenge of engaging consumers and increasing revenue, and with their multi-product strategy and innovative edge, they are uniquely positioned to dominate the eCommerce industry for years to come.”

Yotpo is built as a freemium platform, with some 9,000 customers paying for services, and a further 280,000 customers on its free-usage tier. Customer count grew by 250% in the last year, Tagrin said.

The COVID-19 pandemic has had a well-documented impact on internet use, and specifically e-commerce, as people turned to digital channels in record numbers to procure things while complying with shelter-in-place orders, or trying to increase social distancing to slow down the spread of the coronavirus.

E-commerce has been on the rise for years, but the acceleration of that trend has been drastic since February, with revenue and spend both regularly exceeding baseline figures over the last several months, according to research from digital marketing agency Common Thread Collective.

That, in turn, had a big impact on companies that help enable those e-commerce enterprises operate in more direct and personable ways. Yotpo was a direct beneficiary: It said it had a surge of sign-ups of new customers, many taking paid services, working out to a 170% year-on-year ARR and lower customer churn.

The bigger picture, of course, is not completely rosy, with thousands of layoffs across the whole tech service, and a huge number of brick-and-mortar business closures. Those economic indicators could ultimately also have a knock-on effect not just in more business moving online, but also a slowdown in spending overall.

That will inevitably have an impact on startups like Yotpo, too, which is definitely on a rise now but will continue to think longer term about the impact and how it can continue to diversify its products to meet a wider set of customer use cases.

For example, today, the company addresses customer care needs by way of integrations with companies like Zendesk, but longer term it might consider how it can bring in services like this to continue to build out the touchpoints between D2C brands and their customers, and specifically running those through a bigger picture of the customer as profiled on Yotpo’s platform.

This is a big part of our product in our meetings and debates,” Tagrin said about product expansions.

“I do think any celebration of growth and funding comes to me with something else: we need to be internalising more what is going on,” he said. “The world is not back to normal and we shouldn’t act like it is.”

Powered by WPeMatico

EventGeek was a Y Combinator-backed startup that offered tools to help large enterprises manage the logistics of their events. So with the COVID-19 pandemic essentially eliminating large-scale conferences, at least in-person, it’s not exactly surprising that the company had to reinvent itself.

Today, EventGeek relaunched as Circa, with a new focus on virtual events. Founder and CEO Alex Patriquin said that Circa is reusing some pieces of EventGeek’s existing technology, but he estimated that 80% of the platform is new.

While the relaunch only just became official, the startup says its software has already been used to adapt 40,000 in-person events into virtual conferences and webinars.

The immediate challenge, Patriquin said, is simply figuring out how to throw a virtual event — something for which Circa offers a playbook. But the startup’s goals go beyond virtual event logistics.

“Our new focus is really more at the senior marketing stakeholder level, helping them have a unified view of the customer,” Patriquin said.

He explained that “events have always been kind of disconnected from the marketing stack,” so the shift to virtual presents an opportunity to treat event participation as part of the larger customer journey, and to include events in the broader customer record. To that end, Circa integrates with sales and marketing systems like Salesforce and Marketo, as well as with video conferencing platforms like Zoom and On24.

Image Credits: Circa

“We don’t actually deliver [the conference] experience,” Patriquin said. “We put it into that context of the customer journey.”

Liz Kokoska, senior director of demand generation for North America at Circa customer Okta, made a similar point.

“Prior to Circa, we had to manage our physical and virtual events in separate systems, even though we thought of them as parts of the same marketing channel,” Kokoska said in a statement. “With Circa, we now have a single view of all our events in one place — this is helpful in planning and company-wide visibility on marketing activity. Being able to seamlessly adapt to the new world of virtual and hybrid events has given our team a significant advantage.”

And as Patriquin looks ahead to a world where large conferences are possible again, he predicted that there’s still “a really big opportunity for the events industry and for Circa.”

“As in-person events start to come back, there’s going to be a phase where health and safety are going to be paramount,” he continued. “After that health and safety phase, it’s going to be the age of hybrid events — where everything is virtual right now, hybrid will provide the opportunity to bring key [virtual] learnings back into the in-person world, to have a lot more data and intelligence and really be able to personalize an attendee’s experience.”

Powered by WPeMatico

As COVID-19 infections surge in parts of the U.S., many workplaces remain empty or are operating with skeleton crews.

Most agree that the decision to return to the office should involve a combination of business, government and medical officials and scientists who have a deep understanding of COVID-19 and infectious disease in general. The exact timing will depend on many factors, including the government’s willingness to open up, the experts’ view of current conditions, business leadership’s tolerance for risk (or how reasonable it is to run the business remotely), where your business happens to be and the current conditions there.

That doesn’t mean every business that can open will, but if and when they get a green light, they can at least begin bringing some percentage of employees back. But what that could look like is clouded in great uncertainty around commutes, office population density and distancing, the use of elevators, how much you can reasonably deep clean, what it could mean to have a mask on for eight hours a day, and many other factors.

To get a sense of how tech companies are looking at this, we spoke to a number of executives to get their perspective. Most couldn’t see returning to the office beyond a small percentage of employees this year. But to get a more complete picture, we also spoke to a physician specializing in infectious diseases and a government official to get their perspectives on the matter.

While there are some guidelines out there to help companies, most of the executives we spoke to found that while they missed in-person interactions, they were happy to take things slow and were more worried about putting staff at risk than being in a hurry to return to normal operations.

Iman Abuzeid, CEO and co-founder at Incredible Health, a startup that helps hospitals find and hire nurses, said her company was half-remote even before COVID-19 hit, but since then, the team is now completely remote. Whenever San Francisco’s mayor gives the go-ahead, she says she will reopen the office, but the company’s 30 employees will have the option to keep working remotely.

She points out that for some employees, working at home has proven very challenging. “I do want to highlight two groups that are pretty important that need to be highlighted in this narrative. First, we have employees with very young kids, and the schools are closed so working at home forever or even for the rest of this year is not really an option, and then the second group is employees who are in smaller apartments, and they’ve got roommates and it’s not comfortable to work at home,” Abuzeid explained.

Those folks will need to go to the office whenever that’s allowed, she said. For Lindsay Grenawalt, chief people officer at Cockroach Labs, an 80-person database startup in NYC, said there has to be a highly compelling reason to bring people back to the office at this point.

Powered by WPeMatico

The cloud market is coming into its own during the pandemic as the novel coronavirus forced many companies to accelerate plans to move to the cloud, even while the market was beginning to mature on its own.

This week, the big three cloud infrastructure vendors — Amazon, Microsoft and Google — all reported their earnings, and while the numbers showed that growth was beginning to slow down, revenue continued to increase at an impressive rate, surpassing $30 billion for a quarter for the first time, according to Synergy Research Group numbers.

Powered by WPeMatico

As the Internet of Things proliferates, security cameras are getting smarter. Today, these devices have machine learning capability that helps the camera automatically identify what it’s looking at — for instance, an animal or a human intruder? Today, Cisco announced that it has acquired Swedish startup Modcam and is making it part of its Meraki smart camera portfolio with the goal of incorporating Modcam computer vision technology into its portfolio.

The companies did not reveal the purchase price, but Cisco tells us that the acquisition has closed.

In a blog post announcing the deal, Cisco Meraki’s Chris Stori says Modcam is going to up Meraki’s machine learning game, while giving it some key engineering talent, as well.

“In acquiring Modcam, Cisco is investing in a team of highly talented engineers who bring a wealth of expertise in machine learning, computer vision and cloud-managed cameras. Modcam has developed a solution that enables cameras to become even smarter,” he wrote.

What he means is that today, while Meraki has smart cameras that include motion detection and machine learning capabilities, this is limited to single camera operation. What Modcam brings is the added ability to gather information and apply machine learning across multiple cameras, greatly enhancing the camera’s capabilities.

“With Modcam’s technology, this micro-level information can be stitched together, enabling multiple cameras to provide a macro-level view of the real world,” Stori wrote. In practice, as an example, that could provide a more complete view of space availability for facilities management teams, an especially important scenario as businesses try to find safer ways to open during the pandemic. The other scenario Modcam was selling was giving a more complete picture of what was happening on the factory floor.

All of Modcams employees, which Cisco described only as “a small team,” have joined Cisco, and the Modcam technology will be folded into the Meraki product line, and will no longer be offered as a standalone product, a Cisco spokesperson told TechCrunch.

Modcam was founded in 2013 and has raised $7.6 million, according to Crunchbase data. Cisco acquired Meraki back in 2012 for $1.2 billion.

Powered by WPeMatico

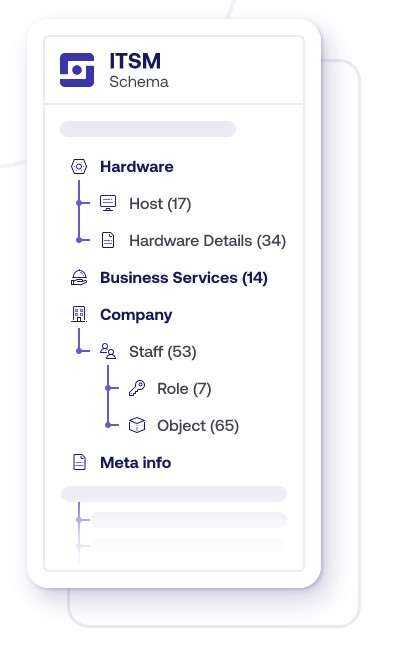

Atlassian today announced that it has acquired Mindville, a Jira-centric enterprise asset management firm based in Sweden. Mindville’s more than 1,700 customers include the likes of NASA, Spotify and Samsung.

Image Credits: Atlassian

With this acquisition, Atlassian is getting into a new market, too, by adding asset management tools to its lineup of services. The company’s flagship product is Mindville Insights, which helps IT, HR, sales, legal and facilities to track assets across a company. It’s completely agnostic as to which assets you are tracking, though, given Atlassian’s user base, most companies will likely use it to track IT assets like servers and laptops. But in addition to physical assets, you also can use the service to automatically import cloud-based servers from AWS, Azure and GCP, for example, and the team has built connectors to services like Service Now and Snow Software, too.

Image Credits: Mindville

“Mindville Insight provides enterprises with full visibility into their assets and services, critical to delivering great customer and employee service experiences. These capabilities are a cornerstone of IT Service Management (ITSM), a market where Atlassian continues to see strong momentum and growth,” Atlassian’s head of tech teams Noah Wasmer writes in today’s announcement.

Co-founded by Tommy Nordahl and Mathias Edblom, Mindville never raised any institutional funding, according to Crunchbase. The two companies also didn’t disclose the acquisition price.

Like some of Atlassian’s other recent acquisitions, including Code Barrel, the company was already an Atlassian partner and successfully selling its service in the Atlassian Marketplace.

“This acquisition builds on Atlassian’s investment in [IT Service Management], including recent acquisitions like Opsgenie for incident management, Automation for Jira for code-free automation, and Halp for conversational ticketing,” Atlassian’s Wasmer writes.

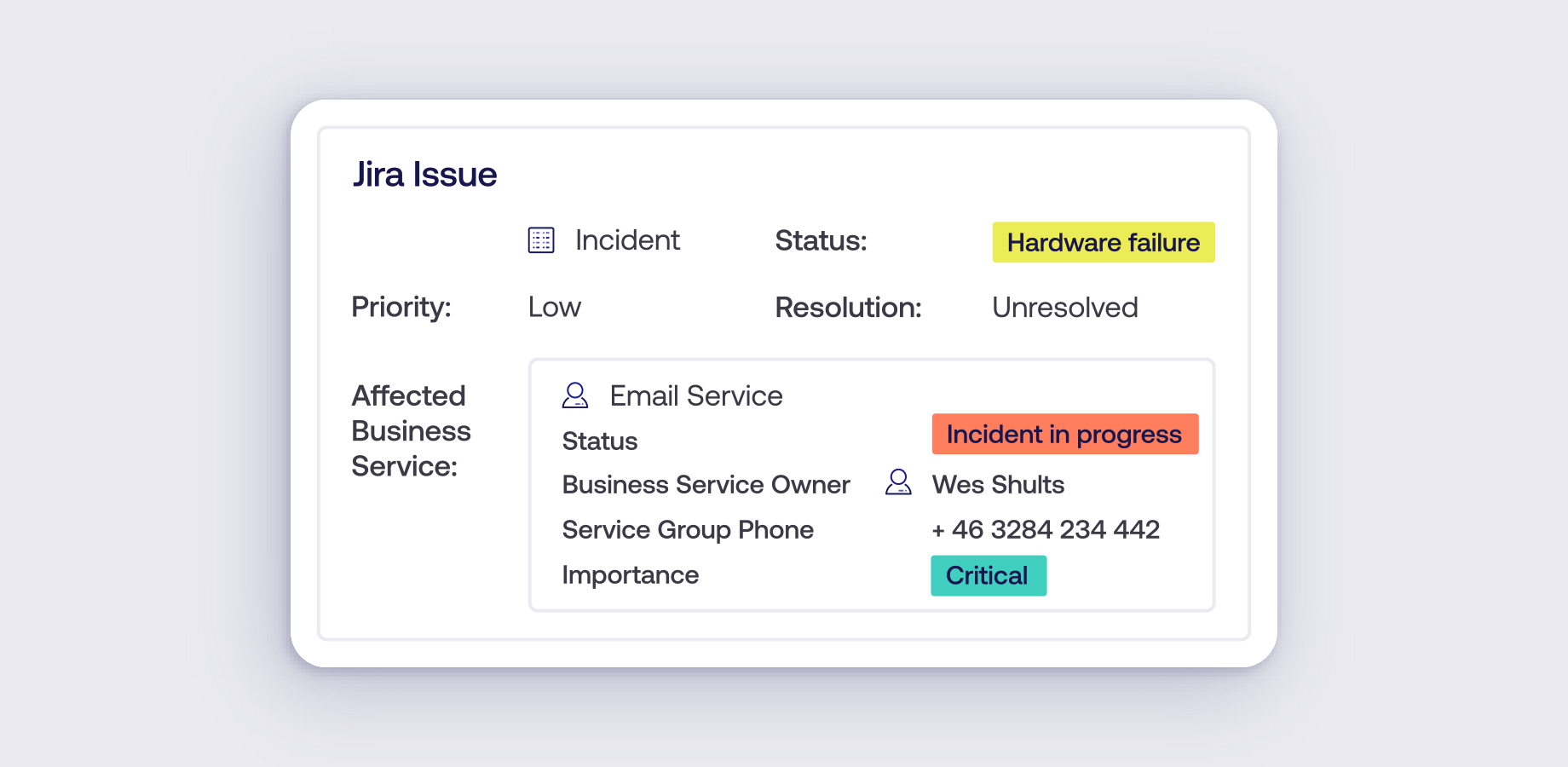

The Mindville team says it will continue to support existing customers and that Atlassian will continue to build on Insight’s tools while it works to integrate them with Jira Service Desk. That integration, Atlassian argues, will give its users more visibility into their assets and allow them to deliver better customer and employee service experiences.

Image Credits: Mindville

“We’ve watched the Insight product line be used heavily in many industries and for various disciplines, including some we never expected! One of the most popular areas is IT Service Management where Insight plays an important role connecting all relevant asset data to incidents, changes, problems, and requests,” write Mindville’s founders in today’s announcement. “Combining our solutions with the products from Atlassian enables tighter integration for more sophisticated service management, empowered by the underlying asset data.”

Powered by WPeMatico

In the monitoring world, typically when you spin up a new instance, you pay a fee to monitor it. If you are particularly active in any given month, that can result in a hefty bill at the end of the month. That leads to limiting what you choose to monitor, to control costs. New Relic wants to change that, and today it announced it’s moving to a model where customers pay by the user instead, with a smaller, less costly data component.

The company is also simplifying its product set with the goal of encouraging customers to instrument everything instead of deciding what to monitor and what to leave out to control cost. “What we’re announcing is a completely reimagined platform. We’re simplifying our products from 11 to three, and we eliminate those barriers to standardizing on a single source of truth,” New Relic founder and CEO Lew Cirne told TechCrunch.

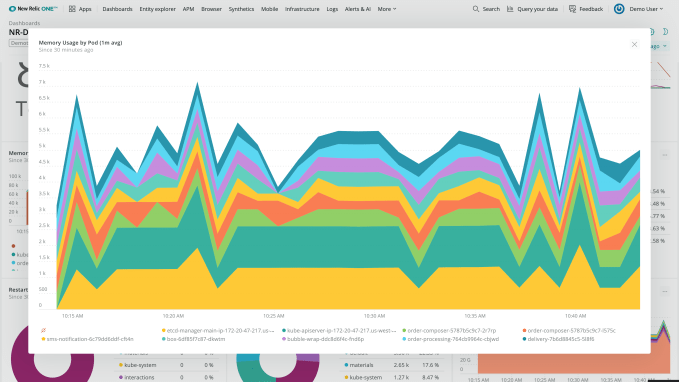

The way the company can afford to make this switch is by exposing the underlying telemetry database that it created to run its own products. By taking advantage of this database to track all of your APM, tracing and metric data all in one place, Cirne says they can control costs much better and pass those savings onto customers, whose bills should be much smaller based on this new pricing model, he said.

“Prior to this, there has not been any technology that’s good at gathering all of those data types into a single database, what we would call a telemetry database. And we actually created one ourselves and it’s the backbone of all of our products. [Up until now], we haven’t really exposed it to our customers, so that they can put all their data into it,” he said.

New Relic Telemetry Data. Image Credit: New Relic

The company is distilling the product set into three main categories. The first is the Telemetry Data Platform, which offers a single way to gather any events, logs or traces, whether from their agents or someone else’s or even open-source monitoring tools like Prometheus.

The second product is called Full-stack Observability. This includes all of their previous products, which were sold separately, such as APM, mobility, infrastructure and logging. Finally they are offering an intelligence layer called New Relic AI.

Cirne says by simplifying the product set and changing the way they bill, it will save customers money through the efficiencies they have uncovered. In practice, he says, pricing will consist of a combination of users and data, but he believes their approach will result in much lower bills and more cost certainty for customers.

“It’ll vary by customer, so this is just a rough estimate, but imagine that the typical New Relic bill under this model will be a 70% per user charge and 30% data charge, roughly, but so if that’s the case, and if you look at our competitors, 100% of the bill is data,” he said.

The new approach is available starting today. Companies can try it with a 100 GB single-user account.

Powered by WPeMatico

Buildots, a Tel Aviv and London-based startup that is using computer vision to modernize the construction management industry, today announced that it has raised $16 million in total funding. This includes a $3 million seed round that was previously unreported and a $13 million Series A round, both led by TLV Partners. Other investors include Innogy Ventures, Tidhar Construction Group, Ziv Aviram (co-founder of Mobileye & OrCam), Magma Ventures head Zvika Limon, serial entrepreneurs Benny Schnaider and Avigdor Willenz, as well as Tidhar chairman Gil Geva.

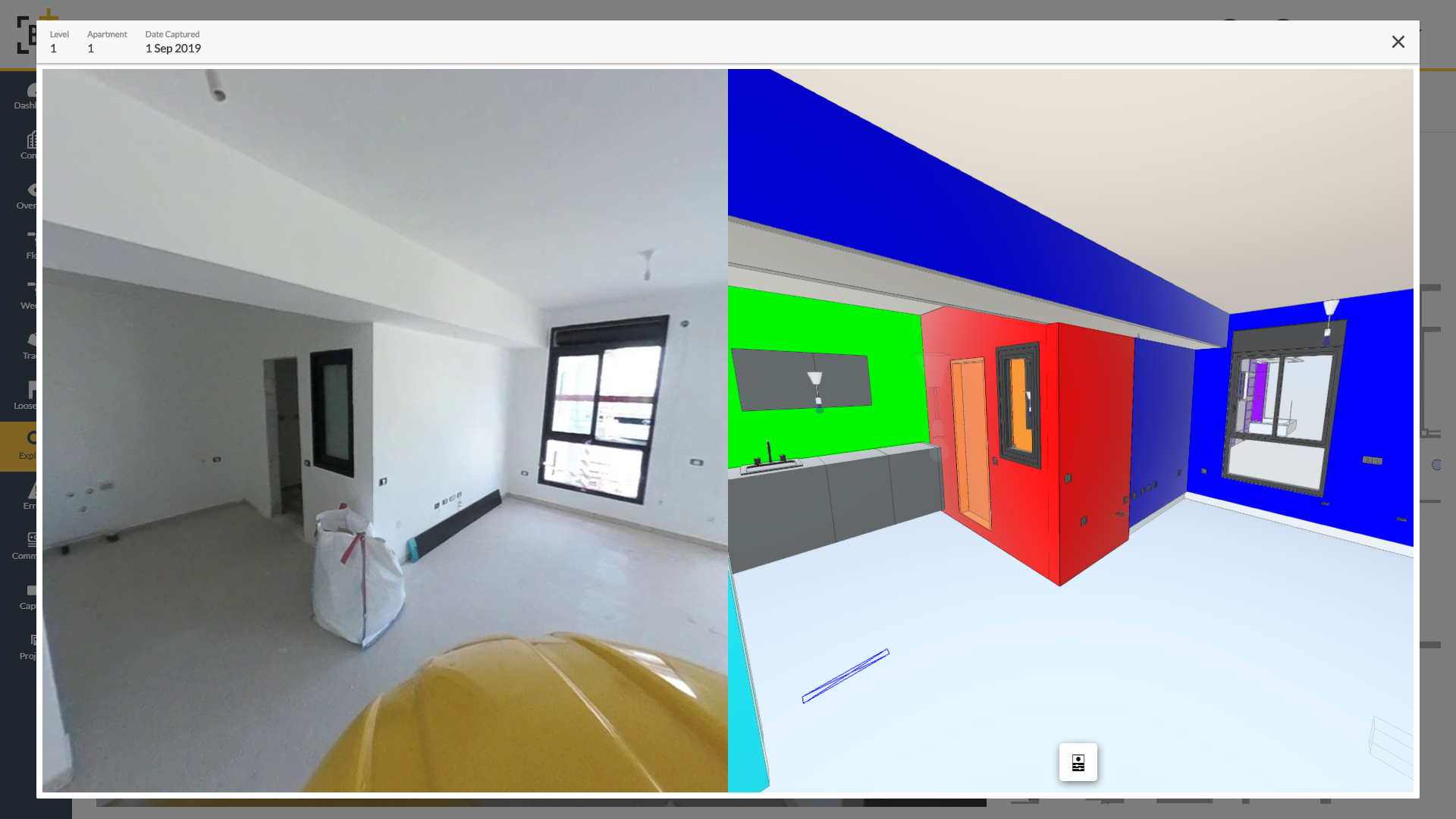

The idea behind Buildots is pretty straightforward. The team is using hardhat-mounted 360-degree cameras to allow project managers at construction sites to get an overview of the state of a project and whether it remains on schedule. The company’s software creates a digital twin of the construction site, using the architectural plans and schedule as its basis, and then uses computer vision to compare what the plans say to the reality that its tools are seeing. With this, Buildots can immediately detect when there’s a power outlet missing in a room or whether there’s a sink that still needs to be installed in a kitchen, for example.

“Buildots have been able to solve a challenge that for many seemed unconquerable, delivering huge potential for changing the way we complete our projects,” said Tidhar’s Geva in a statement. “The combination of an ambitious vision, great team and strong execution abilities quickly led us from being a customer to joining as an investor to take part in their journey.”

The company was co-founded in 2018 by Roy Danon, Aviv Leibovici and Yakir Sundry. Like so many Israeli startups, the founders met during their time in the Israeli Defense Forces, where they graduated from the Talpiot unit.

“At some point, like many of our friends, we had the urge to do something together — to build a company, to start something from scratch,” said Danon, the company’s CEO. “For us, we like getting our hands dirty. We saw most of our friends going into the most standard industries like cloud and cyber and storage and things that obviously people like us feel more comfortable in, but for some reason we had like a bug that said, ‘we want to do something that is a bit harder, that has a bigger impact on the world.’ ”

So the team started looking into how it could bring technology to traditional industries like agriculture, finance and medicine, but then settled upon construction thanks to a chance meeting with a construction company. For the first six months, the team mostly did research in both Israel and London to understand where it could provide value.

Danon argues that the construction industry is essentially a manufacturing industry, but with very outdated control and process management systems that still often relies on Excel to track progress.

Image Credits: Buildots

Construction sites obviously pose their own problems. There’s often no Wi-Fi, for example, so contractors generally still have to upload their videos manually to Buildots’ servers. They are also three dimensional, so the team had to develop systems to understand on what floor a video was taken, for example, and for large indoor spaces, GPS won’t work either.

The teams tells me that before the COVID-19 lockdowns, it was mostly focused on Israel and the U.K., but the pandemic actually accelerated its push into other geographies. It just started work on a large project in Poland and is scheduled to work on another one in Japan next month.

Because the construction industry is very project-driven, sales often start with getting one project manager on board. That project manager also usually owns the budget for the project, so they can often also sign the check, Danon noted. And once that works out, then the general contractor often wants to talk to the company about a larger enterprise deal.

As for the funding, the company’s Series A round came together just before the lockdowns started. The company managed to bring together an interesting mix of investors from both the construction and technology industries.

Now, the plan is to scale the company, which currently has 35 employees, and figure out even more ways to use the data the service collects and make it useful for its users. “We have a long journey to turn all the data we have into supporting all the workflows on a construction site,” said Danon. “There are so many more things to do and so many more roles to support.”

Image Credits: Buildots

Powered by WPeMatico

Financial services companies like banks and insurance tend to be heavily regulated. As such, they require a special level of security and auditability. Hearsay, which makes compliant communications tools for these types of companies, announced a new partnership with Salesforce today, enabling smooth integration with Salesforce CRM and marketing automation tools.

The company also announced that Salesforce would be taking a minority stake in Hearsay, although company co-founder and CEO Clara Shih, did not provide any details on that part of the announcement.

Shih says the company created the social selling category when it launched 10 years ago. Today, it provides a set of tools like email, messaging and websites along with a governance layer to help financial services companies interact with customers in a compliant way. Their customers are primarily in banking, insurance, wealth management and mortgages.

She said that they realized if they could find a way to share the data they were collecting with the Hearsay tool set with CRM and marketing automation software in an automated way, it would make greater use of this information than it could on its own. To that end, they have created a set of APIs to enable that with some built-in connectors. The first one will be to connect Hearsay to Salesforce, with plans to add other vendors in the future.

“It’s about being able to connect [data from Hearsay] with the CRM system of record, and then analyzing it across thousands, if not tens of thousands of advisors or bankers in a single company, to uncover best practices. You could then use that information like GPS driving directions that help every advisor behave in the moment and reach out in the moment like the very best advisor would,” Shih explained.

In practice, this means sharing the information with the customer data platform (CDP), the CRM and marketing automation tooling to deliver more intelligent targeting based on a richer body of information. So the advisor can use information gleaned from everything he or she knows about the client across the set of tools to deliver a more meaningful personal message instead of a targeted ad or an email blast. As Shih points out, the ad might even make sense, but could be tone deaf depending on the circumstances.

“What we focus on is this human-client experience, and that can only be delivered in the last mile because it’s only with the advisor that many clients will confide in these very important life events and life decisions, and then conversely, it’s only in the last mile that the trusted advisor can deliver relationship advice,” she said.

She says what they are trying to do by combining streams of data about the customer is build loyalty in a way that pure technology solutions just aren’t capable of doing. As she says, nobody says they are switching banks because it has the best chat bot.

Hearsay was founded in 2009 and has raised $51 million, as well as whatever other money Salesforce will be adding to the mix with today’s investment. Other investors include Sequoia and NEA Associates. Its last raise was way back in 2013, a $30 million Series C.

Powered by WPeMatico