Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

If businesses are going to meet their increasingly aggressive targets for reducing the greenhouse gas emissions associated with their operations, they’re going to have to have an accurate picture of just what those emissions look like. To get that picture, companies are increasingly turning to businesses like Sweep, which announced its commercial launch today.

The Parisian company boasts a founding team with an impeccable pedigree in enterprise software. Co-founders Rachel Delacour and Nicolas Raspal were the co-founders of BIME Analytics, which was acquired by Zendesk. And together with Zendesk colleagues Raphael Güller and Yannick Chaze, and the founder of the Net Zero Initiative, Renaud Bettin, they’ve created a software toolkit that gives companies a visually elegant view into not just a company’s own carbon emissions, but those of their suppliers as well.

It’s the background of the team that first attracted investors like Pia d’Iribarne, co-founder and managing partner, New Wave, which made their first climate-focused investment into the software developer.

“We decided to invest before we even closed the fund,” d’Iribarne said of the investment in Sweep. “We officially invested in December or January.”

New Wave wasn’t the only investor wowed by the company’s prospects. The new European climate-focused investment firm 2050, and La Famiglia, a fund with strong ties to big European industrial companies, also participated alongside several undisclosed angel investors from the Bay Area. In all Sweep raked in $5 million for its product before it had even launched a beta.

Sweep offers users the ability to visualize each location of a company’s business by brand, location, product or division and see how those different granular operations contribute to a company’s overall carbon footprint. Users can also link those nodes to external suppliers and distributors to share carbon data.

The effects of climate change are increasing, and companies across industries are motivated to do their part. But today’s carbon reduction efforts are being stalled by complex tools and resources that can’t match the urgency of the threat. By putting automation, connectivity and collaboration at the heart of the platform, Sweep is the first to offer companies an efficient mechanism to tackle their indirect Scope 3 emissions, and turn net zero from a buzzword into a reality.

Like the other companies that have come on the market with carbon monitoring and management solutions, Sweep also offers the ability to finance offset projects directly from its platform. And, like those other companies, Sweep’s offsets are primarily in the forestry space.

“Around the world, companies are under pressure from customers, investors and regulators to take action to reduce their emissions,” said Pia d’Iribarne in a statement. “As a result, we’re seeing unprecedented growth in the climate technology market and we expect it to continue to explode. What used to be an issue confined to a company’s sustainability team is now a front-and-center business objective that has the commitment of the CEO. We invested in Sweep because of their world-class expertise in sustainability and their success in developing state-of-the-art, end-to-end SaaS platforms. It’s the right team and the right product at the right time.”

Powered by WPeMatico

Data intelligence company Near is announcing the acquisition of another company in the data business — UM.

In some ways, this echoes Near’s acquisition of Teemo last fall. Just as that deal helped Singapore-headquartered Near expand into Europe (with Teemo founder and CEO Benoit Grouchko becoming Near’s chief privacy officer), CEO Anil Mathews said that this new acquisition will help Near build a presence in the United States, turning the company into “a truly global organization,” while also tailoring its product to offer “local flavors” in each country.

The addition of UM’s 60-person team brings Near’s total headcount to around 200, with UM CEO Gladys Kong becoming CEO of Near North America.

At the same time, Mathews suggested that this deal isn’t simply about geography, because the data offered by Near and UM are “very complementary,” allowing both teams to upsell current customers on new offerings. He described Near’s mission as “merging two diverse worlds, the online world and the offline world,” essentially creating a unified profile of consumers for marketers and other businesses. Apparently, UM is particularly strong on the offline side, thanks to its focus on location data.

Near CEO Anil Mathews and UM CEO Gladys Kong. Image Credits: Near

“UM has a very strong understanding of places, they’ve mastered their understanding of footfalls and dwell times,” Mathews added. “As a result, most of the use cases where UM is seeing growth — in tourism, retail, real estate — are in industries struggling due to the pandemic, where they’re using data to figure out, ‘How do we come out of the pandemic?’ ”

TechCrunch readers may be more familiar with UM under its old name, UberMedia, which created social apps like Echofon and UberSocial before pivoting its business to ad attribution and location data. Kong said that contrary to her fears, the company had “an amazing 2020” as businesses realized they needed UM’s data (its customers include RAND Corporation, Hawaii Tourism Authority, Columbia University and Yale University).

And the year was capped by connecting with Near and realizing that the two companies have “a lot of synergies.” In fact, Kong recalled that UM’s rebranding last month was partly at Mathews’ suggestion: “He said, ‘Why do you have media in your name when you don’t do media?’ And we realized that’s probably how the world saw us, so we decided to change [our name] to make it clear what we do.”

Founded in 2010, UM raised a total of $34.6 million in funding, according to Crunchbase. The financial terms of the acquisition were not disclosed.

Powered by WPeMatico

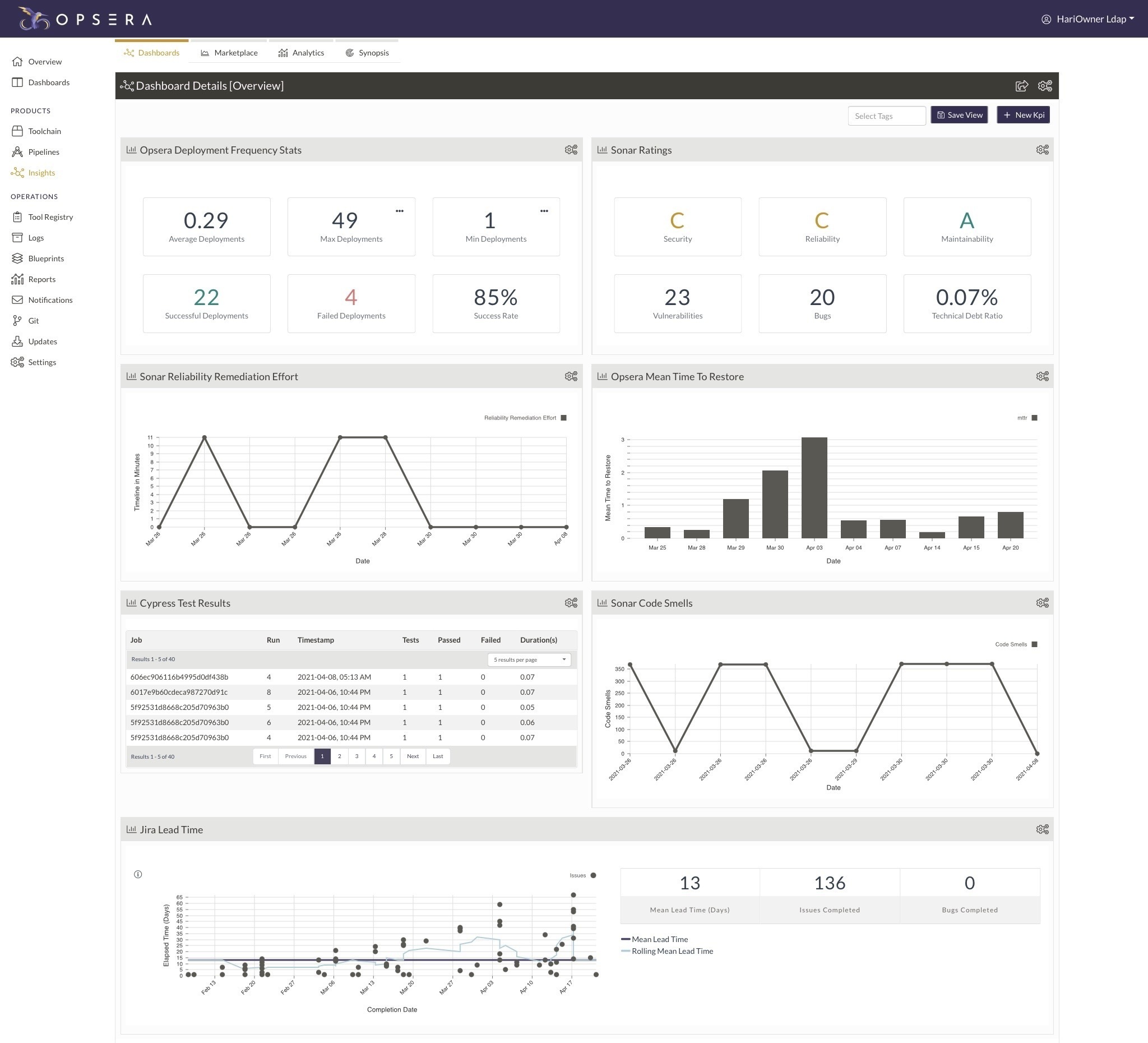

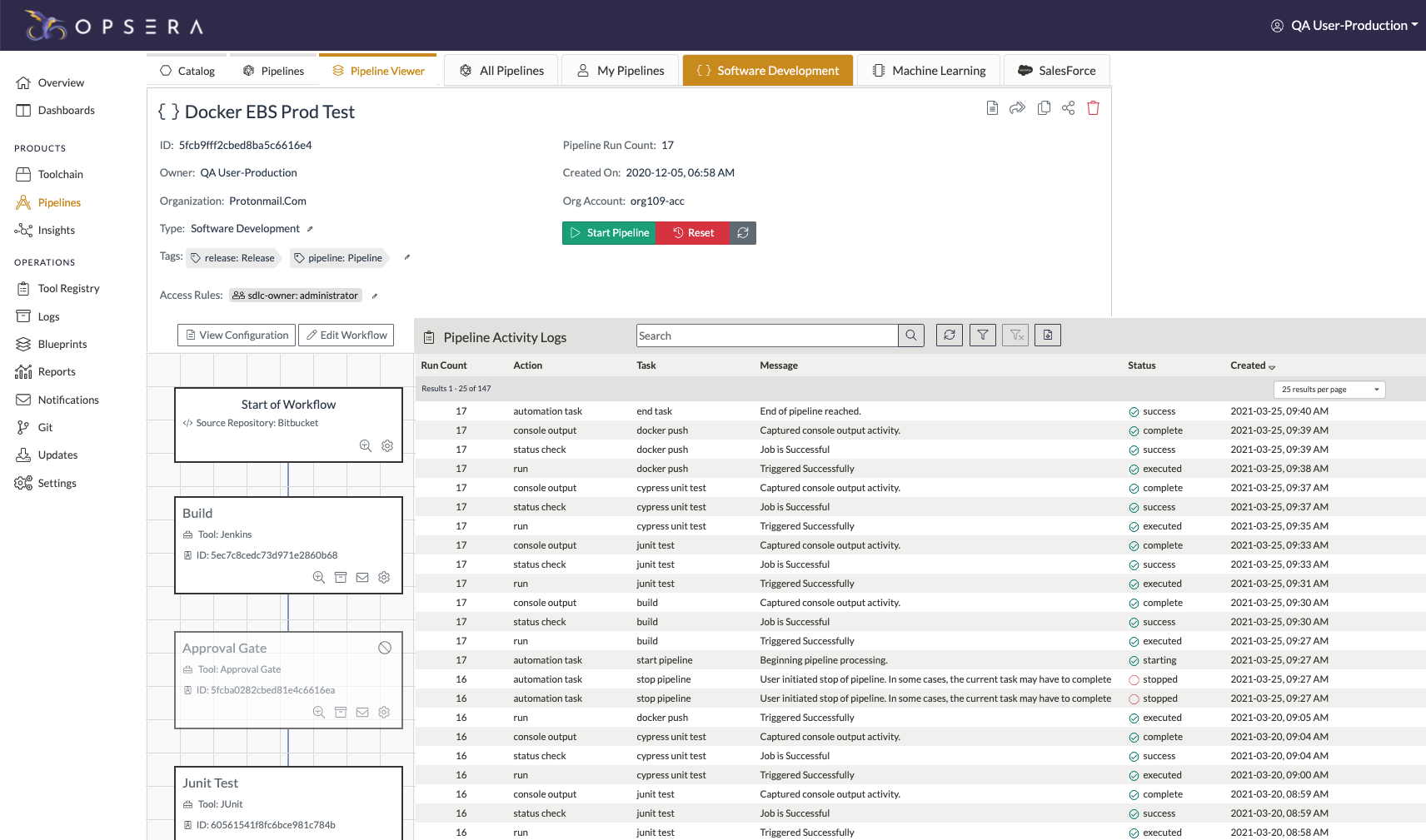

Opsera, a startup that’s building an orchestration platform for DevOps teams, today announced that it has raised a $15 million Series A funding round led by Felicis Ventures. New investor HMG Ventures, as well as existing investors Clear Ventures, Trinity Partners and Firebolt Ventures also participated in this round, which brings the company’s total funding to $19.3 million.

Founded in January 2020, Opsera lets developers provision their CI/CD tools through a single framework. Using this framework, they can then build and manage their pipelines for a variety of use cases, including their software delivery lifecycle, infrastructure as code and their SaaS application releases. With this, Opsera essentially aims to help teams set up and operate their various DevOps tools.

The company’s two co-founders, Chandra Ranganathan and Kumar Chivukula, originally met while working at Symantec a few years ago. Ranganathan then spent the last three years at Uber, where he ran that company’s global infrastructure. Meanwhile, Chivukula ran Symantec’s hybrid cloud services.

Image Credits: Opsera

“As part of the transformation [at Symantec], we delivered over 50+ acquisitions over time. That had led to the use of many cloud platforms, many data centers,” Ranganathan explained. “Ultimately we had to consolidate them into a single enterprise cloud. That journey is what led us to the pain points of what led to Opsera. There were many engineering teams. They all had diverse tools and stacks that were all needed for their own use cases.”

The challenge then was to still give developers the flexibility to choose the right tools for their use cases, while also providing a mechanism for automation, visibility and governance — and that’s ultimately the problem Opsera now aims to solve.

Image Credits: Opsera

“In the DevOps landscape, […] there is a plethora of tools, and a lot of people are writing the glue code,” Opsera co-founder Chivukula noted. “But then they’re not they don’t have visibility. At Opsera, our mission and goal is to bring order to the chaos. And the way we want to do this is by giving choice and flexibility to the users and provide no-code automation using a unified framework.”

Wesley Chan, a managing director for Felicis Ventures who will join the Opsera board, also noted that he believes that one of the next big areas for growth in DevOps is how orchestration and release management is handled.

“We spoke to a lot of startups who are all using black-box tools because they’ve built their engineering organization and their DevOps from scratch,” Chan said. “That’s fine, if you’re starting from scratch and you just hired a bunch of people outside of Google and they’re all very sophisticated. But then when you talk to some of the larger companies. […] You just have all these different teams and tools — and it gets unwieldy and complex.”

Unlike some other tools, Chan argues, Opsera allows its users the flexibility to interface with this wide variety of existing internal systems and tools for managing the software lifecycle and releases.

“This is why we got so interested in investing, because we just heard from all the folks that this is the right tool. There’s no way we’re throwing out a bunch of our internal stuff. This would just wreak havoc on our engineering team,” Chan explained. He believes that building with this wide existing ecosystem in mind — and integrating with it without forcing users onto a completely new platform — and its ability to reduce friction for these teams, is what will ultimately make Opsera successful.

Opsera plans to use the new funding to grow its engineering team and accelerate its go-to-market efforts.

Powered by WPeMatico

Almost two centuries ago, gold prospectors in California set off one of the greatest rushes for wealth in history. Proponents of socially conscious investing claim fund managers will start a similar stampede when they discover that environmental, social and governance (ESG) insights can yield treasure in the form of alternative data that promise big payoffs — if only they knew how to mine it.

First, let’s be clear: ESG is not on the fringe.

There may be some truth to that line of thinking if you take some of the rhetoric and advertising out of the equation.

First, let’s be clear: ESG is not on the fringe. The European Union has implemented new financial regulations via the Sustainable Finance Disclosure Regulation (SFDR). These improve ESG disclosures and considerations and help to direct capital toward products and companies that benefit people and the planet. As we write, the U.S. Securities and Exchange Commission is also considering drafting and implementation of ESG-related regulations.

Whether enacted or currently under consideration, these rules encourage fund managers to integrate sustainability risks into their business processes, report on them publicly, stamp out greenwashing, and promote transparency and knowledge among investors. Accordingly, it will become easier to compare firms’ sustainability efforts, too, allowing stakeholders from all corners to make more informed decisions.

Incorporating ESG factors into investment strategies is not new, of course. The world’s largest asset managers have been practicing it for years. According to the Governance & Accountability Institute, 90% of companies listed on the S&P 500 now produce sustainability reports, an increase of 70 percentage points from more than a decade ago.

Yet some are still groaning about adopting an ESG investing mindset; they see ESG as a nuisance that detracts from their mission of earning high returns. But could this mindset mean they are missing important opportunities?

Waiting for new mandatory ESG reporting and compliance framework standards in the U.S. puts Americas-focused managers at a significant disadvantage. Fund managers can start gaining insights today from alternative data originating in ESG-related data stemming from climate change, natural disasters, harassment and discrimination lawsuits, and other events and information that can be mined.

Powered by WPeMatico

Let’s be clear: The venture capital industry has lacked diversity. The good news is the industry is working to improve itself.

To begin with, as an industry, venture capital can only improve what we measure. In 2016, we set out to develop a rigorous methodology for tracking progress on diversity, equity and inclusion (DEI) in venture capital, and to measure and benchmark those data through our biennial VC Human Capital Survey.

The goals of the survey — powered by the National Venture Capital Association, Venture Forward and Deloitte — are to collect demographic data on the VC workforce across all firm types, sizes, stages, sectors and geographies, as well as trends on firm talent management and recruitment practices. We’ve learned that progress can be slow and seem discouraging, but we’ve also captured evidence that diversity (and firm practices to advance diversity) is increasing in some areas, even as other areas have unfortunately not seen the same pace of change.

To begin with, as an industry, venture capital can only improve what we measure.

We fielded the survey in 2016, 2018 and 2020, and released the outcomes of the third edition last month, featuring data (as of June 30, 2020) collected from 378 firms, a marked increase from 203 participating firms in 2018. Furthermore, more than 145 firms signed the #VCHumanCapital pledge to publicly commit to submitting their DEI data.

At a high level, the data showed that improvements in diversity among investment partners have largely been driven by the hiring and advancement of female investors, while there has been little progress in the equitable representation of Black or Hispanic investment partners.

However, the demographic composition of junior investment professionals reflects greater diversity and wider adoption of diversity-focused talent management and recruitment practices suggest some cause for optimism. The industry still has a long way to go, but here are some of the key insights and changes we identified from the latest survey.

More firms are explicitly assigning responsibility for promoting diversity and inclusion internally — 50% of firms have a staff person or team tasked with this responsibility (compared with 34% in 2018 and 16% in 2016). Simultaneously, diversity and inclusion strategies have become more widespread; 43% of firms have implemented a diversity strategy (against 32% in 2018 and 24% in 2016), while 41% have an inclusion strategy (versus 31% in 2018 and 17% in 2016).

This intentionality translates to improved diversity outcomes. Firms with dedicated DEI staff, strategies and programs achieve greater gender and racial diversity on investment teams and among investment partners. The increased emphasis on DEI is also a broader ecosystem trend. More firms report that limited partners and portfolio companies have requested their DEI details over the past 12 months.

Venture firms are relatively small and turnover is generally low, but 21% of firms in 2020 reported their number of senior-level investment positions had increased, while 43% said their number of junior-level positions had expanded. Meanwhile, the demographic composition of junior investment professionals reflects higher gender and racial diversity, a positive leading indicator for the diversity of future investment partners.

As overall DEI strategies have become increasingly widespread, more firms have also developed DEI-focused recruitment and hiring programs — 33% of firms have formal programs, while 74% have informal programs, both reflecting steady increases from 2016. Firms were also more likely to report that they typically seek external candidates for open positions than they did in 2018.

However, firms continue to largely rely on internal networks for recruitment, which often encourages homogeneous hiring outcomes. Between the 2018 and 2020 surveys, there was little change shown in the use of narrow recruitment methods to find external candidates; notifying peers in the VC industry (78%) and notifying the firm internally (59%) were the strategies cited most often. The exception was posting on third-party websites like LinkedIn or in newsletters, a strategy reported by 54% of firms in 2020 (a substantial increase from 37% in 2018), which presents one avenue to reach a broader audience of candidates outside of existing networks.

Once talent has come on board, inclusive culture and retention become key metrics of DEI progress. More firms are implementing programs dedicated to leadership development, mentorship and retention, with about two-thirds reporting informal versions of such programs (20 percentage points higher than in 2016) and 20% of firms reporting formal programs.

Assessing inclusion through the VC Human Capital Survey is challenging because we survey one representative per firm, and one person cannot speak to the degree of inclusion felt by others. However, we added a new question to the 2020 survey to gauge how firms themselves are assessing inclusion. While 41% of firms reported having an inclusion strategy, only 26% said they conduct surveys of their employees to assess inclusion.

Well-structured, consistently applied policies for career advancement are critical to ensuring that diverse talent reaches the most senior decision-making levels of the industry. About 20% of firms reported having formal DEI programs focused on promotion (up from 5% in 2016), while 65% of firms have informal programs (compared with 39% in 2016).

Although DEI programs focused on the promotion of employees are more widespread, subjective factors remain a key consideration for promotion decisions, which can lead to unequal and biased outcomes.

Almost all firms reported that “contributions to the performance of the fund” (90%) and “deal origination” (82%) were very important or important factors in considering promotions. However, the factor most often rated highly was “soft skills,” with 94% of firms saying it was very important or important. These types of subjective factors present significant opportunity for unconscious bias to creep in and can detract from the weight given to objective measures more demonstrably relevant to performance.

The results of the third edition of our survey are timely, coming on the heels of a year in which social justice and racial equity have been the subjects of sharp national focus, policymakers have sought to increase access to capital for underserved communities, and the VC industry has shown a renewed focus on DEI. The survey shows where the VC industry’s efforts should be focused and also serves as an important reminder of the intersectional needs of DEI-focused initiatives.

The data show that progress within one demographic element can be more nuanced when considering people who represent multiple marginalized communities (e.g., the percentage of investment partners who are women has steadily increased, but the percentage of investment partners who are women of color has not).

The pace of DEI progress has been slow and uneven in some areas, but there are reasons for optimism. On April 6, NVCA, Venture Forward and Deloitte hosted a discussion with industry leaders to further examine the latest survey results and to address DEI challenges, opportunities and strategies for the industry. More firms are prioritizing these constructive conversations, both within their firms and publicly with industry peers. More firms are acting in a collaborative spirit, adopting thoughtful and concrete DEI strategies and acting with intentionality and urgency.

If the industry can continue to build upon this momentum and commitment around DEI efforts, we can reach a tipping point that will translate to meaningful progress reflected in future editions of the survey.

Powered by WPeMatico

TechCrunch’s Early Stage 2021 is back for part two of our bootcamp-for-entrepreneurs event, with a focus on marketing and fundraising. Building on the first half of the event in April, this two-day virtual sprint will take place July 8 & 9, and we’re thrilled to welcome Rebecca Reeve Henderson as one of our all-star slate of experts. Rebecca will be joining us to share insight on how to build an effective earned media strategy for your startup, building on her deep expertise developing effective communications programs for some of the top business software companies in the world.

Earned media, aka the kind of exposure you get from a TechCrunch article, is a key element of any startup’s marketing strategy. It’s something that is best used as a complementary component to paid marketing and owned channel promotional efforts, but it’s also one of the trickiest things to get right, especially for first-time founders. Rebecca has worked with companies ranging from Slack, to Shopify, to Zapier, to Canva and many more, helping craft effective earned media strategies in one of the most difficult areas of all: B2B SaaS.

Image Credits: Rsquared Communications

Rebecca is also a founder herself, having built her communications company Rsquared from the ground up into an international business spanning the U.S. and Canada. Rsquared’s clients included startups at all stages of growth, from their very beginnings through to successful exits, including public market debuts, so she’s run effective communications campaigns at every point on the growth spectrum. Then in 2019, Rsquared had its own exit, with an acquisition by global communications firm Archetype.

We’ll hear tips from Rebecca on how earned media contributes to an effective overall communications strategy, and how you go about earning that media — including how to pitch media, and how to build successful long-term relationships with key reporters and publications in your industry.

Tickets for TC Early Stage: Marketing & Fundraising are available until this Friday at the early bird rate which gives you an instant $100 savings! Secure your seat before this weekend!

Powered by WPeMatico

In the never-ending stream of venture capital funding rounds, from time to time, a group of startups working on the same problem will raise money nearly in unison. So it was with OKR-focused startups toward the start of 2020.

How were so many OKR-focused tech upstarts able to raise capital at the same time? And was there really space in the market for so many different startups building software to help other companies manage their goal-setting? OKRs, or “objectives and key results,” a corporate planning method, are no longer a niche concept. But surely, over time, there would be M&A in the group, right?

During our first look into the cohort, we concluded that it felt likely that there was “some consolidation” ahead for the group “when growth becomes more difficult.” At the time, however, it was clear that many founders and investors expected the OKR software market to have material depth.

They were right, and we were wrong. A year later, in early 2021, we asked the same group how their previous year had gone. Nearly every single company had a killer year, with many players growing by well over 100%.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

OKR company Ally.io grew 3.3x in 2020, for example, while its competitor Gtmhub grew by 3x over the same time period. More capital followed. Ally.io raised $50 million in a Series C in the first quarter, while Gtmhub put together a $30 million Series B during the same period.

They won’t be the final startups in the OKR cohort to raise this year. We know this because we reached out to the group again this week, this time probing their Q1 performance, and, critically, asking the startups to discuss their level of optimism regarding the rest of 2021.

As before, the group’s recent results are strong, at least when compared to their own planning. But notably, the collection of competing companies is more optimistic than before about the rest of the year than they were before Q1 2021. Things are heating up for the OKR startup world.

As before, the group’s recent results are strong, at least when compared to their own planning. But notably, the collection of competing companies is more optimistic than before about the rest of the year than they were before Q1 2021. Things are heating up for the OKR startup world.

A takeaway from our work today is that our prior notes about how impressively deep the software market is proving to be may have been too modest. And frankly, that’s super-good news for startups and investors alike. So much for SaaS-fatigue.

In a sense, we should not be surprised that OKR startups are doing well or that the startup software market is so large. You’d imagine that the historic pace of venture capital investment that we’ve seen so far in 2021 in Europe and the United States was based on results, or evidence that there was lots more room for software-focused startups to grow.

Interestingly, while these companies look similar to outsiders, they are each betting on strategies and differentiators that could help them win in their selected portion of the OKR space. Which also means that the sector may not be as crowded as it seems.

Don’t take our word for it. Let’s hear from Gtmhub COO Seth Elliott, Workboard CEO and co-founder Deidre Paknad, Koan CEO and co-founder Matt Tucker, Ally.io CEO and co-founder Vetri Vellore, and Perdoo CEO and founder Henrik-Jan van der Pol about just what the software market looks like to them.

We’ll start with how the startups performed in Q1 2021, dig into how they feel about the rest of the year, and then talk about how differentiation among the cohort could be helping them not step on each other’s toes.

WorkBoard is having a strong start to 2021. Paknad’s company, which raised in both March of 2019 and January of 2020, told The Exchange that it hired 82 people in the first three months of 2021, and that it plans on doing it again in the current quarter. WorkBoard is “investing heavily,” Paknad said via DM, and “made [its] Q1 targets.”

Powered by WPeMatico

Vena, a Canadian company focused on the Corporate Performance Management (CPM) software space, has raised $242 million in Series C funding from Vista Equity Partners.

As part of the financing, Vista Equity is taking a minority stake in the company. The round follows $25 million in financing from CIBC Innovation Banking last September, and brings Vena’s total raised since its 2011 inception to over $363 million.

Vena declined to provide any financial metrics or the valuation at which the new capital was raised, saying only that its “consistent growth and…strong customer retention and satisfaction metrics created real demand” as it considered raising its C round.

The company was originally founded as a B2B provider of planning, budgeting and forecasting software. Over time, it’s evolved into what it describes as a “fully cloud-native, corporate performance management platform” that aims to empower finance, operations and business leaders to “Plan to Grow” their businesses. Its customers hail from a variety of industries, including banking, SaaS, manufacturing, healthcare, insurance and higher education. Among its over 900 customers are the Kansas City Chiefs, Coca-Cola Consolidated, World Vision International and ELF Cosmetics.

Vena CEO Hunter Madeley told TechCrunch the latest raise is “mostly an acceleration story for Vena, rather than charting new paths.”

The company plans to use its new funds to build out and enable its go-to-market efforts as well as invest in its product development roadmap. It’s not really looking to enter new markets, considering it’s seeing what it describes as “tremendous demand” in the markets it currently serves directly and through its partner network.

“While we support customers across the globe, we’ll stay focused on growing our North American, U.K. and European business in the near term,” Madeley said.

Vena says it leverages the “flexibility and familiarity” of an Excel interface within its “secure” Complete Planning platform. That platform, it adds, brings people, processes and systems into a single source solution to help organizations automate and streamline finance-led processes, accelerate complex business processes and “connect the dots between departments and plan with the power of unified data.”

Early backers JMI Equity and Centana Growth Partners will remain active, partnering with Vista “to help support Vena’s continued momentum,” the company said. As part of the raise, Vista Equity Managing Director Kim Eaton and Marc Teillon, senior managing director and co-head of Vista’s Foundation Fund, will join the company’s board.

“The pandemic has emphasized the need for agile financial planning processes as companies respond to quickly-changing market conditions, and Vena is uniquely positioned to help businesses address the challenges required to scale their processes through this pandemic and beyond,” said Eaton in a written statement.

Vena currently has more than 450 employees across the U.S., Canada and the U.K., up from 393 last year at this time.

Powered by WPeMatico

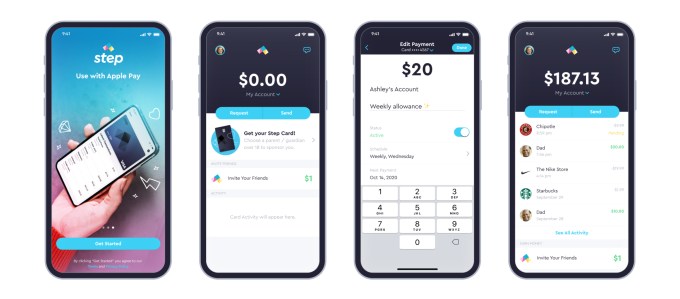

Step, the digital banking service aimed at teens and endorsed by TikTok star Charli D’Amelio, announced this morning the close of a $100 million round of Series C funding after growing to more than 1.5 million users just six months after launch. The new round, led by General Catalyst, comes shortly after Step’s $50 million Series B, announced at the end of last year after the startup hit half a million users in only two months post-launch.

The new round also includes participation from Step’s existing investors, Coatue, Stripe, Charli D’Amelio, The Chainsmokers, Will Smith and Jeffrey Katzenberg, and brings on newcomer Franklin Templeton, signaling a plan to move into investments is on the horizon. It also includes actor and musician Jared Leto. Step is also formally announcing NBA All-Star Stephen Curry as an investor, which had not previously been disclosed, as well as former Square executives Sarah Friar, Jacqueline Reses and Gokul Rajaram.

As a result of the fundraise, Kyle Doherty of General Catalyst is joining Step’s board. To date, Step has raised more than $175 million.

Image Credits: Step

According to CEO CJ MacDonald, Step hasn’t yet spent the money from its Series B, but believes the additional funds can help the startup grow more quickly.

“We’ve signed up more than a million and a half accounts in the first six months. We’re signing up 10,000 accounts-plus a day, and there’s just a lot of things that we want to do to bring this to millions and millions of households to help educate the next generation be smarter with money,” he says. At the time of the Series B, for comparison, Step said it was adding around 7,000 to 10,000 accounts per day.

“Honestly we don’t need the capital,” MacDonald added. “It’s just we think speed to market is really key and we think we can accelerate our growth and invest in infrastructure.”

The company is also planning to hire across operations, engineering, product and design, to double its now 65-person team over the next year.

Step today competes in a crowded market of mobile banking services aimed at a younger demographic, but it’s one of very few that targets teenagers ages 13 to 18. Through Step’s app, teens gain access to an FDIC-insured bank account without fees and a secured Visa card that helps them establish credit before they turn 18. The app also offers Venmo-like functionality for sending money to friends.

Image Credits: Step

Step’s growth so far has benefitted from a combination of factors, including word-of-mouth, use of social media and its popular referral program, which has paid out a few dollars per new sign-up. Step has also leveraged its partnerships with social media influencers like D’Amelio and Josh Richards, as well as celebs like Step investor Justin Timberlake.

The company believes the Curry announcement may also help to raise awareness about the banking app. As a father of three, if Curry talks about introducing Step to his own children, people will take notice.

While the additional funds are focused on driving growth, Step is also thinking about its future as its existing users begin to age up. The company plans to enter into the credit and lending market, as well as introduce investments at some point in the future. The Franklin Templeton investment could be useful here, MacDonald notes.

“Franklin [Templeton is] obviously, one of the largest financial institutions in the world. And, as we start thinking about investments and the journey of the customer, to have a great brand like Franklin Templeton that’s invested in this round — I think it’s just a testament to where they see the world going,” he says.

Step’s fundraise falls on the same day that competitor Current and Greenlight, both which focus on families, also raised new rounds.

Powered by WPeMatico