Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

After their long post-financial-crisis slump, European tech IPOs are starting to rebound. Tech companies raised more money on European public markets between 2015-17 (€5.3 billion) than in the previous seven years combined. With venture capital having boomed in that time, that trend is set to continue: There is a generation of well-funded, fast-growing technology companies now eyeing the public markets as the platform for continued rapid growth. The pipeline is healthy. But what needs to be done to get ready for an IPO and, crucially, what comes next?

Money raised and market opportunity alone do not make for a public-company-in-waiting. You do not transform from a scrappy growth business into a tightly governed, transparent public company overnight. It has to be a gradual evolution, one which requires the right people, structures and mindset to be in place. Companies need to ask themselves not just if they want to pursue an IPO, but how exactly they plan to go about it, and how they will prepare for the realities of life as a public company.

Having advised three companies on their journey to an IPO, across three different geographies, I think there should be at least two years of careful planning between deciding to seek a listing and hearing the bell ring on your market open.

You have to start with bringing in the right people. A business can grow a long way on the back of an inspirational founding team, but as an aspiring public company, you need an experienced and high-performing management team as well. Do you have a CFO who has credibility with public market investors? Does the board have enough members with independent authority; will it meet the requirements of those institutional investors who now require a minimum quota of female directors?

Ultimately it comes down to one question: Can you start operating like a public company before you become one?

Your board will have to grow, not least to fulfill necessary governance functions, from audit to compensation and nomination committees. These are important and often complex hires, which can take anything from six months to a year to put in place. It also takes a while for new board members to start working well together and gain a detailed understanding of the company.

The composition of the board is just one area where a private company has to start asking itself new questions as it prepares for a listing. Another is the financial profile of the business and the trade-off between growth and profitability. Will investors give us credit for growing, say, 80 percent year over year? Should we front-load investments and associated losses, or incur them over time when required? The CEO also must think about how she is going to communicate with the market, and whether she needs others around her to give investors the full package. A very visionary and product-focused CEO, for example, will need to be complemented by a brilliant CFO who can handle detailed questions about the company’s finances.

A company thinking about going public also needs to evolve its mindset. After an IPO, you will no longer be a tight-knit group of founders, early hires and investors who know the business intimately. The relationship you have known with your private backers is going to bear no relation to the one you will experience with public market investors. As a public company, you are no longer being supportively cheered on, but independently scrutinized by investors who understand the business in less detail and are liable to react strongly to indicators whose significance they can easily misinterpret. In this environment, if you set an ambitious target, you can’t achieve only 95 percent of it and expect to be consoled and encouraged. Institutional investors are going to want to know why you didn’t exceed that target, let alone failed to meet it.

Ultimately it comes down to one question: Can you start operating like a public company before you become one? The companies that succeed post-IPO are those that have laid the foundation to make the transition from private to public as seamless as possible. There are rich rewards to be enjoyed on the public markets, but only for those who do the hard work in advance to ease into life as a public company. Europe’s fast-growing tech companies should consider not just whether an IPO is the right option for them, but if they are willing to put in the work that is necessary to make it a success.

Powered by WPeMatico

This is a must-read for understanding the tech industry. We’ve distilled famous investor Mary Meeker’s annual Internet Trends report down from its massive 294 slides of stats and charts to just the most important insights. Click or scroll through to learn what’s up with internet growth, screen addiction, e-commerce, Amazon versus Alibaba, tech investment and artificial intelligence.

Powered by WPeMatico

If you’ve ever been in a pointless meeting at work, odds are you’ve spent part of the time responding to messages or just putzing around on the Internet — but Klaxoon hopes to convert that into something a bit more productive with more interactive meetings.

The French startup today said it’s raised $50 million in a new financing round led by Idinvest Partners, with early round investors BPI, Sofiouest, Arkea and White Star Capital Fund also participating. The company offers a suite of tools designed to make those meetings more engaging and generally just cut down on useless meetings with a room of bored and generally unengaged people that might be better off working away at their desk or even taking other meetings. The company has raised about $55.6 million in total.

The whole point of Klaxoon is to make meetings more engaging, and there are a couple ways to do that. The obvious point is to translate what some classrooms are doing in the form of making the whole session more engaging with the use of connected devices. You might actually remember those annoying clickers in classrooms used to answer multiple choice questions throughout a session, but it is at least one way to engage people in a room — and offering a more robust way of doing that may be something that helps making the session as a whole more productive.

Klaxoon also offers other tools like an interactive whiteboard (remember Smartboards, also in classrooms?) as well as a closed networks for meeting participants that aims to be air-gapped from a broader network so those employees can conduct a meeting in private or if the room isn’t available. All this is wrapped together with a set of analytics to help employees — or managers — better conduct meetings and generally be more productive. All this is going to be more important going forward as workplaces become more distributed, and it may be tempting to just have a virtual meeting on one screen while either working on a different one — or just messing around on the Internet.

Of course, lame meetings are a known issue — especially within larger companies. So there are multiple interpretations of ways to try to fix that problem, including Worklytics — a company that came out of Y Combinator earlier this year — that are trying to make teams more efficient in general. The idea is that if you are able to reduce the time spent in meetings that aren’t really productive, that’ll increase the output of a team in general. The goal is not to monitor teams closely, but just find ways to encourage them to spend their time more wisely. Creating a better set of productivity tools inside those meetings is one approach, and one Klaxoon seems to hope plays out.

Powered by WPeMatico

Pinterest is continuing its push into video as a potential avenue for advertisers by today saying that it will offer advertisers a promoted video tool that takes up the width of the entire screen.

While Pinterest normally offers users a grid that they can flip through — compressing a lot of content into a small space — taking up the full width of the screen with a promoted video would offer advertisers considerable real estate if they’re looking to get the attention of users. Pinterest pitches itself to advertisers as a strong alternative to Facebook or Google, giving marketers a way to reach an audience that behaves a little more differently than when on those other platforms and coming to Pinterest to discover new things.

The company also said it’s hired Tina Pukonen as an entertainment strategist and Mike Chuthakieo as an industry sales lead. Pinterest says more than 42 million people in the U.S. come to Pinterest for entertainment ideas, and that potential tool offers an interesting niche opportunity for advertisers to capture the attention of a user for a product — say, a movie — that needs a lot of awareness marketing. Getting a user’s attention for just a few seconds can be more than enough time to at least plant the seed of potentially buying a product down the line.

It’s that argument that what gives Pinterest potential value for advertisers. The company offers an array of advertising products designed to target users at all phases of a potential buying cycle, whether that’s just clicking around on the platform looking for ideas down to actually saving an idea or buying it — through Pinterest or through a referral. Most of Pinterest’s content consists of images and other content from brands or businesses. That makes sense given that it’s a place where people tend to go to plan life events, whether that’s parties, or weddings, or home improvement — and those events center around products that they may in theory one day buy. All the while Pinterest is accumulating a lot of different plays at advertising products and an experienced level of senior hires, including hiring its first COO Françoise Brougher, who was the former VP of SMB global sales and operations at Google and business lead at Square.

Pinterest, interestingly, seems to have been a little more tolerant of making what might seem like small design changes but may have substantial user implications. The company added a tab for followers at the bottom of the app, shaking up what is often seen as a core navigation bar for any app. But the company continues to grow, crossing 200 million monthly active users in September last year.

Powered by WPeMatico

The Europas Unconference & Awards is back on 3 July in London and we’re excited to announce more speakers and panel sessions as the event takes shape. Crypto and Blockchain will be a major theme this year, and we’re bringing together many of the key players. TechCrunch is once again the key media partner, and if you attend The Europas you’ll be first in the queue to get offers for TC events and Disrupt in Europe later in the year.

You can also potentially get your ticket for free just by sharing your own ticket link with friends and followers. See below for the details and instructions.

To recap, we’re jumping straight into our popular breakout sessions where you’ll get up close and personal with some of Europe’s leading investors, founders and thought leaders.

The Unconference is focused into zones including AI, Fintech, Mobility, Startups, Society, and Enterprise and Crypto / Blockchain.

Our Crypto HQ will feature two tracks of panels, one focused on investing and the other on how blockchain is disrupting everything from financial services, to gaming, to social impact to art.

We’ve lined up some of the leading blockchain VCs to talk about what trends and projects excite them most, including Outlier Ventures’ Jamie Burke, KR1’s George McDonaugh, blockchain angel Nancy Fenchay, Fabric Ventures’ Richard Muirhead and Michael Jackson of Mangrove Capital Partners.

Thinking of an ICO vs crowdfunding? Join Michael Jackson on how ICOs are disrupting venture capital and Ali Ganjavian, co-founder of Studio Banana, the creators of longtime Kickstarter darling OstrichPillow to understand the ins and outs of both.

We’ve also lined up a panel to discuss the process of an ICO – what do you need to consider, the highs, the lows, the timing and the importance of community. Linda Wang, founder and CEO of Lending Block, which recently raised $10 million in an April ICO, joins us.

We are thrilled to announce that Civil, the decentralised marketplace for sustainable journalism, will be joining to talk about the rise of fake news and Verisart’s Robert Norton will share his views on stamping out fraud in the art world with blockchain. Min Teo of ConsenSys will discuss blockchain and social impact and Jeremy Millar, head of Consensys UK, will speak on Smart Contracts.

Our Pathfounders Startup Zone is focused purely on startups. Our popular Meet the Press panel is back where some of tech’s finest reporters will tell you what makes a great tech story, and how to pitch (and NOT pitch them). For a start, TechCrunch’s Steve O’Hear and Quartz’s Joon Ian Wong are joining.

You’ll also hear from angels and investors including Seedcamp’s Carlos Eduardo Espinal; Eileen Burbidge of Passion Capital; Accel Partners’ Andrei Brasoveanu; Jeremy Yap; Candice Lo of Blossom Capital; Scott Sage of Crane Venture Partners; Tugce Ergul of Angel Labs; Stéphanie Hospital of OneRagtime; Connect Ventures’ Sitar Teli and Jason Ball of Qualcomm Ventures.

Sound great? You can grab your ticket here.

All you need to do is share your personal ticket link. Your friends get 15% off, and you get 15% off again when they buy.

The more your friends buy, the more your ticket cost goes down, all the way to free!

The Public Voting in the awards ends 11 June 2018 11:59: https://theeuropas.polldaddy.com/s/theeuropas2018

We’re still looking for sponsor partners to support these editorially curated panels.

Please get in touch with Petra@theeuropas.com for more details.

SPEAKERS SO FAR:

Jamie Burke, Outlier Ventures

Jeremy Millar, ConsenSys

Linda Wang, Lending Block

Robert Norton, Verisart

George McDonaugh, KR1

Eileen Burbidge, Passion Capital

Carlos Eduardo Espinal, Seedcamp

Sitar Teli, Connect Ventures

Michael Jackson, Mangrove Capital Partners

Min Teo, ConsenSys

Steve O’Hear, TechCrunch

Joon Ian Wong, Quartz

Richard Muirhead, Fabric Ventures

Nancy Fechnay, Blockchain Technologist + Angel

Candice Lo, Blossom Capital

Scott Sage, Crane Venture Partners

Andrei Brasoveanu, Accel

Tina Baker, Jag Shaw Baker

Jeremy Yap

Candice Lo, Blossom Capital

Tugce Ergul, Angel Labs

Stéphanie Hospital, OneRagtime

Jason Ball, Qualcomm Ventures

The Europas Awards

The Europas Awards are based on voting by expert judges and the industry itself. But key to the daytime is all the speakers and invited guests. There’s no “off-limits speaker room” at The Europas, so attendees can mingle easily with VIPs and speakers.

Public Voting is still humming along. Please remember to vote for your favourite startups!

Awards by category:

Hottest Media/Entertainment Startup

Hottest E-commerce/Retail Startup

Hottest Marketing/AdTech Startup

Hottest Enterprise, SaaS or B2B Startup

Hottest Platform Economy / Marketplace

Hottest Cyber Security Startup

Hottest Internet of Things Startup

Fastest Rising Startup Of The Year

Hottest GreenTech Startup of The Year

Best Angel/Seed Investor of the Year

Hottest VC Investor of the Year

Hottest Blockchain/Crypto Startup Founder(s)

Hottest Blockchain Protocol Project

Hottest Corporate Blockchain Project

Hottest Blockchain ICO (Europe)

Hottest Financial Crypto Project

Hottest Blockchain for Good Project

Hottest Blockchain Identity Project

Hall Of Fame Award – Awarded to a long-term player in Europe

The Europas Grand Prix Award (to be decided from winners)

The Awards celebrates the most forward thinking and innovative tech & blockchain startups across over some 30+ categories.

Startups can apply for an award or be nominated by anyone, including our judges. It is free to enter or be nominated.

Instead of thousands and thousands of people, think of a great summer event with 1,000 of the most interesting and useful people in the industry, including key investors and leading entrepreneurs.

• No secret VIP rooms, which means you get to interact with the Speakers

• Key Founders and investors speaking; featured attendees invited to just network

• Expert speeches, discussions, and Q&A directly from the main stage

• Intimate “breakout” sessions with key players on vertical topics

• The opportunity to meet almost everyone in those small groups, super-charging your networking

• Journalists from major tech titles, newspapers and business broadcasters

• A parallel Founders-only track geared towards fund-raising and hyper-networking

• A stunning awards dinner and party which honors both the hottest startups and the leading lights in the European startup scene

• All on one day to maximise your time in London. And it’s sunny (probably)!

That’s just the beginning. There’s more to come…

Powered by WPeMatico

Coffee Meets Bagel scored a $12 million Series B this week. The round, led by U.K. VC firm Atami Capital, brings the popular dating app’s total up to just under $20 million since launching back in 2012.

The San Francisco-based dating app has worked to distinguish itself from competitors like Bumble and Tinder by limiting the number of matches it offers during a 24-hour window. Late last year, it expanded its offering with a video feature, to add an extra dimension to profiles. This month, it introduced additional CMB Experiences to bring users together in the real world.

Of course, Coffee Meets Bagel is battling a juggernaut in the form of the billion-dollar Match Group, which currently owns OkCupid, Tinder, PlentyofFish and Match, among others. According to the company, this latest round will drive investments into more CMB Experiences along with international expansion for the service, along with other “product innovation.”

Co-CEO Arum Kang also notes that the Series B brings a number of VC firms with “prominent female investors,” including Gingerbread Capital. “We’re excited for the next phase of Coffee Meets Bagel, and are pleased to have some wonderful international and female investors on board,” Kang says in a release tied to the news. “Given our focus on female experience, it was very important that we have a female perspective at the investor level.”

Powered by WPeMatico

Airbnb brings in billions of dollars of revenue annually and is profitable on an EBITDA basis, so many wonder if and when the home-sharing company will go public. At the Code Conference today, Airbnb CEO Brian Chesky said the company will “be ready to IPO next year, but I don’t know if we will.”

He added that he wants to make sure it’s a major benefit to the company when Airbnb does go public. Following some more probing, Chesky said he has “no issues with [going public] at all. It could happen.”

Meanwhile, Airbnb has been struggling from a regulatory standpoint since at least 2010. Specifically, San Francisco and New York are two of the most difficult cities from a regulatory standpoint, Chesky said.

In New York, for example, there has been a standstill since 2010. At this point, Chesky said he expects it to take a few more years to overcome the challenge in New York.

“It doesn’t seem like the end is in sight with that challenge,” Chesky said. That challenge, Chesky said, involves the hotel industry and unions that “have galvanized people in these perpetual battles.”

Another general critique of Airbnb is its effect on rising rent costs and displacement. Chesky added that if it was simply a business decision, “it probably wouldn’t be worth it to stay there” in New York. But Chesky said there are hosts who have come to rely on Airbnb to earn income.

At Code, Chesky also touted Airbnb’s experiences product and how it’s growing 10x faster than its homes product. Airbnb Experiences sees 1.5 million bookings a year, Chesky said. Experiences, which Airbnb started testing in 2014 and officially launched in 2016, is Airbnb’s product that helps travelers find things to do in cities throughout the world.

When it first launched, Airbnb didn’t verify the experiences, but after some bad experiences, Airbnb has started verifying them.

“They’re doing incredibly well,” Chesky said. He added that the “experience economy” is growing and “there will probably be a massive economy around experiences.”

Powered by WPeMatico

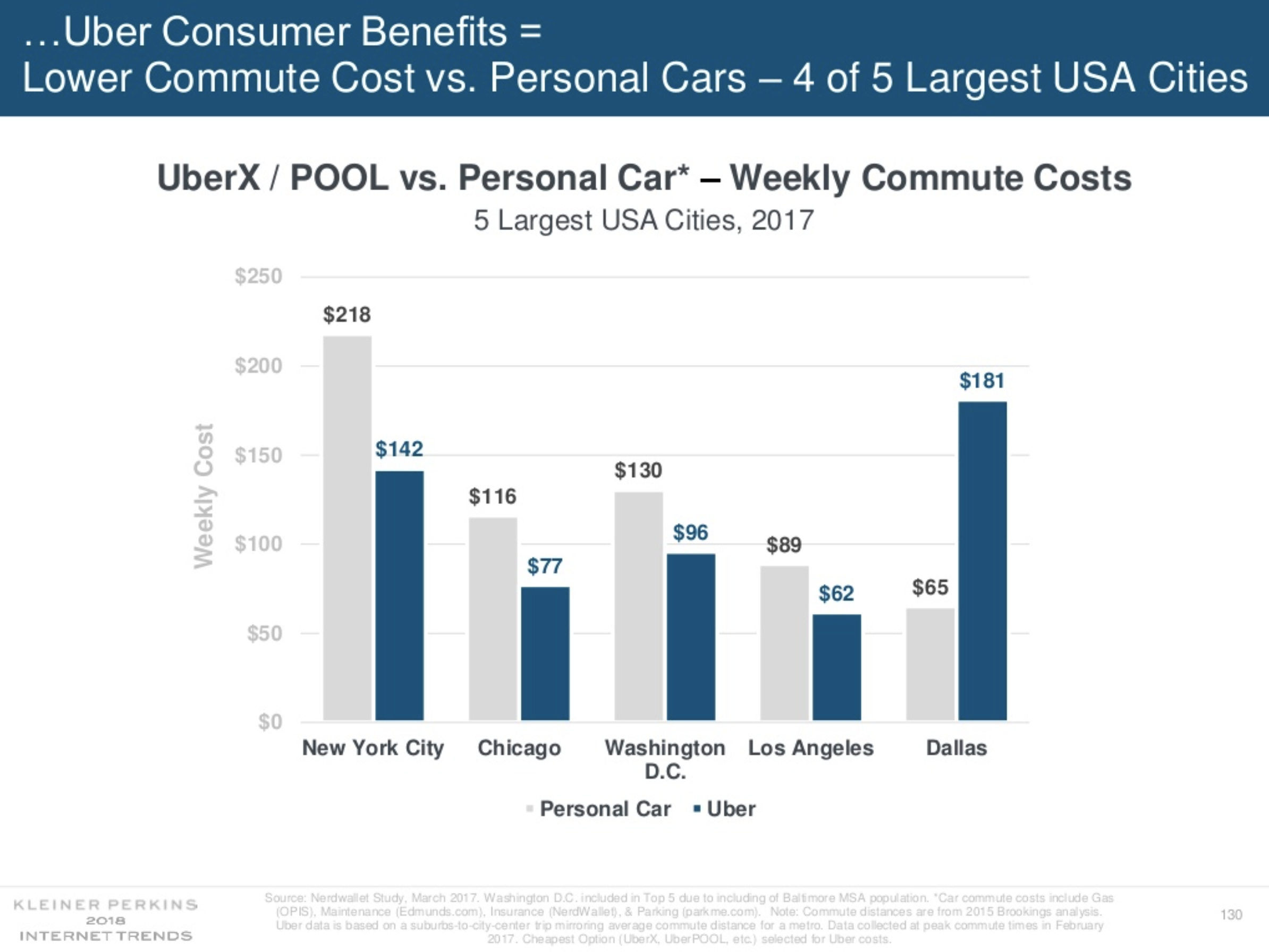

Ride-sharing companies have long touted the cost benefits of their platforms. Well, depending on the city, it can be cheaper on a weekly basis to take an UberX or UberPOOL than it is to own a personal car, according to Kleiner Perkins Caufield Byers partner Mary Meeker’s 2018 annual internet trends report.

In four of the five largest cities in the U.S., it is indeed cheaper to rely on Uber than it is to own a car. Meeker’s analysis took into account cost of gas, car insurance, maintenance and parking.

So, if you live in New York City, Chicago, Washington, D.C. or Los Angeles, it’s cheaper to take an Uber. But that’s not the case in Dallas, where the average weekly cost of car ownership is $65 compared to the average weekly Uber cost of $181.

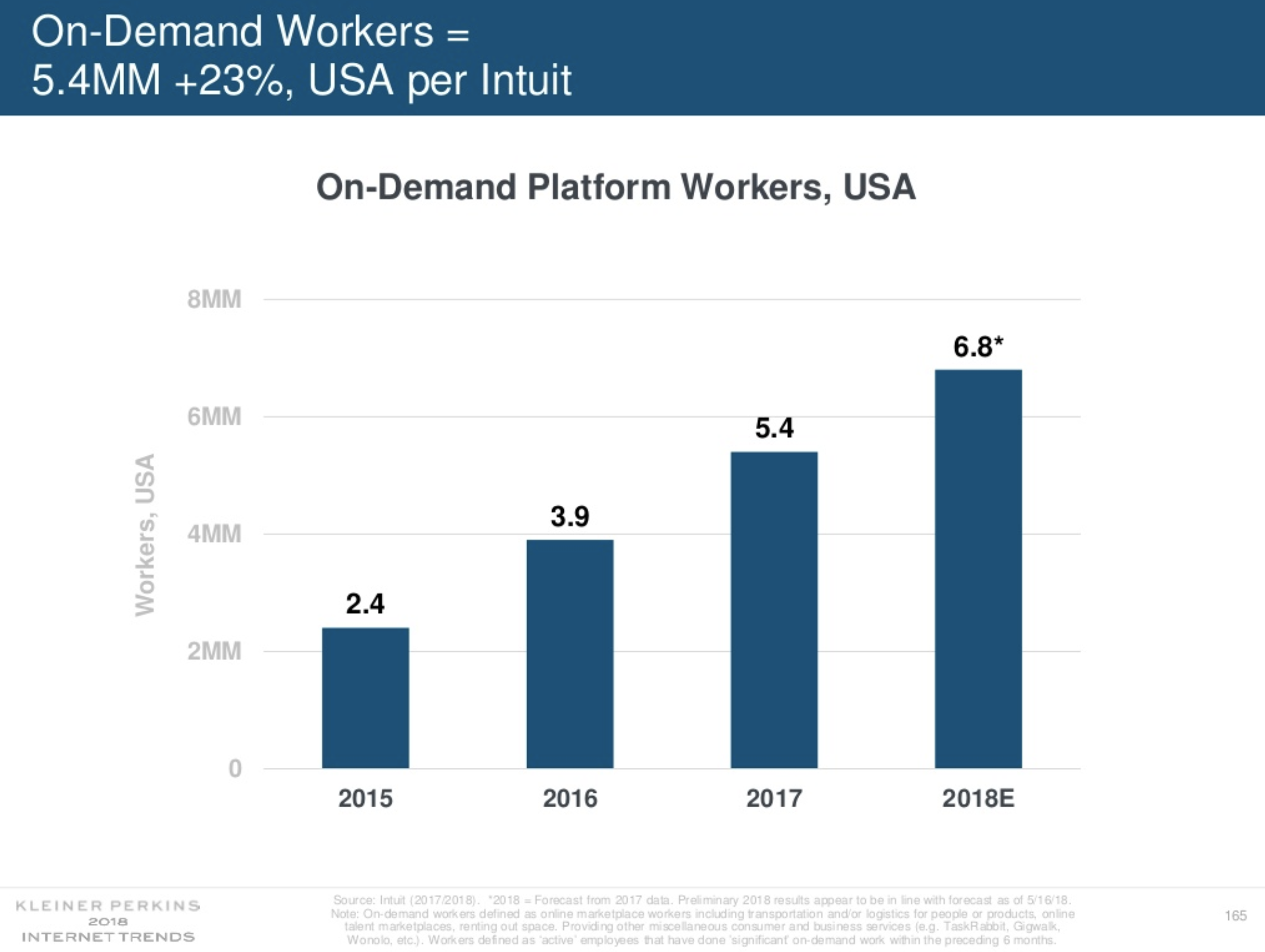

Meeker’s report also looked at the rise of on-demand workers in the U.S. Last year, there were 5.4 million on-demand workers in the country. This year, there are an estimated 6.8 million people working in the on-demand economy.

“These are big numbers,” Meeker said onstage, noting how these types of jobs are helping to supplement income for people, provide greater flexibility and improve work-life balance.

You can check out the full deck below.

Powered by WPeMatico

Want to understand all the most important tech stats and trends? Legendary venture capitalist Mary Meeker has just released the 2018 version of her famous Internet Trends report. It covers everything from mobile to commerce to the competition between tech giants. Check out the full report below, and we’ll add some highlights soon. Then come back for our slide-by-slide analysis of the most important parts of the 294 page report.

Mary Meeker, analyst with Morgan Stanley, speaks during the Web 2.0 Summit in San Francisco, California, U.S., on Tuesday, Nov. 16, 2010. This year’s conference, which runs through Nov. 17, is titled “Points of Control: The Battle for the Network Economy.” Photographer: Tony Avelar/Bloomberg via Getty Images

Powered by WPeMatico

Snapchat is secretly planning the launch of its first full-fledged developer platform, currently called Snapkit. The platform’s prototypes indicate it will let other apps offer a “login with Snapchat” options, use the Bitmoji avatars it acquired and host a version of Snap’s full-featured camera software that can share back to Snapchat. Multiple sources confirm Snap Inc. is currently in talks with several app developers to integrate Snapkit.

The platform could breathe new life into plateauing Snapchat by colonizing the mobile app ecosystem with its login buttons and content. Facebook used a similar strategy to become a ubiquitous utility with tentacles touching everyone’s business. But teens, long skeptical of Facebook and unsettled by the recent Cambridge Analytica scandal, could look to Snapchat for a privacy-safe way to log in to other apps without creating a new username and password.

Snap Inc. declined to comment on this story.

Snapchat is making a big course correction in its strategy here after years of rejecting outside developers. In 2014, unofficial apps that let you surreptitiously save Snaps but required your Snapchat credentials caused data breaches, leading the company to reiterate its ban on using them. It also shut off sharing from a popular third-party music video sharing app called Mindie. In fact, Snap’s terms of service still say “You will not use or develop any third-party applications that interact with the Services or other users’ content or information without our written consent.”

A year ago I wrote that “Snap’s anti-developer attitude is an augmented liability” since it would be tough to populate the physical world with AR experiences unless it has help like Facebook had started recruiting. By December, Snapchat had launched Lens Studio, which lets brands and developers build limited AR content for the app. And it’s been building out its cadre of marketing and analytics partners with which brands can work.

Yet until now, Snapchat hadn’t created functionality that developers could use in their own apps. Snapkit will change that. We don’t know when it will be announced or launched, or who will be the initial developers who take advantage of it. But with Snapchat slipping to its lowest user growth rate ever after being pummeled by competition from Facebook and Instagram, the company needs more than a puppy face filter to regain the spotlight.

According to sources familiar with Snap’s discussions with potential developers, Snapkit’s login with Snapchat feature is designed to let users sign up for new apps with their Snapchat credentials instead of creating new ones. Because Snap doesn’t collect much personal info about you, unlike Facebook, there’s less data to worry about accidentally giving to developers or them misusing. Displaying its branded button on various app’s signup pages could lure in new Snapchat users or reengage lapsed ones. It’s also the key to developing tighter ties between Snap and other apps, even if users sign up for apps another way.

According to sources familiar with Snap’s discussions with potential developers, Snapkit’s login with Snapchat feature is designed to let users sign up for new apps with their Snapchat credentials instead of creating new ones. Because Snap doesn’t collect much personal info about you, unlike Facebook, there’s less data to worry about accidentally giving to developers or them misusing. Displaying its branded button on various app’s signup pages could lure in new Snapchat users or reengage lapsed ones. It’s also the key to developing tighter ties between Snap and other apps, even if users sign up for apps another way.

One benefit of another app knowing who you are on Snapchat, which the company plans to provide with Snapkit, is the ability to bring your Bitmoji avatar with you. Snapchat acquired Bitmoji’s parent company Bitstrips for just $64.2 million in 2016, but the cartoonish personalized avatar app has been a staple of the top 10 chart since. It remains one of Snapchat’s most differentiated offerings, as Facebook has only recently begun work on its clone called Facebook Avatars.

While Bitmoji has offered a keyboard full of your avatar in different scenes, Snapkit could make it easy to add yours as stickers on photos or in other ways in third-party apps. Seeing them across the mobile universe could inspire more users to create their own Bitmoji lookalike.

Snapchat is also working on a way for developers to integrate its editing tool-laden and AR-equipped camera into their own apps. Instead of having to reinvent the wheel if they want to permit visual sharing and inevitably building a poor knockoff, apps could just add Snapchat’s polished camera. The idea is the photos and videos shot with the camera could then be used in that app as well as shared back to Snapchat. Similar to Facebook and Instagram Stories opening up to posts from third-parties, this could inject fresh forms of content into Snapchat at a time when usage is slipping.

Launching a platform also means Snapchat will take on new risks, as third-parties with access to user data could be breached. Snap also will have to convince developers that making it easier for its 191 million daily users to join their apps is worth the engineering resources, given how that community is dwarfed by the multi-billion user Google and Facebook login systems. Login with Snapchat could be especially popular with teen-focused anonymous, or dating, apps you don’t want connected to your Facebook profile.

Snapchat has struggled to get out of Facebook’s shadow despite inventing or acquiring what would become some of the hottest trends in social. Yet Snap Inc. could develop alliances with a platform that leverages its differentiators — a teen audience that doesn’t care for Facebook, inherent privacy and custom avatars. Through an army of developers, Snapchat might find the firepower to challenge the blue empire.

For more on Snapchat and its competitors, check out our other coverage:

Powered by WPeMatico