Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this week, we kicked off our Extra Crunch Live series with an interesting chat with Cowboy’s Aileen Lee and Ted Wang. Today, we will be back at 3 p.m. PST/6 p.m. EST/10 p.m. GMT with a new guest: Charles Hudson, the general partner of Precursor Ventures.

Extra Crunch members will find an AddEvent link below to drop the details directly into their calendar and folks who want to participate directly can hit up the Zoom link (also below). We’ll ask as many audience questions as we can, so please make them sharp — no pitches, please.

Charles Hudson founded Precursor Ventures to invest in pre-seed and seed-stage companies. Earlier this year, the firm filed paperwork to put together a $40 million third fund after previously raising two main funds and one $10 million “opportunity” fund.

As we await hard and accurate numbers on how COVID-19 is impacting fundraising, we’ll ask Hudson to walk us through the changes he has seen and will cover some basics: The best way to pitch him, what his to-do list looks like these days and if the pandemic has made Precursor newly bullish or bearish on certain sectors.

Then, we’ll get much nerdier: Will we see the number of party rounds fall further now that it’s harder to gather investors in real life? Do you think we’ll see pre-seed raises ask for more ownership terms? And what is the latest with the wacky world of early-stage valuations?

There’s a lot to talk about. And we haven’t even mentioned YC’s pro rata change yet.

After Hudson, we have a stacked lineup of Extra Crunch live guests, including Mitch and Freada Kapor, Mark Cuban, Roelof Botha and Kirsten Green, with more to be announced soon.

You can find information below with details for joining today’s discussion, as well as an AddEvent link to put the details directly onto your calendar.

Sign up for Extra Crunch to get access to all these episodes where you can view the talks live, participate in the Q&A with industry leaders and watch later on-demand if you can’t make the live timing. You can also see the chat via YouTube below. Talk soon!

Powered by WPeMatico

Real-time voice transcription service Otter.ai is adding new functionality that will aid home school students and work-from-home employees alike. The company today is introducing an integration with Zoom in order to provide “Live Video Meeting Notes” — meaning, the ability to record and view a live, interactive transcript directly from a video conference.

The feature is also designed to work even if the meeting participant is using a headset or earbuds, the company says.

To access the Live Video Meeting Notes, meeting participants can open the Otter.ai Live Transcript from the LIVE menu at the top of the Zoom window, then log into Otter.ai. However, they won’t need to remember to start or stop the live transcript — that happens automatically. The Otter live transcripts will also be available through the Zoom app on mobile.

When the meeting wraps, users can also refer back to the transcript to highlight, comment and add photos to their meeting notes.

The feature is available for Otter for Teams and Zoom Pro subscribers or higher. The meeting host will need to have an Otter for Teams subscription, which is $20 per seat per month, with a minimum of 3 seats, based on the annual plan. Interested customers can trial the service for free for 2 months using the code “OTTER_RELIEF.”

The ability to access a transcription of the online meeting comes at a time when all business that can be managed virtually by home workers has been moved out of the office, amid the coronavirus pandemic. This, in turn, has seen the use of video conferencing apps skyrocket.

Otter.ai, too, has felt the effects of the COVID-19 pandemic on its business.

According to Otter.ai CEO and founder Sam Liang, Otter usage with Zoom meetings has increased by more than 5X in the past few weeks and the company has seen more sign-ups from remote workers and students engaged in distance learning.

Besides being a useful tool for those attending web conferencing meetings, Otter’s transcripts can help people catch up with meetings they missed — a more common occurrence these days, as workers juggle their jobs, health, parenting, and home school teaching duties simultaneously.

To date, Otter has transcribed more than 25 million meetings, totaling over 750 million transcribed meeting minutes. While the company doesn’t disclose its user numbers or revenue, Liang told TechCrunch Otter.ai’s annual revenue run rate has doubled in less than four months since the end of 2019. The company is not yet profitable, but features like this new Zoom integration may help to push free users to paid plans.

“Virtual meetings have skyrocketed during the COVID-19 outbreak as organizations recognize that high quality voice meeting notes are a critical tool for employee productivity when collaborating within an office or in any virtual meeting,” said Liang, in a statement about the new integration.

The launch comes on the heels of Otter.ai’s existing partnership with Zoom, which allowed the video conferencing solution to license Otter’s voice transcription technology to offer post-meeting transcription. These transcriptions, however, would only be available an hour or two after the meeting wrapped, without any way to view the transcript being written live, in-real time, as today’s new integration allows. It also didn’t offer any way to interact with the transcript, such as highlighting or leaving comments.

In addition, the post-meeting transcription service was only aimed at Zoom Business users, while the new features are offered to Zoom Pro users.

Otter.ai says the new Zoom feature set is only one of several video conferencing integrations it has in the works, but didn’t provide details on what other services may be supported in the future.

The startup earlier this year raised another $10 million in funding from new strategic investor NTT DOCOMO. To date, Otter.ai has raised $23 million from Fusion Fund, GGV Capital, Draper Dragon Fund, Duke University Innovation Fund, Harris Barton Asset Management, Slow Ventures, Horizons Ventures and others.

Correction, 4/23/20, 3:16 PM: Otter has transcribed over 750M minutes, not 250M as previously stated. The article has been updated to correct this.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

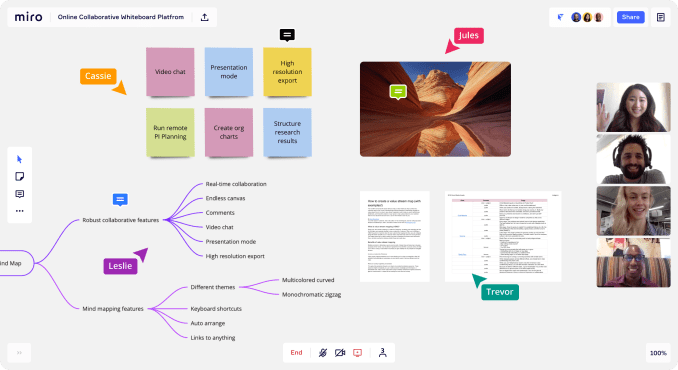

Miro is a company in the right place at the right time. The makers of a digital whiteboard are seeing usage surge right now as businesses move from the workplace and physical whiteboards. Today, the company announced a hefty $50 million Series B.

Iconiq Capital led the round with help from Accel and a slew of individual investors. Today’s investment brings the total raised to around $75 million, according to the company. Among the company’s angel investors was basketball star Steph Curry.

What’s attracting this level of investment is that this is a product made for a moment when workers are forced to stay home. One of the primary complaints about working at home is the inability to sit in the same room with colleagues and brainstorm around a whiteboard. This reproduces that to an extent.

What’s more, Miro isn’t simply light-weight add-in like you might find built into a collaboration tool like Zoom or Microsoft Teams; it’s more of a platform play designed to integrate with many different enterprise tools, much like Slack does for communications.

Miro co-founder and CEO Andrey Khusid said the company planned the platform idea from its earliest days. “The concept from day one was building something for real-time collaboration and the platform thing is very important because we expect that people will build on top of our product,” Khusid told TechCrunch.

Image Credit: Miro

That means that people can build integrations to other common tools and customize the base tool to meet the needs of an individual team or organization. It’s an approach that seems to be working as the company reports it’s profitable with more than 21,000 customers including 80% of the Fortune 100. Customers include Netflix, Salesforce, PwC, Spotify, Expedia and Deloitte.

Khusid says usage has been skyrocketing among both business and educational customers as the pandemic has forced millions of people to work at home. He says that has been a challenge for his engineering team to keep up with the demand, but one that the company has been able to meet to this point.

The startup just passed the 300 employee mark this week, and it will continue to hire with this new influx of money. Khusid expects to have another 150 employees before the end of the year to keep up with increasing demand for the product.

“We understand that we need to come out strong from this situation. The company is growing much faster than we expected, so we need to have a very strong team to maintain the growth at the same pace after the crisis ends.”

Powered by WPeMatico

While some U.S. investors might have taken comfort from China’s rebound, we still find ourselves in the early innings of this period of uncertainty.

Some epidemiologists have estimated that COVID-19 cases will peak in April, but PitchBook reports that dealmaking was down -26% in March, compared to February’s weekly average. The decline is likely to continue in coming weeks — many of the deals that closed last month were initiated before the pandemic, and there is a lag between when deals are made and when they are announced.

However, there’s still hope. A recent report concluded that because valuations are lower and there’s less competition for deals, “the best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery.” There are countless examples from the 2008 recession, including many highly valued VC-backed businesses such as WhatsApp, Venmo, Groupon, Uber, Slack and Square. Other early-stage VCs seem to have arrived at a similar conclusion.

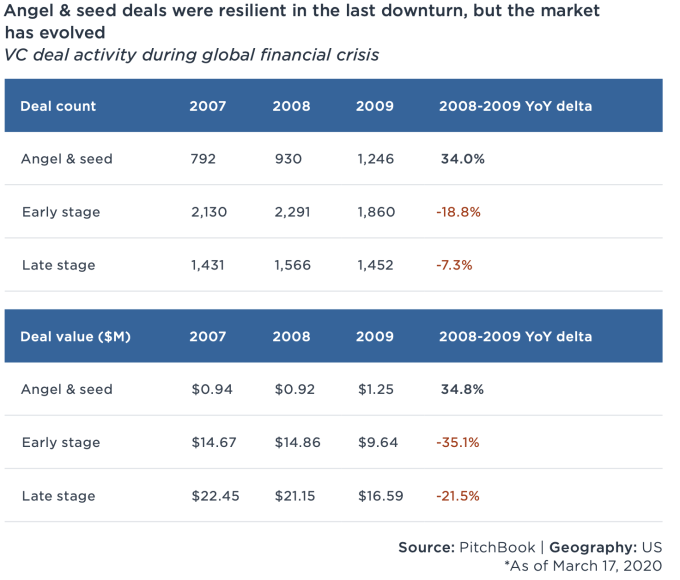

Also, early-stage investing seems more resilient. During the last recession, angel and seed activity increased 34% as interest in the stage boomed during a period of prolonged growth.

Image Credits: PitchBook (opens in a new window)

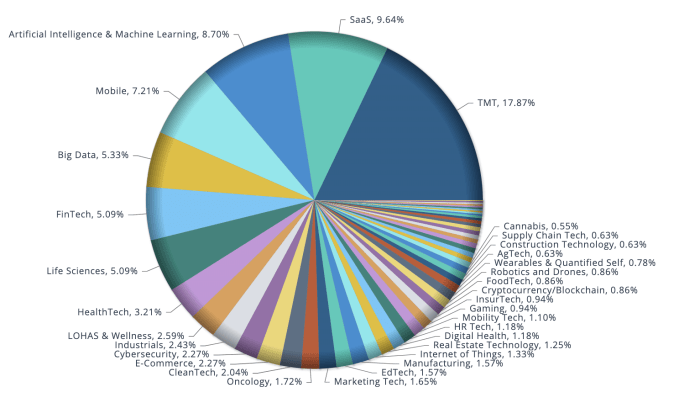

Furthermore, there is still capital to be deployed in categories that interested investors before the pandemic, which may set the new order in a post-COVID-19 world. According to data provider Preqin Ltd., VC dry powder rose for a seventh consecutive year to roughly $276 billion in 2019, and another $21 billion were raised last quarter. And looking at the deals on the early-stage side that were made year to date, especially in March, the vertical categories that garnered the most funding were enterprise SaaS, fintech, life sciences, healthcare IT, edtech and cybersecurity.

Image Credits: PitchBook

That said, if VCs have the capital to deploy and are able to overcome the obstacle of “having never met in person,” here are six investment trends that could emerge when the pandemic is over.

Powered by WPeMatico

Since first uploading a YouTube teaser video of its tech five years ago, Magic Leap’s presence in the augmented reality industry has been controversial.

Some have lauded the team’s ambitions, while others I’ve talked to say the company’s posturing has dissuaded investors from taking chances on other AR hardware startups, which has hampered the industry’s advance.

Regardless of its impact, Magic Leap carries outsized weight, leading one to question what would happen to other AR companies if the company’s situation worsened.

The company announced layoffs today, with reports indicating that it is dismissing around 1,000 employees — about half of the company. Magic Leap’s added news of a major pivot to enterprise makes it seem like that wasn’t its primary strategy over the past year. From my perspective, the company looks like it is on a path to a fire sale and will be dependent on executing a dramatic turnaround, which grows tougher under current economic conditions.

Magic Leap has few users, so a theoretical shutdown would likely have a lesser impact than other unicorn flare-outs; still, losing a company on the forefront of a technology lauded by many as the next ubiquitous platform will certainly impact others that are striving to bring this tech to market.

The impact for startups moving forward would be nuanced. Without a substantial software suite of its own, Magic Leap relied heavily on developer partnerships, though in recent months many of those seemed to promote enterprise use cases. AR/VR startups are already in a rough position, and one less developer platform could force more companies to de-prioritize headset-based platforms and shift their focus to mobile.

Powered by WPeMatico

Ask any woman and she will tell you that most of her bras do not fit her optimally. In fact, a majority of women end up wearing the wrong size. A large part of the problem is that sizing is standardized, unlike women’s bodies. With every passing year, more people are also shopping online, meaning fewer opportunities to actually try on bras — a trend that’s only accelerating given the shutdown the world is experiencing right now.

One particular problem, and a widespread one, according to entrepreneurs Jaclyn Fu and Lia Winograd, is that bras are generally too big for small-chested women. It’s the reason the former co-workers came together to found Pepper, a three-year-old, Denver-based startup that’s expressly focused on creating bras that fit smaller cup sizes.

As Fu explains it, most bra companies use a size, say 36C, then apply that same design to other bra sizes, like a 32A. While the step is logistically sound — applying a standard base design to other sizes — it doesn’t translate well into actual fit.

“It means a person who is a 32A is wearing a design that was intended for a 36C, causing fit issues like cup gaps,” says Fu.

Usually, women try to resolve the problem by tightening their bra straps or changing sizes, but Pepper’s solution is to create its own, smaller cup molds from a factory in Medellin, Colombia, where Winograd grew up.

Fu made the first prototype for Pepper based on her own chest size. Since then, she’s gone to customers’ houses to conduct fittings and research. Beyond cup size, Pepper also addresses underwire woes, making its products less curved and shorter to follow the natural size of a smaller-chested woman.

To increase customer engagement, Pepper started virtual one-to-one fit sessions for customers who are buying a bra online for the first time, and like other companies has a “fit quiz” for people to take online, too.

Pepper now sells a wide variety of sizes, all the way from from 30A to 38B, and prices range from $48 to $54.

Pepper certainly isn’t the only startup trying to fit into the bra industry. Companies like Kala, SlickChicks and ThirdLove all tout comfort and inclusivity in sizing and fitting.

The biggest of the three is ThirdLove, a San Francisco DTC bra and underwear company that has raised $68.6 million in known venture capital to date, per Crunchbase. ThirdLove brands itself as a brand that sells a “bra for every body” with inclusive sizes, and is now expanding into retail, international markets and swim and athletic wear. The company was last valued at more than $750 million.

It’s unclear how many new brands the market can support, or that can survive this pandemic. Even companies with meaningful market share and fresh capital are struggling to stay afloat as shoppers reduce their spend right now. Earlier this month, ThirdLove laid off 30% of its staff, citing COVID-19’s impact on business.

Even still, Pepper’s founders remain optimistic. Pepper’s Kickstarter $10,000 launch campaign — staged in 2017 — was separately funded in less than 10 hours, Fu notes.

The success of that campaign just helped the company secure $2 million in seed funding from investors, including Precursor Ventures, New York University Innovation Fund and Denver Angels. Others participating include the co-founder of MyFitnessPal, Albert Lee.

Fu adds that the company, which employs three people, is “close to profitability” on a $3 million revenue run rate. In 2019, most of its sales came directly from consumers on their site — a good sign that its growth ties to user loyalty versus relying on partnerships with retailers.

The nuance of buying a bra has long been an in-person ordeal. But now, because of COVID-19’s spread and the resulting shut down of many brick-and-mortar stores, those who need a new bra might have to turn online for the very first time. It’s an opportunity for companies like Pepper to prove that they can master fit without measuring tape and a changing room.

Powered by WPeMatico

The tech industry (and the world at large) is not experiencing temporary anxiety — the uncertainty we’re all coping with is the new normal.

Sudden shifts in behavior have made some startups targeting slow-moving, old-school industries more relevant than they could have imagined, such as those in telehealth, distance learning and remote work. Most, however are seeing massive decreases in revenue, forcing them to cut costs and even lay off teams to slash burn rates. Other startups simply won’t be here in three to six months.

Cowboy Ventures founder and managing partner Aileen Lee, who coined the term “unicorn,” says tech companies going through scenario planning need to begin thinking long-term.

“We’ve spent the last month scenario planning with our portfolio companies, and in most cases, we’ll have conversations about what these scenarios can include,” said Lee. “And when we look at the planning around those scenarios, they often don’t feel conservative enough. Most entrepreneurs are optimists, and we are, too! But it seems safer to have more conservative plans [and start expecting] that this is going to impact us for longer and be worse than we expected.”

Lee and Cowboy Ventures partner Ted Wang joined TechCrunch on Tuesday for our first episode of Extra Crunch Live, a virtual speaker series for Extra Crunch members. In a live Q&A that included questions from myself and the Extra Crunch audience, Wang and Lee covered a wide range of topics, including PPP loans, advice for business leaders around layoffs, the right time to seek funding and the right firms from which to seek that funding, how to pitch during a downturn and which sectors in particular Cowboy is interested in financing right now.

You can check out the best insights from the call, or catch up on the full conversation via the YouTube embed below.

We have several outstanding guests, including Charles Hudson, Mitch and Freada Kapor, Mark Cuban, Roelof Botha, Hunter Walk and Kirsten Green, joining us on Extra Crunch Live over the next few weeks. Sign up for Extra Crunch to get access to all of them.

Powered by WPeMatico

Two months ago, seemingly out of nowhere, CrowdStrike’s co-founder Dmitri Alperovitch decided it was time to depart.

Alperovitch, who served as the cybersecurity giant’s chief technology office since its 2011 debut, said he was leaving to launch a non-profit policy accelerator. CrowdStrike named Michael Sentonas, who managed the firm’s tech strategy for three years, as his replacement.

The news came at a critical time for the maker and seller of subscription-based endpoint security software that protects against breaches and cyberattacks. The company’s stock was in recovery after it fell below its IPO price, just months after popping 90% on its first day on the public market. It was one of the biggest offerings of the year, reaching more than $11 billion in value by the end, a far cry from a decade earlier when the security giant started out as a few notes scribbled on a napkin in a hotel lobby.

And then the pandemic happened.

By the time of his appointment, Sentonas was preparing to move to the U.S. from his native Australia, but “that hasn’t been the easiest thing to work through,” he told TechCrunch in a recent call. Despite having to balance the time difference and often swapping days with nights, the newly-appointed chief technology officer says it’s largely been “business as usual” for CrowdStrike.

Here’s why.

This interview was edited for clarity and length.

TechCrunch: Two months ago, you were appointed chief technology officer at CrowdStrike. Prior to that you were vice president of tech strategy. How have things been since the promotion?

Michael Sentonas: In some respects, things have been business as usual. A lot of the work I was doing around tech strategy and longer-term vision about [what] we should be working on hasn’t changed for me. Obviously, when one of the co-founders moves on, they have big shoes to fill. So, I’ve inherited a larger team. It’s working with the team around what can I assist them with to help us continue to focus. Probably the biggest change is just being stuck here because of what’s going on around the world and just adjusting to largely covering a U.S. timezone from Australia, which isn’t easy.

That can’t be easy?

We’re a globally-spread and globally-diverse organization. The last statistic that I looked at a few weeks ago was that 70% of our staff logins are remote. I’m dealing with Europe and the U.S., that’s just the way we’re spread. It’s all around the world.

Powered by WPeMatico

Meet Libeo, a French startup that just raised a $4.4 million (€4 million) funding round led by LocalGlobe, with Breega and various business angels also participating. The company has built a service that helps you pay your providers much more easily. You no longer have to manually keep track of invoices, log into your banking interface, enter banking information and transfer money.

Libeo targets small and medium companies that don’t necessarily have a dedicated accounting team. It wants to simplify payment processes as much as possible.

It starts by collecting invoices from your suppliers. You can import invoices to your Libeo account directly on Libeo by forwarding emails to a special address, by connecting Libeo to popular services, such as Amazon, or by connecting Libeo with your existing accounting platform, such as QuickBooks or Receipt Bank.

Once your invoices are all on Libeo, the startup automatically fills out payment information based on information on the invoice. It also can identify duplicates and keep track of VAT payments.

After that, Libeo wants to simplify payments. When you sign up, you share your company’s IBAN with Libeo so that it can take money from your account using direct debits. Whenever there’s an outstanding invoice in your Libeo account, you can decide to pay it now or schedule payment for later. Libeo transfers money to your recipient and collects money from your bank account at the same time.

What if it’s a new supplier and you don’t have their banking information? Instead of going back and forth with your supplier to get their IBAN, your supplier receives an email from Libeo with a link. The supplier drags and drops their bank details on Libeo’s web page. Libeo then checks that everything matches with the invoice and automatically adds the IBAN information to the payment.

Over time, if you use Libeo, you get an address book of all your suppliers. You can see how much you’re spending with a specific supplier, track your cash flow and more.

Like modern software-as-a-service tools, Libeo lets you collaborate on your invoices. Multiple people can have a Libeo account with different rights. You can set up an approval workflow as well.

There’s a free plan, but it’s limited to five payments per month. You can then pay to access advanced features and get bigger limits. Five thousand companies are currently using Libeo four months after the initial release. The company has facilitated €2 million in payments.

Powered by WPeMatico