Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. You can subscribe to the newsletter here if you haven’t yet.

Ready? Let’s talk money, startups and spicy IPO rumors.

As I write to you on Friday afternoon, the Palantir S-1 has yet to drop, but TechCrunch did break some news regarding the impending filing and just how big the company actually is. Please forgive the block quote, but here’s our reporting:

In screenshots of a draft S-1 statement dated yesterday (August 20), Palantir is listed as generating revenues of roughly $742 million in 2019 (Palantir’s fiscal year is a calendar year). That revenue was up from $595 million in 2018, a gain of roughly 25%. […] Palantir lists a net loss of roughly $580 million for 2019, which is almost identical to its loss in 2018. The company listed a net loss percentage of 97% for 2018, improving to a loss of 78% for last year.

A few notes from this. First, those losses are flat icky. Palantir was founded in 2003 or 2004 depending on who you read, which means that it’s an old company. And it was running an effective -100% net margin in 2018? Yowza.

Second, what the flocking frack is that revenue number? Did you expect to see Palantir come in with revenues of less than $1 billion? If you did, well done. After a deluge of articles over the years discussing just how big Palantir had become, I was anticipating a bit more (more here for context). Here are two examples:

Notably, Palantir’s real revenue result, or one very close to it, made it into Business Insider this April. The reporting makes the company’s S-1 less of a climax and more of a denouement. But, hey, we’re still glad to have the filing.

The Exchange will have a full breakdown of Palantir’s numbers Monday morning, but I think what Palantir coverage over the years shows is that when companies decline to share specific revenue figures that are clear, just presume that what they do share is misleading. (ARR is fine, trailing revenue is fine, “contract” metrics are useless.)

The Exchange spent a lot of time digging into e-commerce venture capital results this week, including notes from some VCs about why e-commerce-focused startups aren’t raising as much as we might have guessed.

Overstock!

We got a chance to fire a question over to the CEO of Overstock.com on the matter, adding to what we learned from private investors on the same topic. So here’s the online retailer’s CEO Jonathan Johnson, answering our question on how many smaller vendors are signing up to sell on its platform during today’s e-comm boom:

We have had increased demand to sell on Overstock and we are adding new partners daily. To protect the customer experience, we have become more selective and have increased the requirements to become a selling partner on our site. Our customers’ experience is critical to our long-term success and if partners cannot perform to our operational standards, we do not allow them to sell on our site.

We care because Shopify and BigCommerce are stacking up new rev, and we were curious how widely the e-commerce step-change from major platforms extended. Seems like all of them are eating.

How today’s evolving economic landscape isn’t working out better for e-commerce-focused startups is still a surprise. Normally when the world changes rapidly, startups do well. This time it seems that Amazon and a few now-public unicorns are snagging most of the gains.

Airbnb!

Anyhoo, onto the Airbnb world; we have a few data points to share this week. According to Edison Trends data that was shared with us, here’s how Airbnb is doing lately:

This explains why the company is prepping to go public sooner rather than later: The second-half of Q2 was a ramp back to normal for the company, and July was pretty good by the looks of it. If Airbnb is worth what it once was is not clear, but the company is certainly doing better than we might have expected it to. (More on the comeback here.)

For more on the big unicorn IPOs, I wrote a digest on Friday that should help ground you. I can say that with some confidence, as I wrote it to ground myself!

Finally some loose ends and other notes like an after-dinner amuse-bouche:

And we’ll wrap with a tiny note from Greg Warnock, managing director at Mercato via email about the late-stage venture capital market. We asked for “notes on current valuation trends, in particular re: ARR/run rate multiples.” Here’s what we heard back:

I think valuations are correlated with economic activity and certainly something like COVID would qualify, but it’s very much a lagging indicator. It takes a while for entrepreneurs’ expectations to shift. Once they feel like the economy has moved in a permanent way, they begin to rethink. The first thing that they experience a little bit more urgency. They start from a belief that they can raise money any time they want, from anyone they want. Soon they realize there are fewer investors in market, that those opportunities appear less frequently, and each one should be managed more carefully. From there they go to thinking about terms. They might have to be flexible around some terms or some construct. Finally, they go to just fundamentally thinking about valuation in terms of multiples.

Going back to my first comment about economic factors being a lagging indicator, COVID related shocks haven’t moved through the system yet. It will take something more like a year for all the expectations to shift. My experience is that a shift in the economy from an investor standpoint creates a flight to quality. Companies with lackluster performance are first to feel lack of options in fundraising and exits. High performing businesses are the last ones to experience a change in valuation multiples. It disproportionately affects average businesses more quickly and more dramatically than high quality businesses which may feel no significant effects.

Hugs, fist bumps and good vibes,

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7am PT). Subscribe here.

The public markets are staying receptive to tech IPOs, and tech unicorns are trying to recover from pandemic damage, polish up their financials, and head back towards the starting gates. This week, it’s Airbnb and Palantir, finally. Both have been startup icons of the past decade, and literally helped define the term “unicorn.” Now, both are illustrating the challenges that can come from sticking to private funding for years when going public was feasible.

First up, the travel rental company filed confidentially on Wednesday for a public offering, which means we’ll probably get a look at the numbers after Q3 is accounted for, as Alex Wilhelm has been covering. It had eventually decided to go public this year, then the pandemic reshaped its business and forced a down-round and mass layoffs. Now, it says its business has been booming again, and at the expense of some incumbents. The cost-savings plus the fresh growth potential could prove an exciting combo to public markets.

Palantir, meanwhile, appears headed to an IPO soonish judging by the S-1 screenshots that Danny Crichton scooped yesterday. However, the oldest unicorn (17 years) is still losing hundreds of millions every year, it still has a concentrated group of customers for its data and consultancy products, and its commercial business is still relatively smaller than government. The more positive financial news it has to offer? Government revenue lines have been up this year, apparently related to more pandemic demand, and the commercial side had been growing since before then. It is also working to manage its stock price, Danny hears, by doing a direct listing that unusually comes with a lock-up period for employees.

There were many reasons for unicorns to stay private this past decade, including huge checks, exciting growth, often-friendly terms and a general lack of scrutiny. Almost nobody actually thought a pandemic would affect everything like this. And without the pandemic, maybe the easy hindsight would be that the slow pace to IPO was the right one? Instead, each company is having to make decisions that damage its precious pool of talented employees and carefully nurtured culture.

In this scary new decade, founders who aspire to succeed on the scale of Airbnb and Palantir may see public markets as a less risky way to reward shareholders and fund future growth?

Or maybe more startups will be less interested in big equity rounds in the first place? Danny talked to one founder for Extra Crunch who has gone this route successfully with SaaS securitization.

Finally, check out Alex’s overview of what other companies are on the IPO track now over on Extra Crunch. These include: Asana, Qualtrics, ThredUp, Ant Financial, Affirm and once you get past this calendar year, many many more.

(Photo by Smith Collection/Gado/Getty Images)

In another sign of the changing times, a prominent local coffee shop for startups in San Francisco has closed up. Yes, The Creamery is done, sooner or later to be bulldozed for a development that has been years in the works. My former TechCrunch colleague Ryan Lawler came back to write a guest requiem for us. Here’s the start, but I suggest reading to the end to fully experience throat-lumping nostalgia about a certain time you didn’t know you were going to miss:

I don’t remember the first time I went to The Creamery, probably sometime in early 2012.

I don’t remember the last time, either, although undoubtedly it was sometime last year, on a day when I had an extra five minutes to spare before boarding the Caltrain for my morning commute.

And I barely remember any of the other hundreds of times I stopped in to grab a coffee, have lunch with a friend or meet a possible source during my years at TechCrunch, which conveniently had an office just over a block away.

The Creamery was not a place you went for the memories. It was located firmly at the apex of convenience and comfort — which is why, for a certain period of about five years from the early to mid-teens of the third millennium, it was the perfect place for the SF technorati to see and be seen.

It’s also why, after 12 years of operating from one global recession to another, it’s shutting its doors for good….

Image Credits: Dennis Lane / Getty Images

In our latest Extra Crunch investor survey, Alex teamed up with Lucas Matney to find where no-code concepts are actually having a big impact (versus just sounding exciting, which they do already). Here’s Laela Sturdy with CapitalG:

I don’t think it’s over-hyped, but I believe it’s often misunderstood. No code/low code has been around for a long time. Many of us have been using Microsoft Excel as a low-code tool for decades, but the market has caught fire recently due to an increase in applicable use cases and a ton of innovation in the capabilities of these new low-code/no-code platforms, specifically around their ease of use, the level and type of abstractions they can perform and their extensibility/connectivity into other parts of a company’s tech stack. On the demand side, the need for digital transformation is at an all-time high and cannot be met with incumbent tech platforms, especially given the shortage of technical workers. Low-code/no-code tools have stepped in to fill this void by enabling knowledge workers — who are 10x more populous than technical workers — to configure software without having to code. This has the potential to save significant time and money and to enable end-to-end digital experiences inside of enterprises faster….

If you look at large businesses today, IT departments and business units are perpetually out of alignment because IT teams are resource constrained and unable to address core business needs quickly enough. There just isn’t enough IT talent out there to meet demand, and issues like security and maintenance take up most of the IT department’s time. If business users want to create new systems, they have to wait months or in most cases years to see their needs met. No-code changes the equation because it empowers business users to take change into their own hands and to accomplish goals themselves. The rapid state of digital transformation — which has only been expedited by the pandemic — requires more business logic to be encoded into automations and applications. No code is making this transition possible for many enterprises.

(Photo by Michael Kovac/Getty Images for Vanity Fair)

After being early to the modern SPAC trend, long-time investor and former Facebook executive Palihapitiya has an additional master plan in the works. It is sort of like the SPAC plan but with even fewer other investors to disagree with. Natasha Mascarenhas has the details:

Hustle is Social Capital’s third acquisition in the past three years. In 2018, Social Capital bought a healthcare business that has a repository of data around human physiology. Last year, the firm scooped up a mental health startup that’s centered around software-based treatments and tracks how users progress. Palihapitiya declined to disclose the names of either investment, citing competitive advantages in keeping them out of the press for now.

“I like businesses that build non-obvious data links,” he said, noting that it is unlike AI, machine learning and other futuristic technologies. Although his SPAC returns could fuel acquisitions, he says that his deals have been funded through personal capital.

Palihapitiya’s long-term strategy for Hustle is to create an empire around it. He plans to acquire auxiliary businesses that see $5 to $15 million in ARR, consolidate them, and “now all of a sudden, you can see us getting to hundreds of millions of ARR.”

The Hustle deal closed in about a week. He says that investing out of a permanent balance sheet of his own capital lets him underwrite decisions faster than a traditional venture capital firm, which lines up with the investor’s general anti-VC sentiment. He pointed to Credit Karma and Intuit’s merger that is yet to close. “We’re still waiting for that deal,” Palihapitiya said. “You know, I couldn’t write an $8.8 billion acquisition myself. But I could write a $5 billion one.”

(Nhat V. Meyer/Bay Area News Group)

The problem is not new, of course, but Lucas got fresh insights from former Facebook PR leader Caryn Marooney about the right strategies to solve the problem, and put together an explainer for Extra Crunch. Here’s an excerpt:

Getting someone to care first depends on proving your relevance. When founders are forming their messaging to address this, they should ask themselves three questions about their strategy, she recommends:

- Why should anyone care?

- Is there a purchase order existing for this?

- Who loses if you win?

These questions get to the root of what you’re providing, whether there’s a customer and who you’re up against. From there they can also help companies identify how to broaden their relevance in the face of new developments in the market.

“As a startup you start with no relevance,” she says. “So your relevance comes from: you’re a founder people know, you’ve come from a company people care about or you’re in a space that’s already relevant and people want to know about, or you’re about to kill a competitor that people really care about, or you have customers where you sort of get the relevance from the customers.”

Cloudflare’s Michelle Zatlyn to discuss building a company with a bold idea at TechCrunch Disrupt

Submit your pitch deck to Disrupt 2020’s Pitch Deck Teardown

The founders of Blavity and The Shade Room are coming to Disrupt 2020

Sign up to interview with accelerators before Disrupt 2020

Students get 60% off passes to Disrupt 2020

Get a free annual Extra Crunch membership when you buy a Disrupt 2020 pass

Announcing the all new, virtual agenda for TC Sessions: Mobility

Investors Reilly Brennan, Amy Gu and Olaf Sakkers coming to TC Sessions: Mobility 2020

CrunchMatch supercharges virtual networking at TC Sessions: Mobility 2020

Join Twilio’s Jeff Lawson for a live Q&A August 25 at 2:30 pm EDT/11:30 am PDT

TechCrunch

Private space industrialization is here

China is building a GitHub alternative called Gitee

There’s no frontrunner to be found among the TikTok alternatives

If Oracle buys TikTok I’ll go to Danny’s house and eat his annoying Stanford sweatshirt

Here are four areas the $311 billion CPPIB investment fund thinks will be impacted by COVID-19

Extra Crunch

Founders can raise funding before launching a product

Max Levchin is looking ahead to fintech’s next big opportunities

How tech can build more resilient supply chains

Dear Sophie: How can I transfer my H-1B to my startup?

PopSugar co-founder says pandemic will create ‘a huge windfall’ for digital mediate

From Alex:

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

What happens when the entire podcast crew is a bit tired from, you know, everything, and does its very best? This episode, apparently. A big thanks to Chris Gates for helping us trim the fat and make something good for you.

Before we get into the topics of the week, don’t forget that Equity is not back on YouTube most weeks, so if you wanted to see us do the talking with some fun extra from the production team, you can do so here. More to come once I get my new external camera to work.

That done, here’s what Natasha and Danny and I got into this week:

Whew! We’re doing a lot over at TechCrunch.com, so, stay tuned and know that if we were a bit frazzled this week it’s because we’re working our backends off to bring you neat things. You will dig ’em.

OK, chat Monday, a show that we’re already planning. Stay cool!

Equity drops every Monday at 7:00 a.m. PT and Friday at 6:00 a.m. PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

A few years ago, I came to the realization that my company, an HR consulting firm, was not as diverse as I wanted it to be. I value diversity because I know it makes teams better — more creative, more productive and more nimble. It helps my firm represent our community and serve our clients.

Though I tried to be inclusive in the language and the images I used on my website, in social media and when posting job openings, clearly something wasn’t working. I’m fortunate to know many talented diversity, equity and inclusion (DEI) experts. I asked them what I needed to do differently to attract a broader and more diverse pool of candidates. Here’s what they told me.

This may seem obvious, but it’s actually something many companies don’t do. When we talk about diversity, people tend to think only of race and gender. Our definition of diversity can be narrow, and we fail not only to include physical ability, gender identity and a host of other underestimated groups, but to recognize that even within a company, who is well represented versus underrepresented can vary by team or department.

I noticed a lack of diversity among my team of coaches; it was all women, but there were few women of color. The gender imbalance is not a surprise; according to the International Coaching Federation (ICF), approximately two-thirds of coaches are women. It would have been all too easy to throw up my hands and say “Well, there just aren’t enough qualified male coaches.” But blaming the pipeline is not a valid excuse and doesn’t fix the problem.

If I told people, “I’m trying to increase diversity on my team,” they would not have known what I meant; they would have been left to assume. Instead, I reached out to a small group of coaches who I know and trust, and told them “I’m looking for more coaches. Specifically, I would like to add women of color and I’d also like to have more men on the team.”

In the U.S., where we’ve been taught for so long not to talk about race or gender while hiring, this felt awkward. I had to push past that, and I’m thankful I did. The result was that I was not only able to add a number of experienced coaches to my team, I also built a whole new network of talented, diverse coaches from whom I continue to learn.

When you want to appeal to the most diverse candidates, language matters. It is (hopefully) obvious that terms like rock star, stud and ninja, which have been used all too frequently in job descriptions, are exclusive and off-putting to many candidates. But other words and phrases to use or avoid aren’t always common sense. The most appealing language can vary by job level, title and even geography.

Using a tool like Textio will help you create a job description that welcomes the most candidates to apply. Textio uses machine learning and algorithms from millions of job descriptions to help you spot and remove language that can unintentionally narrow your pool. Pop in your job description and you’ll get recommendations about the optimal length of your JD, word choices that skew masculine or feminine, sentence length and even whether your job suggests a fixed or growth mindset.

We’ve all seen the old equal employment opportunity (EEO) statement at the end of a job posting, which reads: “We’re an equal opportunity employer. All applicants will be considered for employment without attention to race, color, religion, sex, sexual orientation, gender identity, national origin, veteran or disability status.” It sounds like it came right off the government website, which it probably did. And that’s exactly how it comes across to candidates — like a canned message that you’ve added just to make sure you’re in compliance.

Did you know that you can customize your EEO statement? People do read it, and sticking with the legal jargon can be off-putting. A generic statement doesn’t say anything positive about your brand, and it doesn’t demonstrate a true commitment to diversity. If you haven’t already, now is the perfect time to update your statement, making it more reflective of your culture and values. For example:

“SurveyMonkey is an equal opportunity employer. We celebrate diversity and are committed to creating an inclusive environment for all employees.”

Is it worth the effort? According to FairyGodboss, these personalized EEO statements “…communicate an employer’s dedication to unbiased recruiting, hiring and employment practices, which may encourage traditionally marginalized groups to seek employment within the organization.”

Most people are familiar with unconscious bias, and how it can negatively impact every step of the hiring process. Even as early as the resume review, bias causes recruiters and hiring managers to favor resumes of candidates who are in the majority. Bias can result from information ranging from a candidate’s name to which college they attended or which sports they played.

For instance, those with white-sounding names receive preference. The National Bureau of Economic Research found that “Job applicants with white names needed to send about 10 resumes to get one callback; those with African-American names needed to send around 15 resumes to get one callback.” I have a friend from India who received similar treatment. Even though she had worked with well-known companies, including Google and Deloitte, she had difficulty landing a job when she first came to the U.S. When she was ready to change employers, she adopted an American nickname on her resume and LinkedIn profile, and promptly got five callbacks.

In a blind resume review, identity cues that indicate race or gender are hidden. Tools like TalVista do this automatically, or your team can do it manually by hiding the information. While this helps increase the number of diverse candidates who make it to the next step, it does not address bias that occurs during interviews or later in your hiring process. That’s going to require training.

People from underestimated groups are all too familiar with the phrase “you have to see it to be it.” If I can’t see myself as someone who will be welcome and included in your company, I’m far less likely to join it. Yet too often even when a candidate meets with multiple interviewers, none of those interviewers reflect the candidate’s race or gender.

Imagine a woman of color spending the better part of a day meeting with a potential employer. Over the course of several hours, she meets a number of leaders but she doesn’t meet a single woman of color. She might think there are no women of color in the company, or wonder why they are not included in important decisions like interviewing and hiring.

When Karenga Ross interviewed at Intel after meeting them at a National Society of Black Engineers conference, she was pleasantly surprised to meet two African American women on the interview panel — these were women who looked like her. “It’s nice to be able to look across that table and see someone whom I can aspire to be. I can see someone who looks like me. It was refreshing. It was inspiring.”

One question I get from small companies is how to assemble a diverse interview panel if they don’t yet have diversity within their organization. I encourage them to cast a wide net. Think about who’s affiliated with your company, even if they’re not employees. If you have diverse advisors, investors or board members who are willing to help, invite them to join your panel. It will improve the candidate experience and help eliminate bias from your decision making.

Increasing diversity is an important investment that takes commitment, and a willingness to learn and experiment. You’ll have to try out some new things, and perhaps have conversations that make you uncomfortable. Remember to take one step at a time, and measure your progress and results.

Diverse hiring is one important step toward increasing diversity in your organization. Retention, however, depends on all employees feeling a sense of belonging. Remember to review your internal practices and policies to make sure they too meet the test of inclusion.

Powered by WPeMatico

Few topics garner cheers and groans quite as quickly as the no-code software explosion.

While investors seem uniformly bullish on toolsets that streamline and automate processes that once required a decent amount of technical know-how, not everyone seems to think that the product class is much of a new phenomenon.

On one hand, basic tools like Microsoft Excel have long given non-technical users a path toward carrying out complex tasks. (There’s historical precedent for the perspective.) On the other, a recent bout of low-code/no-code startups reaching huge valuations is too noteworthy to ignore, spanning apps like Notion, Airtable and Coda.

The TechCrunch team was interested in digging in to what defines the latest iteration of no-code and which industries might be the next target for entrepreneurs in the space. To get an answer on what is driving investor enthusiasm behind no-code, we reached out to a handful of investors who have explored the space:

As usual, we’re going to pull out some of the key trends and themes we identified from the group’s collected answers, after which we’ll share their responses at length, edited lightly for clarity and formatting.

Our investor participants agreed that low-code/no-code apps haven’t reached their peak potential, but there was some disagreement in how universal their appeal will prove to various industries. “Every trend is overhyped in some way. Low-code/no-code apps hold a lot of promise in some areas but not all,” Lightspeed’s Raviraj Jain told us.

Meanwhile, Gradient’s Darian Shirazi said “any and all” industries could benefit from increased no-code/low-code toolsets. We can see it either way, frankly.

CapitalG’s Laela Sturdy says the breadth of appeal boils down to finding which industries face the biggest supply constraints of technical talent.

“There just isn’t enough IT talent out there to meet demand, and issues like security and maintenance take up most of the IT department’s time. If business users want to create new systems, they have to wait months or in most cases, years, to see their needs met,” she wrote. “No-code changes the equation because it empowers business users to take change into their own hands and to accomplish goals themselves.”

Mayfield’s Rajeev Batra agreed, saying it would be cool “to see not twenty million developers [building] really cool software but two, three hundred million people developing really cool, interesting software.” If that winds up being the case, the sheer number of monthly-actives in the no and low-code spaces would imply a huge revenue base for the startup category.

That makes a wager on platforms in the space somewhat obvious.

And those bets are being placed. On the topic of valuations and developer interest, our collected interviewees were largely bullish on startup prices (competitive) and VC demand (strong) when it comes to no-code fundraising today.

Sturdy added that the number of early-stage companies in the category “are being funded at an accelerating pace,” noting that her firm is “excitedly watching this young cohort of emerging no-code companies and intend to invest in the trend for years to come.” So, we’re not about to run short of fodder for more Series A and B rounds in the space.

Taken as a whole, like it or not, the no and low-code startup trend appears firm from both a market-fit perspective and from the perspective of investor interest. Now, the rest of the notes.

We’ve seen some skepticism in the market that the low-code/no-code trend has earned its current hype, or product category. Do you agree that the product trend is overhyped, or misclassified?

I don’t think it’s over-hyped, but I believe it’s often misunderstood. No code/low code has been around for a long time. Many of us have been using Microsoft Excel as a low-code tool for decades, but the market has caught fire recently due to an increase in applicable use cases and a ton of innovation in the capabilities of these new low-code/no-code platforms, specifically around their ease of use, the level and type of abstractions they can perform and their extensibility/connectivity into other parts of a company’s tech stack. On the demand side, the need for digital transformation is at an all-time high and cannot be met with incumbent tech platforms, especially given the shortage of technical workers. Low-code/no-code tools have stepped in to fill this void by enabling knowledge workers — who are 10x more populous than technical workers — to configure software without having to code. This has the potential to save significant time and money and to enable end-to-end digital experiences inside of enterprises faster.

What other opportunities does the proliferation of low-code/no-code programs open up when it comes to technical and non-technical folks working more closely together?

This is where things get exciting. If you look at large businesses today, IT departments and business units are perpetually out of alignment because IT teams are resource constrained and unable to address core business needs quickly enough. There just isn’t enough IT talent out there to meet demand, and issues like security and maintenance take up most of the IT department’s time. If business users want to create new systems, they have to wait months or in most cases years to see their needs met. No-code changes the equation because it empowers business users to take change into their own hands and to accomplish goals themselves. The rapid state of digital transformation — which has only been expedited by the pandemic — requires more business logic to be encoded into automations and applications. No code is making this transition possible for many enterprises.

Powered by WPeMatico

Feeling like you should better understand special purpose acquisition vehicles – or SPACs — than you do? You aren’t alone.

It isn’t like you’re totally clueless, right? You’re probably aware that Paul Ryan now has a SPAC, as does baseball executive Billy Beane and Silicon Valley stalwart Kevin Hartz.

You likely know, too, that brash entrepreneur Chamath Palihapitiya seemed to kick off the craze around SPACs — blank-check companies that are formed for the purpose of merging or acquiring other companies — in 2017 when he raised $600 million for a SPAC. Called Social Capital Hedosophia Holdings, it was ultimately used to take a 49% stake in the British spaceflight company Virgin Galactic.

But how do SPACs come together in the first place, how do they work exactly, and should you be thinking of launching one? We talked this week with a number of people who are right now focused on almost nothing but SPACs to get our questions — and maybe yours, too — answered.

Why are SPACs suddenly sprouting up everywhere?

Kevin Hartz — who we spoke with after his $200 million blank-check company made its stock market debut on Tuesday — said their popularity ties in part to “Sarbanes Oxley and the difficulty in taking a company public the traditional route.”

Troy Steckenrider, an operator who has partnered with Hartz on his newly public company, said the growing popularity of SPACs also ties to a “shift in the quality of the sponsor teams,” meaning that more people like Hartz are shepherding these vehicles versus “people who might not be able to raise a traditional fund historically.”

Don’t forget, too, that there are whole lot of companies that have raised tens and hundreds of millions of dollars in venture capital and whose IPO plans may have been derailed or slowed by the COVID-19 pandemic. Some need a relatively frictionless way to get out the door, and there are plenty of investors who would like to give them that push.

How does one start the process of creating a SPAC?

The process is really no different than a traditional IPO, explains Chris Weekes, a managing director in the capital markets group at the investment bank Cowen. “There’s a roadshow that will incorporate one-on-one meetings between institutional investors like hedge funds and private equity funds and the SPAC’s management team” to drum up interest in the offering.

At the end of it, institutional investors, which also right now include a lot of family offices, buy into the offering, along with a smaller percentage of retail investors.

Who can form a SPAC?

Pretty much anyone who can persuade shareholders to buy its shares.

What happens right after SPAC has raised its capital?

The money is moved into a blind trust until the management team decides which company or companies it wants to acquire. Share prices don’t really move much during this period as no investors know (or should know, at least) what the target company will be yet.

These SPACs all seem to sell their shares at $10 apiece. Why?

Easier accounting? Tradition? It’s not entirely clear, though Weekes says $10 has “always been the unit price” for SPACs and continues to be with the very occasional exception, such as with hedge fund billionaire Bill Ackman’s Pershing Square Capital Management. (Last month it launched a $4 billion SPAC that sold units for $20 each.)

Have SPACs changed structurally over the years?

They have! Years back, when a SPAC told its institutional investors (under NDA) about the company it had settled on buying, these investors would either vote ‘yes’ to the deal if they wanted to keep their money in, or ‘no’ if they wanted to redeem their shares and get out. But sometimes investors would team up and threaten to torpedo a deal if they weren’t given founder shares or other preferential treatment in what was to become the newly combined company. (“There was a bit of bullying in the marketplace,” says Weekes.)

Regulators have since separated the right to vote and the right to redeem one’s shares, meaning investors today can vote ‘yes’ or ‘no’ and still redeem their capital, making the voting process more perfunctory and enabling most deals to go through as planned.

I’ve read something about warrants.

That’s because when buying a unit of a SPAC, institutional investors typically get a share of common stock, plus a warrant or a fraction of a warrant, which is a security that entitles the holder to buy more stock of the issuing company at a fixed price at a later date. It’s basically an added sweetener to motivate them to buy into the SPAC.

Are SPACs safer investments than they once were? They haven’t had the best reputation historically.

They’ve “already gone through their junk phase,” suspects Albert Vanderlaan, an attorney in the tech companies group of Orrick, the global law firm. “In the ’90s, these were considered a pretty junky situation,” he says. “They were abused by foreign investors. In the early 2000s, they were still pretty disfavored.” Things could turn on a dime again, he suggests, but over the last couple of years, the players have changed for the better, which is making a big difference.

How much of the money raised does a management team like Hartz and Steckenrider keep?

The rough rule of thumb is 2% of the SPAC value, plus $2 million, says Steckenrider. The 2% roughly covers the initial underwriting fee; the $2 million then covers the operating expenses of the SPAC, from the initial cost to launch it, to legal preparation, accounting, and NYSE or NASDAQ filing fees. It also “provides the reserves for the ongoing due diligence process,” he says.

Is this money like the carry that VCs receive, and do a SPAC’s managers receive it no matter how the SPAC performs?

Yes and yes.

Here’s how Hartz explains it: “On a $200 million SPAC, there’s a $50 million ‘promote’ that is earned.” But “if that company doesn’t perform and, say, drops in half over a year or 18-month period, then the shares are still worth $25 million.”

Hartz calls this “egregious,” though he and Steckenrider formed their SPAC in exactly the same way rather than structure it differently.

Says Steckrider, “We ultimately decided to go with a plain-vanilla structure [because] as a first-time SPAC sponsor, we wanted to make sure that the investment community had as easy as a time as possible understanding our SPAC. We do expect to renegotiate these economics when we go and do the [merger] transaction with the partner company,” he adds.

Does a $200 million SPAC look to acquire a company that’s valued at around the same amount?

No. According to law firm Vinson & Elkins, there’s no maximum size of a target company — only a minimum size (roughly 80% of the funds in the SPAC trust).

In fact, it’s typical for a SPAC to combine with a company that’s two to four times its IPO proceeds in order to reduce the dilutive impact of the founder shares and warrants.

In the case of Hartz’s and Steckenrider’s SPAC (it’s called “one”), they are looking to find a company “that’s approximately four to six times the size of our vehicle of $200 million,” says Hartz, “so that puts us around in the billion dollar range.”

Where does the rest of the money come from if the partner company is many times larger than the SPAC itself?

It comes from PIPE deals, which, like SPACs, have been around forever and come into and out of fashion. These are literally “private investments in public equities” and they get tacked onto SPACs once management has decided on the company with which it wants to merge.

It’s here that institutional investors get different treatment than retail investors, which is why some industry observers are wary of SPACs.

Specifically, a SPAC’s institutional investors — along with maybe new institutional investors that aren’t part of the SPAC — are told before the rest of the world what the acquisition target is under confidentiality agreements so that they can decide if they want to provide further financing for the deal via a PIPE transaction.

The information asymmetry seems unfair. Then again, they’re restricted not only from sharing information but also from trading the shares for a minimum of four months from the time that the initial business combination is made public. Retail investors, who’ve been left in the dark, can trade their shares any time.

How long does a SPAC have to get all of this done?

It varies, but the standard is around two years.

And if they can’t get it done in the designated time frame?

The money goes back to shareholders.

What do you call that phase of the deal after the partner company has been identified and agrees to merge, but before the actual combination?

That’s called the de-SPAC’ing process, and during this stage of things, the SPAC has to obtain shareholder approval, followed by a review and commenting period by the SEC.

Toward the end of this stretch — which can take 12 to 18 weeks altogether — bankers start taking out the new operating team in the style of a traditional roadshow and getting the story out to analysts who cover the industry so that when the combined new company is revealed, it receives the kind of support that keeps public shareholders interested in a company.

Will we see more people from the venture world like Palihapitiya and Hartz start SPACs?

Weekes, the investment banker, says he’s seeing less interest from VCs in sponsoring SPACs and more interest from them in selling their portfolio companies to a SPAC. As he notes, “Most venture firms are typically a little earlier stage investors and are private market investors, but there’s an uptick of interest across the board, from PE firms, hedge funds, long-only mutual funds.”

That might change if Hartz has anything to do with it. “We’re actually out in the Valley, speaking with all the funds and just looking to educate the venture funds,” he says. “We’ve had a lot of requests in. We think we’re going to convert [famed VC] Bill Gurley from being a direct listings champion to the SPAC champion very soon.”

In the meantime, asked if his SPAC has a specific target in mind already, Hartz says it does not. He also takes issue with the word “target.”

Says Hartz, “We prefer ‘partner company.’” A target, he adds, “sounds like we’re trying to assassinate somebody.”

Powered by WPeMatico

As a founding member of TI Platform Management, I have quarterbacked more than $200 million in investments into first-time fund managers around the world. That portfolio includes being one of the first institutional checks into Atomic Labs ($170+ million, SaaStr ($160+ million) and Entrepreneur First ($140+ million), among many others.

Having seen successful returns as a fund manager and an early-stage VC (as well as recently raising my own angel fund), I’ve formulated several best practices and strategies for investing in fund managers. If you want to raise your first fund, here’s how.

Just as VCs bucket startup founders into categories, limited partners (the investors in your venture fund, also known as “LPs”) have an unwritten way of categorizing venture managers. The vast majority fit one of three archetypes:

Here’s how each is perceived by institutional LPs and the unique blockers they have to overcome:

Having been through the journey of starting a company, former founders/operators often have strong intuition in identifying founders and an empathy/rapport that raises their win-rate on deals. Additionally, having built an innovative company, they can bring special insights in where the market is headed. Building a company, however, requires different skills from founding a fund.

If you’re a former founder/operator turned VC, expect LPs to ask questions that suss out:

Powered by WPeMatico

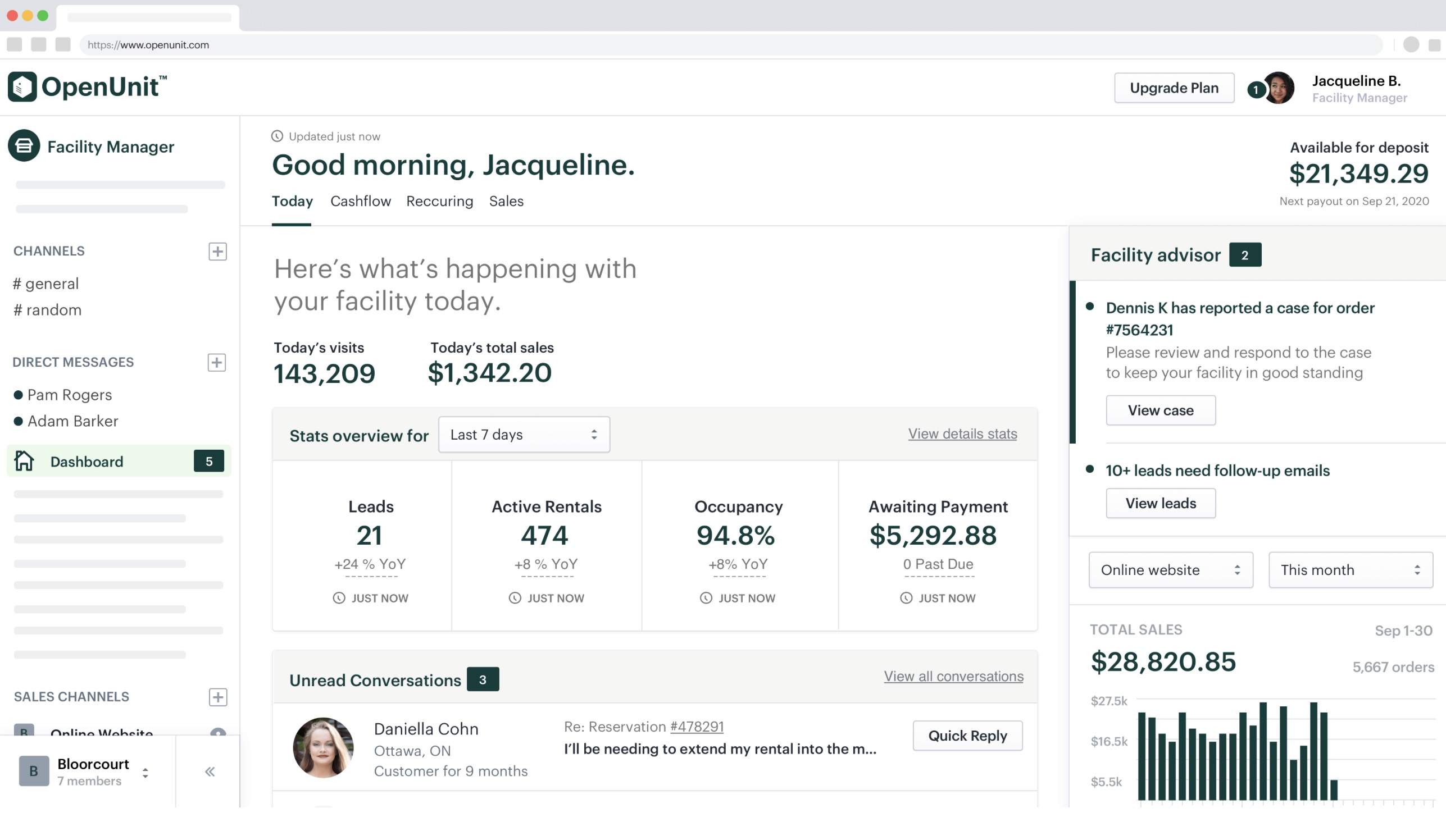

So you’re looking for a storage unit to put some stuff in for a few months. Maybe you’re moving and your new place isn’t ready yet — or maybe you’re just looking to declutter and want to tuck some stuff away for a while and see if you’re really ready to part with it.

As you may find, the process of finding a storage unit can be… not great. While there are a few big storage chains in the market, a huge chunk of the self-storage industry is made up of independent/mom-and-pop shops that don’t necessarily have the time/budget to keep up as tech has evolved. It can involve a lot of poking around out-of-date websites, a lot of phone calls and a lot of paperwork.

OpenUnit, a startup out of Toronto, wants to fix that. They’re aiming to be Shopify for the self-storage industry, with an all-in-one solution that provides a modern interface to help customers make reservations on the front end, and gives facility managers everything they need to keep things running on the back end.

Their management tool provides things like:

The company isn’t charging facility managers a monthly fee; instead, they’re handling credit card payment processing and taking a cut of 2.9% (+ 30 cents) per transaction.

Co-founders Taylor Cooney and Lucas Playford found their way into self-storage when Taylor’s landlords came to him with an offer: they wanted to sell the place he was renting, and they’d give him a stack of cash if he could be out within just a few days. Pulling that off meant finding a place to keep all of his stuff while he looked for a new home, which is when he realized how antiquated the self-storage process could be.

Image Credits: OpenUnit

The two initially set their sites on something a bit different: a Hotwire-style search system that would find deals on local storage units, negotiating the monthly cost on a customer’s behalf for a small one-time fee. The more they worked with facility managers, the more gaps they found in the tools and systems on the market, so they shifted focus to this facility management suite.

OpenUnit was part of the Winter 2020 Y Combinator class which ended back in March, but the team opted to defer their demo day debut until YC’s Summer 2020 event next week. As March came to an end and the severity of the pandemic was becoming more clear, Canadian Prime Minister Justin Trudeau called upon any citizens abroad to return home sooner than later. Launching a company while rushing to get back home is hardly ideal, so the two chose to hold off their launch until now.

After a few weeks of private testing, OpenUnit is now starting to bring more storage facilities on board. Run a storage company and want to give it a look? They’ve got a waiting list here.

Powered by WPeMatico

Avi Freedman is like any other founder: He wants to build a great company. In this case network analytics platform Kentik, and he needs venture capital to do it. Like pretty much all founders, he doesn’t like the dilution that comes from taking vast sums from VCs in order to grow. There’s always been an alluring solution to this dilemma, but one that comes with its own tradeoffs.

Debt.

The word has negative connotations, but the reality is that just like equity capital, debt is a key tool in the corporate finance toolbox. Judicious use of debt with the right terms and conditions can cut the cost of capital for a startup significantly, saving founders and early-stage investors from serious dilution as a company scales. Used too heavily or improperly however, and debt can turn a bad financial quarter into a dead company, stat.

Founders, particularly those who run companies with recurring revenues, are increasingly hearing the debt pitch from bankers and peers, leading many to consider debt options much earlier than has traditionally been the norm. Boards are also getting more comfortable with the idea of a startup taking on early debt to extend runways and double down on growth.

Let’s walk through how a founder sees debt today and discuss what the market looks like for debt options. Freedman was helpful in illuminating his recent fundraise, including the range of term sheets he got, and was willing to share his experience and thinking on how he approached his latest financing.

Some context to get started. Kentik is a six-year-old SaaS platform that has raised more than $60 million in venture capital, according to Crunchbase, including a seed round led by First Round Capital and a Series A led by the now-defunct August Capital (plus the company’s most recent equity/debt round we’re talking about today). Freedman himself has been a long-time entrepreneur, building the first ISP in Philadelphia back in 1992. Kentik was his first true “venture-backed” business in the Silicon Valley startup model.

Powered by WPeMatico

During the COVID-19 pandemic, supply chains have suddenly become hot. Who knew that would ever happen? The race to secure PPE, ventilators and minor things like food was and still is an enormous issue. But perhaps, predictably, the world of “supply chain software” could use some updating. Most of the platforms are deployed “empty” and require the client to populate them with their own data, or “bring their own data.” The UIs can be outdated and still have to be juggled with manual and offline workflows. So startups working in this space are now attracting some timely attention.

Thus, Craft, the enterprise intelligence company, today announces it has closed a $10 million Series A financing round to build what it characterizes as a “supply chain intelligence platform.” With the new funding, Craft will expand its offices in San Francisco, London and Minsk, and grow remote teams across engineering, sales, marketing and operations in North America and Europe.

It competes with some large incumbents, such as Dun & Bradstreet, Bureau van Dijk and Thomson Reuters . These are traditional data providers focused primarily on providing financial data about public companies, rather than real-time data from data sources such as operating metrics, human capital and risk metrics.

The idea is to allow companies to monitor and optimize their supply chain and enterprise systems. The financing was led by High Alpha Capital, alongside Greycroft. Craft also has some high-flying angel investors, including Sam Palmisano, chairman of the Center for Global Enterprise and former CEO and chairman of IBM; Jim Moffatt, former CEO of Deloitte Consulting; Frederic Kerrest, executive vice chairman, COO and co-founder of Okta; and Uncork Capital, which previously led Craft’s seed financing. High Alpha partner Kristian Andersen is joining Craft’s board of directors.

The problem Craft is attacking is a lack of visibility into complex global supply chains. For obvious reasons, COVID-19 disrupted global supply chains, which tended to reveal a lot of risks, structural weaknesses across industries and a lack of intelligence about how it’s all holding together. Craft’s solution is a proprietary data platform, API and portal that integrates into existing enterprise workflows.

While many business intelligence products require clients to bring their own data, Craft’s data platform comes pre-deployed with data from thousands of financial and alternative sources, such as 300+ data points that are refreshed using both Machine Learning and human validation. Its open-to-the-web company profiles appear in 50 million search results, for instance.

Ilya Levtov, co-founder and CEO of Craft, said in a statement: “Today, we are focused on providing powerful tracking and visibility to enterprise supply chains, while our ultimate vision is to build the intelligence layer of the enterprise technology stack.”

Kristian Andersen, partner with High Alpha commented: “We have a deep conviction that supply chain management remains an underinvested and under-innovated category in enterprise software.”

In the first half of 2020, Craft claims its revenues have grown nearly threefold, with Fortune 100 companies, government and military agencies, and SMEs among its clients.

Powered by WPeMatico

Startup founders, brace yourself for a phenomenal opportunity. TechCrunch, in partnership with cela, will host eleven — count ‘em eleven — accelerators in Digital Startup Alley at Disrupt 2020. It gets better: they’re accepting applications for their upcoming virtual accelerator programs, and this is your chance to interview with them.

Do you want in on this potentially life-changing speed networking opportunity? There’s only one requirement: you must be an exhibitor in Digital Startup Alley. If you don’t have one yet, go buy your Digital Startup Alley Package right now.

Not familiar with cela or its mission? The New York City-based company matches early-stage startups to world-class accelerators and incubators — within its global network — that align with a startup’s vertical and business goals.

cela already connected winners of our ongoing Pitchers and Pitches mini pitch-off competitions (register to attend the next one on September 2nd — it’s free) with an appropriate accelerator. Here’s what pitch-off winner Hannah Webb, CEO of Findster Technologies, said about her experience.

“Disrupt and Digital Start Up Alley haven’t even officially started yet, and we’ve already seen great benefits. cela introduced us to multiple accelerators in the NYC area and one is a perfect fit for our company’s situation.”

A good accelerator can give founders an enormous boost. Finding the right one for your startup is crucial, and it can be tricky. That’s where cela’s guidance — and its extensive network — can help.

“During these speed networking events, we will match selected founders to curated, 1:1 meetings with the Managing Directors of some of the world’s most respected accelerator programs. Founders that apply can discuss investment, sales, team building, product development, marketing and any other challenge or opportunity their startup is pursuing.” — John Lynn, co-founder, cela.

Speed networking sessions take place over three days during the week prior to Disrupt 2020. Here’s the schedule, so mark your calendars now and get ready to impress.

Date: September 8

Time: 1 p.m. – 4 p.m. PT

Accelerators: NUMA, Techstars, Entrepreneurs Roundtable Accelerator

Date: September 9

Time: 1 p.m. – 4 p.m. PT

Accelerators: She Gets Sh!t Done, Halo Incubator, Startup Boost Pre- Accelerator, Plug and Play

Date: September 10

Time: 1 p.m. – 4 p.m. PT

Accelerators: Backstage Capital, Global Startup Ecosystem, StartEd Accelerator, Quake Capital

In a classic “but wait, there’s more” moment, don’t forget to sign up for these other webinars exclusively for Digital Startup Alley exhibitors.

All of this happens before the full week of Disrupt (starting September 14th). That’s a ton of opportunity waiting for you. Don’t wait — buy your Digital Startup Alley Package now, join us for speed networking and get ready to accelerate your success.

Is your company interested in sponsoring or exhibiting at Disrupt 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico