Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

CommonGround, a startup developing technology for what its founders describe as “4D collaboration,” is announcing that it has raised $19 million in funding.

This isn’t the first time Amir Bassan-Eskenazi and Ran Oz have launched a startup together — they also founded video networking company BigBand Networks, which won two technology-related Emmy Awards, went public in 2007 and was acquired by Arris Group in 2011. Before that, they worked together at digital compression company Optibase, which Oz co-founded and where Bassan-Eskenazi served as COO.

Although CommonGround is still in stealth mode and doesn’t plan to fully unveil its first product until next year, Bassan-Eskenazi and Oz outlined their vision for me. They acknowledged that video conferencing has improved significantly, but said it still can’t match face-to-face communication.

“Some things you just cannot achieve through a flat video-conferencing-type solution,” Bassan-Eskenazi said. “Those got better over the years, but they never managed to achieve that thing where you walk into a bar … and there’s a group of people talking and you know immediately who is a little taken aback, who is excited, who is kind of ‘eh.’”

CommonGround founders Amir Bassan-Eskenazi and Ran Oz. Image Credits: CommonGround

That, essentially, is what Bassan-Eskenazi, Oz and their team are trying to build — online collaboration software that more fully captures the nuances of in-person communication, and actually improves on face-to-face conversations in some ways (hence the 4D moniker). Asked whether this involves combining video conferencing with other collaboration tools, Oz replied, “Think of it as beyond video,” using technology like computer vision and graphics.

Bassan-Eskenazi added that they’ve been working on CommonGround for more than year, so this isn’t just a response to our current stay-at-home environment. And the opportunity should still be massive as offices reopen next year.

“When we started this, it was a problem we thought some of the workforce would understand,” he said. “Now my mother understands it, because it’s how she reads to the grandkids.”

As for the funding, the round was led by Matrix Partners, with participation from Grove Ventures and StageOne Ventures.

“Amir and Ran have a bold vision to reinvent communications,” said Matrix General Partner Patrick Malatack in a statement. “Their technical expertise, combined with a history of successful exits, made for an easy investment decision.”

Powered by WPeMatico

The Exchange is taking a break from vacation to dig into the new Qualtrics S-1 filing. Then the column and newsletter are back on hold until January 4.

This afternoon, Qualtrics, a software company that helps companies poll their employee base, customers and others, filed to go public. It’s the second time that the Utah-based unicorn has done so, failing the first time to complete its offering after SAP swooped in and bought it for around $8 billion in cash.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SAP announced in late July of this year that Qualtrics would be spun out via an IPO, bringing the smaller company’s saga full-circle.

The new S-1 filing — you can view the 2018 original here — is a different animal from the first. First, Qualtrics is larger than it was, and older. And its financials are more complex as it extricates itself from its soon-to-be-erstwhile corporate parent.

The new S-1 filing — you can view the 2018 original here — is a different animal from the first. First, Qualtrics is larger than it was, and older. And its financials are more complex as it extricates itself from its soon-to-be-erstwhile corporate parent.

Qualtrics intends to list on the Nasdaq under the ticker symbol “XM.”

Looking back at my chat with Ryan Smith, then Qualtrics CEO and today its chairman, and Bill McDermott, then SAP’s CEO and today the CEO of ServiceNow, it’s hard to believe that the acquisition deal was only two years ago.

Much has changed since late 2018. Let’s see what happened to Qualtrics in the meantime. We’ll dig into the financials, the company’s implied valuation range (spoiler: It has gone up) and whatever else we can shake loose.

A few things up top. First, SAP will be the company’s controlling shareholder after the Qualtrics’ IPO. That’s early in the S-1 filing. And, Smith and Silver Lake are investing in the company as part of its new debut.

Powered by WPeMatico

Global investors are running from Chinese tech stocks in the wake of the government’s crackdown on Ant Group and Alibaba, two high-flying businesses founded by Ma Yun (Jack Ma) that were once hailed as paragons of China’s new tech elite.

Shares of major technology companies in the country have fallen sharply in recent days, with Bloomberg calculating that Alibaba, Tencent, JD.com and Meituan have lost around $200 billion in value during a handful of trading sessions.

Already reeling from the last-minute halt of the public debut of Ant Group, a major Chinese fintech player with deep ties to Alibaba, the e-commerce giant came under new fire, as China’s markets watchdog opened a probe into its business practices concerning potentially anticompetitive behavior.

Ant Group was itself summoned by the government on December 26, leading to a plan that will force the company to “rectify” its business practices.

Shares of Alibaba are off around 30% from their recent record highs set in late October. Tech shares are also off in the country more broadly, with one Chinese-technology-focused ETC falling around 8% from recent highs, including a 1.5% drop today.

The American Depositary Receipts used by traders to invest in Alibaba fell from around $256 per share at the close of Wednesday trading on the New York Stock Exchange to around $222 last Thursday. The company is down another half point today. It was worth more than $319 per share earlier in the quarter.

It’s clear that the rising tensions between China’s tech giants and the country’s ruling Communist Party have investors spooked. But Jack Ma’s relationship with the Chinese government has always been a bit more fraught than that of his peers. Ma Huateng (Pony Ma), the founder of Tencent, and Xu Yong (Eric Yong) and Li Yanhong (Robin Li), the co-founders of Baidu, have kept lower profiles than the Alibaba founder.

Bloomberg has a good synopsis of the state of the market right now. The companies that are most directly in the crosshairs appear to be Ma Yun’s, but at different times, Tencent has been the focus of Chinese regulators bent on curbing the company’s influence through gaming.

Specifically for Alibaba things have gone from bad to worse, and a boosted share buyback program was not enough to halt the bleeding.

Whether this new round of regulations is a solitary blip on the radar or the signal of an increasing interest in Beijing tying tech companies closer to national interests remains to be seen. As the tit-for-tat tech conflict between the U.S. and China continues, many companies that had seen their growth as apolitical may become caught in the diplomatic crossfire.

Other tech companies are seeing their fortunes rise, boosted by newfound interest from the central government in Beijing.

This is already apparent in the chip industry, where China’s push for self-reliance has brought new riches and capital for new businesses. It’s true for Liu FengFeng, whose company, Tsinghon, was able to raise $5 million for its attempt at building a new semiconductor manufacturer in the country. Intellifusion, a manufacturer of chipsets focused on machine learning applications, was able to raise another $141 million back in April.

Private investors may be less enthused at the prospect of backing Chinese tech upstarts who could face government censure should the regulatory winds shift. Whether other startup markets in the region — India, Japan, among others — will benefit from the Chinese regulatory barrage will be interesting to track in 2021.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and don’t forget to check out the first of our two holiday eps, the last one talking to VCs about what surprised them in 2020.

Anyhoo, from vacation, here’s what Chris and I got up to:

Tune in Thursday for one more fun episode, and then we’re back to regular programming the week after!

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

During my five years with Global Founders Capital, Rocket Internet’s $1 billion VC arm, I saw more than a hundred of Rocket’s incubated companies attempt to internationalize. For background, Rocket Internet has helped launch some very successful businesses internationally, including HelloFresh ($12.9 billion market cap), Lazada ($1 billion exit to Alibaba), Jumia ($3.2 billion market cap), Zalando ($21.2 billion market cap) and many others. Rocket often followed the Blitzscaling model popularized by Reid Hoffman — earning them an appearance in his book of the same name.

After an initial success helping Groupon scale internationally via a merger with Rocket’s incubation firm CityDeal, Rocket’s team have aggressively scaled businesses from Algeria to Zimbabwe — sometimes in a matter of weeks. No surprise, Rocket also has a graveyard of failed companies that were victims of bad internationalization efforts.

Many companies make the costly mistake of launching abroad too soon.

My personal observations on Rocket’s successes and failures start with this crucial point: These learnings might not apply to your unique combination business model, market and timing. No matter how well you prepare and plan your internationalization, in the end you need to be agile, alert and smart as you dip your toes into your first foreign market.

Internationalization can be a big driver of growth and consequently enterprise value, which is why investors always push for it. But going abroad can also destroy value just as quickly. As a founder, it’s your job to manage financial and operational risks. Finding the right balance between keeping costs in check and not underinvesting can mean doing things more slowly than your board would like. For example, you might launch new markets sequentially instead of rolling 10 out at the same time.

Adopt a “hire slow, fire fast” mentality for your expansion strategy. Don’t be afraid to pull the plug if things don’t work out.

Our team at Heartcore Capital use the following framework and learnings to guide internationalization strategies for our portfolio companies. A successful internationalization strategy needs to answer and address the “Four Ws”: When, Where, Which and With whom to internationalize. (Regarding the fifth W from journalism, you should not need to ask the “Why” question if you want to build a large business!)

Many companies make the costly mistake of launching abroad too soon. They look at internationalization as a detached function, isolated from the rest of the business and then launch their second market prematurely. Follow this simple rule: Wait to internationalize until you hit product/market fit.

How do you know exactly when you’ve reached product/market fit? According to Marc Andreessen, “Product/market fit means being in a good market with a product that can satisfy that market.” He adds that experienced entrepreneurs can usually feel if they’ve reached this point.

Let’s take the man for his word and move on to the actual argument: Until you have product/market fit, you will not be able to distinguish between what you’ve learned from your business model and what you’ve learned from your in-country experience. Mistakes will compound. Complexities and costs will multiply. I contend that insufficient understanding of their business and operating model is the main reason why companies fail with their expansion strategies.

Founders should also consider the underlying costs of internationalizing before they decide to expand (more about this in the “What” section below). Some companies are global by default — think mobile gaming companies — or simply require language localization. Others need to build new warehouses, hire local teams or build entirely new products. The costs and respective risks of expanding prematurely depend heavily on the business model.

There are edge cases where companies need to move quickly to internationalize for strategic reasons — despite uncertainty about their market fit. For instance, companies like Groupon or those engaged in food delivery face winner-takes-most markets, where opportunities for product differentiation are limited. “Blitzscaling” makes sense in cases like these.

However, you should tread carefully if your only reason to start scaling abroad is a large fundraise or to match a competitor’s internationalization efforts. Scaling prematurely for the wrong reasons might just cost you your entire company.

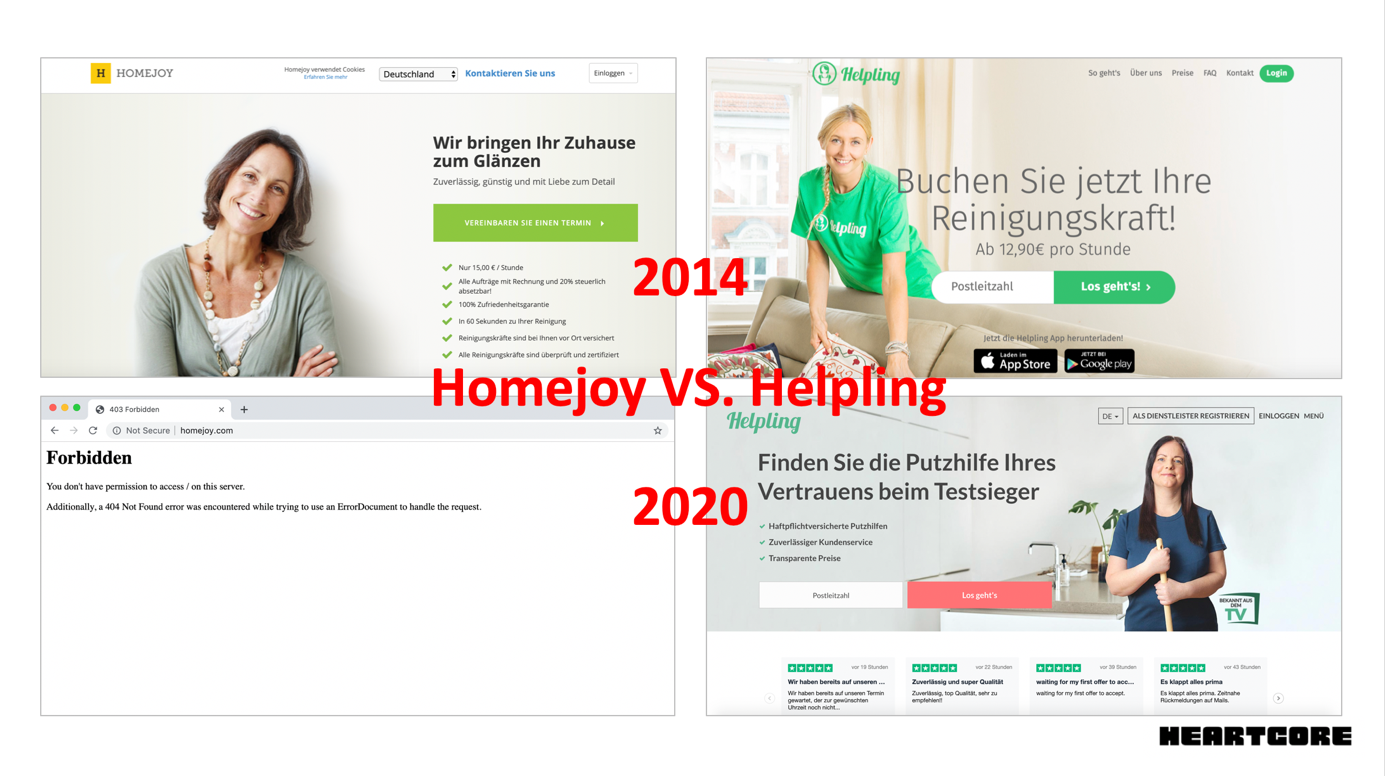

When Rocket Internet announced it would launch the Homejoy model into European markets with Helpling, the American “original” company launched quickly in Germany in an effort to squash their new competitor. In the early days of “on-demand everything,” a managed marketplace for cleaning services sounded like the next unicorn in the making.

In 2013, Homejoy had a fresh $24 million Series A from Google Ventures and First Round — considered a huge round at a time when Instacart had just raised an $8 million Series A and Snapchat had done a $13 million Series A round. It must have seemed like a good idea to squash the German competition early.

As it turned out, Homejoy’s product was not yet ready to scale internationally. Just 13 months after launching in Germany, Homejoy had to cease operations globally, while Rocket’s Helpling is still alive and kicking. Helpling focused carefully on product, automation and making their unit economics work. A rush to crush an international competitor caused the demise of a would-be unicorn.

Homejoy expanded internationally in 2014 in a rush to squash a new German competitor Helpling. Their websites in 2020 show starkly different outcomes. Image Credits: Homejoy/Helpling

When deciding which new international market to tackle, it is vital to do your homework. Analyze the competitive environment, partner availability, infrastructure, culture, regulation and synergies with your home market.

In the early days of e-commerce, it was rather easy to analyze if a market was an expansion target. In the absence of professional competition, Rocket chose new countries based solely on GDP and internet penetration.

Powered by WPeMatico

The rivalry between China’s top online learning apps has become even more intense this year because of the COVID-19 pandemic. The latest company to score a significant funding round is Zuoyebang, which announced today (link in Chinese) that it has raised a $1.6 billion Series E+ from investors including Alibaba Group. Other participants included returning investors Tiger Global Management, SoftBank Vision Fund, Sequoia Capital China and FountainVest Partners.

Zuoyebang’s latest announcement comes just six months after it announced a $750 million Series E led by Tiger Global and FountainVest. The latest financing brings Zuoyebang’s total raised so far to $2.93 billion. The company did not disclose its latest worth, but Reuters reported in September that it was raising at a $10 billion valuation.

One of Zuoyebang’s main competitors is Yuanfudao, which announced in October that it had reached a $15.5 billion valuation after closing a $2.2 billion round led by Tencent. This pushed Yuanfudao ahead of Byju as the world’s most valuable edtech company. Another popular online learning app in China is Yiqizuoye, which is backed by Singapore’s Temasek.

Zuoyebang offers online courses, live lessons and homework help for kindergarten to 12th grade students, and claims about 170 million monthly active users, about 50 million of whom use the service each day. In comparison, there were about 200 million K-12 students in 2019 in China, according to the Ministry of Education (link in Chinese).

In fall 2020, the total number of students in Zuoyebang’s paid livestream classes reached more than 10 million, setting an industry record, the company claims. While a lot of the growth was driven by the pandemic, Zuoyebang founder Hou Jianbin said in the company’s funding announcement that it expects online education to continue growing in the longer term, and will invest in K-12 classes and expand its product categories.

Powered by WPeMatico

As the year draws to a close, a few members of our edit staff shared stories that defined the last 12 months for their beat.

Devin Coldewey: Technology played a pivotal role in the coverage of protests against police violence over the summer. Disinformation and discord spread like wildfire on social media, but so did important information and documentation of brutality, often via the newly popular medium of live streaming.

Kirsten Korosec: Uber evolved from a company trying to cover everything in transportation to one focused on ride-hailing and delivery as it aims for profitability in 2021. To get there, Uber offloaded its micromobility unit Jump, its self-driving subsidiary Uber ATG and air taxi moonshot Uber Elevate.

Powered by WPeMatico

The end of the year is looming and with it one of your most important tasks as a manager. Summarizing the performance of 10, 20 or 50 developers over the past 12 months, offering personalized advice and having the facts to back it up — is no small task.

We believe that the only unbiased, accurate and insightful way to understand how your developers are working, progressing and — last but definitely not least — how they’re feeling, is with data. Data can provide more objective insights into employee activity than could ever be gathered by a human.

It’s still very hard for many managers to fully understand that all employees work at different paces and levels.

Consider this: Over two-thirds of employees say they would put more effort into their work if they felt more appreciated, and 90% want a manager who’s fair to all employees.

Let’s be honest. It’s hard to judge all of your employees fairly if you’re (1) unable to work physically side-by-side with them, meaning you’ll inevitably have more contact with the some over others (e.g., those you’re more friendly with); and (2) you’re relying on manual trackers to keep on top of everyone’s work, which can get lost and take a lot of effort to process and analyze; (3) you expect engineers to self-report their progress, which is far from objective.

It’s also unlikely, especially with the quieter ones, that on top of all that you’ll have identified areas for them to expand their talents by upskilling or reskilling. But it’s that kind of personal attention that will make employees feel appreciated and able to progress professionally with you. Absent that, they’re likely to take the next best job opportunity that shows up.

So here’s a run down of why you need data to set up a fair annual review process; if not this year, then you can kick-start it for 2021.

The best way to track your developers’ progress automatically is by using Git Analytics tools, which track the performance of individuals by aggregating historical Git data and then feeding that information back to managers in minute detail.

This data will clearly show you if one of your engineers is over capacity or underworked and the types of projects they excel in. If you’re assessing an engineering manager and the team members they’re responsible for have been taking longer to push their code to the shared repository, causing a backlog of tasks, it may mean that they’re not delegating tasks properly. An appropriate goal here would be to track and divide their team’s responsibilities more efficiently, which can be tracked using the same metrics, or cross-training members of other teams to assist with their tasks.

Another example is that of an engineer who is dipping their toe into multiple projects. Indicators of where they’ve performed best include churn (we’ll get to that later), coworkers repeatedly asking that same employee to assist them in new tasks and of course positive feedback for senior staff, which can easily be integrated into Git analytics tools. These are clear signs that next year, your engineer could be maximizing their talents in these alternative areas, and you could diversify their tasks accordingly.

Once you know what targets to set, you can use analytics tools to create automatic targets for each engineer. That means that after you’ve set it up, it will be updated regularly on the engineer’s progress using indicators directly from the code repository. It won’t need time-consuming input from either you or your employee, allowing you both to focus on more important tasks. As a manager you’ll receive full reports once the deadline of the task is reached and get notified whenever metrics start dropping or the goal has been met.

This is important — you’ll be able to keep on top of those goals yourself, without having to delegate that responsibility or depend on self-reporting by the engineer. It will keep employee monitoring honest and transparent.

The easiest way for managers to “conclude” how an engineer has performed is by looking at superficial output: the number of completed pull requests submitted per week, the number of commits per day, etc. Especially for nontechnical managers, this is a grave but common error. When something is done, it doesn’t mean it’s been done well or that it is even productive or usable.

Instead, look at these data points to determine the actual quality of your engineer’s work:

Powered by WPeMatico

As the United States entered its first wave of COVID-19 lockdowns, there were wide expectations in startup land that a reckoning had arrived. But the expected comeuppance of high-burn, high-growth startups fueled by cheap capital provided by venture capitalists raising ever-larger funds, failed to arrive.

Instead, the very opposite came to pass.

Layoffs happened swiftly and aggressively during the early months of the pandemic era. But by the middle of Q2, venture activity had warmed and third quarter dealmaking felt swift and competitive, with some investors describing it as the hottest summer in recent years.

Venture capital as an asset class has survived the pandemic’s stress test.

But somewhat lost amongst the splashy megarounds and high-interest IPOs that can dominate the news cycle were seed-stage startups. The raw little companies that represent the grist that will shape itself into the next set of giants.

TechCrunch explored what happened in seed investing to uncover what was missed amidst the storm and fury of late-stage startup activity. According to a TechCrunch analysis of PitchBook data and a survey of venture capitalists, a few trends became clear.

First, the pattern of rising seed-check sizes seen in prior years continued despite the tumultuous business climate. Second, more expensive and larger seed deals were not only caused by excessive capital present in the private markets. Instead, COVID-19 shook up which startups were considered attractive by private investors. And the changeup did not necessarily raise their number.

Let’s dig into the data and see what it can teach us about this wild year. Then we’ll hear from Eniac Ventures’ Nihal Mehta, Freestyle’s Jenny Lefcourt, Pear VC’s Mar Hershenson and Contrary Capital’s Eric Tarczynski about what they saw in 2020 while writing a chunk of the checks that our data encompasses.

If you didn’t think much about seed in 2020, you’re not alone. Late, huge rounds consumed most of the media’s oxygen, leaving smaller startups to compete for scraps of attention. There was so much late-stage activity — around 90 $100 million or larger rounds in Q3, for example — it was difficult for smaller investments to command attention.

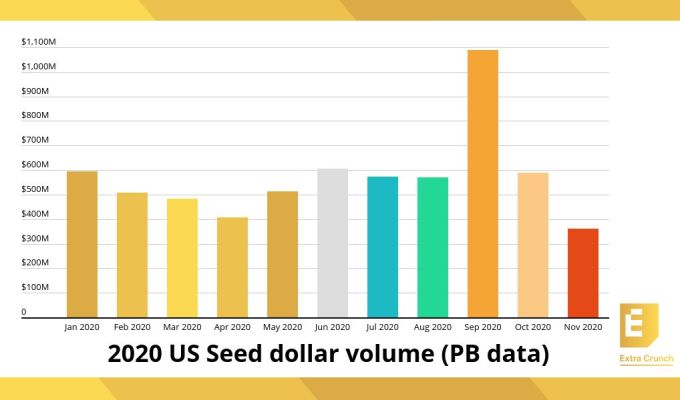

But despite living in the background, the dollars invested into seed-stage startups in the United States had an up-and-down year that was fascinating:

Image Credits: PitchBook

Seed dollar volume fell as Q1 progressed, reaching a 2020 nadir in April, the start of Q2. But as May arrived, the pace at which investors put money into seed-stage startups accelerated, recovering to January levels — which is to say, pre-pandemic — by June. The COVID dip, for seed, then, was a short-term affair.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

Today is our holiday look-back at the year, bringing not only our own Danny and Natasha and Chris and Alex into the mix, but also five venture capitalists who we got to leave us their notes as well. The goal for this episode was to reflect on a year that no one could have ever predicted, but with a specific angle, as always, on venture capital and startups.

We asked about the biggest surprise, non-portfolio companies to watch, and trends they got wrong and right. There was also banter on Zoom investing (Alex came up with Zesting, but we’re taking suggestions if anyone comes up with a better moniker) and startup pricing.

Here’s who we asked to call into our super Fancy Equity Hotline:

Thanks to them all for participating, and of course you, our dear Equity listeners, for a blockbuster year for the podcast.

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico