Enterprise

Auto Added by WPeMatico

Auto Added by WPeMatico

Applications based on artificial intelligence — whether they are systems running autonomous services, platforms being used in drug development or to predict the spread of a virus, traffic management for 5G networks or something else altogether — require an unprecedented amount of computing power to run. And today, one of the big names in the world of designing and building processors fit for the task has closed a major round of funding as it takes its business to the next level.

Graphcore, the Bristol, U.K.-based AI chipmaker, has raised $222 million, a Series E that CEO and co-founder Nigel Toon said in an interview will be used for a couple of key purposes.

First, Graphcore will use the money to continue expanding its technology, based around an architecture it calls “IPU” (intelligence processing unit), which competes against chips from the likes of Nvidia and Intel also optimized for AI applications. And second, Graphcore will use the funding to shore up its finances ahead of a possible public listing.

The funding, Toon said, gives Graphcore $440 million in cash on the balance sheet and a post-money, $2.77 billion valuation to start 2021.

“We’re in a strong position to double down and grow fast and take advantage of the opportunity in front of us,” he added. He said it could be “premature” to describe this Series E as a “pre-IPO” round. “We have enough cash and this puts us in a position to take that next step,” he added. The company has in recent weeks been rumored to be eyeing up a listing not in the U.K. but on Nasdaq in the U.S.

This latest round of funding is coming from a roster of financial investors. Led by the Ontario Teachers’ Pension Plan, it also includes participation from Fidelity International and Schroders, as well as previous investors Baillie Gifford and Draper Esprit. Graphcore has now raised some $710 million to date.

This Series E gives Graphcore a definite step up in its valuation — the company last raised money back in February of this year, a $150 million extension to its Series D that valued the company at $1.95 billion — but all the same, it closes off what Toon described as a “challenging” year for the company (and indeed, the world at large).

“I view this year as a speed bump,” he said. “It has been challenging and we’ve realigned to speed things up.”

As it has been for many companies, the year came in different parts.

On one side, Graphcore’s hardware and software product development continued apace with ever-faster processors in ever-smaller packages. In July, Graphcore launched the second generation of its flagship chip, the GC200, and a new IPU Machine that runs on it, the M2000, which the company described at the time as the first AI computer to achieve a petaflop of processing power “in the size of a pizza box.”

But on the other side, the building and launch of those products was largely done with a remote workforce, with employees sent to work from home to help slow down the spread of the coronavirus that has gripped the world and rewritten how much of it operates.

Indeed, the industry at large, and how companies are spending and investing during a period of uncertainty, has also likely shifted. Some companies like Amazon, Apple and Google are all getting more serious about their own chipmaking efforts. Others are caught up in a wave of consolidation: Witness Nvidia’s efforts to acquire ARM in a $40 billion deal.

All of these spell challenges for an upstart like Graphcore. Toon said Graphcore doesn’t have any plans to make acquisitions: Its strategy is based around organic growth.

And, no great surprises here, he is not excited about Nvidia’s acquisition of ARM: “If we’re not careful, things will consolidate too much and that could kill off innovation,” he said. “We have made our position clear to the U.K. government. We don’t think the Nvidia ARM deal is a good thing.” (Somewhat ironic, considering he and Graphcore co-founder Simon Knowles sold a previous startup to none other than Nvidia.)

He also declined to talk about new customers for Graphcore, but he said that there has been interest from financial services companies, and some from the world of healthcare, automotive and internet companies, “large hyperscalers” in his words, that require the kind of technology that Graphcore is building either to run their systems, or to complement processors that they are potentially also building themselves. (Strategic backers of the company include the likes of Microsoft, BMW, Bosch and Dell.)

Graphcore said that the company is shipping its newest products “in production volume” to customers, and Toon said that a couple of big names are likely to be announced in the coming year, one that some believe might actually be calmer overall for the chip industry compared to 2020.

It’s that pull of technology, and specifically the processing demands of the next generation of computing, that investors believe will continue to drive business to Graphcore as the dust settles on this year.

“The market for purpose-built AI processors is expected to be significant in the coming years because of computing megatrends like cloud technology and 5G and increased AI adoption, and we believe Graphcore is poised to be a leader in this space,” said Olivia Steedman, senior managing director, Teachers’ Innovation Platform (TIP) at Ontario Teachers’. “TIP focuses on investing in tech-enabled businesses like Graphcore that are at the forefront of innovation in their sector. We are excited to partner with Nigel and the strong management team to support the company’s continued growth and product development.”

Powered by WPeMatico

When we examine any year in enterprise M&A, it’s tempting to highlight the biggest, gaudiest deals — and there were plenty of those in 2020. I’ve written about 34 acquisitions so far this year. Of those, 15 were worth $1 billion or more, 12 were small enough to not require that the companies disclose the price and the remainder fell somewhere in between.

Four deals involving chip companies coming together totaled over $100 billion on their own. While nobody does eye-popping M&A quite like the chip industry, other sectors also offered their own eyebrow-raising deals, led by Salesforce buying Slack earlier this month for $27.7 billion.

We are likely to see more industries consolidate the way chips did in 2020, albeit probably not quite as dramatically or expensively.

Yet in spite of the drama of these larger numbers, the most interesting targets to me were the pandemic-driven smaller deals that started popping up in May. Those small acquisitions are the ones that are so insignificant that the company doesn’t have to share the purchase price publicly. They usually involve early-stage companies being absorbed by cash-rich concerns looking for some combination of missing technology or engineering talent in a particular area like security or artificial intelligence.

It was certainly an active year in M&A, and we still might not have seen the last of it. Let’s have a look at why those minor deals were so interesting and how they compared with larger ones, while looking ahead to what 2021 M&A might look like.

It’s always hard to know exactly why an early-stage startup would give up its independence by selling to a larger entity, but we can certainly speculate on some of the reasons why this year’s rapid-fire dealing started in May. While we can never know for certain why these companies decided to exit via acquisition, we know that in April, the pandemic hit full force in the United States and the economy began to shut down.

Some startups were particularly vulnerable, especially companies low on cash in the April timeframe. Obviously companies fail when they run out of funding, and we started seeing early-stage startups being scooped up the following month.

We don’t know for sure of course if there is a direct correlation between April’s economic woes and the flurry of deals that started in May, but we can reasonably speculate that there was. For some percentage of them, I’m guessing it was a fire sale or at least a deal made under less than ideal terms. For others, maybe they simply didn’t have the wherewithal to keep going under such adverse economic conditions or the partnerships were just too good to pass up.

It’s worth noting that I didn’t cover any deals in April. But, beginning on May 7, Zoom bought Keybase for its encryption expertise; five days later Atlassian bought Halp for Slack integration; and the day after that VMware bought cloud native security startup Octarine — and we were off and running. Granted the big companies benefited from making these acquisitions, but the timing stood out.

Powered by WPeMatico

AWS, Amazon’s flourishing cloud arm, has been growing at a rapid clip for more than a decade. An early public cloud infrastructure vendor, it has taken advantage of first-to-market status to become the most successful player in the space. In fact, one could argue that many of today’s startups wouldn’t have gotten off the ground without the formation of cloud companies like AWS giving them easy access to infrastructure without having to build it themselves.

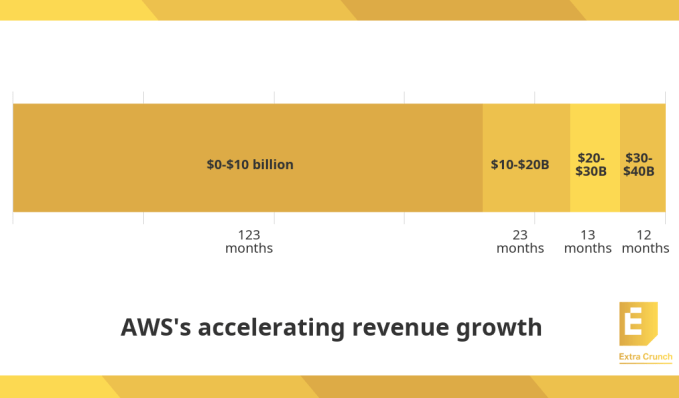

In Amazon’s most-recent earnings report, AWS generated revenues of $11.6 billion, good for a run rate of more than $46 billion. That makes the next AWS milestone a run rate of $50 billion, something that could be in reach in less than two quarters if it continues its pace of revenue growth.

The good news for competing companies is that in spite of the market size and relative maturity, there is still plenty of room to grow.

While the cloud division’s growth is slowing in percentage terms as it comes firmly up against the law of large numbers in which AWS has to grow every quarter compared to an ever-larger revenue base. The result of this dynamic is that while AWS’ year-over-year growth rate is slowing over time — from 35% in Q3 2019 to 29% in Q3 2020 — the pace at which it is adding $10 billion chunks of annual revenue run rate is accelerating.

At the AWS re:Invent customer conference this year, AWS CEO Andy Jassy talked about the pace of change over the years, saying that it took the following number of months to grow its run rate by $10 billion increments:

Image Credits: TechCrunch (data from AWS)

Extrapolating from the above trend, it should take AWS fewer than 12 months to scale from a run rate of $40 billion to $50 billion. Stating the obvious, Jassy said “the rate of growth in AWS continues to accelerate.” He also took the time to point out that AWS is now the fifth-largest enterprise IT company in the world, ahead of enterprise stalwarts like SAP and Oracle.

What’s amazing is that AWS achieved its scale so fast, not even existing until 2006. That growth rate makes us ask a question: Can anyone hope to stop AWS’ momentum?

The short answer is that it doesn’t appear likely.

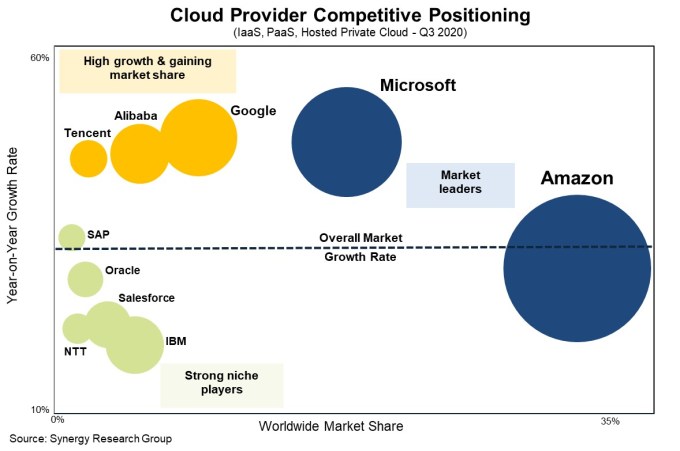

A good place to start is surveying the cloud infrastructure competitive landscape to see if there are any cloud companies that could catch the market leader. According to Synergy Research, AWS remains firmly in front, and it doesn’t look like any competitor could catch AWS anytime soon unless some market dynamic caused a drastic change.

Image Credits: Synergy Research

With around a third of the market, AWS is the clear front-runner. Its closest and fiercest rival Microsoft has around 20%. To put that into perspective a bit, last quarter AWS had $11.6 billion in revenue compared to Microsoft’s $5.2 billion Azure result. While Microsoft’s equivalent cloud number is growing faster at 47%, like AWS, that number has begun to drop steadily while it gains market share and higher revenue and it falls victim to that same law of large numbers.

Powered by WPeMatico

IAC announced today that it plans to turn Vimeo into an independent, publicly traded company.

Last month, IAC CEO Joey Levin wrote a letter to shareholders in which he said the holding company had “begun contemplating spinning Vimeo off to our shareholders.” It sounds like the company has moved beyond the contemplation phase, with plans that will be submitted for stockholder approval in the first quarter of 2021, and the actual spin off happening in Q2.

“The combination of Vimeo’s remarkable growth, solid leadership position and enormous market opportunity have made clear its future,” Levin said in a statement today. “It’s time for Vimeo to spread its wings and become a great independent public company.”

While Vimeo once competed with YouTube as a consumer video destination, its strategy has shifted in recent years to providing video tools for businesses. In November, the company said it had 1.5 million paying subscribers and 3,500 enterprise clients — and that its most recent quarter was with positive EBITDA, plus year-over-year revenue growth of 44%.

The announcement notes that this is the eleventh company that IAC has spun off, a process in which it distributes its ownership stake to IAC shareholders. (Match Group completed its separation from IAC over the summer.)

“Today we have a rare opportunity to help every team and organization in the world integrate video throughout their operations, across all the ways they communicate and collaborate,” said Vimeo CEO Anjali Sud in a statement. “Our all-in-one solution radically lowers the barriers of time, cost and complexity that previously made professional-quality video unattainable. We’re ready for this next chapter and focused on making video far easier and more effective than ever before.”

Powered by WPeMatico

StepZen, a new startup from the crew who gave you Apigee (which was sold to Google in 2016 for $625 million) had a different vision for their latest company. They are building a single API that pulls data from disparate sources to help developers deliver more complex customer experiences online.

Today, the startup emerged from stealth and announced an $8 million seed investment from Neotribe Ventures and Wing Venture Capital .

With years of experience working with APIs, the founders wanted to take that a step further, says CEO and co-founder Anant Jhingran. “StepZen is a product that lets front end developers easily create and consume one API for all the data they need from the back end,” he explained.

This is all in the service of providing a smoother, more consistent customer experience. That means whether you are on an e-commerce site accessing your order history or a banking app grabbing your current balance, these scenarios require pulling data from various back-end data resources. Connecting to those resources is a time-consuming task, and StepZen wants to simplify that for developers.

“Developers spend an enormous amount of time deploying and managing code that accesses the back end, and what StepZen wants to do is to give them that time back,” he said.

Instead of manually writing code to pull this data, StepZen enables developers to simply provide configuration information and credentials to connect to these back-end data sources, and then it builds a single API that handles all of the heavy lifting of pulling that data and presenting it when needed.

Jhingran uses the example of presenting a list of open orders for a customer. It sounds simple enough, but once you consider that the data could live in several places, including the CRM system, the order system or with your courier, that means accessing at least three separate and highly disparate systems. StepZen will help pull this all together via its API and present it smoothly to the user.

Today the company has 11 employees, including the three founders, with plans to add another eight or so in 2021. As they do that, CBO and co-founder Helen Whelan says they are working to build a diverse and inclusive company. While the founding team is itself diverse, they want to hire employees with diverse backgrounds and ways of thinking to build the most complete product and company.

“For the first 10 or so employees, we tapped into the networks of the people who we’ve worked with, people who you know can do a great job. Then I think it’s about deliberately expanding from there and deliberately taking the time that you need to explore and expand your pipeline of candidates,” she said.

The company is just nine months old and has been spending most of this year building the solution and working with pre-alpha users. Today the product is in alpha, with plans to release it as a software service early next year.

As the company emerges from stealth, it’s looking to continue building the product and looking for ways to remove as much complexity as possible. “We know how to do the hard things on the back end. We’ve got the database technologies and the API technologies down, and it’s now about finding how to make all of that simple on the outside and easy for developers to use, ” Whelan said.

Powered by WPeMatico

IBM has been busy since it announced plans to spin out its legacy infrastructure management business in October, placing an all-in bet on the hybrid cloud. Today, it built on that bet by acquiring Helsinki-based multi-cloud consulting firm Nordcloud. The companies did not share the purchase price.

Nordcloud fits neatly into this strategy with 500 consultants certified in AWS, Azure and Google Cloud Platform, giving the company a trained staff of experts to help as they move away from an IBM -centric solution to choosing to work with the customer however they wish to implement their cloud strategy.

This hybrid approach harkens back to the $34 billion Red Hat acquisition in 2018, which is really the lynchpin for this approach, as CEO Arvind Krishna told CNBC’s Jon Fortt in an interview last month. Krishna is in the midst of trying to completely transform his organization, and acquisitions like this are meant to speed up that process:

The Red Hat acquisition gave us the technology base on which to build a hybrid cloud technology platform based on open-source, and based on giving choice to our clients as they embark on this journey. With the success of that acquisition now giving us the fuel, we can then take the next step, and the larger step, of taking the managed infrastructure services out. So the rest of the company can be absolutely focused on hybrid cloud and artificial intelligence.

John Granger, senior vice president for cloud application innovation and COO for IBM Global Business Services, says that IBM’s customers are increasingly looking for help managing resources across multiple vendors, as well as on premises.

“IBM’s acquisition of Nordcloud adds the kind of deep expertise that will drive our clients’ digital transformations as well as support the further adoption of IBM’s hybrid cloud platform. Nordcloud’s cloud-native tools, methodologies and talent send a strong signal that IBM is committed to deliver our clients’ successful journey to cloud,” Granger said in a statement.

After the deal closes, which is expected in the first quarter next year subject to typical regulatory approvals, Nordcloud will become an IBM company and operate to help continue this strategy.

It’s worth noting that this deal comes on the heels several other small recent deals, including acquiring Expertus last week and Truqua and Instana last month. These three companies provide expertise in digital payments, SAP consulting and hybrid cloud applications performance monitoring, respectively.

Nordcloud, which is based in Helsinki with offices in Amsterdam, was founded in 2011 and has raised more than $26 million, according to PitchBook data.

Powered by WPeMatico

The busy year in M&A continued this weekend when private equity firm Thoma Bravo announced it was acquiring RealPage for $10.2 billion.

In RealPage, Thoma Bravo is getting a full-service property management platform with services like renter portals, site management, expense management and financial analysis for building and property owners. Orlando Bravo, founder and a managing partner of Thoma Bravo, sees a company that they can work with and build on its previous track record.

“RealPage’s industry leading platform is critical to the real estate ecosystem and has tremendous potential going forward,” Bravo said in a statement.

As for RealPage, company CEO Steve Winn, who will remain with the company, sees the deal as a big win for stock holders, while giving them the ability to keep investing in the product. “This will enhance our ability to focus on executing our long-term strategy and delivering even better products and services to our clients and partners,” Winn said in a statement.

RealPage, which was founded in 1998 and went public in 2010, is a typical kind of mature platform that a private equity firm like Thoma Bravo is attracted to. It has a strong customer base with more than 12,000 customers, and respectable revenue, growing at a modest pace. In its most recent earnings statement, the company announced $298.1 million in revenue, up 17% year over year. That puts it on a run rate of more than $1 billion.

Under the terms of the deal, Thoma Bravo will pay RealPage stockholders $88.75 in cash per share. That is a premium of more 30% over the $67.83 closing price on December 18th. The transaction is subject to standard regulatory review, and the RealPage board will have a 45-day “go shop” window to see if it can find a better price. Given the premium pricing on this deal, that isn’t likely, but it will have the opportunity to try.

Powered by WPeMatico

OneTrust, the four-year-old privacy platform startup from the folks who brought you AirWatch (which was acquired by VMmare for $1.5 billion in 2014), announced a $300 million Series C on an impressive $5.1 billion valuation today.

The company has attracted considerable attention from investors in a remarkably short time. It came out of the box with a $200 million Series A on a $1.3 billion valuation in July 2019. Those are not typical A round numbers, but this has never been a typical startup. The Series B was more of the same — $210 million on a $2.7 billion valuation this past February.

That brings us to today’s Series C. Consider that the company has almost doubled its valuation again, and has raised $710 million in a mere 18 months, some of it during a pandemic. TCV led today’s round joining existing investors Insight Partners and Coatue.

So what are they doing to attract all this cash? In a world where privacy laws like GDPR and CCPA are already in play, with others in the works in the U.S. and around the world, companies need to be sure they are compliant with local laws wherever they operate. That’s where OneTrust comes in.

“We help companies ensure that they can be trusted, and that they make sure that they’re compliant to all laws around privacy, trust and risk,” OneTrust Chairman Alan Dabbiere told me.

That involves a suite of products that the company has already built or acquired, moving very quickly to offer a privacy platform to cover all aspects of a customer’s privacy requirements, including privacy management, discovery, third-party risk assessment, risk management, ethics and compliance and consent management.

The company has already attracted 7,500 customers to the platform — and is adding1,000 additional customers per quarter. Dabbiere says that the products are helping them be compliant without adding a lot of friction to the building or buying process. “The goal is that we don’t slow the process down, we speed it up. And there’s a new philosophy called privacy by design,” he said. That means building privacy transparency into products, while making sure they are compliant with all of the legal and regulatory requirements.

The startup hasn’t been shy about using its investments to buy pieces of the platform, having made four acquisitions already in just four years since it was founded. It already has 1,500 employees and plans to add around 900 more in 2021.

As they build this workforce, Dabbiere says being based in a highly diverse city like Atlanta has helped in terms of building a diverse group of employees. “By finding the best employees and doing it in an area like Atlanta, we are finding the diversity comes naturally,” he said, adding, “We are thoughtful about it.” CEO Kabir Barday also launched a diversity, equity and inclusion council internally this past summer in response to the Black Lives Matter movement happening in the Atlanta community and around the country.

OneTrust had relied heavily on trade shows before the pandemic hit. In fact, Dabbiere says that they attended as many as 700 a year. When that avenue closed as the pandemic hit, they initially lowered their revenue guidance, but as they moved to digital channels along with their customers, they found that revenue didn’t drop as they expected.

He says that OneTrust has money in the bank from its prior investments, but they had reasons for taking on more cash now anyway. “The number one reason for doing this was the currency of our stock. We needed to revalue it for employees, for acquisitions, and the next steps of our growth,” he said.

Powered by WPeMatico

UiPath, the robotic process automation startup that has been growing like gangbusters, filed confidential paperwork with the SEC today ahead of a potential IPO.

“UiPath, Inc. today announced that it has submitted a draft registration statement on a confidential basis to the U.S. Securities and Exchange Commission (the “SEC”) for a proposed public offering of its Class A common stock. The number of shares of Class A common stock to be sold and the price range for the proposed offering have not yet been determined. UiPath intends to commence the public offering following completion of the SEC review process, subject to market and other conditions,” the company said in a statement.

The company has raised more than $1.2 billion from investors like Accel, CapitalG, Sequoia and others. Its biggest raise was $568 million led by Coatue on an impressive $7 billion valuation in April 2019. It raised another $225 million led by Alkeon Capital last July when its valuation soared to $10.2 billion.

At the time of the July raise, CEO and co-founder Daniel Dines did not shy away from the idea of an IPO, telling me:

We’re evaluating the market conditions and I wouldn’t say this to be vague, but we haven’t chosen a day that says on this day we’re going public. We’re really in the mindset that says we should be prepared when the market is ready, and I wouldn’t be surprised if that’s in the next 12-18 months.

This definitely falls within that window. RPA helps companies take highly repetitive manual tasks and automate them. So for example, it could pull a number from an invoice, fill in a number in a spreadsheet and send an email to accounts payable, all without a human touching it.

It is a technology that has great appeal right now because it enables companies to take advantage of automation without ripping and replacing their legacy systems. While the company has raised a ton of money, and seen its valuation take off, it will be interesting to see if it will get the same positive reception as companies like Airbnb, C3.ai and Snowflake.

Powered by WPeMatico

Businesses today feel, more than ever, the imperative to have flexible e-commerce strategies in place, able to connect with would-be customers wherever they might be. That market driver has now led to a significant growth round for a startup that is helping the larger of these businesses, including those targeting the B2B market, build out their digital sales operations with more agile, responsive e-commerce solutions.

Spryker, which provides a full suite of e-commerce tools for businesses — starting with a platform to bring a company’s inventory online, through to tools to analyse and measure how that inventory is selling and where, and then adding voice commerce, subscriptions, click & collect, IoT commerce and other new features and channels to improve the mix — has closed a round of $130 million.

It plans to use the funding to expand its own technology tools, as well as grow internationally. The company makes revenues in the mid-eight figures (so, around $50 million annually) and some 10% of its revenues currently come from the U.S. The plan will be to grow that business as part of its wider expansion, tackling a market for e-commerce software that is estimated to be worth some $7 billion annually.

The Series C was led by TCV — the storied investor that has backed giants like Facebook, Airbnb, Netflix, Spotify and Splunk, as well as interesting, up-and-coming e-commerce “plumbing” startups like Spryker, Relex and more. Previous backers One Peak and Project A Ventures also participated.

We understand that this latest funding values Berlin -based Spryker at more than $500 million.

Spryker today has around 150 customers, global businesses that run the gamut from recognised fashion brands through to companies that, as Boris Lokschin, who co-founded the company with Alexander Graf (the two share the title of co-CEOs) put it, are “hidden champions, leaders and brands you have never heard about doing things like selling silicone isolations for windows.” The roster includes Metro, Aldi Süd, Toyota and many others.

The plan will be to continue to support and grow its wider business building e-commerce tools for all kinds of larger companies, but in particular Spryker plans to use this tranche of funding to double down specifically on the B2B opportunity, building more agile e-commerce storefronts and in some cases also developing marketplaces around that.

One might assume that in the world of e-commerce, consumer-facing companies need to be the most dynamic and responsive, not least because they are facing a mass market and all the whims and competitive forces that might drive users to abandon shopping carts, look for better deals elsewhere or simply get distracted by the latest notification of a TikTok video or direct message.

For consumer-facing businesses, making sure they have the latest adtech, marketing tech and tools to improve discovery and conversion is a must.

It turns out that business-facing businesses are no less immune to their own set of customer distractions and challenges — particularly in the current market, buffeted as it is by the global health pandemic and its economic reverberations. They, too, could benefit from testing out new channels and techniques to attract customers, help them with discovery and more.

“We’ve discovered that the model for success for B2B businesses online is not about different people, and not about money. They just don’t have the tooling,” said Graf. “Those that have proven to be more successful are those that are able to move faster, to test out everything that comes to mind.”

Spryker positions itself as the company to help larger businesses do this, much in the way that smaller merchants have adopted solutions from the likes of Shopify .

In some ways, it almost feels like the case of Walmart versus Amazon playing itself out across multiple verticals, and now in the world of B2B.

“One of our biggest DIY customers [which would have previously served a mainly trade-only clientele] had to build a marketplace because of restrictions in their brick and mortar assortment, and in how it could be accessed,” Lokschin said. “You might ask yourself, who really needs more selection? But there are new providers like Mano Mano and Amazon, both offering millions of products. Older companies then have to become marketplaces themselves to remain competitive.”

It seems that even Spryker itself is not immune from that marketplace trend: Part of the funding will be to develop a technology AppStore, where it can itself offer third-party tools to companies to complement what it provides in terms of e-commerce tools.

“We integrate with hundreds of tech providers, including 30-40 payment providers, all of the essential logistics networks,” Lokschin said.

Spryker is part of that category of e-commerce businesses known as “headless” providers — by which they mean those using the tools do so by way of API-based architecture and other easy-to-integrate modules delivered through a “PaaS” (clould-based Platform as a Service) model.

It is not alone in that category: There have been a number of others playing on the same concept to emerge both in Europe and the U.S. They include Commerce Layer in Italy; another startup out of Germany called Commercetools; and Shogun in the U.S.

Spryker’s argument is that by being a newer company (founded in 2018) it has a more up-to-date stack that puts it ahead of older startups and more incumbent players like SAP and Oracle.

That is part of what attracted TCV and others in this round, which was closed earlier than Spryker had even planned to raise (it was aiming for Q2 of next year) but came on good terms.

“The commerce infrastructure market has been a high priority for TCV over the years. It is a large market that is growing rapidly on the back of e-commerce growth,” said Muz Ashraf, a principal at TCV, to TechCrunch. “We have invested across other areas of the commerce stack, including payments (Mollie, Klarna), underlying infrastructure (Redis Labs) as well as systems of engagement (ExactTarget, Sitecore). Traditional offline vendors are increasingly rethinking their digital commerce strategy, more so given what we are living through, and that further acts as a market accelerant.

“Having tracked Spryker for a while now, we think their solution meets the needs of enterprises who are increasingly looking for modern solutions that allow them to live in a best-of-breed world, future-proofing their commerce offerings and allowing them to provide innovative experiences to their consumers.”

Powered by WPeMatico