Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

EngineEars today announced a $1 million raise. The company’s first round of funding features investments from Kendrick Lamar, DJ Mustard, Roddy Rich and Slauson and Co. “Quality of sound is still important in music,” Lamar said in a quote provided to TechCrunch. “Ali has always been a progressive thinker. Engineers will transcend the culture.”

The service was launched in 2018 by Grammy winner Derek “MixedByAli” Ali, who has worked on a slew of high-profile tracks from artists including Lamar, Jay Rock, SZA, Nipsey Hussle and Snoop Dogg.

The educational courses turned into a touring curriculum, with 15 workshops in four countries, where Ali says he was able to determine what the community most needed.

“During that time, we really learned what the problem is,” says Ali. “All of the problems entailed tracking payments, being credited, the antiquated business model of file transfers and essentially just helping an independent audio engineer sustain and create a business for themselves.”

EngineEars has since branched out into something more akin to a marketplace for audio engineers. Independent mixers can offer their services and connect with artists and labels, get credit for the tracks they’ve worked on and — perhaps most importantly in the world of freelancing — get paid.

The platform launched an alpha version in January and since has 120 engineers verified by an existing vetting process. The invite-only service has another 2,000 people on its waiting list, according to Ali.

The service is currently working on a feature roadmap based on the requests of existing users and looking toward potential additions like the ability to buy beats, going forward. Other suggested features include contract negotiations for work-for-hire, but much of this is still very much in early stages.

Powered by WPeMatico

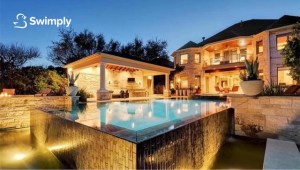

As the oldest of 12 children, Bunim Laskin spent much of his teen years looking for ways to help keep his siblings entertained. Noticing that a neighbor’s pool was often empty, Laskin reached out to ask if his family could use her pool. To make it worth her while, he suggested that they could help cover her expenses for maintaining the pool.

Soon after, five other families had made the same arrangement with her and the pool owner had six families covering 25% of her expenses. This meant that the neighbor was actually making money off her pool. The arrangement sparked a business idea in Laskin’s mind. At the age of 20, he founded Swimply, a marketplace for homeowners to rent out their underutilized pools to local swimmers, with Asher Weinberger.

The Cedarhurst, New York-based company launched a beta in 2018, starting with four pools in the New Jersey area.

“We used Google Earth to find houses, and then knocked on 80 doors with a pool,” CEO Laskin recalls. “We got to 100 pools organically. Word of mouth really helped us grow.” The site was pretty bare bones, he admits, with potential customers only able to view photos of the pools and connect with the pool owner by phone.

That year, Swimply did around 400 reservations and raised $1.2 million from friends and family.

In 2019, Swimply launched what he describes as a “proper” website and app with an automated platform. It grew “four to five times” that year, again mostly organically. In an episode that aired in March 2020, the company appeared on Shark Tank but went home without a deal.

Then the COVID-19 pandemic hit. Swimply, Laskin said, pivoted right into the pandemic.

“We were the perfect solution for people when the world was falling on its head,” he said. The company restructured its offering to ensure that pool owners did not have to interact with guests. “It was the perfect, contact-free, self-serve experience to hang out and be with people you quarantined with.”

The CDC then came out to say that it was safe to swim because chlorine could help kill the virus, and that proved to be a big boon to its business.

“On one end, it was a way for people to have a normal day and on the other, it helped give owners a way to earn an income, at a time when many people were being affected financially,” Laskin told TechCrunch.

Business took off in 2020 with revenue growing 4,000% and now Swimply is announcing a $10 million Series A round. Norwest Venture Partners led the financing, which also included participation from Trust Ventures and a number of angel investors such as Poshmark founder and CEO Manish Chandra; Rob Chesnut, former general counsel and chief ethics officer at Airbnb; Ancestry.com CEO Deborah Liu and Michael Curtis.

Swimply is now operating in a total of 125 U.S. markets, two markets in Canada and five markets in Australia. It plans to use its new capital in part to expand into new markets and toward product development.

Image Credits: Swimply

The way it works is pretty straightforward. Swimply simply connects homeowners that have underutilized backyard spaces and pools with those seeking a way to gather, cool off or exercise, for example. People or families can rent pools by the hour, ranging in price from $15 to $60 per hour (at an average of $45/hour) depending on the amenities. New markets that Swimply has recently expanded to include Portland, Oregon; Raleigh, North Carolina and the California cities of Oakland, San Luis Obispo and Los Gatos.

“The shifting mindset from younger generations about ownership is a huge contributor to increased growth of the Swimply marketplace,” said co-founder Weinberger, who serves as Swimply’s COO. “Swimming is the third most popular activity for adults and number one for children, and yet no other company has tackled the aquatic space to make swimming more affordable and accessible…until now.”

While the company declined to provide hard revenue figures, Laskin said Swimply was seeing “seven digits a month in revenue” and 15,000 to 20,000 reservations a month. Families represent the most popular reservation.

“People can book and pay through our platform, and only 20% of hosts ever meet their guests,” Laskin said. “We’re enabling a new kind of consumer behavior with what we’re doing.”

The company is planning to use its new capital to also rebuild much of its tech infrastructure and boost its customer support team to be more “readily available.”

It is also now offering a complimentary up to $1 million worth of insurance per booking for liability as well as $10,000 for property damage.

Swimply has a little over 20 employees, up 10 times from two people in December of 2020. It plans to double that number over the next few months.

The company’s model has proven quite lucrative for some owners, according to Laskin.

“Last year, there were some owners who earned $10,000 a month. One owner in Denver earned $50,000 last year and he had signed up toward the end of the summer. He should make over $100,000 this year,” Lasken projects.

Its only criteria is that owners offer a clean pool. Eighty-five percent of hosts offer restrooms as well. If they don’t, they are limited to one-hour reservations with a max of five guests. Swimply has also partnered with local pool companies, and if they pay one of its owners a visit and certify that pool, that owner gets a badge on the site “so guests get an additional level of security,” Laskin said.

Ed Yip of Norwest Venture Partners admits that when he first heard of the concept of Swimply, he “didn’t know what to make of it.”

But the more he heard about it, the more excited he got.

“This is the Holy Grail for a consumer investor. We’re not changing consumer behavior, but rather [we] productize the experience and make it safer and easier on both sides,” Yip told TechCrunch.

What also gets the investor excited is the potential for Swimply beyond just swimming pools in the future.

“We’re seeing a ton of demand from hosts wanting to list hot tubs and tennis courts, for example,” Yip said. “So this can turn into a marketplace for shared outdoor resources and that’s a huge market opportunity that adds value on both sides.”

Indeed, the concept of monetizing underutilized space is a growing concept. Earlier this year, we reported on Neighbor, which operates a self-storage marketplace, raising $53 million in a Series B round of funding. Neighbor’s unique model aims to repurpose under-utilized or vacant space — whether it be a person’s basement or the empty floor of an office building — and turn it into storage.

Powered by WPeMatico

It’s an entrepreneur’s market in digital health today, with startups raising record-breaking funding at soaring valuations and debuting on public markets to eager investors.

According to CB Insights, as of March 3, 2021, there are 51 healthcare unicorns — “startups” — worth $1 billion or more around the world. Global venture capital funding, including private equity and corporate VC, into digital health was the highest ever in the first quarter 2021 at $7.2 billion, according to Mercom Capital Group.

The massive influx of capital to healthcare should not be surprising; the pandemic has made it starkly clear that digital health is the future of healthcare. To that end, we should anticipate additional healthcare exits worth more than $1 billion in the near term. Which again, is great for entrepreneurs — as long as they understand how hard it is to build a unicorn in healthcare. Today, becoming a unicorn requires founders who are long on vision and operational experience.

Today, becoming a unicorn requires founders who are long on vision and operational experience.

Company founders most often turn to veteran investors for help with grand-slam strategies to create the next healthcare unicorn. That’s why many of them seek counsel from the Merck Global Health Innovation Fund: Because we have the experience, resources, successful track record and networks to build real scale in digital health.

During the pandemic, lots of investors jumped in to invest in digital health for the first time. But we’ve been investing for more than a decade. Two of our portfolio companies, Preventice Solutions and Livongo, exited last year as unicorns, rounding out the $6.2 billion in digital health market value MGHIF has exited over the last two years. And we are expecting two more unicorn exits in 2021. But we’re not stopping there; we’ll be investing our $500 million fund in drone-supported supply chain technologies, telehealth, AI, digital pathology, remote clinical trials and Internet of Medical Things (IoMT).

Given our success, here are four instrumental strategies to building a unicorn in digital health that we know work.

We often ask entrepreneurs: Would you rather own 20% of a $50 million company or 5% of a $1 billion company? To most, the answer is obvious. In our experience, too many entrepreneurs worry about dilution and never raise the right amount of capital.

It’s well known that companies with rapidly growing revenues are valued at a premium — but it’s important to remember that this is hard to do in healthcare. Getting to scale takes time because healthcare is so complicated and involves so many stakeholders.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

For this week’s deep dive Natasha and Alex and Chris dug into the world of the IPO. Not just the numbers and the metrics and the calculations of valuations at diluted, and non-diluted, share counts. No. We wanted to talk about the morality and efficacy of going public.

So to round out our conversation we enlisted Steve Cakebread, the CFO of Yext, and Garth Mitchell, the CFO of Latch. Cakebread is known for being aboard the Salesforce, Pandora and Yext IPOs. Mitchell has sat on both sides of the table during the IPO process, and is currently helming the money equations as Latch approaches the public markets via a SPAC.

For more context, Yext, a company that first launched at a TechCrunch event back in 2009, provides data tooling and search software to businesses, while Latch builds software and hardware for rental-focused buildings. Yext is public. Latch will be in a few months.

Back to our topic, we asked Cakebread to talk about his thesis on why going public earlier than later can help a company’s maturity process and can help provide greater returns to the general public. The CFO has written a rather good book about the IPO process more generally and what it means for a company’s internal processes, but his morality notes especially stood out because it’s an argument far less noisy than the POP critics. Baked beans come up, somehow!

We also asked Mitchell to talk about Latch’s choice to go public, and what opportunities and challenges the SPAC route brings for the company. Of course, there’s a SPAC joke in there (or two), but we get into broader “what’s next” debates about if more companies will start to leave the private world, venture capital’s role in this whole mess and the financial lift of going to the public market.

Hope you enjoy the show, and get excited: Equity is going to have more guests on from time to time, and we welcome any suggestions you want to throw at us.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I’ve been working for a large tech company on an H-1B visa for about a year and a half. I’d like to establish my own company while maintaining my current, secure job.

Can I keep working on the H-1B, found my own company, and then have my startup sponsor me for an H-1B or another visa?

— Scrappy in Santa Clara

Hi Scrappy,

You need to be very careful while navigating this process because there are many different legal requirements that you need to pay careful attention to so you comply with U.S. immigration laws. But yes, it is possible for you to own a portion of a business on H-1B, and it is possible for a founder to obtain an H-1B transfer to work at the startup.

Take a listen to a recent podcast episode in which I discuss having two H-1B jobs — or concurrent H-1Bs. Concurrent H-1Bs enable your second employer — in this case, your startup — to avoid having to go through the H-1B lottery process because you have already gone through that process with your current employer.

Be kind to your attorneys — you will need their support to navigate this process! Before you embark on creating your startup, you should review and discuss your employment contract and NDA with an employment lawyer.

Big companies often require employees to obtain their consent prior to forming a startup. You should also consult with an experienced immigration attorney when considering embarking on this path and determining how to structure your startup. The H-1B has specific requirements that you and your startup must meet to qualify.

As you probably already know, the H-1B visa allows you to work for a specific employer in a specific job at a specific location. That means you cannot work for or at your startup under your current H-1B. Therefore, we often advise clients not to found any startup as a sole proprietorship. There will probably need to be a corporation or a limited liability company.

You may be advised to find a co-founder or two. One of the key requirements for the H-1B that you need to keep in mind is your startup and you must have an employer-employee relationship. That means someone at your startup, such as a co-founder, must have the ability to hire you, supervise you, hold you accountable for poor job performance, and fire you, according to the terms and conditions of the H-1B.

Also, you may need to work with a corporate attorney to draft certain bylaws, and it can be helpful if you personally own less than 50% of your startup. All of these things depend on the specific details of your situation, so definitely talk to experienced attorneys to guide you through, step by step!

Image Credits: Joanna Buniak / Sophie Alcorn (opens in a new window)

Your position and your startup must meet other requirements for an H-1B. To qualify for an H-1B, the future position must meet the definition of a “specialty occupation.” That means your position requires theoretical and practical application of highly specialized knowledge.

It also means you must have at least a bachelor’s degree or equivalent experience in a field that’s directly related to the position.

Moreover, your startup must be able to pay you the prevailing wage for the position and for the location where your startup or the position is based. Prevailing wages, which are determined by the U.S. Department of Labor, are broken down into four levels based on experience, with Level I being an entry-level position and Level IV being the most experienced.

Before filing an H-1B petition on your behalf to U.S. Citizenship and Immigration Services (USCIS), your startup’s immigration attorney will have to first submit a Labor Condition Application (LCA) for certification by the Department of Labor. An LCA seeks to ensure that the wages and working conditions of American workers are not negatively impacted by an H-1B position.

Equity in a company and stock options are not considered wages in the H-1B context. Therefore, your startup will need to show that it can afford to pay you the prevailing wage as well as support business operations.

If you’re pre-revenue, this can be shown by a business plan plus your bank statements showing your runway from an initial investment. The amounts required depend on the details of your company’s situation.

There are no restrictions on the number of hours an individual on an H-1B must work. An H-1B position can be full time or part time or involve working just a few hours a week. Take a listen to my podcast on best practices for submitting a strong H-1B petition.

Concurrent H-1B employment can last as long as the original H-1B with your large tech employer. If you want to remain permanently in the United States, you or one of the companies sponsoring your H-1B should apply for a green card at least a year before your sixth year on the H-1B. (If you apply for a green card before your sixth year on an H-1B, the sponsoring employer can continue to extend your H-1B beyond six years until you receive your green card so you don’t have to leave the United States to apply at a U.S. embassy in your home country).

If you want to apply for a green card on your own, consider the EB-1A green card for individuals with extraordinary ability or the EB-2 NIW (National Interest Waiver) for individuals with exceptional ability.

Other employment-based green cards, such as the EB-2 green card for professionals holding advanced degrees and EB-3 for skilled workers and professionals, require an employer to sponsor you as well as the PERM process, which can be challenging if you own substantial equity in the company.

Check with your current employer to find out if the company is willing to sponsor you for a green card. Depending on the timing, you might be able to bypass a second H-1B completely, avoiding the employer-employee relationship restrictions with your startup venture.

The work permit that comes in the I-485 adjustment of status process is unrestricted as to the type of employment in which you can engage!

Wishing you the best on your journey,

Sophie

Have a question for Sophie? Ask it here. We reserve the right to edit your submission for clarity and/or space.

The information provided in “Dear Sophie” is general information and not legal advice. For more information on the limitations of “Dear Sophie,” please view our full disclaimer. You can contact Sophie directly at Alcorn Immigration Law.

Sophie’s podcast, Immigration Law for Tech Startups, is available on all major platforms. If you’d like to be a guest, she’s accepting applications!

Powered by WPeMatico

Timescale, makers of the open-source TimescaleDB time series database, announced a $40 million Series B financing round today. The investment comes just over two years after it got a $15 million Series A.

Redpoint Ventures led today’s round, with help from existing investors Benchmark, New Enterprise Associates, Icon Ventures and Two Sigma Ventures. The company reports it has now raised approximately $70 million.

TimescaleDB lets users measure data across a time dimension, so anything that would change over time. “What we found is we need a purpose-built database for it to handle scalability, reliability and performance, and we like to think of ourselves as the category-defining relational database for time series,” CEO and co-founder Ajay Kulkarni explained.

He says that the choice to build their database on top of Postgres when it launched four years ago was a key decision. “There are a few different databases that are designed for time series, but we’re the only one where developers get the purpose-built time series database plus a complete Postgres database all in one,” he said.

While the company has an open-source version, last year it decided rather than selling an enterprise version (as it had been), it was going to include all of that functionality in the free version of the product and place a bet entirely on the cloud for revenue.

“We decided that we’re going to make a bold bet on the cloud. We think cloud is where the future of database adoption is, and so in the last year […] we made all of our enterprise features free. If you want to test it yourself, you get the whole thing, but if you want a managed service, then we’re available to run it for you,” he said.

The community approach is working to attract users, with over 2 million monthly active databases, some of which the company is betting will convert to the cloud service over time. Timescale is based in New York City, but it’s a truly remote organization, with 60 employees spread across 20 countries and every continent except Antarctica.

He says that as a global company, it creates new dimensions of diversity and different ways of thinking about it. “I think one thing that is actually kind of an interesting challenge for us is what does D&I mean in a totally global org. A lot of people focus on diversity and inclusion within the U.S., but we think we’re doing better than most tech companies in terms of racial diversity, gender diversity,” he said.

And being remote-first isn’t going to change even when we get past the pandemic. “I think it may not work for every business, but I think being remote first has been a really good thing for us,” he said.

Powered by WPeMatico

With cybercrime on course to be a $6 trillion problem this year, organizations are throwing ever more resources at the issue to avoid being a target. Now, a startup that’s built a platform to help them stress-test the investments that they have made into their security IT is announcing some funding on the back of strong demand from the market for its tools.

Cymulate, which lets organizations and their partners run machine-based attack simulations on their networks to determine vulnerabilities and then automatically receive guidance around how to fix what is not working well enough, has picked up $45 million, funding that the startup — co-headquartered in Israel and New York — will be using to continue investing in its platform and to ramp up its operations after doubling its revenues last year on the back of a customer list that now numbers 300 large enterprises and mid-market companies, including the Euronext stock exchange network as well as service providers such as NTT and Telit.

London-based One Peak Partners is leading this Series C, with previous investors Susquehanna Growth Equity (SGE), Vertex Ventures Israel, Vertex Growth and Dell Technologies Capital also participating.

According to Eyal Wachsman, the CEO and co-founder, Cymulate’s technology has been built not just to improve an organization’s security, but an automated, machine learning-based system to better understand how to get the most out of the security investments that have already been made.

“Our vision is to be the largest cybersecurity ‘consulting firm’ without consultants,” he joked.

The valuation is not being disclosed, but as some measure of what is going on, David Klein, managing partner at One Peak, said in an interview that he expects Cymulate to hit a $1 billion valuation within two years at the rate it’s growing and bringing in revenue right now. The startup has now raised $71 million, so it’s likely the valuation is in the mid-hundreds of millions. (We’ll continue trying to get a better number to have a more specific data point here.)

Cymulate — pronounced “sigh-mulate”, like the “cy” in “cyber” and a pun of “simulate”) is cloud-based but works across both cloud and on-premises environments and the idea is that it complements work done by (human) security teams both inside and outside of an organization, as well as the security IT investments (in terms of software or hardware) that they have already made.

“We do not replace — we bring back the power of the expert by validating security controls and checking whether everything is working correctly to optimize a company’s security posture,” Wachsman said. “Most of the time, we find our customers are using only 20% of the capabilities that they have. The main idea is that we have become a standard.”

The company’s tools are based in part on the MITRE ATT&CK framework, a knowledge base of threats, tactics and techniques used by a number of other cybersecurity services, including a number of others building continuous validation services that compete with Cymulate. These include the likes of FireEye, Palo Alto Networks, Randori, Khosla-backed AttackIQ and many more.

Although Cymulate is optimized to help customers better use the security tools they already have, it is not meant to replace other security apps, Wachsman noted, even if the by-product might become buying fewer of those apps in the future.

“I believe my message every day when talking with security experts is to stop buying more security products,” he said in an interview. “They won’t help defend you from the next attack. You can use what you’ve already purchased as long as you configure it well.”

In his words, Cymulate acts as a “black box” on the network, where it integrates with security and other software (it can also work without integrating, but integrations allow for a deeper analysis). After running its simulations, it produces a map of the network and its threat profile, an executive summary of the situation that can be presented to management and a more technical rundown, which includes recommendations for mitigations and remediations.

Alongside validating and optimising existing security apps and identifying vulnerabilities in the network, Cymulate also has built special tools to fit different kinds of use cases that are particularly relevant to how businesses operate today. They include evaluating remote working deployments, the state of a network following an M&A process, the security landscape of an organization that links up with third parties in supply chain arrangements, how well an organization’s security architecture is meeting (or potentially conflicting) with privacy and other kinds of regulatory compliance requirements, and it has built a “purple team” deployment, where in cases where security teams do not have the resources for running separate “red teams” to stress test something, blue teams at the organization can use Cymulate to build a machine learning-based “team” to do this.

The fact that Cymulate has built the infrastructure to run all of these processes speaks to a lot of potential of what more it could build, especially as our threat landscape and how we do business both continue to evolve. Even as it is, though, the opportunity today is a massive one, with Gartner estimating that some $170 billion will be spent on information security by enterprises in 2022. That’s one reason why investors are here, too.

“The increasing pace of global cyber security attacks has resulted in a crisis of trust in the security posture of enterprises and a realization that security testing needs to be continuous as opposed to periodic, particularly in the context of an ever-changing IT infrastructure and rapidly evolving threats. Companies understand that implementing security solutions is not enough to guarantee protection against cyber threats and need to regain control,” said Klein, in a statement. “We expect Cymulate to grow very fast,” he told me more directly.

Powered by WPeMatico

Earlier today recent dog-parent Alex Konrad and fellow Forbes staffer Eliza Haverstock broke the news that Divvy, a Utah-based corporate spend unicorn, is considering selling itself to Bill.com for a price that could top $2 billion. For the fintech sector, it’s big news.

Corporate spend startups including Ramp and Brex are raising rapid-fired rounds at ever-higher valuations and growing at venture-ready cadences. Their growth and its resulting private investment were earned by a popular approach to offering corporate cards, and, increasingly, the group’s ability to build software around those cards that took into account a greater portion of the functionality that companies needed to track expenses, manage spend access, and, perhaps, save money.

The latter category was what Ramp focused on when it launched. It worked. More recently Ramp added expense tracking efforts to its own software suite. And Brex, an early leader in its efforts to get corporate cards into the hands of smaller, and more nascent businesses, has also built out its software efforts. So much so that the company, in conjunction with its huge recent fundraise, announced that it will begin offering a software package for a monthly fee.

Competitors like Airbase charge for their code, while some, like Divvy, traditionally have not.

Enter Bill.com. As the software work from the corporate spend startups has improved, it may have begun cutting into the corporate payments and expense software categories. For Bill.com in the payments world, and Expensify in the expense universe, that possible incursion could prove to be a growth-retarding concern. Thus, it makes sense to see Bill.com decide to take on the yet-private corporate spend startups that are playing the field; why not absorb a growing customer base and fend off competition in a single move?

To get a better handle on how the startups that compete with Divvy feel about the deal, TechCrunch reached out to both Ramp CEO Eric Glyman, and Brex CEO Henrique Dubugras. We’ll start with Glyman, who broadly agrees with our read of the situation:

Powered by WPeMatico

It’s only been three years since they hit the streets and Revel’s blue electric mopeds have already become a common sight in New York, San Francisco and a growing number of U.S. cities. However, Revel founder and CEO Frank Reig has set his sights far beyond building a shared moped service.

In fact, since the beginning of 2021, Revel has launched an e-bike subscription service, an EV charging station venture and an all-electric rideshare service driven by a fleet of 50 Teslas.

So we caught up with Reig to talk about what he learned from building the company, how Revel’s business strategy has evolved, and what lies ahead.

Before we get to the good stuff, here’s some background:

The idea for Revel seems like it came from the classic entrepreneur’s guidebook: Reig had a need that no existing company addressed. He’d seen mopeds used as major, if not dominant, forms of transportation as he traveled around Europe, Asia and Latin America, and he wondered why this logical (and fun) mode of transport was largely absent from American cities in general, and in his hometown, New York City, in particular.

So in 2018, Reig quit his job, raised $1.1 million from 57 people, and launched a small pilot program involving 68 mopeds in Brooklyn. In May 2019, he raised $4 million in VC funding, which helped him expand to 1,000 electric mopeds across Brooklyn and Queens. Revel secured another $33.8 million in September 2019, in a round that included funding from Ibex Investments, Toyota Ventures, Maniv Capital, Shell and Hyundai, according to Reig. This has allowed the founder to execute a grander plan to build an electric mobility company.

The company now operates more than 3,000 e-mopeds in New York City, and has another 3,000 across Washington, D.C., Miami, Oakland, Berkeley and San Francisco.

TechCrunch: You’ve added three new business lines and told us previously that you have more on the way. That’s a lot.

Frank Reig: Yes, we have had a busy start to 2021! We began the year announcing our fast-charging stations across the city that will help fill the large gap in infrastructure to support the wide-scale adoption of EVs. We launched our e-bike subscription program to offer New Yorkers another way to navigate their city, and with our newly announced electric ride-sharing program, we are solving the “chicken and egg” problem of EV charging and demand. We are focused on building out these business lines and our moped business as well and very much looking forward to what is to come.

When shared micromobility companies expand, they often just offer different vehicles. You seem to be going, “Ok, we’ll offer a different vehicle — an e-bike, but it’s a subscription. And we’re also doing electric vehicle chargers, and let’s add an EV rideshare to the mix.” It’s pretty broad.

If we’re talking about electrifying mobility in major cities, it starts with infrastructure. And we’re the company rolling up our sleeves and doing it now by building that infrastructure and operating fleets. Because in a city like New York, the infrastructure does not exist for electric mobility.

There are a few Tesla superchargers around the city, usually behind parking paywalls, so you have to pay the garage to even use it. And, of course, you need a Tesla for that infrastructure to even be relevant. And when you think about other public fast-charging access points in the city, they are few and far between. We’re building 30 in one site and many more beyond that in 2021.

New York is a complicated city to operate in, so it’s easier for us to add e-bikes as a service because I already have the infrastructure and on-the-ground operations that we built with the mopeds. I have multiple warehouses throughout this city. I have full-time staff that I’ve employed, from field technicians to mechanics, and a fleet of over 3,000 vehicles on the streets in New York. So it’s a natural extension of the platform to be able to add another product to it, to reach a new type of user, or to supplement the use case of our current moped users. All we needed to do was finance some e-bikes, and then you have another line of business.

Powered by WPeMatico

An issue every developer faces is dealing with problems on a live application without messing it up. In fact, in many companies such access is restricted. Cased, an early stage startup, has come up with a solution to provide a way to work safely with the live application.

Today, the company announced a $2.25 million seed round led by Founders Fund along with a group of prestigious technology angel investors. The company also announced that the product is generally available to all developers today for the first time. It’s worth noting that the funding actually closed last April, and they are just announcing it today.

Bryan Byrne, CEO and co-founder at Cased says he and his fellow co-founders, all of whom cut their teeth at GitHub, experienced this problem of working in live production environments firsthand. He says that the typical response by larger companies is to build a tool in-house, but this isn’t an option for many smaller companies.

“We saw firsthand at GitHub how the developer experience gets more difficult over time, and it becomes more difficult for developers to get production work done. So we wanted to provide a developer friendly way to get production work done,” Byrne explained.

He said without proper tooling, it forces CTOs to restrict access to the production code, which in turn makes it difficult to fix problems as they arise in production environments. “Companies are forced to restrict access to production and restrict access to tools that developers need to work in production. A lot of the biggest tech companies invest in millions to deliver great developer experiences, but obviously smaller companies don’t have those resources. So we want to give all companies the building blocks they need to deliver a great developer experience out of the box,” he said.

This involves providing development teams with open access to production command line tools by adding logging and approval workflows to sensitive operations. That enables executives to open up access with specific rules and the ability to audit who has been accessing the production environment.

The company launched at the beginning of last year and the founders have been working with design partners and early customers prior to officially opening the site to the general public today.

They currently have five people including the four founders, but Byrne says that they have had a good initial reaction to the product and are in the process of hiring additional employees. He says that as they do, diversity and inclusion is a big priority for the founders, even as a very early stage company.

“It’s very prominent in our company handbook, so that we make sure we prioritize an inclusive culture from the very beginning because [ … ] we know firsthand that if you don’t invest in that early, it can really hold you back as a company and as a culture. Culture starts from day one, for sure,” he said.

As part of that, the company intends to be remote first even post-pandemic, a move he believes will make it easier to build a diverse company.

“We will definitely be remote first. We believe that also helps with diversity and inclusion as you allow people to work from anywhere, and we have a lot of experience in leading remote-first culture from our time at GitHub, so we began as a remote culture and we will continue to do that,” he said.

Powered by WPeMatico