Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

HQ Trivia was removed from the App Store following a controversial ending to a $25K game on Sunday night, according to Business Insider.

HQ has introduced a new high-stakes version of the game where one winner takes home a larger prize. However, on Sunday night, no one won the $25K.

The company posted on its Twitter account that moderators kick players who break the company’s TOS.

HQ moderators kick players that violate HQ’s Terms of Service and Contest Rules. For more information, please refer to our Terms of Service here: https://t.co/septsPVgOm

— HQ Trivia (@hqtrivia) March 19, 2018

HQ would not be specific about what rules were broken, but BI reports that Twitter users had suggested it was due to jailbroken iPhones, which could be running software that gives users a leg up in the trivia competition.

For those who missed the game last night, two players remained for the final question. One was removed due to breaking the TOS, and the remaining player missed the last question, resulting in no winner.

Cheating seems to be a growing problem with HQ Trivia. There are countless guides online about how to cheat, including obvious methods like using voice dictation and a second device to Google search each question. The time limit makes that more difficult, but not impossible.

But as HQ grows its prize pot — the original prize was $1000 — cheating on the platform, and the methods by which people cheat, is only bound to intensify.

Even more bizarre, the app was seemingly removed from the App Store following the game. It has since re-appeared on the App Store.

HQ says that last night’s game and HQ’s removal from the App Store are unrelated events. A spokesperson from the company confirmed Mashable’s report that the app was removed because of a clerical error. Long story short, someone at HQ forgot to update the expired credit card info in the developer portal of the App Store.

App analytics firm Apptopia confirmed that HQ Trivia was removed from the App Store briefly, and that it has been falling in ranking for the past 30 to 60 days.

![]()

We reached out to Apple and haven’t heard back. We will report back as soon as we know more.

Powered by WPeMatico

Pinterest is looking to continue to increase its portfolio of ads, though sometimes that can take a little while to see the light of day — and that includes a new-ish tool called Shopping Ads that’s slowly getting opened to more marketers and advertisers.

Getting new ad formats is important for a smaller company looking to build out an advertising business, as it has to show potential advertisers it can offer an array of tools to play with as they experiment with that service. The company said today that it’s expanding those shopping ad tools to hundreds of additional advertisers after launching a pilot program last year as it looks to continue to ramp up that tool. Pinterest has to be able to convince marketers that it should be a mainstay advertising purchase alongside Facebook and Google, which are able to routinely show returns in value for their advertising spend.

Shopping ads automatically create promoted pins from an existing product feed for a retailer. That means it’s basically one less thing for retailers to worry about as they add more and more content to the service. Most of Pinterest’s content online is business content as users share products they might be interested in one day buying or already own. As Pinterest gets more and more data on this, they’ll have a better handle on what ads work best, and hope that businesses will hand off the process in full to something more automated.

Pinterest hopes to capture that routine user behavior of planning what they want to do next, whether that’s an outfit to wear that day or some kind of major event or purchase down the line. Getting a hold of those users in the moment they might be interested in a new product is key to the company’s pitch to advertisers. You can more or less consider this a continued test as the company starts to slowly give the tool to the advertisers it works with before it becomes generally available. If it works, it could probably end up down the line in the hands of all advertisers, which could help for small- to medium-sized businesses without a lot of experience build out their early marketing campaigns.

Powered by WPeMatico

Autonomous vehicles are increasingly becoming the shiny object in Silicon Valley. But the opportunity doesn’t just extend to cars driving around the streets of a major metropolitan area, and Igino Cafiero and Aubrey Donnellan hope to take it somewhere a little less obvious: the middle of an orchard.

Cafiero and Donnellan are building an autonomously-driven tractor as part of a startup called Bear Flag Robotics. The pair argue that there’s increasingly a struggle to find enough labor to work on farms, and even then, the costs are continuing to rise over time — leading to a need to increase those efficiencies on the actual field in addition to a lot of new technology like satellite imagery and computer vision to analyze the health of plants. The first product for Bear Flag Robotics is a self-driving tractor, and the company is coming out of Y Combinator’s winter class this year.

“We got a tour of an orchard and just how pronounced the labor problem is,” Donnellan said. “They’re struggling to fill seats on tractors. We talked to other growers in California. We kept hearing the same thing over and over: labor is one of the most significant pain points. It’s really hard to find quality labor. The workforce is aging out. They’re leaving the country and going into other industries.”

There are certainly a lot of technical challenges that go into it, and not just pertaining from having the right computer vision products in place in order to create an autonomous tractor. For example, the tractors have to be able to operate without a GPS signal, Donnellan said, simply because operating a tractor in an orchard may mean driving around with a ton of canopy cover — which could block the signal. It might be a little simpler to just drive down a path in an orchard, but there’s still quite a lot to consider, she said.

“We have this platform that we’ve plugged a ton of sensors into it,” Cafiero said. “That includes cameras. When you look forward, once we’ve automated the driving part, the sky’s the limit in terms of utilizing some of this technology once it’s out there. When we’re out there we can use these cameras, and be able to make recommendations and spot treatment in the field.”

When it comes to testing, Cafiero and Donnellan just go out to an orchard over in Sunnyvale a few times a week to see what some of the challenges growers face.

While finding labor has been a challenge, Cafiero acknowledges that there are still questions around undocumented labor when it comes to labor on those farms. He said, in the end, Bear Flag Robotics’ aim is to augment the workforce by taking away some of the more mundane tasks required on the fields. Cafiero also said that there’s a lot of reverse immigration happening from the U.S., leading to more of a labor shortage.

“The work itself is really tough work,” Donnellan said. “You’re in the field all day long, sometimes in inclement conditions. One of the tasks we’re automating is spraying, fungicides, herbicides, and these people out there, they’re wearing hazmat suits. It’s not good for their health to be doing these tasks in general. When you’re presented in higher paying jobs in other fields, there’s less of a case to go into that job, and there’s demand in a lot of other industries like construction [and other industries] where it’s easier work and better pay.”

Selling the actual tractor can also be a challenge, simply because potential customers will be buying their equipment down the road at sellers they know. If something breaks down, they need someone to come over, in person, as soon as possible to fix it or risk losing yield. And the major equipment providers may too see the need to start working on autonomous tools. Cafiero’s hope is that the startup will be able to work with local sellers and get into those channels, and that’s the only logical place to start. There might be some aim to scale up over time, but the company hopes to just get started with local dealerships for now.

Powered by WPeMatico

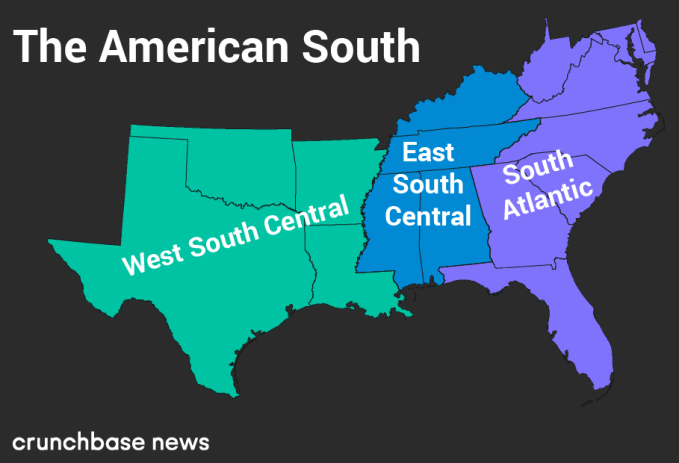

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

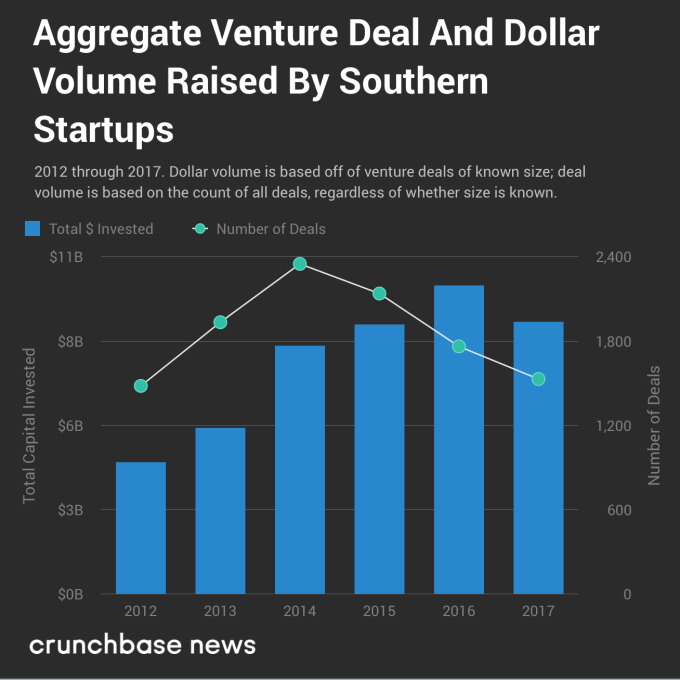

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

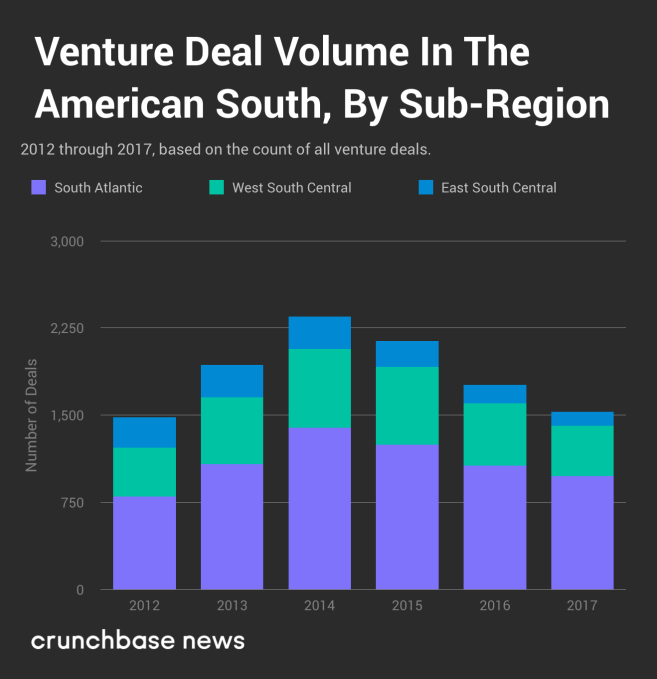

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

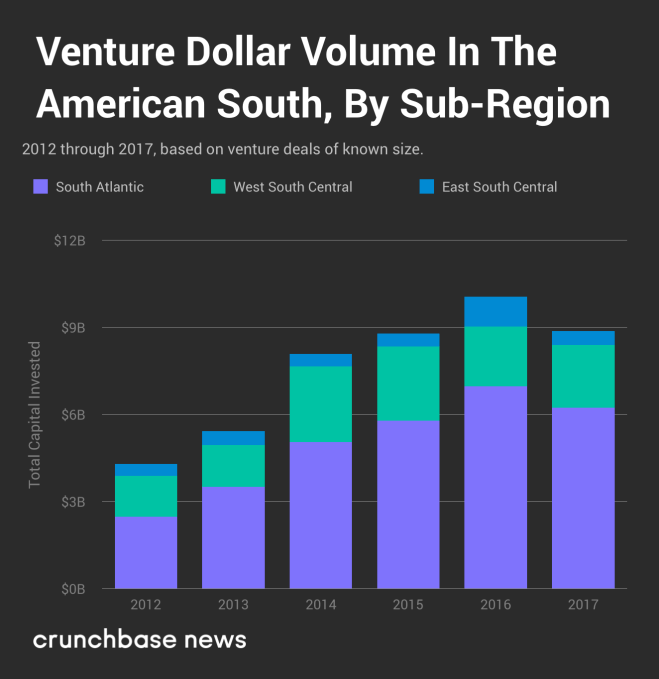

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

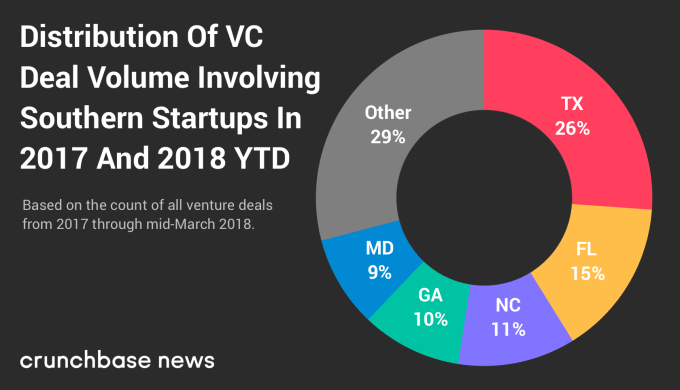

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

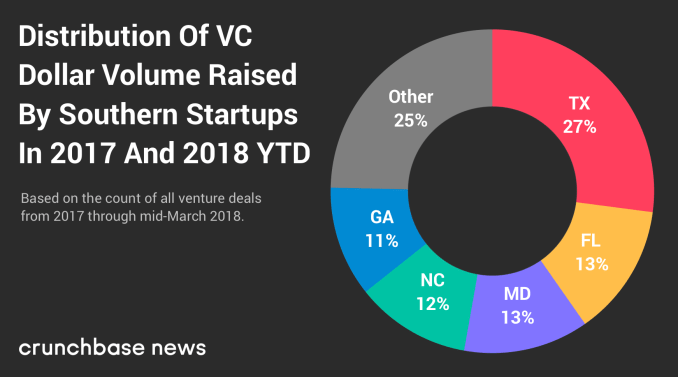

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

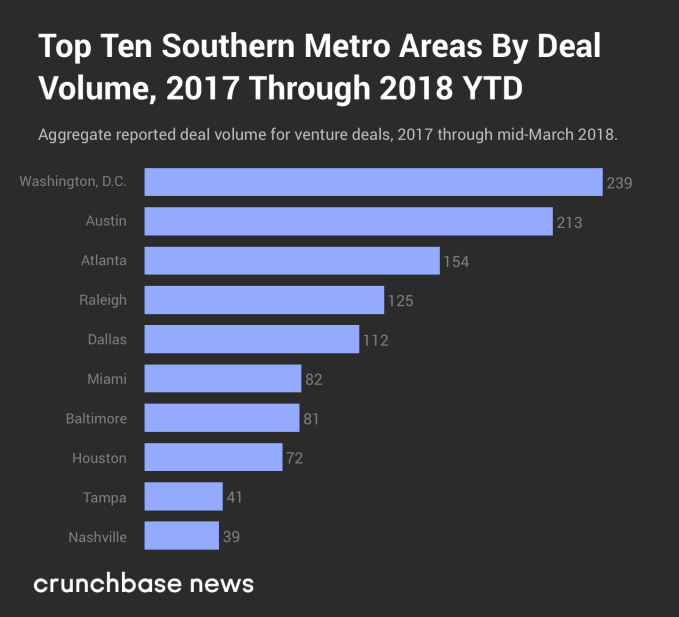

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

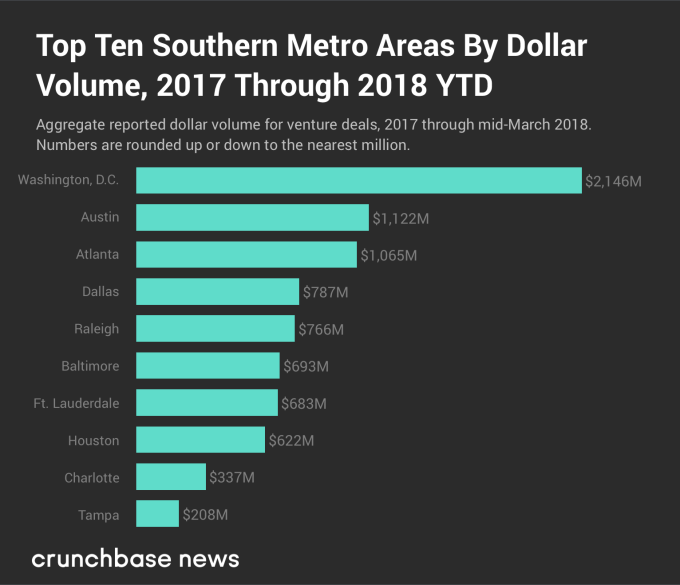

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

Drama is heating up between the dating apps.

Tinder, which is owned by Match Group, is suing rival Bumble, alleging patent infringement and misuse of intellectual property.

The suit alleges that Bumble “copied Tinder’s world-changing, card-swipe-based, mutual opt-in premise.” The lawsuit also accuses Tinder-turned-Bumble employees Chris Gulczynski and Sarah Mick of copying elements of the design. “Bumble has released at least two features that its co-founders learned of and developed confidentially while at Tinder in violation of confidentiality agreements.”

It’s complicated because Bumble was founded by CEO Whitney Wolfe, who was also a co-founder at Tinder. She wound up suing Tinder for sexual harassment.

Yet Match hasn’t let the history stop it from trying to buy hotter-than-hot Bumble anyway. As Axios’s Dan Primack pointed out, this lawsuit may actually try to force the hand for a deal. Bumble is majority-owned by Badoo, a dating company based in London and Moscow.

(It wouldn’t be the first time a dating site sued another and then bought it. JDate did this with JSwipe.)

Match provided the following statement:

Match Group has invested significant resources and creative expertise in the development of our industry-leading suite of products. We are committed to protecting the intellectual property and proprietary data that defines our business. Accordingly, we are prepared when necessary to enforce our patents and other intellectual property rights against any operator in the dating space who infringes upon those rights.

I have, um, tested out both Tinder and Bumble and they are similar. Both let you swipe on nearby users with limited information like photos, age, school and employer. And users can only chat if both opt-in.

However, Tinder has developed more of the reputation as a “hookup” app and Bumble doesn’t seem to have quite the same image, largely because it requires women to initiate the conversation, thus setting the tone.

As TechCrunch’s Sarah Perez pointed out recently, “according to App Annie, Tinder is more than 10x bigger in terms of monthly users and 7x bigger in terms of downloads in the last 12 months, versus Bumble.”

We’ve reached out to Bumble for comment.

Powered by WPeMatico

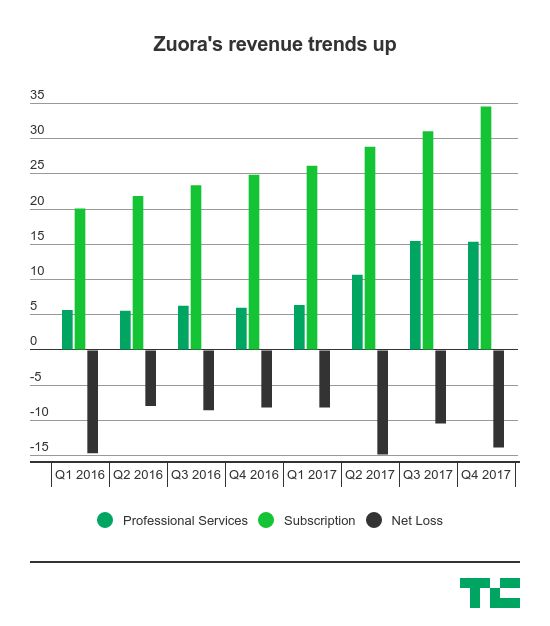

Zuora, which helps businesses handle subscription billing and forecasting, filed for an initial public offering this afternoon following on the heels of Dropbox’s filing earlier this month.

Zuora’s IPO may signal that Dropbox going public, and seeing a price range that while under its previous valuation seems relatively reasonable, may open the door for coming enterprise initial public offerings. Cloud security company Zscaler also made its debut earlier this week, with the stock doubling once it began trading on the Nasdaq. Zuora will list on the New York Stock Exchange under the ticker “ZUO.” Zuora CEO Tien Tzuo told The Information in October last year that it expected to go public this year.

Zuora’s numbers show some revenue growth, with its subscriptions services continue to grow. But its losses are a bit all over the place. While the costs for its subscription revenues is trending up, the costs for its professional services are also increasing dramatically, going from $6.2 million in Q4 2016 to $15.6 million in Q4 2017. The company had nearly $50 million in overall revenue in the fourth quarter last year, up from $30 million in Q4 2016.

But, as we can see, Zuora’s “professional services” revenue is an increasing share of the pie. In Q1 2016, professional services only amounted to 22% of Zuora’s revenue, and it’s up to 31% in the fourth quarter last year. It also accounts for a bigger share of Zuora’s costs of revenue, but it’s an area that it appears to be investing more.

Zuora’s core business revolves around helping companies with subscription businesses — like, say, Dropbox — better track their metrics like recurring revenue and retention rates. Zuora is riding a wave of enterprise companies finding traction within smaller teams as a free product and then graduating them into a subscription product as more and more people get on board. Eventually those companies hope to have a formal relationship with the company at a CIO level, and Zuora would hopefully grow up along with them.

Snap effectively opened the so-called “IPO window” in March last year, but both high-profile consumer IPOs — Blue Apron and Snap — have had significant issues since going public. While both consumer companies, it did spark a wave of enterprise IPOs looking to get out the door like Okta, Cardlytics, SailPoint and Aquantia. There have been other consumer IPOs like Stitch Fix, but for many firms, enterprise IPOs serve as the kinds of consistent returns with predictable revenue growth as they eventually march toward an IPO.

The filing says it will raise up to $100 million, but you can usually ignore that as it’s a placeholder. Zuora last raised $115 million in 2015, and was PitchBook data pegged the valuation at around $740 million, according to the Silicon Valley Business Journal. Benchmark Capital and Shasta Ventures are two big investors in the company, with Benchmark still owning around 11.1% of the company and Shasta Ventures owning 6.5%. CEO Tien Tzuo owns 10.2% of the company.

Powered by WPeMatico

Developer bootcamps — several-month training programs that are designed to help people get up to speed with the technical skills they need to become a developer — exploded in popularity in the early part of the decade, but there’s been a bit of a shakedown on the space recently.

And that could be a product of a lot of things, but for Jacob Hess and Terry Kim, it’s just not enough time to become a fully-fledged developer. With training in the Air Force, where both had to work on these kinds of compressed programs for entry-level technicians, both decided to try their own approach. The end result is NexGenT, which is own kind of bootcamp — but it’s for getting a certificate in network management, and not a one-size-fits-all sticker as a developer. That approach, which includes a 16-week class, is considerably more reasonable and helps get people industry-ready with a skill that’s teachable in that compressed period of time, Hess says. The company is launching out of Y Combinator’s winter class this year.

“There are 500,000 open IT jobs, but when you look at that number, what’s more interesting is so many of them are IT operation roles, and the remaining is software development,” Hess said. “The bigger pie in IT is non-software programming jobs. Cyber security is also huge because of the automation and AI. We want to create the stepping stone. Network engineering becomes a foundation for a lot of these jobs, whether you want to be a cloud architect and work for Amazon, it all starts with understanding and building a foundation around networking.”

The end result is a 16-week program where a batch of applicants gets a review, and a percentage of them are accepted into a cohort of students. They go through an engineering module, which teaches them the basics and mechanics of network engineering and learn about the IT industry. Students can go faster if they want — it’s primarily online — and then start working on labs where they are building their own lab, either physical or virtual. The process culminates in a project where the students have to roll out an HQ facility in two branch offices from design to technically implementing it.

The next phase is about getting them certifications for various technologies, which help them basically show that they are ready to start entering the workforce. Think of it as something similar to having a Github account where prospective employers can review the work, except the process is a lot more formalized and you end up with something concrete on the resume. The final phase is around career coaching and helping them get a job, which can last up to 6 months. Throughout this process, students have access to a mentor and live coaching where students can ask whatever questions they wish.

So, the process is not so dissimilar from the notion of a developer bootcamp. But at the same time, there’s a small-ish graveyard of developer bootcamps and some with issues. Galvanize in August said it would lay off around 11% of its staff, while Dev Bootcamp and Iron Yard shut down altogether. The knock on these camps is it’s hard to get developers ready to start shipping code in such a small period of time — but Kim argues that getting them certified and ready to be a network engineer is definitely something that’s doable in around 16 weeks.

“It’s more realistic,” Kim said. “For coding bootcamps, you have to go by off the portfolios and check their Github, and they have to pass that technical interview. In our world of IT operations, it’s not about the bachelor’s degree, it’s about the person having the knowledge. But the industry certifications come from third parties, and when they come out of our program and have two or three certifications. It’s enough to get into that entry-level job.”

It remains to be seen if this kind of an approach is going to work. NexGenT charges a tuition — around $12,000, which with maximum discounts hits around $6,500. The company offers a 36-month payment plan as well that comes with an enrollment fee, which stretches out that very steep ticket price. In reality, these zero-to-60 programs are designed to be for-profit, though there are some different models that take in a percentage of salary among other approaches. With that in mind, though, there’s always an opportunity to build a strong pipeline with certain companies, and if they can identify high-performing students they can offer more of a proof point and potentially use that as an opportunity to offer some variation of scholarship.

While this is more of a bootcamp-ish style program, there are already some IT certification programs through tools like Coursera. Google, in one instance, is offering financial aid for a batch of those students, and companies with deep pockets might be able to build out these kinds of pipeline programs on their own. Hess and Kim hope to offer some kind of high-touch approach, instead of just a class on a platform of many, that will give them an edge to be a preferred option.

Powered by WPeMatico

Gusto, formerly ZenPayroll, is the rare startup unicorn that has stayed relatively mum on its product and growth — its last press release, for instance, was more than a year ago. The company’s core offering remains payroll for small businesses, and it has been working to expand its customer base across the nation, including having its CEO, Joshua Reeves, go on a tour of the country to visit SMBs in an RV.

Now the company is opening up a bit on its recent progress. Gusto hit 60,000 customers nationwide in January, or roughly 1% of all employers in the United States, according to the company.

The company is also working on new products. One challenge small businesses face is getting access to high-quality, yet affordable, software, particularly in HR. “Small businesses actually get that people are the core more than large companies,” Reeves explained to me. “In a 10-person company, you know everyone, your customers are your neighbors, but they never really had access to high-quality software.”

Gusto is hoping to fill that gap, announcing the beta launch of a new product it’s calling HR Basics. The product offers a suite of tools for small businesses to handle the quotidian tasks of HR, including managing vacation time, compiling employee directories and improving the onboarding of new hires. Most importantly, the product is free, and doesn’t require a credit card or a bank account to sign up.

Reeves believes that Gusto has two purposes: to offer “peace of mind” to small business owners around areas like compliance that can lead to negative enforcement actions, and to provide software that can help companies become “great places to work” that are more focused on community. Reeves is particularly passionate about the latter point. “Even the terminology ‘human capital management’ — humans are not capital, humans are not resources, they are people, thank you very much.”

One particular area of focus for HR Basics is around onboarding. Gusto is hoping it can move all HR paperwork online, so that everything required to officially onboard an employee can be done even before the employee walks into work the first day. With that out of the way, Gusto can then focus on helping companies create the right corporate culture. For instance, the product offers a “Welcome Wall” where other employees can write cheerful and encouraging notes for a new employee to make them feel like they belong at the company from day one.

The Welcome Wall is designed to encourage new employees joining a company

This new product is free for businesses, and Gusto obviously hopes that it creates a funnel of potential customers who will eventually sign up for its payroll service and full HR platform, which charge around $6-12 a month per employee based on the specific plan that a business chooses.

One interesting commitment Gusto is making according to Reeves is that an employee’s profile on the platform will be a lifetime account. The company’s vision is that if an employee moves from one company to the next and both use Gusto, all of the preferences and other data required to administer HR would work immediately.

That portability mattered less in a world where employees spent decades at a single company, but now that employees often switch employers as often as every year, the repeated savings of time in the transition can be quite significant. Longer term, Gusto sees that sort of portability as critical for facilitating the changing nature of work in the 21st century.

Gusto, which was founded in 2011, is now entering middle age, and the company has 530 employees across its San Francisco and Denver offices, according to Reeves.

Update: Added the number of customers Gusto currently has.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This week Katie Roof and I were joined by Mayfield Fund’s Navin Chaddha, an investor with early connections with Lyft to talk about, well, Lyft — as well as two bombshell news events in the form of an SEC fine for Theranos and Broadcom’s hostile takeover efforts for Qualcomm hitting the brakes. Alex Wilhelm was not present this week but will join us again soon (we assume he was tending to his Slayer shirt collection).

Starting off with Lyft, there was quite a bit of activity for Uber’s biggest competitor in North America. The ride-sharing startup (can we still call it a startup?) said it would be partnering with Magna to “co-develop” an autonomous driving system. Chaddha talks a bit about how Lyft’s ambitions aren’t to be a vertical business like Uber, but serve as a platform for anyone to plug into. We’ve definitely seen this play out before — just look at what happened with Apple (the closed platform) and Android (the open platform). We dive in to see if Lyft’s ambitions are actually going to pan out as planned. Also, it got $200 million out of the deal.

Next up is Theranos, where the SEC investigation finally came to a head with founder Elizabeth Holmes and former president Ramesh “Sunny” Balwani were formally charged by the SEC for fraud. The SEC says the two raised more than $700 million from investors through an “elaborate, years-long fraud in which they exaggerated or made false statements about the company’s technology, business, and financial performance.” You can find the full story by TechCrunch’s Connie Loizos here, and we got a chance to dig into the implications of what it might mean for how investors scope out potential founders going forward. (Hint: Chaddha says they need to be more careful.)

Finally, BroadQualm is over. After months of hand-wringing over whether or not Broadcom would buy — and then commit a hostile takeover — of the U.S. semiconductor giant, the Trump administration blocked the deal. A cascading series of events associated with the CFIUS, a government body, got it to the point where Broadcom’s aggressive dealmaker Hock Tan dropped plans to go after Qualcomm altogether. The largest deal of all time in tech will, indeed, not be happening (for now), and it has potentially pretty big implications for M&A going forward.

That’s all for this week, we’ll catch you guys next week. Happy March Madness, and may fortune favor* your brackets.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocketcast, Downcast and all the casts.

* assuming you have Duke losing before the elite 8.

Powered by WPeMatico