Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

In what looks like a European first, the London-based early-stage venture capital firm Balderton Capital is announcing it has closed a new $145 million “secondary” fund dedicated to buying equity stakes from early shareholders in European-founded “high growth, scale-up” technology companies.

Dubbed “Balderton Liquidity I,” the new fund will invest in European growth-stage companies through the mechanism of purchasing shares from existing, early shareholders who want to liquidate some or all of their shares “pre-exit.”

“Balderton will take minority stakes, between regular fund-raising rounds, making it possible for early shareholders — including angels, seed funds, current and former founders and employees — to realise early returns, reinvest capital in the ecosystem, or reward founders and early employees,” explains the firm.

The move essentially formalises the secondary share dealing that already happens — typically as part of a Series C or other later rounds — which often sees founders take some money off the table so they can improve their own financial situation and won’t be tempted to sell their company too soon, but also gives early investors a way out so they can begin the cycle all over again. Otherwise it can literally take five to 10 years before a liquidity event happens, either via IPO or through a private acquisition, if it happens at all.

“The bigger picture is there are lots of shareholders who either want or need or have to take liquidity at some point,” Balderton partner Daniel Waterhouse tells me on a call. “Founders are one part of that… but I think the majority of this fund is more targeted at other shareholders — business angels, seed funds, maybe employees who left, founders who left — who want to reinvest their money, want to solve a personal financial issue, want to de-risk their personal balance sheets, etc. So we’re not obsessed with founders in this fund, we’re obsessed with many different types of early shareholders, which for many different reasons would like to get liquidity before the grand exit event.”

Waterhouse says that one of the big drivers for doing this now is that Balderton’s analysis suggests there is “a critical mass of interesting companies” that are in the growth stage: “businesses that have got a scalable commercial engine” and a proven commercial model. This critical mass has happened only over the last two years, which is why — unlike in Silicon Valley — we haven’t yet seen a fund of this kind launch in Europe.

“We think there’s now about 500 companies in Europe that have raised over $20 million. That doesn’t mean they are all great companies but it’s an interesting, crude data point in terms of the scale they’ve got to. As a consequence, within that 500 we expect there to be quite a lot of interesting companies for this fund to help and we obviously have a pretty good lens on the market. Through our early-stage investing, and working with companies from the early-stage through to exit, and then obviously staying in touch with companies we don’t necessarily invest in, we have a pretty good sense of that from a bottom up perspective on how many opportunities are out there.”

He explained that there are three aspects behind the secondary funding strategy. First is that by investing via secondary funding, more companies will gain access to the “Balderton platform,” which includes an extensive executive and CEO network and support with recruitment and marketing. Secondly, it is good for the ecosystem as it will not only help relieve financial pressure from founders so they can “shoot for the next growth point” but will also let business angels cash out and recycle their money by investing in new startups. Thirdly, and perhaps most importantly, Balderton thinks it represents a good investment opportunity for the firm and its LPs as secondary liquidity is “underserved as a market.”

(Separately, one London VC I spoke to said a dedicated secondary fund in Europe made sense except in one scenario: that European valuations see a price correction sometime in the future promoted by the current trajectory of available funding slowing down, which he believes will eventually happen. “Funds are 10 years so they just have to get out in time,” is how said VC framed it.)

To that end, Waterhouse says Balderton is looking to do around 15-20 investments out of the fund, but in some instances may start slowly and then buy more shares in the same company at an even later stage. It will be managed by Waterhouse with support from investment principal Laura Connell, who recently joined the VC firm.

Struggling to see many downsides to the new fund — which by virtue of being later-stage is less risky and will likely command a discount on secondary shares it does purchase — I ask if perhaps Balderton is being a little opportunistic in bringing a reasonably large amount of institutional capital to the secondary market.

“No, I don’t think so,” he replies. “What we’ve seen in our portfolio is [that] the point in time when someone is looking for liquidity isn’t set on the calendar alongside when companies do fund raising. In particular as a company gets more mature, the gap between fund raises can stretch out because the businesses are more close to profitability. And so it’s not deterministic. We want to just be there to help people who are actually looking to sell out of cycle in those points of time and at the moment have very little options. If someone wants to wait, they’ll wait.”

Finally, I was curious to know how it might feel the first time Balderton buys a substantial amount of secondary shares in a company that it previously turned its nose down at during the Series A stage. After pointing out that companies usually look very different at Series A compared to later on in their existence — and that Balderton can’t and doesn’t invest in every promising company — Waterhouse replies diplomatically: “Maybe we kick ourselves a bit, but we’re quite happy with the performance of our early funds and obviously we’ll be happy to add other new companies that are doing really well into the family.”

Powered by WPeMatico

Cratejoy, a startup that runs a marketplace for subscription businesses and helps founders launch and scale their own subscription box services, has laid off 18 members of its 43-person team.

The company’s co-founder and chief executive officer Amir Elaguizy confirmed the lay-offs to TechCrunch. He says the cuts are part of a restructuring effort to keep costs in line and that subscribers and merchants will not be impacted.

The startup has raised a total of $10 million to date from investors, including Charles River Ventures, SV Angel, Andreessen Horowitz, Maverick Capital, Start Fund and ACE Venture Fund. Cratejoy completed the Y Combinator accelerator program in the summer of 2013 alongside DoorDash, Le Tote and Bloom That, which itself recently hit pause on its on-demand flower service.

“This was a hard decision made by the leadership team to keep our costs in line,” Elaguizy told TechCrunch. “Whenever we’re forced to make hard staffing decisions it is difficult, and this reduction was no exception. We had to part ways with many very good and talented people.”

Elaguizy declined to elaborate on any other changes to the business.

Austin-based Cratejoy sells a curated collection of subscription boxes and helps entrepreneurs develop their own subscription box. It exists on the premise that the future of e-commerce is these packaged collections of goods delivered on a recurring basis.

For some time, venture capitalists were drinking the subscription box Kool-Aid, but those days appear to be over. Funding into subscription box startups, according to Crunchbase data, has dropped off significantly.

Cratejoy was founded in 2014 amid the subscription box funding boom. The same year it completed its $4 million Series A, Birchbox completed a $60 million round, Dollar Shave Club raised $13 million and Stitch Fix brought in $30 million. With 30 companies raising about $200 million, 2014 was the highest on record for investment in subscription box companies.

Last year, companies in the sector raised just $39.7 million across 20 deals.

Powered by WPeMatico

Not even Techstars NYC can avoid the end of summer, where 10 startups are wrapping up their participation in the accelerator’s summer program.

This also marks the end of Alex Iskold’s tenure as managing director of the program. He’s certainly going out with a varied groups of startups — these entrepreneurs are working on everything from tampons to spices to skin care, plus more traditional tech categories like finance and security.

Here’s a quick rundown of each company.

Powered by WPeMatico

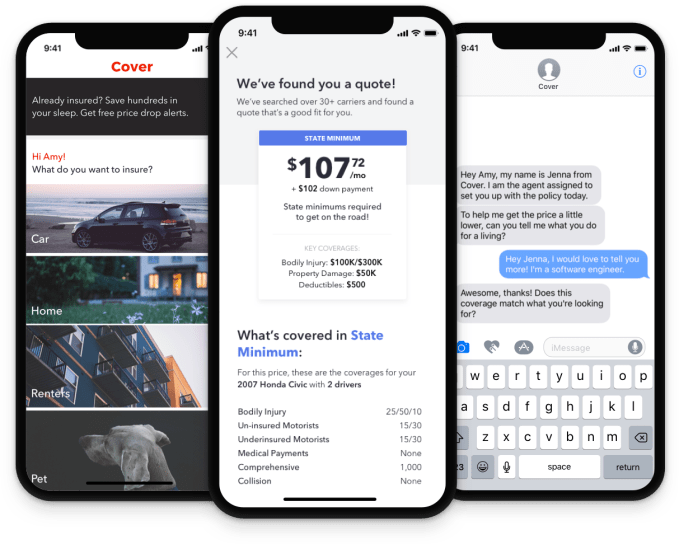

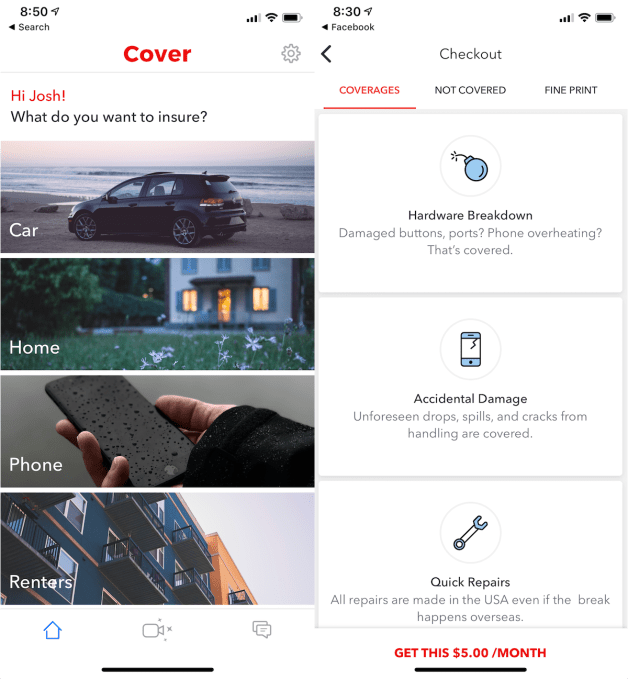

People procrastinate about buying insurance because it’s such a boring and complicated chore to compare policies. But Cover combines plans from 45 insurance companies into a single marketplace so it’s easy to find the best one for your car, home, rental, business, personal property, pets, jewelry and more. Now Cover is building powerful onboarding tricks like a driving school that earns you lower car insurance rates, and a way for Shopify merchants to sell warranties for their items.

The potential to use tech to run circles around the old insurance brokers has attracted a new $16 million Series B for Cover led by Tribe Capital’s Arjun Sethi, who led the Series A and sits on the startup’s board. The round was joined by Y Combinator, Social Capital, Exor and Samsung, and brings the company to a total of $27.1 million in funding.

“Insurance isn’t very different from being a white-collar bookie, where the house’s rake is too high and the dollars at stake are in the hundreds of billions in the U.S. alone,” says co-founder and CEO Karn Saroya. “This, all to the detriment of regular people, who view insurance as a tax. We’re here to change that perception.”

Saroya and his co-founders have deep ties. He went to high school with Anand Dhillon, is engaged to Natalie Gray and hired Ben Aneesh at the team’s previous startup, a high-end fashion marketplace called StyleKick that was eventually acqui-hired by Shopify. “We were tossing around ideas for what we wanted to do after StyleKick/Shopify, running hackathons on weekends. We built a couple different apps, but Cover — the MVP, where we just asked potential customers to take pictures of things they wanted to insure, surprised us” says Saroya. “Our customers sent us walkthroughs of their homes, pictures of their dogs and videos of themselves washing their cars. When you come across behavior that violates your expectations in consumers, that’s usually when you double-down.”

Cover co-founder and CEO Karn Saroya

So they built Cover, where you don’t have to cobble together an endless set of insurance websites or wait on hold. You download the app, pick your item, list how much you paid and where, provide some photos or video of its condition using its TensorFlow-equipped camera and Cover will check across its insurance partners and find you the best quote instantly. You can easily see what is and isn’t covered, learn how to make claims, and text with an agent if you have questions. For example, I was quickly quoted $5 per month to insure my new iPhone against damage but not loss or theft.

Cover earns between 10 to 35 percent per dollar of premium you pay. Its annualized premium already exceeds $8.5 million and is growing 30 percent per month. Thanks to its low-churn business model, easy cross-promotion of products, low training requirements for customers and no need to constantly update its existing subscriptions, Cover starts to look like a very efficient software-as-a-service business.

The big question remains whether Cover can consistently find the best rates for customers so they don’t second guess its quotes and search somewhere else. It will have to outcompete multi-insurance providers, like State Farm and Geico, as well as startups like MetroMile tackling specific insurance verticals with mobile apps. To really earn the big profits, Cover is building out its own in-house insurance plans. But that will put it under constant threat of insuring the wrong risks and ending up paying out too much.

“We built Cover because we saw an opportunity to build elegant products that could deliver on pricing and customer experience in a way that no incumbent insurance entity can,” Saroya concludes. By bringing the service to mobile and making it a seamless part of owning something, Cover could ensure you’re insured, even if insurance is the last thing you want to think about.

Powered by WPeMatico

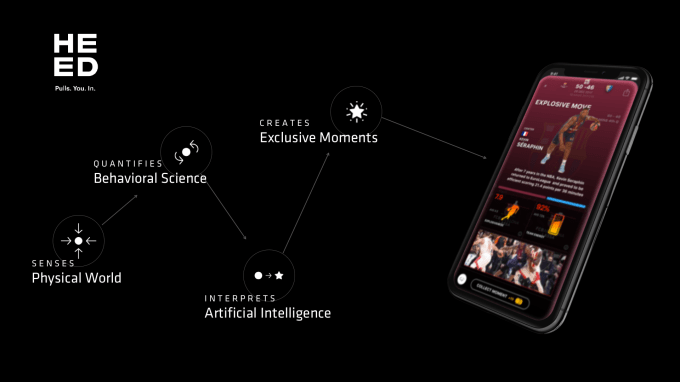

Heed, a startup looking to create new ways for sports leagues and clubs to engage with fans, is announcing that it has raised $35 million led by SoftBank Group International.

As laid out for me by CEO Danna Rabin, the company sits at the intersection of sports and IoT — which makes sense, since it was founded by Internet of Things company AGT International and talent agency Endeavor .

“Our primary mission is to connect the young audience with sports leagues and clubs,” Rabin said. “[Those] audiences are consuming less broadcast TV, consuming less of anything linearly. Sports clubs and brands are having more and more issues connecting with and reengaging those younger audiences.”

To create that connection, Heed places sensors around the match or game venue, even potentially on players’ clothing and equipment.

For example, the team let me make a couple punches using gloves with sensors inside, which were created for the mixed martial arts league UFC. Afterwards, I could see the measured force of each of my swings. (I didn’t really have any points of comparison, but I think it’s safe to say that my numbers weren’t too impressive.)

Rabin emphasized that Heed’s real focus isn’t on building fancy hardware, but rather on the artificial intelligence it uses to take that data (which can also be drawn from video and audio footage of the match) and transform it into a general narrative that can be viewed on the Heed smartphone app.

Pointing to the UFC glove, Rabin said, “We extract, only from this sensor, 70 different data points. What’s happening is, the fusion of these data points is what creates the stories.”

Put another way, the goal is to replace the generic commentary that you often get in sports coverage and live games with unique details about how the game or match is unfolding. Those aren’t just numbers like how hard someone is punching, but also inferences about a player’s emotional state based on the data.

“One of our core promises is that it’s not editorial driven,” Rabin added. “The AI is selecting what’s interesting in a match. Of course, we have a creative team that designs the formats, the visuals, how the packaging should look like, but that’s incorporated into the technology, which is automatically selecting the moments and creating the experiences with no human interpretation.”

So does Heed aim to be a technology provider or a sports media company of its own? Well, Rabin said it didn’t make sense to simply provide the tech to individual leagues or teams.

“A specific club does not have the breadth of technologies to keep evolving,” she said. Plus, she argued that the audience isn’t looking for just a one-off site with stories about one team, but an all-around destination where they can “get a bit of everything.”

In addition to the UFC, Heed is also working with EuroLeague (the European basketball league), various soccer clubs and Professional Bull Riding. In the latter case, it’s not just creating content, but actually working with the organization to create a more automated and objective form of judging.

“By leveraging AI and IoT, HEED has developed a unique platform that is changing the way fans watch and interact with sports,” said Softbank President and CFO Alok Sama. “HEED is taking a traditionally static experience and providing fans with deeper insights into the physical and emotional aspects of the sporting event by gathering and analyzing large, complex data in real time.”

Powered by WPeMatico

Serverless has become a big buzzword of late, and with good reason. It has the potential to completely alter how developers write code. They can simply write a series of event triggers, while letting the cloud vendor worry about providing whatever amount of compute resources are required to complete the job. It represents a huge shift in how programs are developed, but it’s been difficult to find companies who were built from the ground up using this methodology because it’s fairly new.

Blissfully, a startup that helps customers manage their Software-as-a-Service usage inside their companies, is one company that decided to do just that. Aaron White, co-founder and CTO, says that when he was building early versions of Blissfully, he found he needed quick bursts of compute power to deliver a list of all the SaaS products an organization is using.

He figured he could set aside a bunch of servers to provide that burst of power as needed, but that would have required a ton of overhead on his part to manage. At this point, he was a lone programmer trying to prove his SaaS management idea was even possible. As he looked at the pros and cons of serverless versus traditional virtual machines, he began to see serverless as a viable approach.

What he learned along the way was that serverless offers many advantages to a company with a bursty approach like Blissfully, scaling up and down as needed. But it isn’t perfect and there are issues around management and tooling and handling the pros and cons of that scaling ability that he had to learn about on the fly, especially coming in as early as he did with this approach.

Blissfully is a service where serverless made a lot of sense. It wouldn’t have to manage or pay for servers it wasn’t using. Nor would it have to worry about the underlying infrastructure at all. That would be up to the cloud provider, and it would only pay for the bursts as they happened.

Serverless is actually a misnomer, in that it doesn’t mean there are no servers. It actually means you don’t have to set up servers in order to run your program, which is a pretty mind-blowing transformation. In traditional programming you have to write your code and set up all the underlying hardware ahead of time, whether it’s in your data center or in the cloud. With serverless, you just write the code and the cloud provider handles all of that for you.

The way it works in practice is that programmers set up a series of event triggers, so when a certain thing happens, the cloud provider sees this and provides the necessary resources on demand. Most of the cloud vendors are offering this type of service, whether AWS Lambda, Azure Functions or Google Functions.

At this point, White began to think about serverless as a way of freeing him from thinking about managing and maintaining infrastructure and all that entailed. “I started thinking, let’s see how far we can take this. Can we really do absolutely everything serverless, and if so that reduces a ton of traditional DevOps-style work you have to do in practice. There’s still plenty, but that was the thinking at the beginning,” he said.

But there were issues, especially getting into serverless as early as he did. For starters, White needed to find developers who could work in this fashion, and in 2016 when it launched there weren’t a large number of people out there with serverless skills. White said he wasn’t looking for direct experience so much as people who were curious to learn and were flexible enough to deal with new technology, regardless of how Blissfully implemented that.

Once he figured out the basics, he needed to think about how this would work structurally. “Part of the challenge is figuring out where do you draw the boundaries between different serverless functions? How do you think about how much you want to overload the capability of one function versus another? How do you want to split it up? You could go way too specific, and you can of course, go way too broad. So there’s a lot of judgement calls to be made in terms of how you want to split your code base to work in this way,” he said.

The other challenge he faced going with a serverless approach so early was a dearth of tooling around it. White found Serverless, Inc. right way, which helped him with a basic framework for developing, but he lacked good logging tools and says that the company still struggles with this even now. “DevOps doesn’t go away. This is still running on a server somewhere (even if you don’t control that) and you will run into issues.” One such issue he calls a “cold start issue.”

Blissfully uses AWS Lambda, and as their customers require resources, it isn’t as though Amazon has a set of dedicated resources set aside waiting for such an event. If it needs to start servers cold, that could result in latency. To compensate for that, Blissfully runs a job that pings Lambda continually, so that it’s always ready to run the actual application, and there isn’t a lag time related to starting from scratch.

The other issue could be the opposite problem. You can scale much faster than you’re ready to deal with and that can be a problem for a small team. He says in that case, you want to put a limiter on the speed of the calls so you don’t end up spending more than you can afford, and it doesn’t scale beyond your team’s ability to manage it, “I think, in some ways, this actually accelerates you running into problems where you would normally be larger scale before you really had to think about them,” White said.

The other piece is that once Lambda gets everything going, it can move data faster than your external APIs can handle, and that could require limiters to actually slow things down. “I never had that problem in the past where I was provisioning so many computational resources that Google was yelling at me for being too fast. Being too fast for Google takes a lot of effort, but it doesn’t take a lot of effort with Lambda. When it does decide to spool up whatever resources, you can do some serious outbound damage to other APIs.” That meant he and his team actually had to think very early on about building sophisticated rate-limiting schemes.

As for costs, White estimates that his costs are much lower now that he has the service built and in place. “Our costs are so low right now, and far lower than if we had server-based infrastructure. Our computational pattern is very bursty.” That’s because it re-parses the SaaS database once a day or when the customer first signs up, and in between, usage is fairly low beyond interacting with the data.

“So for us that was perfect for serverless because I don’t really need to keep capacity around that would be pure waste.”

Powered by WPeMatico

Bespoke Post says it has more than 100,000 subscribers signed up to receive a monthly “box of awesome” (that’s what it calls its bundles of curated men’s products). Next up: Creating brands and products of its own.

It’s a common move for retailers and e-commerce companies to launch their own brands, but it sounds like Bespoke Post isn’t just looking to create generic versions of stuff you’re already buying.

Instead, it says its “brand development studio” the Foundry will identify opportunities for men’s products that don’t exist, work with manufacturers to create those products and improve them with feedback from Bespoke Post customers.

The company is also unveiling its first new brand, Base Light, which creates grooming products for men, starting with a line of bar soaps. How is this different from any other soap? Bespoke Post says the bars are handmade in the United States, without “harsh” ingredients like synthetic dyes, parabens, sulfates or phthalates.

Base Light soaps are available for purchase individually, or as part of the company’s Refresh Grooming Box. There also are plans to launch Base Light-branded face wash, face scrub, face moisturizer, shampoo, conditioner, body wash and beard oil products this fall.

“Each month, we deliver hundreds of thousands of unique box experiences filled with everything from apparel and grooming products to home goods and cocktail kits,” said Bespoke Post co-founder Rishi Prabhu in the announcement. “We know the kinds of products our customers will love and can spot market opportunities for products that don’t exist yet.”

Bespoke Post says it will also launch brands in categories like homewares, apparel and shoe care.

Powered by WPeMatico

The HRP-5P is a humanoid robot from Japan’s Advanced Industrial Science and Technology institute that can perform common construction tasks including — as we see above — install drywall.

HRP-5P — maybe we can call it Herb? — uses environmental measurement, object detection and motion planning to perform various tasks. In this video we see it use small hooks to grab the wallboard and slide it off onto the floor. Then, with a bit of maneuvering, it’s able to place the board against the joists and drill them in place.

“By utilizing HRP-5P as a development platform of industry-academia collaboration, it is expected that research and development for practical use of humanoid robots in building construction sites and assembly of large structures such as aircraft and ships will be accelerated,” write the creators.

The researchers see the robot as a replacement for an aging population and a declining birth rate. “It is expected that many industries such as the construction industry will fall into serious manual shortages in the future, and it is urgent to solve this problem by robot technology,” the write. “Also, at work sites assembling very large structures such as building sites and assembling of aircraft / ships, workers are carrying out dangerous heavy work, and it is desired to replace these tasks with robot technology. However, at the assembly site of these large structures, it is difficult to develop a work environment tailored to the robot, and the introduction of robots has not progressed.”

Considering there are 6 million contractors in the U.S. alone, robots like this one could be a boon or a curse. What happens when we can easily replace humans in shipping, logistics and construction? Let’s just hope Herb here needs a supervisor.

Powered by WPeMatico

Ettitude, recently graduated from the ERA accelerator, is looking to ride the growing wave of e-commerce by offering eco-friendly sheets.

The company offers bamboo lyocell sheets and pajamas, which feel like a hybrid between silk and cotton, and stay cool longer than cotton or other fabrics.

Bamboo lyocell fabric is essentially organic fabric made from weaving together tiny fibers of organic bamboo material or pulp. Ettitude says that the fiber yield per acre from bamboo is about 10 times higher than cotton and requires less than 10 percent of the water to grow.

I tried out the Ettitude sheets and found that they were indeed soft and kept me cool in the hot NYC summer, but they also require slightly more attentive laundering. Ettitude sheets should be washed in cold water and separately (or in a laundry bag), which is a slight departure from throwing your sheets in with the regular wash.

Still, the company is growing. Ettitude, a predominantly bootstrapped company, first launched in Australia and gained traction via ecommerce channels. Late this summer, the company launched in the U.S. and has sold “tens of thousands” of units, with a 20 percent month over month growth rate.

Ettitude has taken some investment from friends and family, and also received $100,000 in investment from Entrepreneurs Roundtable Accelerator .

While the consumer side of the business seems to be growing, Ettitude is also receiving inbound requests from enterprise brands such as airlines to get involved with the brand. Qantas, the largest airline in Australia, has started selling Ettitude in its online portal to frequent fliers.

Ettitude Queen set sheets cost $178.

Powered by WPeMatico

I’d like to meet some high-tech folks in Vancouver this week and I need your help. I’d like to hold a micro meet up at about 7pm on October 4 and I need a recommended place. If we can manage it we might be able to have a pitch off as well so let me know if you Vancouverians (Vancouverites?) know of any place with a bar and maybe a little stage and a microphone.

Please let me know if you can think of any good spots and I’ll finalize the meetup tomorrow. Email me at john@techcrunch.com or Tweet me @johnbiggs with ideas/help. If you’d like to pitch please fill this out. I’ll contact the people who are selected to pitch on Wednesday.

See you soon, eh!

Powered by WPeMatico