Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Venture capitalists aren’t supposed to make their portfolio companies battle to the death. There’s a long-standing but unofficial rule that investors shouldn’t fund multiple competitors in the same space. Conflicts of interest could arise, information about one startup’s strategy could be improperly shared with the other, and the companies could become suspicious of advice provided by their investors. That leads to problems down the line for VCs, as founders may avoid them if they fear the firm might fund their rival down the line.

SoftBank shatters that norm with its juggernaut $100 billion Vision Fund plus its Innovation Fund. The investor hasn’t been shy about funding multiple sides of the same fight.

The problem is that SoftBank’s power distorts the market dynamics. Startups might take exploitative deals from the firm under the threat that they’ll be outspent whoever is willing to take the term sheet. That can hurt employees, especially ones joining later, who might have a reduced chance for a meaningful exit. SoftBank could advocate for mergers, acquisitions, or product differentiation that boost its odds of reaping a fortune at the expense of the startups’ potential.

Powered by WPeMatico

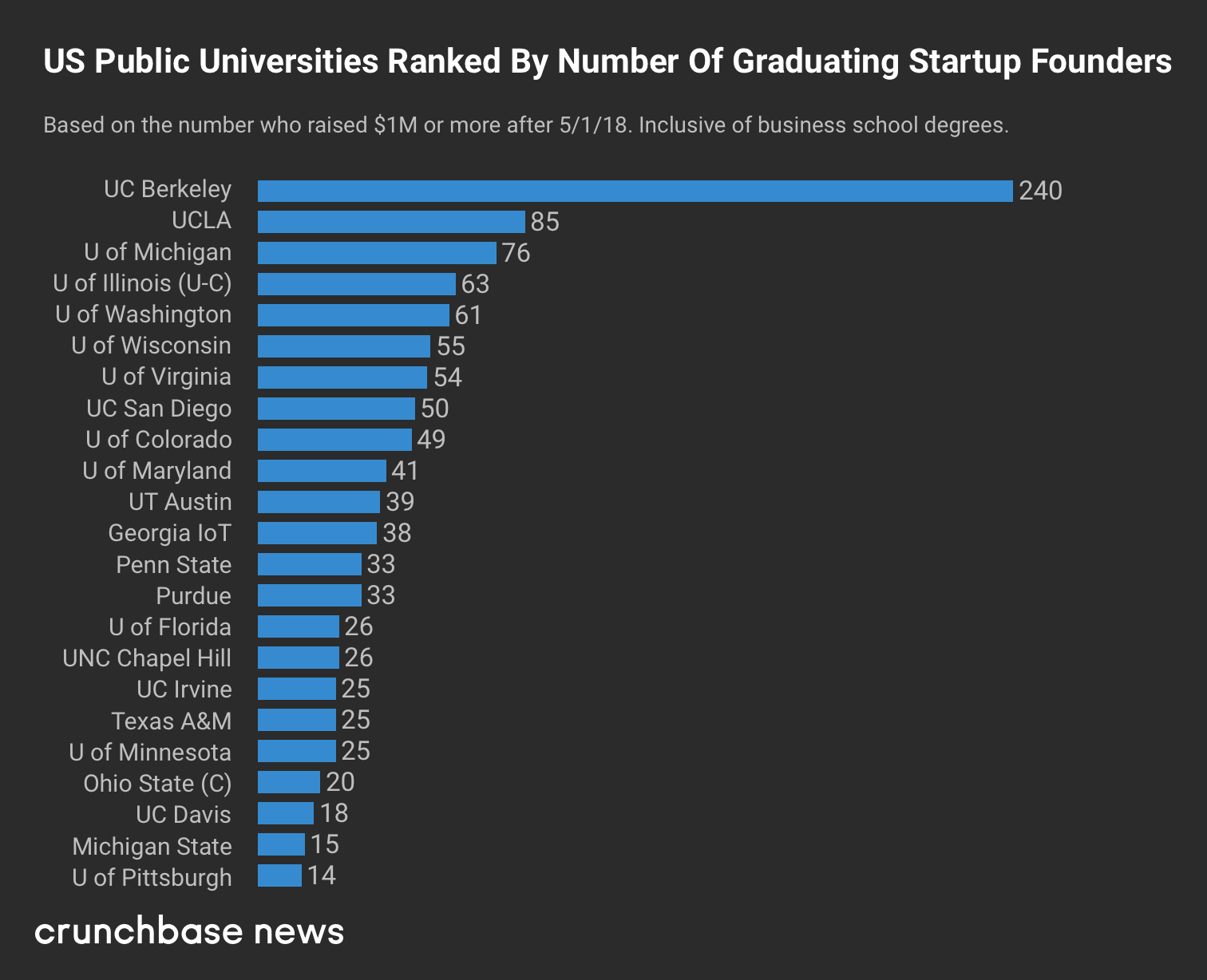

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s most noteworthy venture deals, fundraises, M&A transactions and trends. Let’s take a quick moment to catch up. Last week, I wrote about an alternative to venture capital called revenue-based financing and before that, I jotted down some notes on one of VCs’ favorite spaces: cannabis tech. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

This week, I want to share some thoughts — questions, rather — on beverages. Just as my inbox has been full of cannabis-related pitches, it’s also been packed with descriptions of new…drinks. Perhaps the most noted so far is Liquid Death, canned water for the punk rock crowd, because why not? Liquid Death has attracted nearly $2 million in funding from angel investors like Away co-founder Jen Rubio and Twitter co-founder Biz Stone. Before I tell you about a few other up-and-coming beverage makers, I must beg the question: Does the beverage industry need disrupting?

Founders say yes. Why? For one, because millennials, according to various studies, are consuming less alcohol than previous generations and are therefore seeking non-alcoholic beverage alternatives. Enter Seedlip, a non-alcoholic spirits company, for example. Or Haus, launching this summer, an all-natural apéritif distilled from grapes that has a lower alcohol content than most hard liquors. Haus, like any good consumer startup in 2019, is shipped directly to your door.

Beverages are being disrupted, there’s no stopping it. pic.twitter.com/DMEg88t4iO

— Kate Clark (@KateClarkTweets) May 21, 2019

Bev, a canned wine business that recently raised $7 million in seed funding from Founders Fund, thinks marketing in the alcohol industry is the problem. Founder Alix Peabody designed a line of female-focused canned rosé. If you’re wondering why alcohol needs to be gendered in such a way, you’re not alone. Peabody explained most alcohol brands cater to men, and that’s a problem.

“The joke I like to make is there’s a go-to type of alcohol for every type of bro and we just don’t have that for women,” Peabody told TechCrunch earlier this year.

Finally, the wellness movement is taking over, driving VCs toward some odd upstarts. From wellness chat and journaling apps to therapy substitutes to fitness companies, stick wellness in a pitch and investors will take a second look. More Labs, for example, is backed with $8 million in VC funding. The company is readying the launch of Liquid Focus, a biohacking-beverage that claims to “solve modern-day stressors without the negative side effects.” Finally, Elements, “an elevated functional wellness beverage formulated with clinical levels of adaptogens to give your body exactly what it needs in four categories (focus, vitality, calm, and rest) for specific cognitive functions” (damn, what copy), recently launched. It doesn’t appear to be funded yet, but let’s just give it a few months.

There’s more where that came from, but I’m done for now. On to other news.

I almost skipped IPO corner this week because no big-name companies dropped or amended their S-1s or completed a highly anticipated IPO, as has been the case basically every week of 2019. But I decided I better give a quick update on Luckin Coffee’s tough second week on the stock market. Luckin Coffee, if you aren’t familiar, is Starbucks’ Chinese rival. The company raised more than $550 million after pricing at $17 per share a little over a week ago. Immediately the stock skyrocketed 20 percent to a roughly $5 billion market cap; then came concerns of the company’s lofty valuation, major cash burn and uncertain path to profitability. Luckin has dropped around 25 percent since closing its debut trading day. It closed Friday down 3 percent.

Y Combinator, the popular accelerator program and investment firm announced this week that it has promoted longtime partner Geoff Ralston to president. This comes two months after former president Sam Altman stepped down to focus his efforts full-time on OpenAI. The promotion of Ralston is an unsurprising choice for YC, an organization that employs roughly 60 people, many of whom have been affiliated with it in one way or another for years.

Automattic acquires subscription payment company Prospress

Shopify quietly acquires Handshake, an e-commerce platform for B2B wholesale purchasing

Streem buys Selerio in an effort to boost its AR conferencing tech

As Amex scoops up Resy, a look at its acquisition history

The Los Angeles ecosystem is $76 million stronger this week as Fika Ventures, a seed-stage venture capital firm, announced its sophomore investment fund. Fika invests roughly half of its capital exclusively in startups headquartered in LA, with a particular fondness for B2B, enterprise and fintech companies. The firm was launched in 2017 by general partners Eva Ho and TX Zhuo, formerly of Susa Ventures and Karlin Ventures, respectively. The pair raised $41 million for the debut effort, opting to nearly double that number the second time around as a means to participate in more follow-on fundings.

DoorDash raises $600M at a $12.7B valuation

TransferWise completes $292M secondary round at a $3.5B valuation

Auth0 raises $103M, pushes its valuation over $1B

Canva gets $70M at a $2.5B valuation

Payment card startup Marqeta confirms $260M round at close to $2B valuation

Modsy scores $37M to virtually design your home

Sun Basket whips up $30M Series E

Zero raises $20M from NEA for a credit card that works like debit

Nigeria’s Gokada raises $5.3M for its motorcycle ride-hail biz

Our premium subscription service had another great week of interesting deep dives. This week, TechCrunch’s Lucas Matney went deep on Getaround’s acquisition of Drivy for his latest installment of The Exit, a new series at TechCrunch where we chat with VCs who were in the right place at the right time and made the right call on an investment that paid off. Here are some of the other Extra Crunch pieces that stood out this week:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I discuss how startups are avoiding IPOs and VC’s insatiable interest in food delivery startups.

Powered by WPeMatico

With a growing number of challenger banks taking on the U.S. market, one of the original startup banks, Simple — now owned by BBVA — has taken the unusual step of removing a core banking feature: bill pay. The company claimed the feature was under-utilized and usage was trending downwards, which is why it decided to sunset the option to pay bills through its app. That decision, not surprisingly, has angered a number of customers who are taking to social media and online forums like Reddit, threatening to switch banks as a result.

It’s likely true that fewer people today use bill pay than in the past.

The feature is something of a holdover from an earlier era before electronic payment options and auto pay became as ubiquitous as they are now. And many customers may still have bill pay set up even though another electronic option has since become available. Or they may not want to take the time to reconfigure things, when what they have works.

But despite bill pay’s waning usage, it’s odd to shut down such a commonplace banking feature. It’s rare to find a bank that doesn’t offer bill pay services, in fact, outside of a handful of smaller up-and-comers that aren’t full-service banks.

Even most of the newer U.S. fintech players like Chime, Qapital, SoFi Money, Varo, Aspiration and others offer bill pay services where they mail a check for you. And it’s common among more traditional online banks like Ally, as well.

Removing bill pay also greatly impacts those who pay their rent by way of a mailed check, as many landlords are not set up for electronic payments. This is a recurring complaint among the customers who are lambasting Simple for its decision.

Instead, these customers will now have to purchase Simple’s newly available paper checks (sold in packs of 25 for $5 — oh, what a timely launch!).

They’ll then need to buy stamps, address envelopes, fill out checks and actually mail them.

Postal mail, of course, is not preferred by today’s younger generation — many of whom never had to write letters, having grown up in the internet age. Millennials have even complained that the very act of having to mail things gives them anxiety, due to all the steps involved and their overall unfamiliarity with the process.

I use bill pay to support a family member.

You’re saying “paper checks will put me in control” but really what that means is that I now have something that previously was automatically handled and no I have to manually do it.

I was in control prior, you’re just taking it away

— Jonah Moses (@jonahmoses) May 19, 2019

Considering that banks like Simple are targeting the millennial customer, forcing them back to checks they have to mail themselves is not the smartest move — at least from a public relations perspective.

On top of all this, Simple’s announcement about the discontinuation of bill pay was not well-communicated. As it touted the arrival of paper checks, an email footer also quietly noted that bill bay would also shut down after July 9, 2019. Customers dinged Simple for its lack of transparency.

In the spirit of transparency, @simple should also let its users know that Bill Pay is going away. Proof here (from an email from them) pic.twitter.com/LuDmnHJIA2

— BC (@bcurielv) May 7, 2019

The company claimed it was sending emails about bill pay to customers — but many didn’t receive any message before learning of the change on Twitter. And they were angry.

Since the decision was announced, Simple has been dutifully responding to customers’ complaints on Twitter, sometimes with smiley emojis and cheerful customer service-ese, like: “We hear ya. Mailing payments for bills can be nerve wracking.”

The company even wished one customer well on their journey to find another bank.

No…..you aren’t hearing us….that’s the problem.

— Rebecca Ford (@rebannford) May 9, 2019

We do now offer paper checks for folks who want them, and many of our customers set up automatic withdrawals from the biller’s websites for their bill payments. But if you decide to look for a new bank partner, we wish you the best.

-DG

— Simple (@simple) May 23, 2019

In addition to declining usage, the company said its newer Expenses feature was not working well with Bill Pay, which was another factor in its decision.

Good question – both are true. We knew that our existing bill pay process wasn’t working well with our expenses feature, so combined with the low usage rates we decided to end it. Hope that helps to clarify! ^BC

— Simple (@simple) May 19, 2019

Predictably, the volume of customer complaints has led to the creation of a Change.org petition.

Things are now going so badly that Simple just sent customers another email in response to all the backlash. In it, the company acknowledges how unhappy customers are about its decision and its handling of the news.

“To be completely transparent, a really small percentage of our customers use Bill Pay,” the email reads. “With this service’s usage declining, we made the decision to sunset it. This allows us to use those resources to build new features that benefit a broader number of customers. We know that some of you aren’t happy about this decision or how we broke the news, and for that, we’re sorry.”

The decision, however, still stands.

Simple was one of the original innovators in online banking. But after its acquisition, the pace of innovation has decreased and customer growth has stagnated. Over the years, the company has been maligned for not allowing non-U.S. citizens to sign up and for shutting down customers’ accounts with little notice, due to transition issues.

Now it’s angering customers again just as a number of new, millennial-focused online banks are hitting the market — and as challenger banks from Europe, like N26 and Revolut, are preparing to make the jump to the U.S. That may not be the best time to send a core group of users in search of alternatives.

The full email sent to customers is below:

You probably heard this already but if you haven’t: Simple’s “Pay a bill” and “Mail a check” features (also known as “Bill Pay”) are going away on or after July 9. If you have a payment scheduled on or after that date, it will not be paid or sent.

To be completely transparent, a really small percentage of our customers use Bill Pay. With this service’s usage declining, we made the decision to sunset it. This allows us to use those resources to build new features that benefit a broader number of customers.

We know that some of you aren’t happy about this decision or how we broke the news, and for that, we’re sorry.

We’ll continue to be in touch over the coming weeks. In the meantime, if you have any questions, we’re reachable via a support message or at (888) 248-0632.

Thanks,

— The Team at Simple

Simple has been offered the opportunity to comment.

Powered by WPeMatico

Every company’s online acquisition strategy is out in the open. If you know where to look.

This post shows you exactly where to look, and how to reverse engineer their growth tactics.

Why is this important? Competitive analysis de-risks your own growth experiments: You find the best growth ideas to adopt and the worst ones to avoid.

First, a warning: Your goal is not to repurpose another company’s hard work. That makes you a thief. Your goal is to identify other companies who face the same growth challenges as you, then to study their approaches for solutions to draw from.

As I walk through uncovering a competitor’s tactics, keep in mind which competitors are worth looking at: For instance, you should rarely over-analyze early-stage companies. They’re unlikely to be methodical at growth.

Meaning, if you blindly copy their site and their ads, it’s possible you’ll be copying tactics that are not actually responsible for their growth. Their success may instead be from network effects or other hidden factors.

Instead, it’s safest to get inspiration from companies who’ve sustained high growth rates for a long time, and who face the same growth challenges as you. They’re likely to have sophisticated growth operations worth studying deeply. Examples include:

If these aren’t your direct competitors, don’t worry. You don’t need to audit a direct competitor’s tactics to get incredibly valuable insights.

You’ll gain useful insights from auditing the user acquisition funnel of any company who has a similar audience and business model.

Examples of audiences:

Audiences matter because their behaviors and needs differ wildly. Each requires its own growth strategy. You want to audit a company whose audiences is similar to yours.

You also want to ensure the company shares your business model. Examples include:

Each model may necessitate different ads, landing pages, automated emails, and sales collateral.

Never implement another company’s tactics blindly.

There’s an effective process for growth analysis, and it looks like this:

Here’s a brief example before we dive into tactics.

Let’s pretend we’re a SaaS company offering consumer banking tools, and that we’re struggling to get users to onboard our app. Our hypothesis is that visitors are bouncing because they don’t trust us with their sensitive information.

Our first step is to define both our audience and our business model:

Our next step is to look for companies who share those two aspects. (We can find them on Crunchbase.)

Once we have a few in hand, we look for how they handle customers’ sensitive information throughout their funnel. Specifically, we audit their:

It’s time to learn how we audit all that. I’ll share how our marketer training program teaches marketers to do this on the job.

Powered by WPeMatico

Erik Finman is a twenty-something bitcoin maximalist as famous for his precocity as he is for his $12 bet on the currency a few years ago.

Now, Finman, who built his first company while still in high school, is launching a new startup called CoinBits, which allows users to passively invest in bitcoin.

The idea, according to Finman, is to democratize access to the currency by letting everyday folks invest nominal sums through well-known mechanisms like roundups on transactions made with a credit or debit card or through regular transactions from a customer’s savings or checking account to bitcoin through CoinBits.

Every transaction also helps Finman’s own bitcoin holdings grow, and makes the young entrepreneur a little wealthier himself through his bitcoin holdings.

Users can make one-time investments of $10, $25, $50 or $100 through the web-based platform and can establish a level of risk for their holdings.

Finman’s app collects no commissions on transactions, and 98% of the bitcoin is stored offline — for safety.

“Overall, investing in bitcoin is complicated and can feel almost impossible,” said Finman. “Coinbits allows you to put that spare change in bitcoin. For example, if you spend $1.75 on French fries, that remaining 25 cents is invested automatically.”

Withdrawals are handled by CoinBits, which will give users same-day processing for a 50 cent-fee, and offers an easily downloadable record for accountants to deal with any gains or losses associated with bitcoin.

Given the fractional nature of these investments, and the volatility of bitcoin, it’s hard to know what real value investors can reap from these small transactions, but it’s a less risky way to experiment with building bitcoin holdings than take a huge flyer on the market.

Powered by WPeMatico

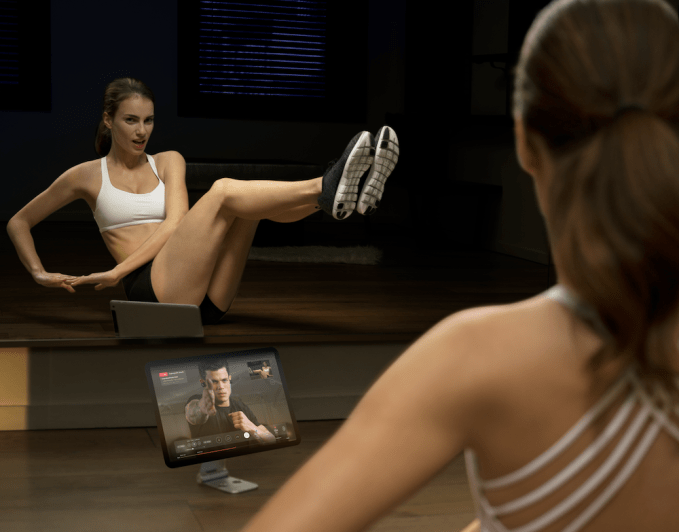

Livekick, a startup that gives customers access to one-on-one personal training and yoga from their home (or hotel room, or elsewhere), is announcing that it has raised $3 million in seed funding.

The company was founded by entrepreneur Yarden Tadmor and fitness expert Shayna Schmidt. Tadmor said that with all his travel for work, his fitness routine “really eroded,” so he contacted Schmidt and asked her to train him remotely — they’d connect via FaceTime, he’d mount his phone at the gym and she’d supervise his workout.

“We trained this way for a while, and then we realized: Hey, this is something that other people can really benefit from,” Tadmor said.

So with Livekick, users can sign up for one, two or three live, 30-minute sessions with a remote trainer, who they’ll connect with via the Livekick iOS app or website. (After a two-week trial, pricing starts at $32 per week.) The workouts will be tailored to the space and equipment that you have access to, and the trainers will also assign other workouts for the rest of the week.

Tadmor and Schmidt contrasted this approach with companies like Peloton and Mirror, which are bringing new exercise equipment and classes into the home, but which don’t offer one-on-one interaction with a trainer. Tadmor said this individualized approach is not just better-tailored to each user’s needs, but also more effective at keeping them motivated. And Schmidt said the live interaction also ensures that people are doing their workouts correctly and safely.

As for the trainers, Schmidt said this gives them a new way to find clients, particularly during their off-hours.

“For trainers, the hours that users are never booked are usually noon to 4pm — they never get a client because people are at work, obviously,” she said. “So we can give trainers in London those hours because for a user in New York, that’s morning. We can really fill their schedules [and] help them make some more income.”

Beyond consumer subscriptions, Livekick also offers a corporate program called Livekick for Work. And just to be clear, the service isn’t just for frequent travelers, as Tadmor noted: “If you live in New York, you have access to a lot of fitness options, but most people don’t. You’ve got to do a lot of commuting to get to a studio with great trainers, and so part of what we’re trying to bring is really let you do that from the comfort of your home.”

And while we recently covered the launch of a similar service called Future, Livekick actually launched in September, and Tadmor said the average retention rate has been over six months.

The round was led by Firstime VC, with participation from Rhodium and Draper Frontier.

“With its leading technology and ethos to make exercise accessible and affordable, we believe Livekick has the capacity to improve the lives and health of millions,” said Firstime’s Nir Tarlovsky in a statement.

Powered by WPeMatico

On January 12, 2016, Grindr announced it had sold a 60% controlling stake in the company to Beijing Kunlun Tech, a Chinese gaming firm, valuing the company at $155 million. Champagne bottles were surely popped at the small-ish firm.

Though not at a unicorn-level valuation, the 9-figure exit was still respectable and signaled a bright future for the gay hookup app. Indeed, two years later, Kunlun bought the rest of the firm at more than double the valuation and was planning a public offering for Grindr.

On March 27, 2019, it all fell apart. Kunlun was putting Grindr up for sale instead.

What went wrong? It wasn’t that Grindr’s business ground to a halt. By all accounts, its business seems to actually be growing. The problem was that Kunlun owning Grindr was viewed as a threat to national security. Consequently, CFIUS, or the Committee for Foreign Investment in the United States, stepped in to block the transaction.

So what changed? CFIUS was expanded by FIRRMA, or the Foreign Risk Review Modernization Act, in late 2018, which gave it massive new power and scale. Unlike before, FIRRMA gave CFIUS a technology focus. So now CFIUS isn’t just an American problem—it’s an American tech problem. And in the coming years, it will transform venture capital, Chinese involvement in US tech, and maybe even startups as we know it.

Here’s a closer look at how it all fits together.

Image via Getty Images / Busà Photography

CFIUS is the most important agency you’ve never heard of, and until recently it wasn’t even more than a committee. In essence, CFIUS has the ability to stop foreign entities, called “covered entities,” from acquiring companies when it could adversely affect national security—a “covered transaction.”

Once a filing is made, CFIUS investigates the transaction and both parties, which can take over a month in its first pass. From there, the company and CFIUS enter a negotiation to see if they can resolve any issues.

Powered by WPeMatico

In the first few days following Luckin Coffee’s initial public offering, the stock chart for LK looked like a roller coaster. Now it’s looking more like a free fall.

The Chinese Coffee chain successfully completed its highly anticipated offering roughly a week ago, raising more than $550 million after pricing at $17 per share, the high end of its $15-$17 per share range.

Luckin was met with a warm reception from the markets, with the stock skyrocketing roughly 20% to a greater than $5 billion market cap in its first day of trading. However, concerns over the company’s lofty valuation, major cash burn and uncertain path to profitability have caused the stock to nosedive since.

Luckin has dropped around 25% since closing its debut trading day at $20.38 per share, and 40% from its intraday peak of $25.96. As of Friday’s open, Luckin stock sat at $15.44, now well below its IPO price.

Leading into the IPO, Luckin had already been the topic of much debate. Luckin had filed for its public offering just a year and a half after its founding. And prior to its filing, Luckin had raised more than $500 million in venture capital through four fundraising rounds that all occurred just within roughly one year’s time, per PitchBook and Crunchbase data.

As Luckin’s valuation continued to level up, many questioned the sustainability of its business model and heavily discounted pricing strategy, with Luckin’s limited operating history already pointing to substantial losses and heavy cash outflows.

The concerns have followed Luckin into the public markets, and it’s unclear whether the stock’s early struggles are just growing pains or a broader indication that public investors have limits to the levels of nascency and unprofitability they are willing to accept and bet capital on.

As one of the few publicly traded early-stage growth companies, and likely the only one in the “coffee” vertical, Luckin lacks similar companies for investors to compare the stock to and also seems to lack a natural investor base — with the story a bit too foreign for typical tech sector investors and a bit too hectic for your typical food and beverage investor.

What is clear is that much is still misunderstood regarding the company’s unique history, its growth strategy, local market dynamics or otherwise. We’ll continue to keep an eye on Luckin stock to see whether the picture gets a bit brighter once investors get more comfortable with the story and as management proves its ability to execute.

For now, check out articles on Extra Crunch written by TechCrunch’s Danny Crichton and Rita Liao for deep dive primers into Luckin and all its moving parts.

Powered by WPeMatico

Starbucks plans to double its store count in China to 5,000 in 2021 and Luckin, a one-year-old coffee startup, is matching up by aiming to reach 4,500 by the end of this year. Luckin’s upsized $651 million flotation has brought American investors’ attention to this potential Starbucks rival in China, where the Seattle giant controlled over half of the coffee market as late as 2017. But as soon as you make your first purchase with Luckin, you realize its ultimate goal may not be to topple Starbucks.

To get your caffeine intake from Luckin, the ordering process happens entirely on its app. First, you will decide how you want to fetch the drink: have it delivered within 30 minutes, pick it up at a nearby Luckin kiosk, or sit back and sip at one of its full-on cafes, or what it calls ‘relax stores.’

Say you’re tied up at the desk, you can input your location to check if you’re within Luckin’s delivery radius. Luckin has essentially built a vast coffee delivery network through its partnership with one of China’s biggest courier services SF Express, which dispatch staff to ferry the drinks on scoot fleets. You then place the order, choosing from a range of drinks and customizing it — hot or cold, the amount of sugar and portions of creamer, the type of syrup flavor and the likes. When you get to the end, Luckin will ask you to pay via its app. If you’re a first-time user, you get a ‘first order free’ voucher, a common strategy for many Chinese consumer-facing apps to lure new users.

You then place the order, choosing from a range of drinks and customizing it — hot or cold, the amount of sugar and portions of creamer, the type of syrup flavor and the likes. When you get to the end, Luckin will ask you to pay via its app. If you’re a first-time user, you get a ‘first order free’ voucher, a common strategy for many Chinese consumer-facing apps to lure new users.

Powered by WPeMatico