Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

This is it, code jockeys — your last call to grab a seat and compete in the TC Hackathon at Disrupt Berlin 2019 on 11-12 December. We limited participation to 500 people and, with just eight days to go, only a few spots remain. Do you have the skills, stamina and creativity it takes to build a working product in less than 24 hours? Well, do ya? Then apply to the Hackathon today and snag one of the few remaining seats.

Competing in the Hackathon is free, plus we give every participant an Innovator pass to take in the show on day two. Sweet! When you’re done hacking, explore the early-stage startups exhibiting in Startup Alley, including the TC Top Picks. Be sure to catch some of our incredible speakers — you can use the Disrupt Berlin ’19 agenda to help you plan your time.

New to the TC Hackathon? Here’s how it works.

You join a team — either one you come with or one you find on site — and pick one of the sponsored challenges. Sponsors look for working solutions to real-world problems, and they pony up cash and prizes for the winning team(s). Plus, TechCrunch will award $5,000 to one team it deems to have created the best overall hack.

Hackers have roughly 24 sleep-deprived hours to work their magic — and we’ll have plenty of food, drink and caffeine on hand to fuel your genius. When the clock runs out, the judges review every completed project and choose 10 teams to move on to the finals on day two.

Those 10 bleary-eyed teams will have two minutes to pitch their creation to the judges — in front of a live audience on the Extra Crunch Stage. Then it’s time for the big reveal. First, the various sponsors announce their winners, then TechCrunch names the team it deems the best overall hack-at-the-thon. See what we did there?

We’ll announce specifics about this year’s sponsors and challenges soon. In the meantime, check out the other sponsored contests, prizes and winners from DSF ’18 to get a sense of what awaits you in Berlin.

Strut your skills, compete for cash, prizes, adulation and the pure joy of coding something into existence. But don’t wait, because we have only a few seats left. Apply to compete in the TC Hackathon, come to Disrupt Berlin 2019 on 11-12 December and show us what you can do.

Is your company interested in sponsoring or exhibiting at Disrupt Berlin 2019? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Podcorn, the service that connects brands with podcasters to acquire in-broadcast sponsored time (not pre- or post-roll advertising), is officially launching its services today.

“For brands, the benefit is that we are scaling the discovery of relevant podcasters of all sizes and making it possible to work with hundreds of really targeted podcasters within their niche at scale,” writes Podcorn co-founder Agnes Kozera. “Historically, if you look at programmatic pre-roll ads in video, programmatic wasn’t enough to sustain the creator ecosystem in terms of revenue and a lot of audiences skip those ads. And importantly, only a small portion of top creators end up making a sustainable income from programmatic because it is strictly based on impressions so smaller creators with niche but very engaged audiences don’t generate a sufficient amount of revenue.”

The company, which raised $2.2 million in a round of financing led by Global Founders Capital, with participation from Bessemer Venture Partners, 500 Startups, Alumni Ventures Group, Correlation Ventures and the investment firm Next 10 Ventures, was founded by Kozera and her high school friend, David Kierzkowski.

The two previously launched the influencer marketing company Famebit, which was acquired by Google three years after its launch — and after raising $1.5 million from 500 Startups and the Los Angeles-based incubator and early-stage investment firm, Science.

“[Podcasts] need alternative monetization such as native sponsorships (why influencer marketing blew up) because creators started making a lot more money from it than traditional ad formats because it takes into consideration other criteria that make their podcast valuable,” Kozera writes. “It also gives brands an opportunity to see the value of creators irrespective of size.”

Like the influencer marketing business which gave Kozera and Kierzowski their first exit, Podcorn connects brands with a range of different podcasting formats and manages the types of contracts these new media broadcasters can offer to increasingly targeted audiences that follow them.

It’s a strategy that’s been a boon for influencer marketing, and now that increasing numbers of ad dollars are going to podcasts, it was only a matter of time before the practice made its way into the new format.

Companies like Acast, Midroll, Audiogo and ThoughtLeaders are also all vying for a piece of the podcast advertising market.

“We are giving brands the opportunity to be part of the conversation, where listeners can hear from the brands – so not just pre, mid, and post-roll host read ads but brand interviews, panel discussions with experts and professionals who are within the brand’s industry,” Kozera wrote in an email.

Powered by WPeMatico

Uberflip is acquiring SnapApp, bringing together two startups that promise to help marketers use their content more effectively.

President and Chief Marketing Officer Randy Frisch argued that Uberflip focuses on content experience, not content marketing. In other words, it’s not selling productivity and workflow tools for marketers to write blog posts and create videos. Instead, it helps them present their existing content in a smarter and more personalized way.

For example, it worked with data warehousing company Snowflake to create content streams highlighting the topics most likely to grab the attention of different sales prospects, then embedded those content streams in Snowflake’s marketing emails.

“Content marketing has gotten a bad rap in some ways,” Frisch said, noting that there’s been “a lot of consolidation in that space in the last number of years,” so Uberflip has been working to distance itself from that term. (To that end, Frisch recently published a book with the colorful title “F#ck Content Marketing.”)

As for SnapApp, I wrote about the company’s interactive content tools back in 2015, but Uberflip CEO Yoav Schwartz told me that the product has changed dramatically in the last 18 months — it now offers “a better, smarter way to understand a visitor” by “peppering them with questions” as they’re browsing a marketer’s website.

So Schwartz sees this acquisition — Uberflip’s first — as a way to help the company improve its personalized content recommendations.

“We’re going to let SnapApp continue to run as is,” he added. “We’re not going to attempt to integrate on day one. We’re going to allow time to understand how those two technologies can work together.”

Frisch and Schwartz said that 10 to 15 SnapApp team members will be joining Uberflip, bringing the total headcount to around 150. And SnapApp’s current headquarters will become the Boston office of Toronto-based Uberflip.

The financial terms of the acquisition were not disclosed. SnapApp previously raised $22 million in funding, while Uberflip has raised $36 million.

Powered by WPeMatico

Salv, an anti-money laundering (AML) startup founded by former TransferWise and Skype employees, has raised $2 million in seed funding.

The round is led by Fly Ventures, alongside Passion Capital and Seedcamp. Angel investors also participating include N26 founder Maximilian Tayenthal (who seems to be doing quite a bit of angel investing), former Twilio CTO Ott Kaukver, and Taavi Kotka, former CIO for Estonia (the actual country!).

Founded in June 2018 and initially offering consultancy, Estonia-based Salv has built a software platform that helps banks find and stop financial crime. The idea, says co-founder and CEO Taavi Tamkivi, is to move AML beyond just compliance to something more proactive that actually does defeat crime. That’s quite the promise, although he and his co-founders have a lot experience to draw from, both within fast-growing startups and AML.

Tamkivi built the AML, fraud, and Know Your Customer (KYC) teams at TransferWise and Skype. COO Jeff McClelland also worked in the anti-fraud team at Skype, followed by a stint at TransferWise, first as an analyst and then in HR. And CTO Sergei Rumjantsev was also formerly at TransferWise, leading the engineering team responsible for KYC and verification.

“This was a highly demanding role, especially given how fast TransferWise was growing, how many new markets were coming online, and how central user verification is for compliance,” Tamkivi tells me. “Under Sergei’s leadership, the team made the verification process incredibly smooth over time for genuine customers. But also robust enough to protect TransferWise from on-boarding bad actors”.

Bad actors within financial services are aplenty, of course. Yet, despite the European banking sector spending billions tackling the problem, it is estimated that only 1-2% of global money-laundering is detected.

“AML should be all about stopping money laundering but, particularly in the last decade, layer upon layer of regulations have been added for banks to comply with,” says Tamkivi. “This would be great if that meant that there was no more money laundering, but sadly, that’s a long way off. Today, between $1-2 trillion a year is still laundered. But the excessive regulations mean that nearly all of a bank’s compliance team’s effort goes into compliance. They have very little energy left to actually focus on improving their financial crime-fighting abilities. The software they’re using is similar, focused almost wholly on compliance, not crime-fighting”.

That is where Salv wants to step in, and Tamkivi says the main difference between the startup’s AML software and other existing solutions is a much greater emphasis on crime-fighting rather than a box-ticking compliance exercise.

“We’re aiming to create a transformation similar to what’s happened in virus scanning,” he says. “10-15 years ago virus scanners on everyone’s PCs were an enormous hassle, consumed tons of resources and stopped you from getting work done. The same is true in financial institutions today. They’re using outdated, heavy software and processes to handle AML. But today, virus scanning still happens, but nobody’s worried about it. It happens in the background, with few resources. We’ll do the same in the AML world”.

In addition, the Salv CEO claims that the company’s software is faster than competitors’ offerings, both in terms of set up time and integration, and making changes to the rules the system adheres to.

“Our system, by contrast, takes a month or less to set up and minutes to modify the rules,” he says. “As a result, our customers can take everything they learn today from new criminal patterns, encode it in automated rules tomorrow, and repeat that cycle every day to protect their bank. Moving fast is the only way to keep up with the innovative organised criminals moving millions or billions around the world”.

To that end, Salv already counts Estonian bank LHV as its first customer. “They offer a full suite of banking products across Estonia,” says Tamkivi. “They’re also active in London, in particular, supporting fintechs. We have another couple of customers in the Lithuanian fintech scene. One of those is DeVere e-Money”.

More generally, Salv’s product is said to be suitable for Tier 2 and Tier 3 banks, as well as regulated fintechs and challenger banks.

Meanwhile, the business model is straightforward enough. Salv charges a monthly subscription, while the price varies based on the number of active customers a bank or fintech has.

Powered by WPeMatico

Vancouver-based mobility startup Damon Motorcycles has entered the EV arena with a preview of its first e-moto, the Hypersport Pro.

The seed-stage company had previously focused on creating digital safety technology — like its 360-degree radar detection system — to augment two-wheelers made by other manufacturers.

Damon has determined to create its own EV model designed to overcome common flaws it sees in existing motorcycle offerings.

“We are for the first time being black and white about the fact that we are a full-on producer and we have a motorcycle we’re going to unveil at CES,” Damon Motorcycle founder and CEO Jay Giraud told TechCrunch.

That machine is the fully electric Damon Hypersport Pro. The news is a pre-announcement ahead of the full January debut, so Giraud would not offer much in the way of core specs — such as price, range, charge-time and performance.

He was clear the motorcycle is meant to be a direct competitor to the latest e-motos released by Harley-Davidson and California-based venture Zero Motorcycles — and to the gas-motorcycle market overall.

“We’ve come at this and the motorcycle problem in a way that no other company has,” Giraud explained.

“We’re trying to change the industry by addressing the issues of safety and handling and comfort and the problems that have persisted with everyone in the industry, including all the e-moto companies today.”

Damon’s Hypersport Pro is designed around the company’s CoPilot system, which uses sensors, radar and cameras to detect and track moving objects around the motorcycle, including blind spots, and alert riders to danger.

Damon has also taken on the problem of one-size-fits-all in motorcycle design, integrating a system on its Hypersport Pro that allows for adjustable ergonomics. The startup’s debut model will allow riders to electronically shift the motorcycle’s windscreen, seat, footpegs and handlebars to accommodate for different positions and conditions — from more upright city riding to more aggressive high-speed runs.

Damon Motorcycles is taking pre-orders for its Hypersport Pro and will skip dealers, opting to use a direct-sales and service model similar to Tesla . The startup’s Vancouver facility is equipped to build 500 motorcycles a year, according to Giraud.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

Harley-Davidson released its first e-motorcycle — the $29K LiveWire — in 2019 and California EV startup Zero Motorcycles launched its $19K SR/F, both in bids to go take e-motos mass-market. Aside from the price-gap, both have comparable charge times (about an hour), performance and range (around 100 miles for combined city and highway riding).

The U.S. motorcycle industry has been in pretty bad shape since the recession. New sales dropped by roughly 50% since 2008 — with sharp declines in ownership by everyone under 40 — and have never recovered.

Harley-Davidon’s EV pivot is likely to bring e-moto offerings from the other large gas manufacturers, such as Honda and Yamaha, which are also attempting to revive sales to younger riders.

Harley-Davidson’s LiveWire

With Damon’s pivot to e-moto production, the startup is not alone. Italy’s Energica is expanding distribution of its high-performance EVs in the U.S. Other competitors include e-moto startup Fuell, with plans to release its $10K, 150-mile range Flow in the near future.

Of course, there have already been some speed bumps and market attrition, with three e-moto startups — Alta Motors, Mission Motors and Brammo — forced to power down over the last several years.

So how does Damon Motors plan to succeed as a new entrant in a motorcycle market with stagnant new bikes sales and increased EV competition from established OEMs and startups?

“We have so many advantages the others don’t have and we’re leveraging everyone of their weaknesses,” founder Jay Giraud said. The company’s direct-sale model will lend to more competitive pricing and higher margins for R&D, he said.

Then there are what Damon Motorcycles sees as its Hypersport Pro’s purposely designed comparative advantages over existing manufacturers.

“You’re gonna love the horsepower and range and all that good stuff, but that’s not what makes Damon different from every one else,” explained Giraud.

“What’s different is that it’s a safer motorbike with the safety features and transforming ergonomics that will keep you from smashing into someone’s car,” he said.

Not crashing into other people’s cars is certainly a compelling feature to offer in a motorcycle. Time and sales will ultimately tell how Damon fares in the inevitable cycle of events — profitability, failure, acquisition — that will play out in the increasingly competitive e-moto space.

Powered by WPeMatico

Xometry, the U.S.-based marketplace for on-demand manufacturing that raised $55 million in Series D funding this summer, has acquired Munich-based Shift as a path to European expansion.

Exact terms of the deal remain undisclosed, although the exit sees at least some of Shift’s investors, such as Cherry Ventures, picking up shares in Xometry . I also understand the Shift team is staying on and the company’s founders — Albert Belousov, Dmitry Kafidov and Alexander Belskiy — will now be heading up Xometry’s newly formed European business.

Specifically, via this acquisition, Xometry says it will accelerate international expansion into 12 new countries, leveraging a now worldwide network of over 4,000 manufacturers. The company’s on-demand manufacturing marketplace is already used by global companies like BMW and Bosch, which are Europe-based, and so it makes sense to have much stronger operations in the continent.

“We’re eager to leverage Xometry’s technology to continue to scale our business in Europe,” says Shift’s Kafidov in a statement. “We look forward to providing our customers additional manufacturing capabilities, including additive manufacturing and injection molding.”

Shift claims to have built the largest on-demand manufacturing network in Europe and a customer base that includes some of the leading manufacturing companies in the region. Now operating as Xometry Europe, the subsidiary will continue to be headquartered in Munich, Germany, an area known for its manufacturing heritage.

Cue statement from Christian Meermann, founding partner, Cherry Ventures: “The custom manufacturing industry is a massive global market of over $100 billion. We’re excited for Shift to utilize Xometry’s industry-leading technology as well as leverage the global manufacturing expertise from other Xometry investors, including BMW i Ventures and Robert Bosch Venture Capital.”

Xometry has raised $118 million since being founded in 2013. Over the past two years, the company has grown from 100 employees to over 300 while more than doubling revenue each year. Via its partner manufacturing facilities, the company offers CNC machining, 3D printing, sheet metal fabrication, injection molding and urethane casting.

Contrast that with Shift, which was founded in 2018 and had raised around €4 million (~$4.4 million) to date. Sources also tell me the startup had nearly closed a Series A round before Xometry preempted the investment by making an acquisition offer.

Powered by WPeMatico

After growing its lending business in West Africa, emerging markets credit startup Migo is expanding to Brazil on a $20 million Series B funding round led by Valor Capital Group.

The San Franicso-based company — previously branded Mines.io — provides AI-driven products to large firms so those companies can extend credit to underbanked consumers in viable ways.

That generally means making lending services to low-income populations in emerging markets profitable for big corporates, where they previously were not.

Founded in 2013, Migo launched in Nigeria, where the startup now counts fintech unicorn Interswitch and Africa’s largest telecom, MTN, among its clients.

Offering its branded products through partner channels, Migo has originated more than 3 million loans to over 1 million customers in Nigeria since 2017, according to company stats.

“The global social inequality challenge is driven by a lack of access to credit. If you look at the middle class in developed countries, it is largely built on access to credit,” Migo founder and CEO Ekechi Nwokah told TechCrunch.

“What we are trying to do is to make prosperity available to all by reinventing the way people access and use credit,” he explained.

Migo does this through its cloud-based, data-driven platform to help banks, companies and telcos make credit decisions around populations they previously may have bypassed.

These entities integrate Migo’s API into their apps to offer these overlooked market segments digital accounts and lines of credit, Nwokah explained.

“Many people are trying to do this with small micro-loans. That’s the first place you understand risk, but we’re developing into point of sale solutions,” he said.

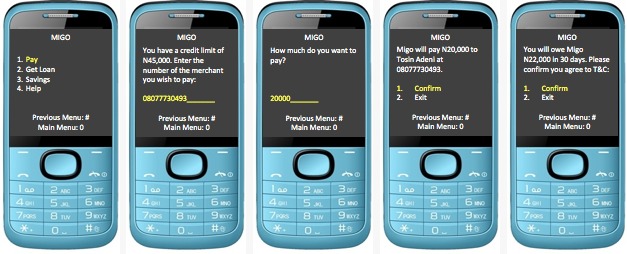

Migo’s client consumers can access their credit lines and make payments by entering a merchant phone number on their phone (via USSD) and then clicking on “Pay with Migo.” Migo can also be set up for use with QR codes, according to Nwokah.

He believes structural factors in frontier and emerging markets make it difficult for large institutions to serve people without traditional credit profiles.

“What makes it hard for the banks is its just too expensive,” he said of establishing the infrastructure, technology and staff to serve these market segments.

Nwokah sees similarities in unbanked and underbanked populations across the world, including Brazil and African countries such as Nigeria.

“Statistically, the number of people without credit in Nigeria is about 90 million people and its about 100 million adults that don’t have access to credit in Brazil. The countries are roughly the same size and the problem is roughly the same,” he said.

On clients in Brazil, Migo has a number of deals in the pipeline — according to Nwokah — and has signed a deal with a big-name partner in the South American country of 210 million, but could not yet disclose which one.

Migo generates revenue through interest and fees on its products. With lead investor Valor Capital Group, Velocity Capital and The Rise Fund joined the startup’s $20 million Series B.

Increasingly, Africa — with its large share of the world’s unbanked — and Nigeria — home to the continent’s largest economy and population — have become proving grounds for startups looking to create scalable emerging market finance solutions.

Migo could become a pioneer of sorts by shaping a fintech credit product in Africa with application in frontier, emerging and developed markets.

“We could actually take this to the U.S. We’ve had discussions with several partners about bringing the technology to the U.S. and Europe,” said founder Ekechi Nwokah. In the near-term, though, Migo is more likely to expand to Asia, he said.

Powered by WPeMatico

Cuvva, the app-based insurance provider that began life offering pay-as-you-go driving cover but has since expanded to also sell travel insurance, has raised £15 million in Series A funding.

Backing comes from RTP Global, Breega and Digital Horizon, joining existing investors LocalGlobe, Techstars Ventures, Tekton and Seedcamp. A number of angels also joined the round, including Dominic Burke, the CEO of Jardine Lloyd Thompson, and Faisal Galaria, the former chief strategy and investments officer of GoCompare.

Launched in 2016 when founder Freddy Macnamara (pictured) become frustrated he couldn’t let others drive his car intermittently because of lack of insurance cover, Cuvva was an early pioneer of pay-as-you-go car insurance.

The idea, which was easier explained than done, was to make it possible to insure a car only when it was being driven, and therefore be cheaper for low-mileage drivers, and, via an app and access to the DVLA database, make it easier to on-board new drivers for pay-as-you-drive cover.

The insurtech still offers hourly car insurance, but its product line has since been expanded to daily covery, as well as a product specifically aimed at learner drivers. In addition, Cuvva entered the travel insurance space, no doubt spotting overlap with its presumably younger, millennial demographic.

To that end, Cuvva says it will use the new capital to launch a new pay-monthly motor product in early 2020 that it says could cut average annual bills for car owners “significantly.” It will do this by cutting out various middle people, including brokers and comparison websites, which it says charge insurers about £70 on each policy sold.

“Unlike legacy insurers, Cuvva will not charge a fee to spread payments over the year and it will not penalise loyal customers with dual pricing,” says the startup. Cuvva also says it will offer the same savings, whether you are signing up as a new customer or are a returning customer, and won’t charge admin fees to alter personal details registered with your policy.

Cue canned statement from Macnamara: “I started Cuvva when I couldn’t find flexible insurance to help me share my car. Four years on from launch we are still discovering how big the problem we are solving really is. We’re now selling 3% of all UK motor insurance policies but we’ve got so much further to go. Cuvva is going to be the place where you buy all your insurance, all through our mobile app.”

Powered by WPeMatico

Penta, the Berlin-based business banking challenger that also now operates in Italy, has partnered with BBVA-backed card reader company SumUp in a bid to attract more offline businesses.

Up until recently, Penta had been targeting digital businesses, such as startups and e-commerce SMEs, but has since re-positioned itself for wider business banking appeal.

By partnering with a POS provider offering easy card reader-enabled payments, the German challenger bank wants to extend that offline (such as restaurants, craftsman, healthcare and architects).

Specifically, Penta says businesses can order a SumUp Card Reader via Penta, and in doing so will save money on the initial SumUp setup fee and be able to seamlessly integrate SumUp-powered payments with their Penta account.

They’ll also get access to the existing Penta features, such as being able to open a business banking account entirely digitally, issue multiple payment cards, grant limits and permissions per card for staff, facilitate expense management and integrate with popular accounting tools.

In the future, the SumUp integration is planned to go deeper. This will include the ability to use SumUp payments data to forecast future sales and feed into a business’s credit worthiness when they seek a loan.

“One request that we’ve had since day one has been for our customers to easily and quickly accept card payments, so we are very proud to be able to offer this with our newest partner SumUp,” says Penta CEO Marko Wenthin in a statement.

Adds James Henry, head of Sales and Partnerships at SumUp: “By cooperating with Penta, we will enable even more small and medium-sized companies to digitize their business and make the payment experience as convenient as possible for their customers. Penta, with its growing customer base of companies, is the ideal partner for us to reach the broad mid-market.”

Powered by WPeMatico

Work tools startup Notion, which recently reached a reported $800 million valuation, isn’t on the verge of a big SoftBank round. In fact, COO Akshay Kothari says the startup has “never felt like if we had more money we could grow faster.”

The company, centered around an app that helps non-developers build collaboration tools, has more than one million users and has scaled its product quickly despite having a team of just 27.

I wrote about the company’s partnership with some of tech’s top accelerators and venture capital firms last month. People are very curious about this small company and how it is run, so here’s more from my recent interview with COO Akshay Kothari in which we discussed the hyped startup’s philosophy of staying small and some of the challenges it may have ahead with this brand of thinking as competitors are raising massive sums.

This interview has been edited for length and clarity.

Notion COO Akshay Kothari (Photo: Notion)

Where does your story begin with Notion? Give me a snapshot of where the team is now.

Akshay Kothari: [Notion co-founders Ivan Zhao and Simon Last] started Notion six years ago and that’s when I invested. I had sold my previous company and I had this newfound money that I didn’t know what to do with. I invested in Notion, so that’s my connection.

We were kind of in research mode for many years trying to uncover what the market needs were. We launched about two years ago; 1.0 was just notes that you could take and a wiki so that you could collaborate with people. And then last year we launched databases and that was the 2.0 version, which kind of seemed like an inflection point, where now you could not only have your notes and your wiki, but also manage your tasks, manage your projects, manage candidates and recruiting, all in a single tool.

Over the last year and a half, the company has grown extremely fast. I joined about a year ago, there were about 10 people at the beginning of this year and now we’re close to 30. It’s still a really small engineering team. We’re 9 engineers, we don’t have any product managers, and we’re 2 designers. So there are about 10 people that are building the product, and 10 people on community and support teams, something that we’ve invested very heavily in. We’re starting to have a sales and marketing team. We have 2 people in marketing and 2 people in sales. That all rounds up to about 27 which is where we are now.

Since you joined do you think the idea has shifted at all?

In terms of the original idea, we were thinking about how people who didn’t know how to code could build things like tools and software that were really useful. I guess the only realization has been that not everyone wakes up wanting to build software, but everyone wakes to solve problems. That was the pivot to focusing on notes, wikis and tasks, because that’s actually something that every team needs.

Are those needs universal for big and small teams?

For the first 100 people you can actually do a lot with Notion. With 30 people, we pretty much run the entire company, except for using Slack for internal communication and Intercom for external communication like talking to customers. Everything else is actually on Notion, like our application tracking system for recruiting inside Notion, our sales CRM is in Notion, our wiki obviously is, our project management as well — no, we don’t use Jira.

For sub-100 businesses, you actually don’t need another tool. When you get to hundreds of people what tends to happens is that some person or some team tends to have a preference for a specific tool. In those situations, Notion plays well with other tools. You can embed things easily. So let’s say Excel or Google Sheets is something that you want to use, you can just embed that inside Notion. So Notion becomes this kind of central nervous system for all of the work that people are doing.

Building on that, one of the things we haven’t done is we don’t do synchronous communication so we’ve stayed away from that because I feel like people like using Slack. On Slack, you can’t actually collaborate on a project… Notion has become a place where you can actually do a lot of your work alongside the synchronous communication.

So, no interest in building a chat or video chat product?

Not in the near term. I think Slack is one of those enterprise tools that people at companies actually like. For a lot of these other tools, we just have to use it, not because we love it but because that that’s what exists.

Notion’s headquarters (Photo: Notion)

What are the barriers for satisfying the customers with 100+ employees?

Powered by WPeMatico