Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Founded in 2012, Nomiku became a plucky Silicon Valley darling by bringing affordable sous vide cooking to home kitchens. A Kickstarter project that same year generated $750,000, several times its $200,000 goal. The company scored a glowing TechCrunch profile the following year, as well, thanks in part to a great backstory.

Today, however, the company noted on its site and various social media channels that it is winding down operations:

Well, I am sorry to say that we have reached the end of the road. It is with a heavy heart (and deep-felt gratitude for your patronage) that we are writing to let you know that we are discontinuing the Nomiku Smart Cooker and Nomiku Meals effective immediately, and suspending operations. While we still believe in the concept, we simply were not able to get to a place of sustainability to keep the business going. Thank you very much for your support, it has meant a lot to myself and everyone here at Nomiku.

“The total climate for food tech is different than it used to be,” Lisa Fetterman said in a call to TechCrunch. “There was a time when food tech and hardware were much more hot and viable. I think a company can survive a few hurdles, and a few challenges [ …] For me, it was the perfect storm of all these things.”

In total, the company raised more than $1.3 million over two Kickstarter campaigns, putting it in the upper echelons of food crowdfunding. In 2015, the startup joined Y Combinator and launched a cooking app called Tender, featuring recipes from prominent chefs.

In some ways, Nomiku appears to be a victim of its own popularity. The company was able to bring a cost-prohibitive cooking technology down to an affordable price point, only to see the market flooded by competitors. Fetterman highlighted some of those issues in a recent Extra Crunch interview.

In 2017, Samsung Ventures invested in the company, with plans to integrate it into its SmartThings connected platform. That same year, Nomiku began to pivot into subscription meal plans, but had difficulty getting the word out. Fetterman says the company was seeking funding toward the end, but ultimately couldn’t make things work.

Even with a buzzy company and a great product, the startup world can still be unforgiving.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re taking stock of a cohort of special companies: still-private startups that have reached $100 million in annual recurring revenue (ARR). Our goal is to understand which startup companies are actually exceptional. This late in the unicorn era, hundreds of companies around the world have reached a valuation of $1 billion, making the achievement somewhat pedestrian.

Reaching $100 million in ARR, however, still stands out.

We explored the idea earlier this week, citing Asana, Druva and WalkMe as private companies that recently reached $100 million ARR. In addition to that trio, Bill.com and Sprout Social, both of which went public this week, also crossed the nine-figure annual recurring revenue mark in 2019.

After we posted that short list, four other companies either just shy of $100 million ARR, or with a little bit more, reached out to TechCrunch, touting their own successes. Given that our point was that companies which reach the revenue threshold million are neat, it’s worth taking a moment to look at the other companies joining the $100 million ARR club.

For extra fun I got on the phone with a number of their CEOs to chat about their progress. We’ll start with a look at a company that is nearly a member of the club, and then talk about a few that recently punched their membership cards.

To be frank, I did not know that GitLab was as large as it is. Backed by more than $400 million in private capital, GitLab competes with the now-purchased GitHub as a developer resource and service. Its backers include Goldman Sachs, ICONIQ, GV, August Capital and Khosla.

GitLab became a unicorn back in September of 2018, when it raised $100 million at a $1 billion post-money valuation. Its more recent $268 million Series E raised this September pushed that valuation to nearly $2.8 billion.

It’s a good company for us to include, as it provides a good example of how far in advance a $1 billion valuation can precede a $100 million ARR business; in GitLab’s case, provided that it grows as expected, its unicorn valuation came nearly 1.5 years before reaching nine-figure ARR.

To understand more about the company’s growth, we caught up with its CEO Sid Sijbrandij (full discussion here), learning that he views the unicorn tag as a way to help a company brand itself, but something that is outside of his company’s control. Revenue, in his view, is “much more within your control.” According to Sijbrandij, GitLab is aiming for $1 billion in revenue in 2023 and has a November, 2020 IPO targeted.

GitLab is sharing its impending ARR milestone as it runs its whole business very transparently (hence why my chat with its CEO was live-streamed, and archived on YouTube). It will be super interesting to see if the company hits the ARR target on time, and then if it can also stick the landing with a Q4 2020 IPO.

Egnyte, a player in the enterprise productivity, storage and security spaces, has kept growing since its $75 million Series E it raised last October.

The company, backed by Goldman Sachs (again), GV (again) and Kleiner Perkins, has raised just $137.5 million to date. Reaching $100 million ARR on that level of funding means that Egnyte has run efficiently as a business. In fact, as TechCrunch has reported, Egnyte has occasionally made money on its path to the public markets.

TechCrunch has spoken to Egnyte’s CEO Vineet Jain a number of times, but it seemed appropriate to get him back on the phone now that his company is nearly ready to go public (at least in terms of size). According to Jain, in fresh data released to Extra Crunch:

Powered by WPeMatico

On the heels of Bill.com’s debut, Chicago-based social media software company Sprout Social priced its IPO last night at $17 per share, in the middle of its proposed $16 to $18 per-share range. Selling 8.8 million shares, Sprout raised just under $150 million in its debut.

Underwriters have the option to purchase an additional 1.3 million shares if they so choose.

The IPO is a good result for the company’s investors (Lightbank, New Enterprise Associates, Goldman Sachs and Future Fund), but also for Chicago, a growing startup scene that doesn’t often get its due in the public mind.

At $17 per share, not including the possible underwriter option, Sprout Social is worth about $814 million. That’s just a hair over its final private valuation set during its $40.5 million Series D in December of 2018. That particular investment valued Sprout at $800.5 million, according to Crunchbase data.

Sprout’s debut is interesting for a few reasons. First, the company raised just a little over $110 million while private, and will generate over $100 million in trailing GAAP revenue this year. In effect, Sprout Social used less than $110 million to build up over $100 million in annual recurring revenue (ARR) — the firm reached the $100 million ARR mark between Q2 and Q3 of 2019. That’s a remarkably efficient result for the unicorn era.

And the company is interesting, as it gives us a look at how investors value slower-growth SaaS companies. As we’ve written, Sprout Social grew by a little over 30% in the first three quarters of 2019. That’s a healthy rate, but not as fast as, say, Bill.com . (Bill.com’s strong market response puts its own growth rate in context.)

Thinking very loosely, Sprout Social closed Q3 2019 with ARR of about $105 million. Worth $814 million now, we can surmise that Sprout priced at an ARR multiple of about 7.75x. That’s a useful benchmark for private companies that sell software: If you want a higher multiple when you go public, you’ll have to grow a little faster.

All the same, the IPO is a win for Chicago, and a win for the company’s investors. We’ll update this piece later with how the stock performs, once it begins to trade.

Powered by WPeMatico

Reliance Industries, one of India’s largest industrial houses, has acquired a majority stake in NowFloats, an Indian startup that helps businesses and individuals build online presence without any web developing skills.

In a regulatory filing on Thursday, Reliance Strategic Business Ventures Limited said (PDF) it has acquired an 85% stake in NowFloats for 1.4 billion Indian rupees ($20 million).

Seven-and-a-half-year old, Hyderabad-headquartered NowFloats operates an eponymous platform that allows individuals and businesses to easily build an online presence. Using NowFloats’ services, a mom and pop store, for instance, can build a website, publish their catalog, as well as engage with their customers on WhatsApp.

The startup, which has raised about 12 million in equity financing prior to today’s announcement, claims to have helped over 300,000 participating retail partners. NowFloats counts Blume Ventures, Omidyar Network, Iron Pillar, IIFL Wealth Management, and Hyderabad Angels among its investors.

Last year, NowFloats acquired LookUp, an India-based chat service that connects consumers to local business — and is backed by Vinod Khosla’s personal fund Khosla Impact, Twitter co-founder Biz Stone, Narayana Murthy’s Catamaran Ventures and Global Founders Capital.

Reliance Strategic Business Ventures Limited, a wholly-owned subsidiary of Reliance Industries, said that it would invest up to 750 million Indian rupees ($10.6 million) of additional capital into the startup, and raise its stake to about 89.66%, if NowFloats achieves certain unspecified goals by the end of next year.

In a statement, Reliance Industries said the investment will “further enable the group’s digital and new commerce initiatives.” NowFloats is the latest acquisition Reliance has made in the country this year. In August, the conglomerate said it was buying a majority stake in Google-backed Fynd for $42.3 million. In April, it bought a majority stake in Haptik in a deal worth $100 million.

There are about 60 million small and medium-sized businesses in India. Like hundreds of millions of Indians, many in small towns and cities, who have come online in recent years thanks to world’s cheapest mobile data plans and inexpensive Android smartphones, businesses are increasingly building online presence as well.

But vast majority of them are still offline, a fact that has created immense opportunities for startups — and VCs looking into this space — and major technology giants. New Delhi-based BharatPe, which helps merchants accept online payments and provides them with working capital, raised $50 million in August. Khatabook and OkCredit, two digital bookkeeping apps for merchants, have also raised significant amount of money this year.

In recent years, Google has also looked into the space. It has launched tools — and offered guidance — to help neighborhood stores establish some presence on the web. In September, the company announced that its Google Pay service, which is used by more than 67 million users in India, will now enable businesses to accept digital payments and reach their customers online.

Powered by WPeMatico

Bill.com went public today after pricing its shares higher than it initially expected. The B2B payments company sold nearly 10 million shares at $22 apiece, raising around $216 million in its IPO. Public investors felt that the company’s price was a deal, sending the value of its equity to $35.51 per share as of the time of writing.

That’s a gain of over 61%.

On the heels of its successful pricing run and raucous first day’s trading, TechCrunch caught up with Bill.com CEO René Lacerte to dig into his company’s debut. We wanted to know how pricing went, and whether the company (which possibly could have valued itself more richly during its IPO pricing, given its first-day pop) had considered a direct listing.

Lacerte detailed what resonated with investors while pricing Bill.com’s shares, and also did a good job outlining his perspective on what matters for companies that are going public. As a spoiler, he wasn’t super focused on the company’s first-day return.

For more on the Bill.com IPO’s nuts and bolts, head here. Let’s get into the interview.

The following interview has been edited for length and clarity. Questions have been condensed.

TechCrunch: How did your IPO pricing feel, and what did you learn from the process?

Lacerte: I think the whole experience has been an incredible learning experience from a capitalism perspective; that’s probably a broader conversation. But you know, it really came down to how our story resonated with investors, and so there’s three components that we kind of really talked to folks about.

Powered by WPeMatico

DataRobot, a company best known for creating automated machine learning models known as AutoML, announced today that it intends to acquire Paxata, a data prep platform startup. The companies did not reveal the purchase price.

Paxata raised a total of $90 million before today’s acquisition, according to the company.

Up until now, DataRobot has concentrated mostly on the machine learning and data science aspect of the workflow — building and testing the model, then putting it into production. The data prep was left to other vendors like Paxata, but DataRobot, which raised $206 million in September, saw an opportunity to fill in a gap in their platform with Paxata.

“We’ve identified, because we’ve been focused on machine learning for so long, a number of key data prep capabilities that are required for machine learning to be successful. And so we see an opportunity to really build out a unique and compelling data prep for machine learning offering that’s powered by the Paxata product, but takes the knowledge and understanding and the integration with the machine learning platform from DataRobot,” Phil Gurbacki, SVP of product development and customer experience at DataRobot, told TechCrunch.

Prakash Nanduri, CEO and co-founder at Paxata, says the two companies were a great fit and it made a lot of sense to come together. “DataRobot has got a significant number of customers, and every one of their customers have a data and information management problem. For us, the deal allows us to rapidly increase the number of customers that are able to go from data to value. By coming together, the value to the customer is increased at an exponential level,” he explained.

DataRobot is based in Boston, while Paxata is in Redwood City, Calif. The plan moving forward is to make Paxata a west coast office, and all of the company’s almost 100 employees will become part of DataRobot when the deal closes.

While the two companies are working together to integrate Paxata more fully into the DataRobot platform, the companies also plan to let Paxata continue to exist as a standalone product.

DataRobot has raised more than $431 million, according to PitchBook data. It raised $206 million of that in its last round. At the time, the company indicated it would be looking for acquisition opportunities when it made sense.

This match-up seems particularly good, given how well the two companies’ capabilities complement one another, and how much customer overlap they have. The deal is expected to close before the end of the year.

Powered by WPeMatico

One share of Amazon stock costs more than $1,700, locking out less-wealthy investors. So to continue its quest to democratize stock trading, Robinhood is launching fractional share trading this week. This lets you buy 0.000001 shares, rounded to the nearest penny, or just $1 of any stock, with zero fee.

The ability to buy by millionth of a share lets Robinhood undercut Square Cash’s recently announced fractional share trading, which sets a $1 minimum for investment. Robinhood users can sign up here for early access to fractional share trading. “One of our core values is participation is power,” says Robinhood co-CEO Vlad Tenev. “Everything we do is rooted in this. We believe that fractional shares have the potential to open up investing for even more people.”

Fractional share trading ensures no one need be turned away, and Robinhood can keep growing its user base of 10 million with its war chest of $910 million in funding. As incumbent brokerages like Charles Schwab and E*Trade move to copy Robinhood’s free stock trading, the startup has to stay ahead in inclusive financial tools. In this case, though, it’s trying to keep up, since Schwab, Square, Stash and SoFi all launched fractional shares this year. Betterment has actually offered this since 2010.

Robinhood has a bunch of other new features aimed at diversifying its offering for the not-yet-rich. Today its Cash Management feature it announced in October is rolling out to its first users on the 800,000-person wait list, offering them 1.8% APY interest on cash in their Robinhood balance plus a Mastercard debit card for spending money or pulling it out of a wide network of ATMs. The feature is effectively a scaled-back relaunch of the botched debut of 3% APY Robinhood Checking a year ago, which was scuttled because the startup failed to secure the proper insurance it now has for Cash Management.

Additionally, Robinhood is launching two more widely requested features early next year. Dividend Reinvestment Plan (DRIP) will automatically reinvest into stocks or ETF cash dividends Robinhood users receive. Recurring Investments will let users schedule daily, weekly, bi-weekly or monthly investments into stocks. With all this, and Crypto trading, Robinhood is evolving into a full financial services suite that will be much harder for competitors to copy.

“We believe that if you want to invest, it shouldn’t matter how much money you have. With fractional shares, we’re opening up a whole universe of stocks and funds, including Amazon, Apple, Disney, Berkshire Hathaway, and thousands of others,” Robinhood product manager Abhishek Fatehpuria tells me.

Users will be able to place real-time fractional share orders in dollar amounts as low as $1 or share amounts as low as 0.000001 shares rounded to the penny during market hours. Stocks worth over $1 per share with a market capitalization above $25 million are eligible, with 4,000 different stocks and ETFs available for commission-free, real-time fractional trading.

“We believe that participation is power. Since day one, we’ve focused on breaking down barriers like trade commissions and account minimums to help people participate in the financial system,” says Fatehpuria. “We have a unique user base — half our customers tell us they’re first-time investors, and the median age of a Robinhood customer is 30. This means we have a unique opportunity to expand access to the markets for this new generation.”

Robinhood is racing to corner the freemium investment tool market before other startups and finance giants can catch up. It opened a waitlist for its U.K. launch next year, which will be its first international market. But in just the past month, Alpaca raised $6 million for an API that lets anyone build a stock brokerage app, and Atom Finance raised $12.5 million for its free investment research tool that could compete with Robinhood’s in-app feature. Meanwhile, Robinhood suffered an embarrassing bug, letting users borrow more money than allowed.

The move fast and break things mentality triggers new dangers when introduced to finance. Robinhood must resist the urge to rush as it spreads itself across more products in pursuit of a more level investment playing field.

Powered by WPeMatico

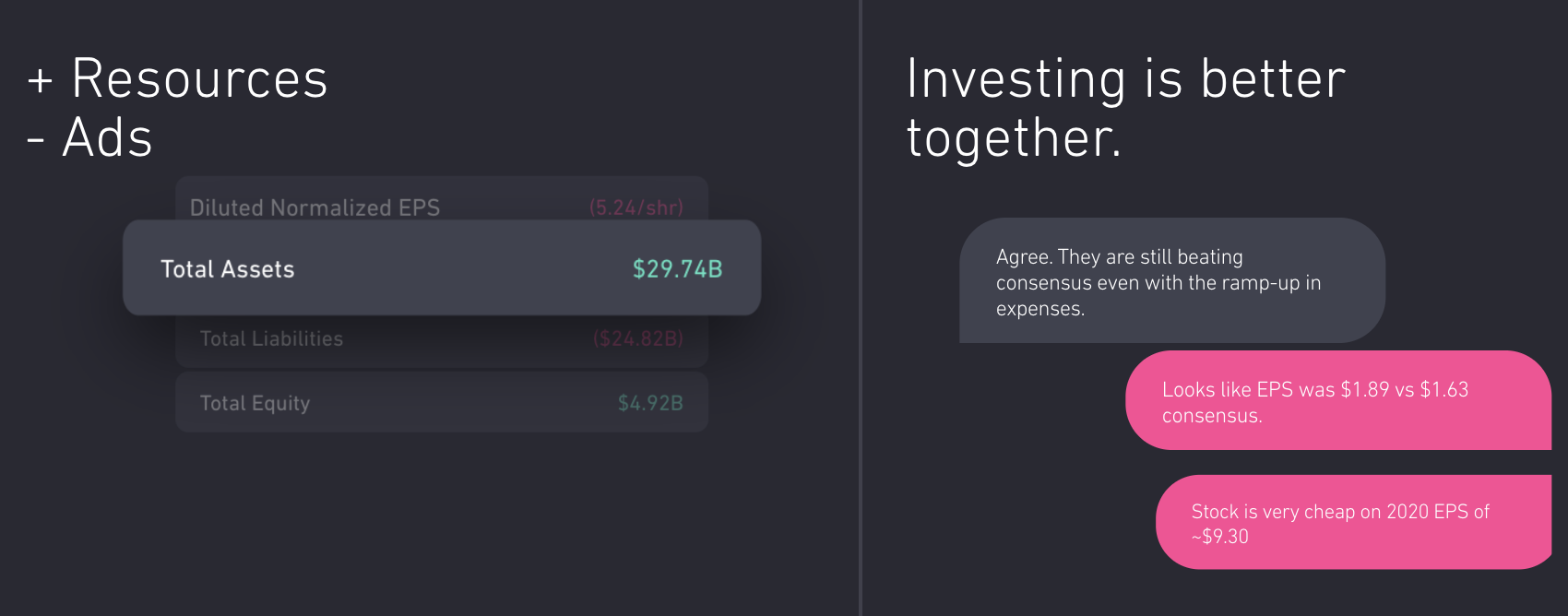

If you want to win on Wall Street, Yahoo Finance is insufficient but Bloomberg Terminal costs a whopping $24,000 per year. That’s why Atom Finance built a free tool designed to democratize access to professional investor research. If Robinhood made it cost $0 to trade stocks, Atom Finance makes it cost $0 to know which to buy.

Today Atom launches its mobile app with access to its financial modeling, portfolio tracking, news analysis, benchmarking and discussion tools. It’s the consumerization of finance, similar to what we’ve seen in enterprise SaaS. “Investment research tools are too important to the financial well-being of consumers to lack the same cycles of product innovation and accessibility that we have experienced in other verticals,” CEO Eric Shoykhet tells me.

In its first press interview, Atom Finance today revealed to TechCrunch that it has raised a $10.6 million Series A led by General Catalyst to build on its quiet $1.9 million seed round. The cash will help the startup eventually monetize by launching premium tiers with even more hardcore research tools.

Atom Finance already has 100,000 users and $400 million in assets it’s helping steer since soft-launching in June. “Atom fundamentally changes the game for how financial news media and reporting is consumed. I could not live without it,” says The Twenty Minute VC podcast founder and Atom investor Harry Stebbings.

Individual investors are already at a disadvantage compared to big firms equipped with artificial intelligence, the priciest research and legions of traders glued to the markets. Yet it’s becoming increasingly clear that investing is critical to long-term financial mobility, especially in an age of rampant student debt and automation threatening employment.

“Our mission is two-fold,” Shoykhet says. “To modernize investment research tools through an intuitive platform that’s easily accessible across all devices, while democratizing access to institutional-quality investing tools that were once only available to Wall Street professionals.”

Shoykhet saw the gap between amateur and expert research platforms firsthand as an investor at Blackstone and Governors Lane. Yet even the supposedly best-in-class software was lacking the usability we’ve come to expect from consumer mobile apps. Atom Finance claims that “for example, Bloomberg hasn’t made a significant change to its central product offering since 1982.”

The Atom Finance team

So a year ago, Shoykhet founded Atom Finance in Brooklyn to fill the void. Its web, iOS and Android apps offer five products that combine to guide users’ investing decisions without drowning them in complexity:

“Our Sandbox feature allows users to create simple financial models directly within our platform, without having to export data to a spreadsheet,” Shoykhet says. “This saves our users time and prevents them from having to manually refresh the inputs to their model when there is new information.”

Shoykhet positions Atom Finance in the middle of the market, saying, “Existing solutions are either too rudimentary for rigorous analysis (Yahoo Finance, Google Finance) or too expensive for individual investors (Bloomberg, CapIQ, Factset).”

With both its free and forthcoming paid tiers, Atom hopes to undercut Sentieo, a more AI-focused financial research platform that charges $500 to $1,000 per month and raised $19 million a year ago. Cheaper tools like BamSEC and WallMine are often limited to just pulling in earnings transcripts and filings. Robinhood has its own in-app research tools, which could make it a looming competitor or a potential acquirer for Atom Finance.

Shoykhet admits his startup will face stiff competition from well-entrenched tools like Bloomberg. “Incumbent solutions have significant brand equity with our target market, and especially with professional investors. We will have to continue iterating and deliver an unmatched user experience to gain the trust/loyalty of these users,” he says. Additionally, Atom Finance’s access to users’ sensitive data means flawless privacy, security, and accuracy will be essential.

The $12.5 million from General Catalyst, Greenoaks, Global Founders Capital, Untitled Investments, Day One Ventures and a slew of angels gives Atom runway to rev up its freemium model. Robinhood has found great success converting unpaid users to its subscription tier where they can borrow money to trade. By similarly starting out free, Atom’s eight-person team hailing from SoFi, Silver Lake, Blackstone and Citi could build a giant funnel to feed its premium tiers.

Fintech can feel dry and ruthlessly capitalistic at times. But Shoykhet insists he’s in it to equip a new generation with methods of wealth creation. “I think we’ve gone long enough without seeing real innovation in this space. We can’t be complacent with something so important. It’s crucial that we democratize access to these tools and educate consumers . . . to improve their investment well-being.”

Powered by WPeMatico

Fourteen startups presented onstage today at Disrupt Berlin, giving live demos and rapid-fire presentations on their origin stories and business models, then answering questions from our expert judges.

Now, with the help of those judges, we’ve narrowed the group down to five startups working on everything from productivity to air pollution.

These finalists will be presenting again tomorrow (at 2pm Berlin time, viewable on the TechCrunch website or in-person at Disrupt) in front of a new set of judges. The winner will receive $50,000 and custody of the storied Disrupt Cup.

Here are the finalists:

Gmelius is building a workspace platform that lives inside Gmail, allowing teams to get more bespoke tools without adding yet another piece of software to their repertoire. It slots into the Gmail workspace, adding a host of features like shared inboxes, a help desk, an account-management solution and automation tools.

Hawa Dawa combines data sources like satellites and dedicated air monitoring stations to build a granular heat map of air pollutants, selling this map to cities and companies as a subscription API. While the company notes it’s hardware-agnostic, it does build its own IoT sensors for companies and cities that might not have existing air quality sensors in place.

Read more about Hawa Dawa here.

Inovat makes it much easier for travelers to get reimbursed for the value-added tax, through an app that employs optical character recognition and machine learning to interpret receipts, determine how much VAT you should be owed for your purchase and prepare the requisite forms for submission online or to a customs officer.

Scaled Robotics has designed a robot that can produce 3D progress maps of construction sites in minutes, precise enough to detect that a beam is just a centimeter or two off. Supervisors can then use the software to check things like which pieces are in place on which floor, whether they have been placed within the required tolerances or if there are safety issues like too much detritus on the ground in work areas.

Read more about Scaled Robotics here.

Stable offers a solution as simple as car insurance, designed to protect farmers around the world from pricing volatility. Through the startup, food buyers ranging from owners of a small smoothie shop to Coca-Cola employees can insure thousands of agricultural commodities, as well as packaging and energy products.

Powered by WPeMatico

This week Gtmhub announced a $9 million Series A led by CRV. The investment was not a large round, even for an A. But the capital found its way into one of the fastest-growing SaaS companies that we’ve spoken with recently, which made it interesting all the same.

And, the firm was willing to talk about its financial performance in some detail. The combination made its Series A impossible to ignore.

TechCrunch caught up with Gtmhub’s CMO Seth Elliott this morning to learn more.

Let’s start with OKRs. Objectives and key results, better known as OKRs, are a method for organizational planning. They are famous thanks to their roots in Google’s success, but have since broken free of the technology world and become a well-known planning method for corporations of all sizes and types.

Gtmhub deals with them, providing software and services around OKR implementation, training and tracking. (If you an OKR neophyte, head here for a quick overview of what they are.)

Making OKR software isn’t a differentiator in today’s market. Ally does it (it also raised capital recently), along with WorkBoard, Koan and Lattice, among others.

Given the crowded market, Gtmhub stressed during our call how it thinks of itself as differentiated. The company has three things that it hopes will give it an edge in the market. The first is a focus on enterprise customers. According to Elliott, enterprise-sized clients are his company’s “bread and butter,” from a revenue perspective. Instead of starting with a small or mid-sized business target market and later targeting enterprise-scale customers, Gtmhub is going after the top-end of the market first.

Second, the company’s software is designed to interface with external tooling, allowing for real-time OKR tracking as it ingests information to help teams vet how they are progressing against their goals. And, the firm is working on a marketplace where, over time, customers will be able to learn from existing OKR setups and leverage analytics setups that help with data importation and visibility.

In its own words, Gtmhub is an OKR-centric software company, while “provid[ing] a long-term vision and the execution process necessary to bridge the strategy/execution gap,” according to Elliot.

Notably, Gtmhub, despite its enterprise focus, is not abandoning smaller companies. According to Elliot, the startup is announcing a new, stripped-down, $1 per user per month plan next week called START, aimed at smaller firms.

If START is an attempt to onboard companies when they are small so they can be upsold later, or if it is more a contra-competitor move, isn’t clear. But the new, cheap plan (priced at about 10% of other Gtmhub tiers) could shake up the OKR software space by making table-stakes features worth less than they were before.

Gtmhub is a distributed company, with offices in Denver, Sofia, Berlin and London for its roughly 60 workers. You might think, given its global footprint and number of employees, that the company had raised lots of capital to fund its operations. The opposite, as it turns out.

The startup’s $9 million Series A dwarfs its preceding rounds, including about $1.3 million in seed capital raised (here) in February of 2018. Aside from those checks and the new capital, all we know about Gtmhub’s fundraising history is that it picked up $100,000 in angel money in early 2017.

All told, Gtmhub has raised just over $10 million to date, making its Series A about 87% of its known raised capital. That’s not the mark of a company built on burn.

Of course, if Gtmhub kept a lid on its expenses by growing slowly, its parsimony might be more sin than virtue; after all, private companies backed with venture dollars are built for expansion.

The opposite, as it turns out.

Elliot shared a number of notable metrics with TechCrunch that we’ve prepared for you below, in an ingestible format:

Take a moment and square those results with how much capital Gtmhub raised and ask yourself if the performance matches the raise. It doesn’t. I suspect that Gtmhub could have raised a lot more money than it chose to, given its growth rate and other marks of financial health.

But, after expanding to 60 people on less than $3.5 million in known venture, the company probably isn’t too unprofitable, and can do a lot with just $9 million. (Gtmhub could also raise more if it needed to, given its metrics.)

With Gtmhub and Ally each flush with new cash, it’s going to be enjoyable to watch the OKR and OKR-empowered software space grow over the next few years. There will be eventual consolidation, right?

Correction: This post misstated the amount of capital raised by Gtmhub before its Series A and has been corrected.

Photo by Startaê Team on Unsplash

Powered by WPeMatico