Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Hi everyone, my name is Eric Eldon and I’m the new writer of the Startups Weekly newsletter.

I’ll be picking my favorite explicitly startup-focused articles of the week for you from Extra Crunch (where I’m the editor now), as well as TechCrunch (where I was the co-editor years ago… long story).

Some people tell us that TechCrunch doesn’t cover startups like it used to. I don’t know if that is true, but it is definitely hard to keep track of our startup coverage mixed in with the rest of our news.

This newsletter will highlight the best startup coverage on TechCrunch and Extra Crunch to help fix that.

I probably hate reading bad startup advice and analysis even more than you do, and not only because I’ve had to read a lot of it over the years as an editor. I’ve also started a few companies myself, and I’ve had the chance to experience exits, failures and venture backing.

I’ll be highlighting articles that I think address something significant about building a company, and I’ll tell you why each one is worth a read.

There will also be some experiments. Thanks for reading! And if you want it in your inbox, you can subscribe here.

Plaid’s product is beyond boring to most people, but it is already a name brand to its enterprise users and across the greater startup world, as its stats and funding rounds have grown. The $5.3 billion outcome announced this week cements its status as a top SaaS/fintech startup story of this era, in addition to being a popular platform for developers who need to sync user payment data.

Alex Wilhelm was all over the news. He dug into Visa’s presentation explaining the purchase on Extra Crunch — it paid more than twice Plaid’s last valuation — and found the classic tale of a large, slow-moving incumbent strategically buying a hot younger company in order to grow into newer markets. Then he got comments for Extra Crunch from a range of analysts… who basically said the same thing.

You can now tune into the latest TechCrunch Equity episode to hear him talk about it with our resident former VC Danny Crichton.

Closely watched Atrium is shutting down the law firm to focus on the tech company. Founder Justin Kan tells Josh Constine on TechCrunch that this is part of the evolution toward providing a better tech service.

The law firm had been designed to provide the human touch in a way that machines couldn’t, but Kan says that lawyers do that great as third parties.

Many SaaS startups are trying to take on the back office processes of the 20th century. Atrium’s change will be another reason for them to go all-in on software, with humans not included.

One of the most loved and feared people in tech communications today, Brooke Hammerling has been in the middle of key stories of the decade with founders young and old. And sometimes on the opposite side of me.

She knows her stuff. Here’s one of my favorite gems from the full interview with Jordan Crook over on Extra Crunch:

If you’re an early-stage company, and you’re an unknown founder, and you’re coming out with your own take on something, you don’t want to spend your money on PR too early.

You want to spend that money on product development and engagement and engineering and so forth.

That’s the word on the street from our resident former VC, who was recently out in San Francisco visiting his many friends and professional acquaintances. Danny put his notes together for TechCrunch back in the comfort of his New York apartment, and found that everyone is raising huge rounds [emphasis his] — and it’s all about being there for the future. Plaid’s cap table is a good example.

One of my favorite quotes:

As one VC explained to me last week (paraphrasing), “What’s weird today is that you have firms like Sequoia who show up for seed rounds, but they don’t really care about … anything. Valuation, terms, etc. It’s all a play for those later-stage rounds.” I think that’s a bit of an exaggeration to be clear, but ultimately, those one million-dollar checks are essentially a rounding error for the largest funds. The real return is in the mega rounds down the road.

He also noticed for TechCrunch that VCs today seem to be especially tired. You can tell him what you think about these observations at danny@techcrunch.com.

(Photo by David Becker/Getty Images)

I have never been to CES and don’t plan to go, but Brian Heater always goes and this year he came back thinking that the home robot sector is getting serious.

His takeaway for Extra Crunch:

There’s a cynical (and probably at least partially correct) view that these sorts of deals are publicity stunts — big companies using CES to demonstrate how forward-thinking they are about new technologies. But there’s something to be said for the show’s position at the forefront of such technologies. The products are real, even if wider use is hypothetical. And in an era when Amazon has deployed more than 100,000 robots across its U.S. fulfillment centers to enable next and same-day delivery, we’re well into the realm of real-world use.

Brian is also hosting a one-day TechCrunch conference focused on robotics startups at UC Berkeley in early March, for those who are focused on this space. The event last year was a huge hit and we’re looking forward to the next one. Follow the link to learn more.

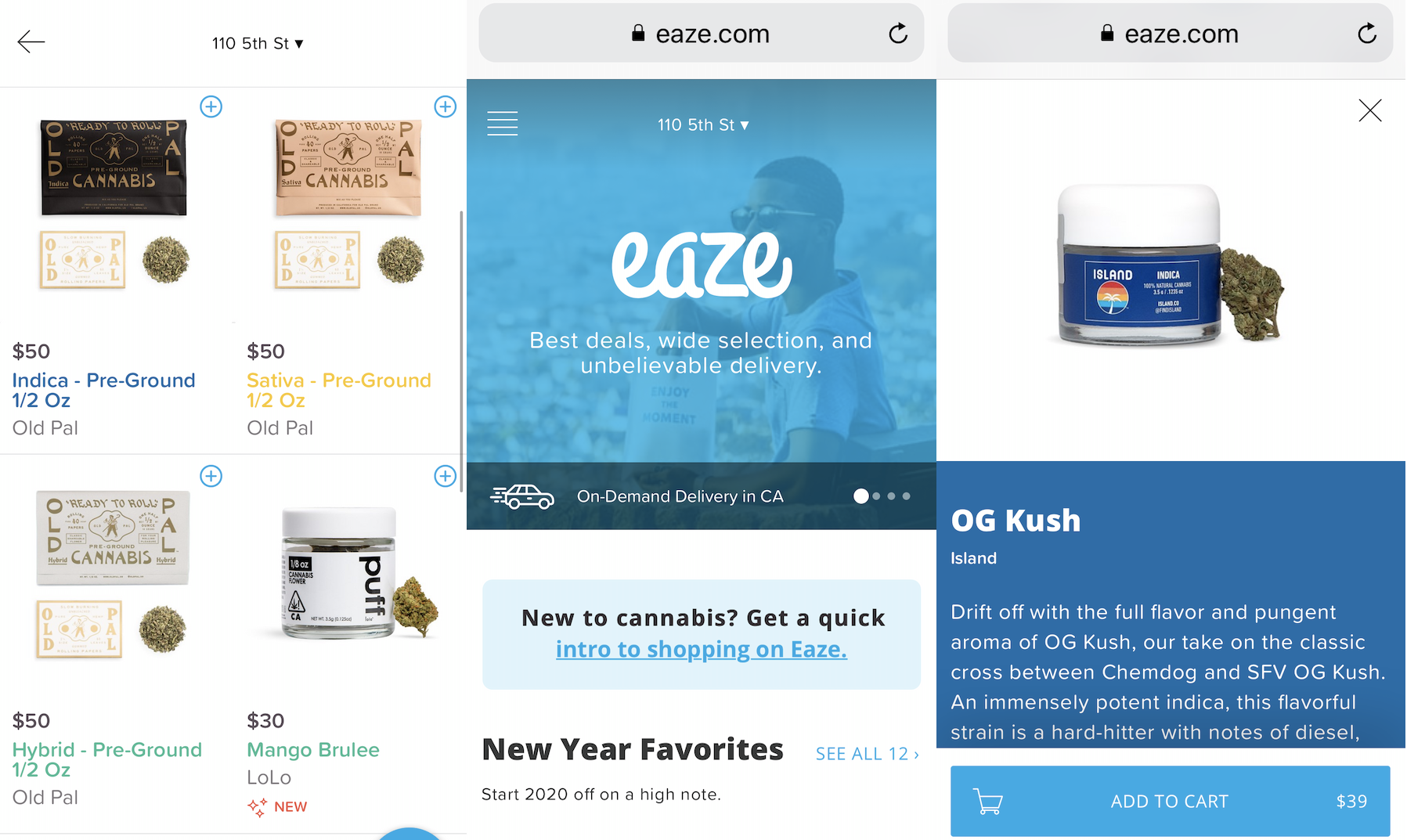

Eaze has been one of the highest-profile cannabis distributors, but now it might be running out of cash, report Ingrid Owen and Josh Constine. There are many structural reasons why any cannabis business is very hard, legal or otherwise.

But it’s interesting to take a look at who is succeeding in the consumer cannabis market and why.

One local example is Berner, a high school dropout in San Francisco who became a budtender and partnered with cannabis geneticists to create and promote the Girl Scout Cookies strain, and also became an international rap star (the main topic is his weed) and clothing designer.

These days, he’s opening more and more Cookies retail cannabis outlets, including in Oakland and L.A., and cutting licensing and certification deals with a broad network of partners, (and claims to be turning down huge acquisition offers). Basically, his cannabis is also his modern multi-platform brand and the cool kids are into it. He does not appear to be running out of cash.

Powered by WPeMatico

This week, LaunchDarkly announced that it has raised another $54 million. Led by Bessemer Venture Partners and backed by the company’s existing investors, it brings the company’s total funding up to $130 million.

For the unfamiliar, LaunchDarkly builds a platform that allows companies to easily roll out new features to only certain customers, providing a dashboard for things like “canary launches” (pushing new stuff to a small group of users to make sure nothing breaks) or launching a feature only in select countries or territories. By productizing an increasingly popular development concept (“feature flagging”) and making it easier to toggle new stuff across different platforms and languages, the company is quickly finding customers in companies that would rather not spend time rolling their own solutions.

I spoke with CEO and co-founder Edith Harbaugh, who filled me in on where the idea for LaunchDarkly came from, how their product is being embraced by product managers and marketing teams and the company’s plans to expand with offices around the world. Here’s our chat, edited lightly for brevity and clarity.

Powered by WPeMatico

Continuing our irregular surveys of the public markets, two things happened this week that are worth our time. First, a third domestic technology company — Alphabet — passed the $1 trillion market capitalization threshold. And, second, software as a service (SaaS) stocks reached record highs on the public markets after retreating over last summer.

The two milestones, only modestly related events, indicate how temperate the public waters are for technology companies today, a fact that should extend warmth into the private market where startups, and their venture capital backers, work.

The happenings are good news for technology startups for a number of reasons, including that major tech players have never had as much wealth in hand with which to buy smaller companies, and strong SaaS valuations help both smaller startups fundraise, and their larger brethren possibly exit.

Indeed, the stridently good valuations that major tech companies and their smaller siblings enjoy today should be just the sort of market conditions under which unicorns want to debut. We’ll continue to make this point so long as the public markets continue to rise, pricing tech companies that have already floated higher like the cliche’s own tide.

But while Alphabet, Microsoft and Apple are worth $3.68 trillion as a trio, and SaaS stocks are now worth 12.3x times their revenue (using enterprise value instead of market cap, for those keeping score at home), not every private, venture-backed company will necessarily benefit from public investor largesse.

How much the current public-market tech valuation expansion will help companies that are increasingly sorted into the tech-enabled bucket isn’t clear; some companies that went public in 2019 were quickly spit up by investors unwilling to support valuations that matched or rose above their final private valuations. SmileDirectClub was one such offering.

The dividing line between what counts as tech — often fuzzy — appears to be slicing along gross margin lines, and the repeatability of business. The higher margin, and more recurring a company is, the more it’s worth. This market reality is why SaaS stocks’ recent return to form is not a surprise.

For Casper and One Medical, the first two venture-backed IPO hopefuls of the year, the more tech-ish they can appear between now and pricing the better. Because technology companies today are valued so highly, perhaps even a faint dusting of tech will save their valuations as they cross the chasm between private and adult.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Yesterday, TechCrunch reported that Eaze, a well-known cannabis-focused startup, is struggling to stay in business amidst a cash crunch, leadership turmoil, banking issues and a business model pivot. It’s a compelling, critical read.

The news, however, asks a question: How are other cannabis-focused startups faring? We’ll explore the question through the lens of fundraising and the public market results of public cannabis companies in Canada.

Powered by WPeMatico

It seems like every company making lidar has a new and clever approach, but Baraja takes the cake. Its method is not only elegant and powerful, but fundamentally avoids many issues that nag other lidar technologies. But it’ll need more than smart tech to make headway in this complex and evolving industry.

To understand how lidar works in general, consult my handy introduction to the topic. Essentially a laser emitted by a device skims across or otherwise very quickly illuminates the scene, and the time it takes for that laser’s photons to return allows it to quite precisely determine the distance of every spot it points at.

But to picture how Baraja’s lidar works, you need to picture the cover of Pink Floyd’s “Dark Side of the Moon.”

GIFs kind of choke on rainbows, but you get the idea.

Imagine a flashlight shooting through a prism like that, illuminating the scene in front of it — now imagine you could focus that flashlight by selecting which color came out of the prism, sending more light to the top part of the scene (red and orange) or middle (yellow and green). That’s what Baraja’s lidar does, except naturally it’s a bit more complicated than that.

The company has been developing its tech for years with the backing of Sequoia and Australian VC outfit Blackbird, which led a $32 million round late in 2018 — Baraja only revealed its tech the next year and was exhibiting it at CES, where I met with co-founder and CEO Federico Collarte.

“We’ve stayed in stealth for a long, long time,” he told me. “The people who needed to know already knew about us.”

The idea for the tech came out of the telecommunications industry, where Collarte and co-founder Cibby Pulikkaseril thought of a novel use for a fiber optic laser that could reconfigure itself extremely quickly.

“We thought if we could set the light free, send it through prism-like optics, then we could steer a laser beam without moving parts. The idea seemed too simple — we thought, ‘if it worked, then everybody would be doing it this way,’ ” he told me, but they quit their jobs and worked on it for a few months with a friends and family round, anyway. “It turns out it does work, and the invention is very novel and hence we’ve been successful in patenting it.”

Rather than send a coherent laser at a single wavelength (1550 nanometers, well into the infrared, is the lidar standard), Baraja uses a set of fixed lenses to refract that beam into a spectrum spread vertically over its field of view. Yet it isn’t one single beam being split but a series of coded pulses, each at a slightly different wavelength that travels ever so slightly differently through the lenses. It returns the same way, the lenses bending it the opposite direction to return to its origin for detection.

It’s a bit difficult to grasp this concept, but once one does it’s hard to see it as anything but astonishingly clever. Not just because of the fascinating optics (something I’m partial to, if it isn’t obvious), but because it obviates a number of serious problems other lidars are facing or about to face.

First, there are next to no moving parts whatsoever in the entire Baraja system. Spinning lidars like the popular early devices from Velodyne are being replaced at large by ones using metamaterials, MEMS, and other methods that don’t have bearings or hinges that can wear out.

Baraja’s “head” unit, connected by fiber optic to the brain.

In Baraja’s system, there are two units, a “dumb” head and an “engine.” The head has no moving parts and no electronics; it’s all glass, just a set of lenses. The engine, which can be located nearby or a foot or two away, produces the laser and sends it to the head via a fiber-optic cable (and some kind of proprietary mechanism that rotates slowly enough that it could theoretically work for years continuously). This means it’s not only very robust physically, but its volume can be spread out wherever is convenient in the car’s body. The head itself also can be resized more or less arbitrarily without significantly altering the optical design, Collarte said.

Second, the method of diffracting the beam gives the system considerable leeway in how it covers the scene. Different wavelengths are sent out at different vertical angles; a shorter wavelength goes out toward the top of the scene and a slightly longer one goes a little lower. But the band of 1550 +/- 20 nanometers allows for millions of fractional wavelengths that the system can choose between, giving it the ability to set its own vertical resolution.

It could for instance (these numbers are imaginary) send out a beam every quarter of a nanometer in wavelength, corresponding to a beam going out every quarter of a degree vertically, and by going from the bottom to the top of its frequency range cover the top to the bottom of the scene with equally spaced beams at reasonable intervals.

But why waste a bunch of beams on the sky, say, when you know most of the action is taking place in the middle part of the scene, where the street and roads are? In that case you can send out a few high frequency beams to check up there, then skip down to the middle frequencies, where you can then send out beams with intervals of a thousandth of a nanometer, emerging correspondingly close together to create a denser picture of that central region.

If this is making your brain hurt a little, don’t worry. Just think of Dark Side of the Moon and imagine if you could skip red, orange and purple, and send out more beams in green and blue — and because you’re only using those colors, you can send out more shades of green-blue and deep blue than before.

Third, the method of creating the spectrum beam provides against interference from other lidar systems. It is an emerging concern that lidar systems of a type could inadvertently send or reflect beams into one another, producing noise and hindering normal operation. Most companies are attempting to mitigate this by some means or another, but Baraja’s method avoids the possibility altogether.

“The interference problem — they’re living with it. We solved it,” said Collarte.

The spectrum system means that for a beam to interfere with the sensor it would have to be both a perfect frequency match and come in at the precise angle at which that frequency emerges from and returns to the lens. That’s already vanishingly unlikely, but to make it astronomically so, each beam from the Baraja device is not a single pulse but a coded set of pulses that can be individually identified. The company’s core technology and secret sauce is the ability to modulate and pulse the laser millions of times per second, and it puts this to good use here.

Collarte acknowledged that competition is fierce in the lidar space, but not necessarily competition for customers. “They have not solved the autonomy problem,” he points out, “so the volumes are too small. Many are running out of money. So if you don’t differentiate, you die.” And some have.

Instead companies are competing for partners and investors, and must show that their solution is not merely a good idea technically, but that it is a sound investment and reasonable to deploy at volume. Collarte praised his investors, Sequoia and Blackbird, but also said that the company will be announcing significant partnerships soon, both in automotive and beyond.

Powered by WPeMatico

Meet Harvestr, a software-as-a-service startup that wants to help product managers centralize customer feedback from various places. Product managers can then prioritize outstanding issues and feature requests. Finally, the platform helps you get back to your customers once changes have been implemented.

The company just raised a $650,000 funding round led by Bpifrance, with various business angels also participating, such as 360Learning co-founders Nicolas Hernandez and Guillaume Alary, as well as Station F director Roxanne Varza through the Atomico Angel Programme.

Harvestr integrates directly with Zendesk, Intercom, Salesforce, Freshdesk, Slack and Zapier. For instance, if a user opens a ticket on Zendesk and another user interacts with your support team through an Intercom chat widget, everything ends up in Harvestr.

Once you have everything in the system, Harvestr helps you prioritize tasks that seem more urgent or that are going to have a bigger impact.

When you start working on a feature or when you’re about to ship it, you can contact your users who originally reached out to talk to you about it.

Eventually, Harvestr should help you build a strong community of power users around your product. And there are many advantages in pursuing this strategy.

First, you reward your users by keeping them in the loop. It should lead to higher customer satisfaction and lower churn. Your most engaged customers could also become your best ambassadors to spread the word around.

Harvestr costs $49 per month for five seats and $99 per month for 20 seats. People working for 360Learning, HomeExchange, Dailymotion and other companies are currently using it.

Powered by WPeMatico

SpinLaunch, a company that aims to turn the launch industry on its head with a wild new concept for getting to orbit, has raised a $35M round B to continue its quest. The team has yet to demonstrate their kinetic launch system, but this year will be the year that changes, they claim.

TechCrunch first reported on SpinLaunch’s ambitious plans in 2018, when the company raised its previous $35 million, which combined with $10M it raised prior to that and today’s round comes to a total of $80M. With that kind of money you might actually be able to build a space catapult.

The basic idea behind SpinLaunch’s approach is to get a craft out of the atmosphere using a “rotational acceleration method” that brings a craft to escape velocity without any rockets. While the company has been extremely tight-lipped about the details, one imagines a sort of giant rail gun curled into a spiral, from which payloads will emerge into the atmosphere at several thousand miles per hour — weather be damned.

Naturally there is no shortage of objections to this method, the most obvious of which is that going from an evacuated tube into the atmosphere at those speeds might be like firing the payload into a brick wall. It’s doubtful that SpinLaunch would have proceeded this far if it did not have a mitigation for this (such as the needle-like appearance of the concept craft) and other potential problems, but the secretive company has revealed little.

The time for broader publicity may soon be at hand, however: the funds will be used to build out its new headquarter and R&D facility in Long Beach, but also to complete its flight test facility at Spaceport America in New Mexico.

“Later this year, we aim to change the history of space launch with the completion of our first flight test mass accelerator at Spaceport America,” said founder and CEO Jonathan Yaney in a press release announcing the funding.

Lowering the cost of launch has been the focus of some of the most successful space startups out there, and SpinLaunch aims to leapfrog their cost savings by offering orbital access for under $500,000. First commercial launch is targeted for 2022, assuming the upcoming tests go well.

The funding round was led by previous investors Airbus Ventures, GV, and KPCB, as well as Catapult Ventures, Lauder Partners, John Doerr and Byers Family.

Powered by WPeMatico

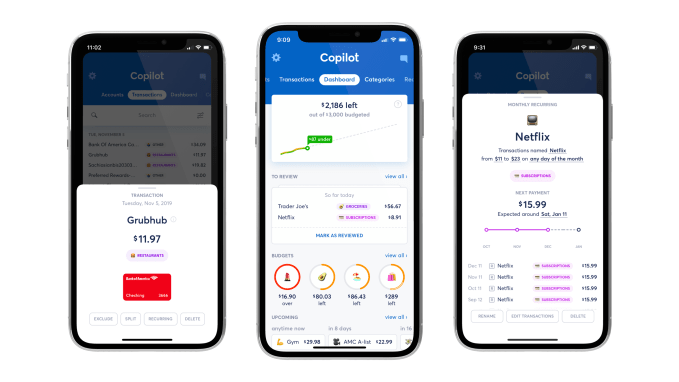

When Intuit acquired Mint more than a decade ago, mobile was in a different place — as were tech-enabled financial services. There hasn’t been much progress for the personal finance tracker app category in the meantime. Mint has stumbled along with integration issues and tiresome data misclassifications. For many, the best alternative has been firing up a spreadsheet.

Copilot is a new personal finance-tracking app from a former Googler that seems like it could garner a following based on its slick design and ease of use. The subscription iOS app lets you load your financial data, create custom categories for transactions and set budgets. It has been invitation-only for the past several months, but is launching publicly today.

Founder Andrés Ugarte told TechCrunch that he started the effort after eight years at Google — most recently inside its Area 120 experimental products division — because of slow progress in the personal finance space since Mint’s acquisition.

“I’ve been trying to use personal finance apps for the last eight years, and I eventually ended up giving up on them,” Ugarte says. “I was willing to make them work, and create my own categories and fix the data so that stuff was all categorized correctly. But I was always disappointed because the apps never felt smart because they would make the same mistakes again.”

I spent a few hours poking around Copilot over the past couple of days and I like what I’ve seen. The design is friendlier than other options, but its major strengths are that you can easily re-categorize a transaction that didn’t automatically fall in the bucket that you wanted it to, mark internal transfers between accounts and exclude one-off purchases from your tracked budget. Other apps have also allowed these functionalities, but Copilot lets you denote whether you want every transaction with a particular vendor to route to a certain category or bypass your budget entirely, so it actually learns from your activity.

In some ways, the killer feature of Copilot is just how great Plaid is. The app relies heavily on the Visa-acquired financial services API startup, and I can see why the startup was so successful. The integration’s intuitiveness alongside Copilot’s already smooth on-boarding process gives users early indication for the app’s thoughtful design.

Copilot has its limitations, mainly in that the team is just two people right now, so those holding out for desktop or Android support might have to wait a bit. Some may be turned off by the app’s $2.99 monthly subscription price, though there are more than a few reasons to avoid free apps that have access to all of your financial info. Copilot maintains that users’ financial info will never be sold to or shared with third parties.

Ugarte has largely been self-funding the effort by selling off his Google shares, but the team just locked down a $250,000 angel round and is searching for more funding.

Powered by WPeMatico

When Visa bought Plaid this week for $5.3 billion, a figure that was twice its private valuation, it was a clear signal that traditional financial services companies are looking for ways to modernize their approach to business.

With Plaid, Visa picks up a modern set of developer APIs that work behind the scenes to facilitate the movement of money. Those APIs should help Visa create more streamlined experiences (both at home and inside other companies’ offerings), build on its existing strengths and allow it to do more than it could have before, alone.

But don’t take our word for it. To get under the hood of the Visa-Plaid deal and understand it from a number of perspectives, TechCrunch got in touch with analysts focused on the space and investors who had put money into the erstwhile startup.

Powered by WPeMatico

The first cannabis startup to raise big money in Silicon Valley is in danger of burning out. TechCrunch has learned that pot delivery middleman Eaze has seen unannounced layoffs, and its depleted cash reserves threaten its ability to make payroll or settle its AWS bill. Eaze was forced to raise a bridge round to keep the lights on as it prepares to attempt major pivot to ‘touching the plant’ by selling its own marijuana brands through its own depots.

TechCrunch spoke with nine sources with knowledge of Eaze’s struggles to piece together this report. If Eaze fails, it could highlight serious growing pains amid the ‘green rush’ of startups into the marijuana business.

Eaze, the startup backed by some $166 million in funding that once positioned itself as the “Uber of pot” — a marketplace selling pot and other cannabis products from dispensaries and delivering it to customers — has recently closed a $15 million bridge round, according to multiple source. The funding was meant to keep the lights on as Eaze struggles to raise its next round of funding amid problems with making decent margins on its current business model, lawsuits, payment processing issues, and internal disorganization.

An Eaze spokesperson confirmed that the company is low on cash. Sources tell us that the company, which laid off some 30 people last summer, is preparing another round of cuts in the meantime. The spokesperson refused to discuss personnel issues but noted that there have been layoffs at many late stage startups as investors want to see companies cut costs and become more efficient.

From what we understand, Eaze is currently trying to raise a $35 million Series D round according to its pitch deck. The $15 million bridge round came from unnamed current investors. (Previous backers of the company include 500 Startups, DCM Ventures, Slow Ventures, Great Oaks, FJ Labs, the Winklevoss brothers, and a number of others.) Originally, Eaze had tried to raise a $50 million Series D, but the investor that was looking at the deal, Athos Capital, is said to have walked away at the eleventh hour.

Eaze is going into the fundraising with an enterprise value of $388 million, according to company documents reviewed by TechCrunch. It’s not clear what valuation it’s aiming for in the next round.

An Eaze spokesperson declined to discuss fundraising efforts but told TechCrunch, “The company is going through a very important transition right now, moving to becoming a plant-touching company through acquisitions of former retail partners that will hopefully allow us to more efficiently run the business and continue to provide good service to customers.

The news comes as Eaze is hoping to pull off a “verticalization” pivot, moving beyond online storefront and delivery of third-party products (rolled joints, flower, vaping products and edibles) and into sourcing, branding and dispensing the product directly. Instead of just moving other company’s marijuana brands between third-party dispensaries and customers, it wants to sell its own in-house brands through its own delivery depots to earn a higher margin. With a number of other cannabis companies struggling, the hope is that it will be able to acquire brands in areas like marijuana flower, pre-rolled joints, vaporizer cartridges, or edibles at low prices.

An Eaze spokesperson confirmed that the company plans to announce the pivot in the coming days, telling TechCrunch that it’s “a pretty significant change from provider of services to operating in that fashion but also operating a depot directly ourselves.”

The startup is already making moves in this direction, and is in the process of acquiring some of the assets of a bankrupt cannabis business out of Canada called Dionymed — which had initially been a partner of Eaze’s, then became a competitor, and then sued it over payment disputes, before finally selling part of its business. These assets are said to include Oakland dispensary Hometown Heart, which it acquired in an all-share transaction (“Eaze effectively bought the lawsuit,” is how one source described the sale). This will become Eaze’s first owned delivery depot.

In a recent presentation deck that Eaze has been using when pitching to investors — which has been obtained by TechCrunch — the company describes itself as the largest direct-to-consumer cannabis retailer in California. It has completed more than 5 million deliveries, served 600,000 customers and tallied up an average transaction value of $85.

To date, Eaze has only expanded to one other state beyond California, Oregon. Its aim is to add five more states this year, and another three in 2021. But the company appears to have expected more states to legalize recreational marijuana sooner, which would have provided geographic expansion. Eaze seems to have overextended itself too early in hopes of capturing market share as soon as it became available.

An employee at the company tells us that on a good day Eaze can bring in between $800,000 and $1 million in net revenue, which sounds great, except that this is total merchandise value, before any cuts to suppliers and others are made. Eaze makes only a fraction of that amount, one reason why it’s now looking to verticatlize into more of a primary role in the ecosystem. And that’s before considering all of the costs associated with running the business.

Eaze is suffering from a problem rampant in the marijuana industry: a lack of working capital. Since banks often won’t issue working capital loans to weed-related business, deliverers like Eaze can experience delays in paying back vendors. Another source says late payments have pushed some brands to stop selling through Eaze.

Another drain on its finances have been its marketing efforts. A source said out-of-home ads (billboards and the like) allegedly were a significant expense at one point. It has to compete with other pot purchasing options like visiting retail stores in person, using dispensaries’ in-house delivery services, or buying via startups like Meadow that act as aggregated online points of sale for multiple dispensaries.

Indeed, Eaze claims that its pivot into verticalization will bring it $204 million in revenues on gross transactions of $300 million. It notes in the presentation that it makes $9.04 on an average sale of $85, which will go up to $18.31 if it successfully brings in ‘private label’ products and has more depot control.

The poor margins are only one of the problems with Eaze’s current business model, which the company admits in its presentation have led to an inconsistent customer experience and poor customer affinity with its brand — especially in the face of competition from a number of other delivery businesses.

Playing on the on-demand, delivery-of-everything theme, it connected with two customer bases. First, existing cannabis consumers already using some form of delivery service for their supply; and a newer, more mainstream audience with disposable income that had become more interested in cannabis-related products but might feel less comfortable walking into a dispensary, or buying from a black market dealer.

It is not the only startup that has been chasing that audience. Other competitors in the wider market for cannabis discovery, distribution and sales include Weedmaps, Puffy, Blackbird, Chill (a brand from Dionymed that it founded after ending its earlier relationship with Eaze), and Meadow, with the wider industry estimated to be worth some $11.9 billion in 2018 and projected to grow to $63 billion by 2025.

Eaze was founded on the premise that the gradual decriminalisation of pot — first making it legal to buy for medicinal use, and gradually for recreational use — would spread across the US and make the consumption of cannabis-related products much more ubiquitous, presenting a big opportunity for Eaze and other startups like it.

It found a willing audience among consumers, but also tech workers in the Bay Area, a tight market for recruitment.

“I was excited for the opportunity to join the cannabis industry,” one source said. “It has for the most part has gotten a bad rap, and I saw Eaze’s mission as a noble thing, and the team seemed like good people.”

Eaze CEO Ro Choy

That impression was not to last. The company, this employee was told when joining, had plenty of funding with more on the way. The newer funding never materialised, and as Eaze sought to figure out the best way forward, the company cycled through different ideas and leadership: former Yammer executive Keith McCarty, who cofounded the company with Roie Edery (both are now founders at another Cannabis startup, Wayv), left, and the CEO role was given to another ex-Yammer executive, Jim Patterson, who was then replaced by Ro Choy, who is the current CEO.

“I personally lost trust in the ability to execute on some of the vision once I got there,” the ex-employee said. “I thought that on one hand a picture was painted that wasn’t the truth. As we got closer and as I’d been there longer and we had issues with funding, the story around why we were having issues kept changing.” Several sources familiar with its business performance and culture referred to Eaze as a “shitshow”.

The quick shifts in strategy were a recurring pattern that started well before the company got tight financial straits.

One employee recalled an acquisition Eaze made several years ago of a startup called Push for Pizza. Founded by five young friends in Brooklyn, Push for Pizza had gone viral over a simple concept: you set up your favourite pizza order in the app, and when you want it, you pushed a single button to order it. (Does that sound silly? Don’t forget, this was also the era of Yo, which was either a low point for innovation, or a high point for cynicism when it came to average consumer intelligence… maybe both.)

Eaze’s idea, the employee said, was to take the basics of Push for Pizza and turn it into a weed app, Push for Kush. In it, customers could craft their favourite mix and, at the touch of a button, order it, lowering the procurement barrier even more.

The company was very excited about the deal and the prospect of the new app. They planned a big campaign to spread the word, and held an internal event to excite staff about the new app and business line.

“They had even made a movie of some kind that they showed us, featuring a caricature of Jim” — the CEO at a the time — “hanging out of the sunroof of a limo.” (I’ve been able to find the opening segment of this video online, and the Twitter and Instagram accounts that had been created for Push for Kush, but no more than that.)

Then just one week later, the whole plan was scrapped, and the founders of Push for Pizza fired. “It was just brushed under the carpet,” the former employee said. “No one could get anything out of management about what had happened.”

Something had happened, though: the company had been taking payments by card when it made the acquisition, but the process was never stable and by then it had recently gone back to the cash-only model. Push for Kush by cash was less appealing. “They didn’t think it would work,” the person said, adding that this was the normal course of business at the startup. “Big initiatives would just die in favor of pushing out whatever new thing was on the product team’s radar.”

Eaze’s spokesperson confirmed that “we did acquire Push For Pizza . . but ultimately didn’t choose to pursue [launching Push For Kush].”

Payments were a recurring issue for the startup. Eaze started out taking payments only in cash — but as the business grew, that became increasingly problematic. The company found itself kicked off the credit card networks and was stuck with a less traceable, more open to error (and theft) cash-only model at a time when one employee estimated it was bringing in between $800,000 and $1 million per day in sales.

Eventually, it moved to cards, but not smoothly: Visa specifically did not want Eaze on its platform. Eaze found a workaround, employees say, but it was never above board, which became the subject of the lawsuit between Eaze and Dionymed. Currently the company appear to only take payments via debit cards, ACH transfer, and cash, not credit card.

Another incident sheds light on how the company viewed and handled security issues.

At one point, employees allegedly discovered that Eaze was essentially storing all of its customer data — including users’ signatures and other personal information — in an Azure bucket that was not secured, meaning that if anyone was nosing around, it could be easily discovered and exploited.

The vulnerability was brought to the company’s attention. It was something that was up to product to fix, but the job was pushed down the list. It ultimately took seven months to patch this up. “I just kept seeing things with all these huge holes in them, just not ready for prime time,” one ex-employee said of the state of products. “No one was listening to engineers, and no one seemed to be looking for viable products.” Eaze’s spokesperson confirms a vulnerability was discovered but claims it was promptly resolved.

Today, the issue is a more pressing financial one: the company is running out of money. Employees have been told the company may not make its next payroll, and AWS will shut down its servers in two days if it doesn’t pay up.

Eaze’s spokesperson tried to remain optimistic while admitting the dire situation the company faces. “Eaze is going to continue doing everything we can to support customers and the overall legal cannabis industry. We’re excited about the future and acknowledge the challenges that the entire community is facing.”

As medicinal and recreational marijuana access became legal in some states in the latter 2010s, entrepreneurs and investors flocked to the market. They saw an opportunity to capitalize on the end of a major prohibition — a once in a lifetime event. But high government taxes, enduring black markets, intense competition, and a lack of financial infrastructure willing to deal with any legal haziness have caused major setbacks.

While the pot business might sound chill, operations like Eaze depend on coordinating high-stress logistics with thin margins and little room for error. Plenty of food delivery startups from Sprig to Munchery went under after running into similar struggles, and at least banks and payment processors would work with them. With the odds stacked against it, Eaze has a tough road ahead.

Powered by WPeMatico