Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Robinhood, the startup with a stock trading app valued upwards of at least $7.6 billion, suffered one of its worst outages on one of the busiest trading days of the year.

As the Dow Jones Industrial Average enjoyed the single biggest point-gain in the history of the index, Robinhood’s application fell prey to an error that locked users out of the service for the duration of Monday’s trading.

“We started experiencing downtime issues across our platform this morning at market open,” a spokesperson wrote in an email. “We don’t have an estimate when the issue will be resolved but all of us at Robinhood are working as hard as we can to resume service.”

One potential cause of the outages could just be the high trading volumes that have accompanied highly volatile markets over the past month. While there were some early reports that the bug was caused by a Leap Day bug, the company has denied that a February 29th error was at fault.

The company’s mistake could cost its users lots of money as they sought to trade on stocks that were hit in last week’s string of losses due to investor worries over the impact the novel coronavirus, COVID-19, would have on the global economy.

This isn’t the first time that Robinhood’s code has got the company into trouble. Last year, faulty coding allowed users to borrow more money than the company intended, giving a potential windfall to would-be traders.

Back in 2013 when the founders of the company discussed their idea around TechCrunch reporter Josh Constine’s kitchen table, they envisioned the app as a way to share hot tips. That quickly morphed into a trading platform that the company says has more than 10 million users on its platform.

The secret to the company’s initial success was free stock trading — a pricing model which many of its competitors have since gone on to copy.

According to Apptopia, Robinhood is far and away the most popular of the free stock trading services, having far more volume and users than its legacy contenders. However, as today’s outage showed, that user base may be negatively impacted by not working with companies who have had their services stress tested over decades. Even so, the big trading houses have also experienced technical issues over the past week, as CNBC reported earlier today.

Powered by WPeMatico

Sonantic, a U.K. startup that has developed “human-quality” artificial voice technology for the games and entertainment industry, has raised €2.3 million in funding.

Leading the round is EQT Ventures, with participation from existing backers, including Entrepreneur First (EF), AME Cloud Ventures and Bart Swanson of Horizons Ventures. I also understand one of the company’s earlier investors is Twitch co-founder Kevin Lin.

Founded in 2018 by CEO Zeena Qureshi and CTO John Flynn as they went through EF’s company builder programme in London, Sonantic (previously Speak Ai) says it wants to disrupt the global gaming and entertainment voice industry. The startup has developed artificial voice tech that it claims is able to offer “expressive, realistic voice acting” on-demand for use by game studios. It already has R&D partnerships underway with more than 10 AAA game studios.

“Getting dialogue into game development is a slow, expensive and labour-intensive task,” says Qureshi, when asked to define the problem Sonantic wants to solve. “Dialogue pipelines consist of casting, booking studios, contracts, scheduling, editing, directing and a whole lot of coordination. Voiced narrative video games can take up to 10 years to make with game design changing frequently, defaulting game devs to carry out several iteration cycles — often leading to going over budgets and game releases being delayed.”

To help remedy this, Sonantic offers what Qureshi dubs “dynamic voice acting on-demand,” with the ability to craft the exact type of character in terms of gender, personality, accent, tone and emotional state. The startup’s human quality text-to-speech system is offered via an API and a graphical user interface tool that lets its synthetic voice actors be edited, sculpted and directed “just like a human actor,” she tells me.

This sees Sonantic work directly with actors to synthesise their voices whilst also harnessing their unique skills in performance. “We then augment how actors work by offering them a digital version of themselves that can create passive income for them,” explains the Sonantic CEO.

For the games studios, Sonantic offers faster iteration cycles at a cheaper price because it cuts down logistical costs and has voice models ready to perform. Its SaaS model and API also makes it easier to create audio performances to test out potential narratives or to finesse a story, helping with editing and directing.

Meanwhile, Sonantic says it is gearing up to publicly reveal how its technology can capture “deep emotions across the full spectrum,” from subtle all the way through to exaggerated, which it says is usually something only very skilled actors can achieve.

Powered by WPeMatico

Last week, I sat down with Connie Chan, a general partner with Andreessen Horowitz who focuses on investing in consumer tech. She joined the firm in 2011 after working at HP in China.

From her temporary offices located in a modest skyscraper with unobscured views of San Francisco, we talked about where she sees the biggest opportunities right now, along with how big of an impact fears over coronavirus could have on the startup industry — and for how long.

Our conversation has been edited for length. You can also find a longer version of our chat in podcast form.

TechCrunch: There’s so much money flowing into the Bay Area and startups generally from all over the world. What happens if that slows down because of the coronavirus?

Connie Chan: It’s interesting, I was just talking to a friend of mine who is an investor in Asia, in China. And she said that some industries are going to suffer significantly. Restaurants, for example, are hurting [along with] any store that relies on foot traffic [like] bookstores, so forth. Yet you see a lot of companies also doing really well in this time. You’ll see grocery delivery as something that’s in high demand. Insurance is in very high demand. People are spending more time at home, so whether it’s games or streaming or whatever they’re doing at home is doing well. Lots of my counterparts in China are also taking all their pitches via video conference. They’re still doing work, but they’re all just working from home.

Where do you think we’ll see the biggest impact most immediately?

Powered by WPeMatico

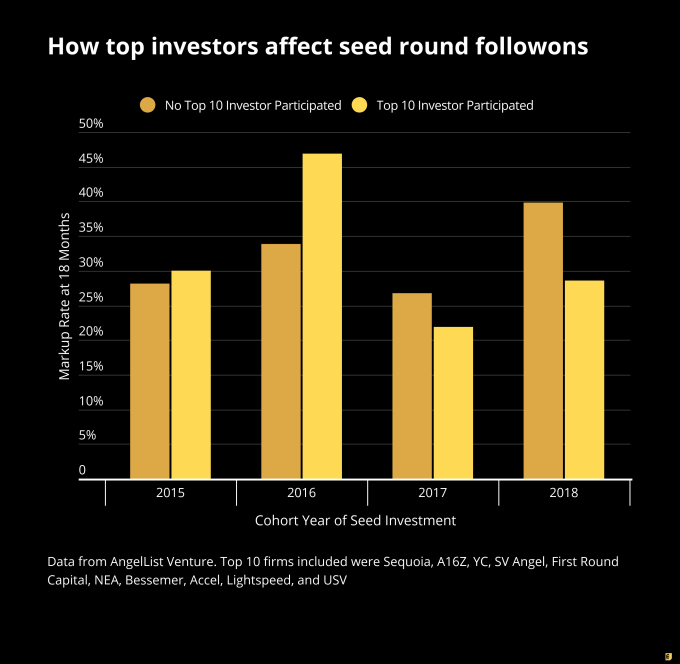

One of the big, ongoing debates in VC and founder circles concerns whether to accept money from top-tier, later-stage venture capitalists during a seed round. Even as their funds reach monstrous sizes, more and more top funds are investing in the earliest stages of a startup’s life, intensifying the question for founders of so-called “signaling risk”: if a later-stage investor in your seed round doesn’t actually do your later-stage rounds, does that negatively signal to other potential investors that they should walk away from your company?

It’s a perennial debate largely because it’s hard to build a quality data set to definitively answer the question. But now, we might have some data that finally sheds light on this signaling risk.

AngelList’s data science team collected information from its Venture portfolio (which includes approximately $1.8 billion assets under management according to the company) to look at how signaling risk has changed over time according to the cohort performance of startups in their portfolio. The essential question was, “Does having a top-10 investor in your seed round improve or hurt your chances of a follow-on round 18 months later, compared to seed rounds without such an investor?” Their work produced this chart:

Two quick and important notes. First, AngelList processed its own data (given the need to protect confidentiality, I wasn’t given direct access to their data set for analysis). Second, AngelList supplied notes on its methodology, which I have attached at the end unedited for those curious how the data set and chart were constructed.

The short summary of the data is that in the 2015 and 2016 cohorts, having a top-10 VC investor in your seed round appeared to improve a startup’s chances to raise a follow-on equity round, particularly in 2016. However, that benefit seemed to reverse itself in the 2017 cohort, and the negative effect was magnified in the 2018 cohort.

The typical caveat emptor applies: correlations are not causations. That said, we know signaling is a real mechanism for VCs to make an investment decision, so there is at least some form of causal path here in the data.

My analysis (and it should be noted this isn’t endorsed by AngelList) is that top-10 investors like Sequoia or a16z have radically expanded their seed investment programs over the past two years in pursuit of more and more cap table access. As VCs scour the universe looking for the next great startup, those firms with the deepest pockets are choosing to invest in any round rather than to try to time their investment into a later round that would more properly fit into the thesis of their massive funds.

So for startups in the 2015 and 2016 cohorts, there was real selectivity (or at least, more selectivity) when it came to getting an investment from a top investor. Those startups may not have gone through the full due diligence process typical of a Series A investment, but they were typically well-vetted, and that sent a strong positive signal to other investors in later rounds.

Perhaps most importantly, and this is based on my own anecdotal data here, but most Series A and later firms that participated in a seed round in those years ended up getting toward the kind of equity ownership they normally target (let’s say 20% as a typical example). So the signaling risk was fairly mute, since if an investor already has their ownership locked in, it’s understandable they wouldn’t necessarily lead the next venture rounds of a company.

All that has changed in the last two years though. Large funds increasingly slosh money through the ecosystem, whether directly as a firm, through seed funds managed by GPs, through scout networks, or indirectly by investing in other seed funds. The exclusivity of these sorts of investments has markedly declined as the capital flood has flowed through the Valley.

Plus, these firms now write ever-smaller checks, and may even join party rounds as well, which means that their ownership post-seed is not nearly as high as it once was. If a top firm does part of your seed and owns 3%, there really is a legitimate question as to why they wouldn’t fund your Series A if they were indeed excited about your prospects and also had information rights to keep track of your startup’s development.

I’ve talked quite extensively about how there are now six stages of seed investing in 2020, and that founders should more carefully identify which stage they truly are in and reach out judiciously to the investors who actually fit those micro-stages.

I think this AngelList data would seem to indicate that big-firm investors can be complicated at the seed stage these days. I’ve generally argued that signaling risk is a relative myth these days, given the competition for deals, but AngelList’s data would seem to indicate that the signaling risk may be more important than I expected.

We looked at all of the AngelList Venture seed deals (investments by syndicates and funds tagged as “Pre-Seed”, “Seed”, or “Seed+”) that closed in the given year-cohort. Then we looked at whether, after 18 months, those investments had been marked up and had not exited. We believe that is the best proxy in our data for “was an active Series A company”, because the AngelList valuation methodology is to only update valuations on priced equity rounds; companies that raised again with SAFEs would not trigger a markup, even if those SAFEs are at a higher cap. For 2018 deals, we did not consider deals after August 2018 because deals at the end of that year have not had 18 months to season.

After segmenting by year cohort, we further segmented based on whether those deals had the participation of a Top 10 Seed investor. That set of investors was not based on AngelList data but instead used an external data source for which Seed investors have surfaced the most “unicorn” deals. We use the loosest definition of participation: a deal where one of these firms led the seed deal, one of these firms co-led the seed deal, one of these firms wrote a 50k check while a different firm wrote a 500k check, or one or more of these firms participated in a “party round” would all be counted as having the participation of a Top 10 investor.

And adding one more note here that the top-10 investors included in the sample were ultimately Sequoia, a16z, YC, SV Angel, First Round Capital, NEA, Bessemer, Accel, Lightspeed and USV.

Powered by WPeMatico

Podium, a Utah-based SaaS company focused on small business customer interactions, added payments technology to its product suite today. The move accretes a new income stream to the company’s quickly growing annual recurring revenue (ARR).

While I tend to stay away from product news, Podium’s decision to add payment technology to its service hit a number of themes that we’ve recently explored, like the rise of payments technology players (Finix, for example) and how it is increasingly common to see fintech and finservices solutions find their way into new places.

And Podium is one of SaaS’s fastest-growing companies. Cribbing from some prior reporting, Podium’s ARR reached roughly $30 million at the end of 2017. It expected to reach $60 million by the end of 2018, and had $100 million in its sights for 2019. Those figures, collected in November, are now decidedly out of date. But they illustrate how quickly Podium was growing before it added payments to its arsenal.

Update: Adding a little clarification here. The addition of payments to Podium’s tech allows its customers (the companies using its software) to collect payments from their own customers. This gives Podium customers the ability to charge folks for their goods and services in a manner that is integrated into the rest of the software company’s service.

I wanted to dig into the news, so I emailed with Eric Rea, the company’s CEO. What follows is an email exchange (due to scheduling difficulties). We’ll chat after about what was said.

TechCrunch: Did Podium build out its own payments tech or does it employ third-party tech like Finix?

Podium: Podium has a great relationship with Stripe, a fellow Y Combinator company, which was partnered with our own technology to make it work best for our customers. This was key in order to create a payment tool that actually works in the kinds of businesses we work with. [The] majority of businesses who operate from a physical location, from dentist offices and home services companies to larger retail stores, have very specific needs that haven’t been met by traditional card present or POS systems. As a result, many of them rely on mailing paper invoices or awkward conversations where someone gives their card info over the phone. Putting Podium’s platform technology alongside Stripe’s best-in-class processing tech was able to finally meet this need for the companies that create roughly a third of the US non-farming GDP.

TechCrunch: Does the majority of the economics (profit/margin) from the payments product accrue to the Podium client, or Podium itself?

Podium: The genius behind this product is just how immense the economic impact is for these companies. For many of them, they are able to create a whole new convenient way to serve their customers through conversational commerce, and in doing so, they are able to be more successful.

One of our major furniture retailers that participated in the beta of Payments told me about how there has been a completely new selling motion that has opened up for their stores through this product. One of their biggest leaks was when customers would come in and look at a couch or dresser, but didn’t know if dimensions would work in their home. Once they left, there was a steep drop off getting them back into the store to actually make the purchase.

Now, with Payments, they are able to give all the info to their customer, have them check it out in their home and then text them if it works or not. They can then use Payments to collect payment in the very same text conversation and the delivery crew can complete the purchase all in the same day without having the customer return to the store. So it’s not just shifting where they are processing their payments, but opening up new revenue that they would never have had before they started using Payments.

Then consider the ancient process that businesses are still using who invoice for services, like a dentist or a home services provider. A majority are still using mailed statements and invoices or phone conversations. Believe it or not, the expenses for these are immense. Not only that, but the turnaround and success rates are abysmal, meaning these businesses have to wait weeks to months in order to receive payment, if at all. With Payments, it is as quick as a seamless text.

In our beta, Payments tripled the conversion rates over invoices and reduced employee workload related to payment by 80%. In healthcare, for example, 40% of customers send payment within 48 hours. To get that same level through their legacy operations, it would take 14 days to get to that point. The economic impact on that speed and completion is astounding for these businesses.

On the processing, Podium sees the profit on the transaction cost.

TechCrunch: Does Podium anticipate that payments will provide material revenue over the next 18 months? 36?

Podium: Yes. We see this as being the second major phase of the Podium platform. We have been proud to have created one of the fastest-growing SaaS companies in history through our existing products. We have 43,000 businesses currently using Podium, and one of the biggest things they have all been telling us is how much they need a tool like this. Just in our existing customer base and verticals, they are creating more than $100B in gross processing volume annually in payments that are better suited to be done through this tool.

TechCrunch: How long did it take to build out the tech?

Podium: This product actually took the longest of all of our products to develop, given the unique expectations and requirements it took on the technology side. This product has been about a year in the making. When it comes to the business of making money and us being the facilitator of that, we take it very seriously to ensure the tool is secure and stable.

TechCrunch: What percent of Podium customers are good candidates to use the tech?

Podium: Almost universal. We gave a lot of intention behind making this a tool that would work across market verticals so that our customers could provide a better experience for their customers and get paid faster at the same time.

TechCrunch: What is the fee and cost structure?

Podium: We charge a flat rate for processing, which is intentional to allow transparency and consistency in their fees.

It’s not a surprise that Podium is taking the economics of the payment processing (with Stripe doing well at the same time). This means that Podium’s business itself will grow thanks to its addition.

At the same time, the clients using Podium’s platform also do well. If the feature can assist as many companies as Podium expects, then it could help a host of small, local firms boost their sales by improving their respective close rates. Even merely faster payments could help smaller shops better manage their cash flow.

So this feels a bit like a win-win. And it goes to show that the addition of payments to other bits of tech is more than hype (Finix will like that). Instead, it feels like adding the ability for transactions to flow directly through one’s platform is going to rise in popularity. Podium is not the first to the trend, and it won’t be the last. But it is a company that could accelerate the trend thanks to its scale and, so far at least, success.

What we’d love to see, frankly, is an S-1 from Podium this year; that would allow us to better dissect its business. Now at least we’ll have one more thing to look for when we do get the document.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re in for a treat, as we get to dig into Procore’s S-1 filing. In case you aren’t familiar, Procore sells software that helps manage construction projects, but it offers more than a single app: Procore’s service allows other apps to plug into it, making it a platform of sorts. The company filed to go public last Friday, meaning that we have endless new numbers to delve into.

Even better for us, Procore is a SaaS company, which means we can understand its numbers.

Procore lists $100 million as its IPO placeholder raise, intends to list on the NYSE as PCOR and its debut is being underwritten by Goldman, J.P. Morgan, Barclays and Jefferies.

Why do we care about this particular IPO? A few reasons. First, Procore filed to go public after the worst week in the stock market since the 2008 crash. That’s either calculated bravery, unbridled hubris or accidental folly. We’ll see. And second, the company’s backers are well-known: Bessemer, Greater Pacific Capital, ICONIQ, Dragoneer and Tiger, according to Crunchbase.

Powered by WPeMatico

Good morning friends, and welcome back to TechCrunch’s Equity Monday, a short-form audio hit to kickstart your week. Regular Equity episodes still drop Friday morning, so if you’ve listened to the show over the years don’t worry — we’re not changing the main show. (Here’s last week’s episode with Danny Crichton, going over the huge Roblox round and what is going on with no-code startups.)

What to say about this Monday other than it feels a bit like last Monday. The markets aren’t doing well, coronavirus is a worry, and we have a cool early-stage round to talk about.

After the stock market took a beating last week, the weekend brought more news concerning the novel coronavirus, with more infections being discovered in the United States. It’s not been the best time to check your 401k if you saving for the long-term.

But in better news, DoorDash’s filing was followed by one from Procore, meaning that IPO season isn’t dead, it’s just glacial, slow, slothful, and far too measured compared to our prior hopes.

This week will see a few sets of earnings that we care about some (JD.com), less, (HPE), and lots (Zoom). When Zoom reports on March 4th it will be carrying the torch for recent, venture-backed IPOs, SaaS companies more broadly, and future-of-work startups specifically. Other than that, no one will be watching what happens to the video conferencing startup that is caught in a rare COVID19 updraft.

Next, we talked about Briza, a very neat early-stage startup that is working in the commercial insurance API space. Yes, this the fusion of several things I love to write about. Namely insurance-tech and API-infra companies. What would you get if you crossed the insurance marketplaces we’ve been writing about with Plaid? Something like Briza, I reckon.

The 500 Startups-backed company has put together $3 million in capital to date, has 10 people on-staff, is looking to double its personnel, and is heading to the market soon on the back of some notable momentum. With more insurance providers hitting Briza up for inclusion in its product, the startup has good pace heading into its impending Demo Day. And it already has the cash it needs to grow.

Infra is hot because it’s the digital equivalent of selling picks and shovels. And APIs are hot because they are the SaaS of infra.

Infra APIs? So hot right now.

I’m stoked beyond belief that Equity turns three this month. Who would have thought that our little show that started life as a few Facebook Lives with myself, Katie Roof (WSJ) and Matthew Lynley (ex-Brex and now a solo operator) would make it this far. I’m lucky to still be a part of it.

Ok! Back Friday. Stay cool.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

mParticle, which helps companies like Spotify, Paypal and Starbucks umanage their customer data, is announcing that it has raised $45 million in Series D funding.

Co-founder and CEO Michael Katz told me that the company has benefited from broader shifts — like new privacy regulation and the shift away from cookie-based browser tracking — that increase brands’ needs for a platform like mParticle that uses “modern data infrastructure” to deliver a personalized experience for customers without running afoul of any regulations.

As result, he said mParticle has nearly quintupled its revenue since it raised a $35 million Series C in 2017. (The company has raised more than $120 million total.)

“The challenges that we solve are universal,” Katz said. “It doesn’t matter if there’s a small company or big company. Data fragmentation, data quality, consistent change in the privacy landscape, consistent change in the technology ecosystem, these are universal challenges.”

Perhaps for that very reason, a whole industry of customer data platforms has sprung up since mParticle was founded back in 2013, all offering tools to help marketers create a single view of their customers by unifying data from various sources. Even big players like Adobe and Salesforce have announced their own CDPs as part of their larger marketing clouds.

When asked about the competition, Katz said, “The market has responded overwhelmingly by saying, ‘I don’t want one vendor to rule everything for me.’ Why be beholden to one suite of tools that’s just an amalgamation of products that were built in the early 2000s?”

Instead, he argued that mParticle customers want “a best-in-breed combination of independent solutions that can be integrated seamlessly.”

Getting back to the new funding — Arrowroot Capital led the round, with the firm’s managing partner Matthew Safaii joining mParticle’s board of directors. Existing investors also participated.

Katz said the funding will be spent in three broad areas: building new products, scaling its global data infrastructure and finding new partners. In fact, the company is also announcing a partnership with LiveRamp, through which mParticle customers can combine their first-party data with the third-party party data from Liveramp.

“We see this partnership with Liveramp as an opportunity to extend the surface area by which our customers can deliver highly personalized, privacy-friendly experiences,” Katz said.

Powered by WPeMatico

The world of consumer banking has seen a massive shift in the last ten years. Gone are the days where you could open an account, take out a loan, or discuss changing the terms of your banking only by visiting a physical branch. Now, you can do all this and more with a few quick taps on your phone screen — a shift that has accelerated with customers expecting and demanding even faster and more responsive banking services.

As one mark of that switch, today a startup called Thought Machine, which has built cloud-based technology that powers this new generation of services on behalf of both old and new banks, is announcing some significant funding — $83 million — a Series B that the company plans to use to continue investing in its platform and growing its customer base.

To date, Thought Machine’s customers are primarily in Europe and Asia — they include large, legacy outfits like Standard Chartered, Lloyds Banking Group, and Sweden’s SEB through to “challenger” (AKA neo-) banks like Atom Bank. Some of this financing will go towards boosting the startup’s activities in the US, including opening an office in the country later this year and moving ahead with commercial deals.

The funding is being led by Draper Esprit, with participation also from existing investors Lloyds Banking Group, IQ Capital, Backed and Playfair.

Thought Machine, which started in 2014 and now employs 300, is not disclosing its valuation but Paul Taylor, the CEO and founder, noted that the market cap is currently “increasing healthily.” In its last round, according to PitchBook estimates, the company was valued at around $143 million, which, at this stage of funding, puts this latest round potentially in the range of between $220 million and $320 million.

Thought Machine is not yet profitable, mainly because it is in growth mode, said Taylor. Of note, the startup has been through one major bankruptcy restructuring, although it appears that this was mainly for organisational purposes: all assets, employees and customers from one business controlled by Taylor were acquired by another.

Thought Machine’s primary product and technology is called Vault, a platform that contains a range of banking services: checking accounts, savings accounts, loans, credit cards and mortgages. Thought Machine does not sell directly to consumers, but sells by way of a B2B2C model.

The services are provisioned by way of smart contracts, which allows Thought Machine and its banking customers to personalise, vary and segment the terms for each bank — and potentially for each customer of the bank.

It’s a little odd to think that there is an active market for banking services that are not built and owned by the banks themselves. After all, aren’t these the core of what banks are supposed to do?

But one way to think about it is in the context of eating out. Restaurants’ kitchens will often make in-house what they sell and serve. But in some cases, when it makes sense, even the best places will buy in (and subsequently sell) food that was crafted elsewhere. For example, a restaurant will re-sell cheese or charcuterie, and the wine is likely to come from somewhere else, too.

The same is the case for banks, whose “Crown Jewels” are in fact not the mechanics of their banking services, but their customer service, their customer lists, and their deposits. Better banking services (which may not have been built “in-house”) are key to growing these other three.

“There are all sorts of banks, and they are all trying to find niches,” said Taylor. Indeed, the startup is not the only one chasing that business. Others include Mambu, Temenos and Italy’s Edera.

In the case of the legacy banks that work with the startup, the idea is that these behemoths can migrate into the next generation of consumer banking services and banking infrastructure by cherry-picking services from the VaultOS platform.

“Banks have not kept up and are marooned on their own tech, and as each year goes by, it comes more problematic,” noted Taylor.

In the case of neobanks, Thought Machine’s pitch is that it has already built the rails to run a banking service, so a startup — “new challengers like Monzo and Revolut that are creating quite a lot of disruption in the market” (and are growing very quickly as a result) — can integrate into these to get off the ground more quickly and handle scaling with less complexity (and lower costs).

Taylor was new to fintech when he founded Thought Machine, but he has a notable track record in the world of tech that you could argue played a big role in his subsequent foray into banking.

Formerly an academic specialising in linguistics and engineering, his first startup, Rhetorical Systems, commercialised some of his early speech-to-text research and was later sold to Nuance in 2004.

His second entrepreneurial effort, Phonetic Arts, was another speech startup, aimed at tech that could be used in gaming interactions. In 2010, Google approached the startup to see if it wanted to work on a new speech-to-text service it was building. It ended up acquiring Phonetic Arts, and Taylor took on the role of building and launching Google Now, with that voice tech eventually making its way to Google Maps, accessibility services, the Google Assistant and other places where you speech-based interaction makes an appearance in Google products.

While he was working for years in the field, the step changes that really accelerated voice recognition and speech technology, Taylor said, were the rapid increases in computing power and data networks that “took us over the edge” in terms of what a machine could do, specifically in the cloud.

And those are the same forces, in fact, that led to consumers being able to run our banking services from smartphone apps, and for us to want and expect more personalised services overall. Taylor’s move into building and offering a platform-based service to address the need for multiple third-party banking services follows from that, and also is the natural heir to the platform model you could argue Google and other tech companies have perfected over the years.

Draper Esprit has to date built up a strong portfolio of fintech startups that includes Revolut, N26, TransferWise and Freetrade. Thought Machine’s platform approach is an obvious complement to that list. (Taylor did not disclose if any of those companies are already customers of Thought Machine’s, but if they are not, this investment could be a good way of building inroads.)

“We are delighted to be partnering with Thought Machine in this phase of their growth,” said Vinoth Jayakumar, Investment Director, Draper Esprit, in a statement. “Our investments in Revolut and N26 demonstrate how banking is undergoing a once in a generation transformation in the technology it uses and the benefit it confers to the customers of the bank. We continue to invest in our thesis of the technology layer that forms the backbone of banking. Thought Machine stands out by way of the strength of its engineering capability, and is unique in being the only company in the banking technology space that has developed a platform capable of hosting and migrating international Tier 1 banks. This allows innovative banks to expand beyond digital retail propositions to being able to run every function and type of financial transaction in the cloud.”

“We first backed Thought Machine at seed stage in 2016 and have seen it grow from a startup to a 300-person strong global scale-up with a global customer base and potential to become one of the most valuable European fintech companies,” said Max Bautin, Founding Partner of IQ Capital, in a statement. “I am delighted to continue to support Paul and the team on this journey, with an additional £15 million investment from our £100 million Growth Fund, aimed at our venture portfolio outperformers.”

Powered by WPeMatico

A new startup called Notivize aims to give product teams direct access to one of their most important tools for increasing user engagement — notifications.

The company has been testing the product with select customers since last year and says it has already sent hundreds of thousands of notifications. And this week, it announced that it has raised $500,000 in seed funding led by Heroic Ventures .

Notivize co-founder Matt Bornski has worked at a number of startups, including AppLovin and Wink, and he said he has “so many stories I can tell you about the time it takes to change a notification that’s deeply embedded in your stack.”

To be clear, Bornski isn’t talking about a simple marketing message that’s part of a scheduled campaign. Instead, he said that the “most valuable” notifications (e.g. the ones that users actually respond to) are usually driven by activity in an app.

For example, it might sound obvious to send an SMS message to a customer once the product they’ve purchased has shipped, but Bornski said that actually creating a notification like that would normally require an engineer to write new code.

“There’s the traditional way that these things are built: The product team specs out that we need to send this email when this happens, or send this SMS or notification when this happens, then the engineering team will go in and find the part of the code where they detect that such a thing has happened,” he said. “What we really want to do is give [the product team] the toolkit, and I think we have.”

So with Notivize, non-coding members of the product and marketing team can write “if-then” rules that will trigger a notification. And this, Bornski said, also makes it easier to “A/B test and optimize your copy and your send times and your channels” to ensure that your notifications are as effective as possible.

He added that companies usually don’t build this for themselves, because when they’re first building an app, it’s “not a rational thing to invest your time and effort in when you’re just testing the market or you’re struggling for product market fit.” Later on, however, it can be challenging to “go in and rip out all the old stuff” — so instead, you can just take advantage of what Notivize has already built.

Bornski also emphasized that the company isn’t trying to replace services that provide the “plumbing” for notifications. Indeed, Notivize actually integrates with SendGrid and Twilio to send the notifications.

“The actual sending is not the core value [of what we do],” he said. “We’re improving the quality of what you’re paying for, of what you send.”

Notivize allows customers to send up to 100 messages per month for free. After that, pricing starts at $14.99 per month.

“The steady march of low-code and no-code solutions into the product management and marketing stack continues to unlock market velocity and product innovation,” said Heroic Ventures founder Michael Fertik in a statement. “Having been an early investor in several developer platforms, it is clear that Notivize has cracked the code on how to empower non-technical teams to manage critical yet complex product workflows.”

Powered by WPeMatico

{kind=link}