Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

More than ever before, people are getting life’s essentials delivered — good news for Amazon, but bad news for the environment, which must bear the consequences of the resulting waste. LivingPackets is a Berlin-based startup that aims to replace the familiar cardboard box with an alternative that’s smarter, more secure and possibly the building block of a new circular economy.

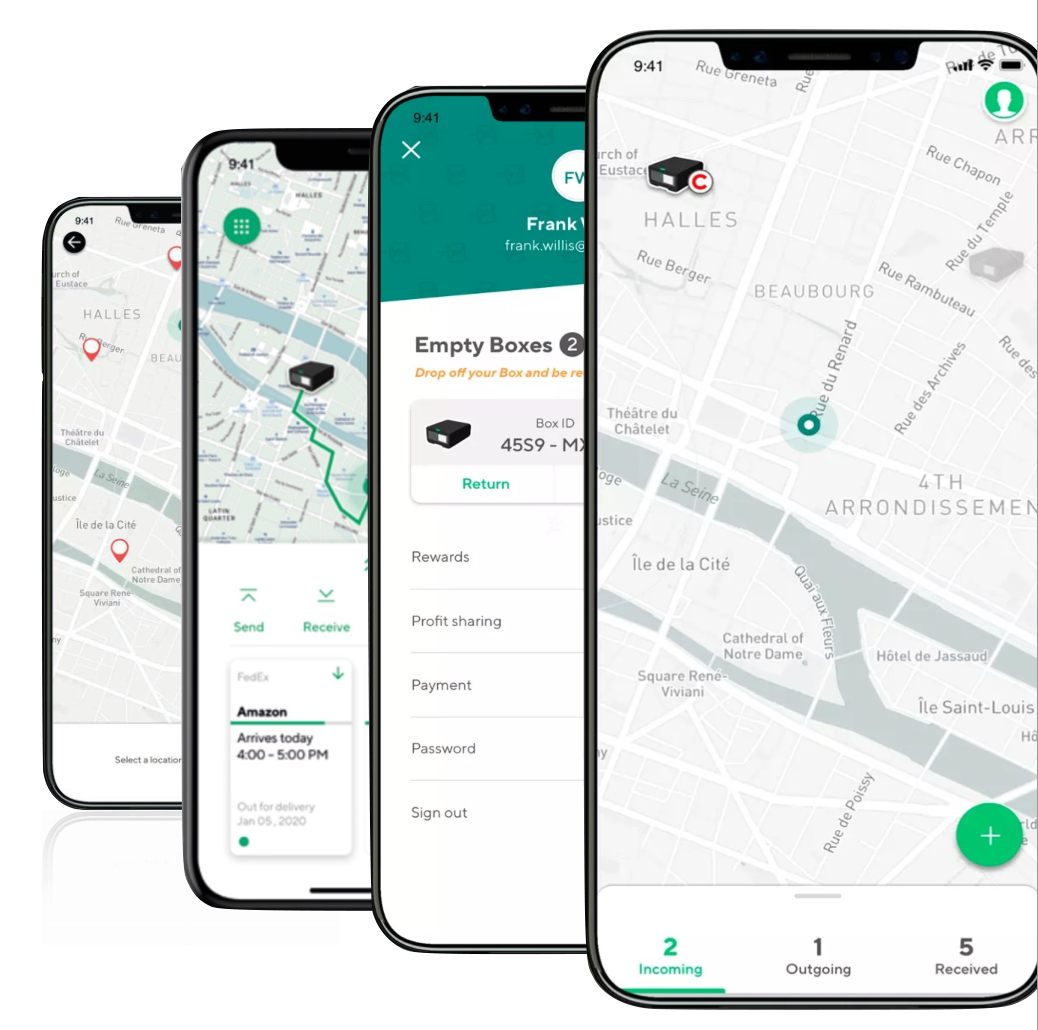

The primary product created by LivingPackets is called The Box, and it’s just that: a box. But not just any box. This one is reusable, durable, digitally locked and monitored, with a smartphone’s worth of sensors and gadgets that make it trackable and versatile, and an E-Ink screen so its destination or contents can be updated at will. A prototype shown at CES and a few other locations attracted some interest, but the company is now well into producing V2 of The Box, improved in many ways and ready to be deployed at the scale of hundreds of thousands.

Sure, it costs a lot more than a cardboard box. But once a LivingPackets Box has been used a couple hundred times for returns and local distribution purposes, it breaks even with its paper-based predecessor. Cardboard is cheap to make new, but it doesn’t last long — and that’s not its only problem.

The Box, pictured here with standard cardboard boxes on a conveyor belt, is meant to be compatible with lots of existing intrastructure. Image Credits: LivingPackets

“If you think about it, online transactions are still risky,” said co-founder Sebastian Rumberg. “The physical transaction and financial transaction don’t happen in parallel: You pay up front, and the seller sends something into the void. You may not receive it, or maybe you do and you say you didn’t, so the company has to claim it with insurers.”

“The logistics system is over-capacity; there’s frustration with DHL and other carriers,” he said. “People in e-commerce and logistics know what they’re missing, what their problems are. Demand has grown, but there’s no innovation.”

And indeed, it does seem strange that although delivery has become much more important to practically everyone over the last decade and especially in recent months, it’s pretty much done the same way it’s been done for a century — except you might get an email when the package arrives. LivingPackets aims to upend this by completely reinventing the package, leaving things like theft, damage and missed connections in the past.

Apps let users track the location and status of their box. Image Credits: LivingPackets

“You’re in full control of everything involved,” he explained. “You know where the parcel is, what’s happening to it. You can look inside. You can say, I’m not at the location for delivery right now, I’m at my office, and just update the address. You don’t need filling material, you don’t need a paper label. You can tell when the seal is broken, when the item is removed.”

It all sounds great, but cardboard is simple and, while limited, proven. Why should anyone switch over to such a fancy device? The business model has to account for this, so it does — and then some.

To begin with, LivingPackets doesn’t actually sell The Box. It provides it to customers and charges per use — “packaging as a service,” as they call it. This prevents the possibility of a business balking at the upfront cost of a few thousand of these.

As a service, it simplifies a lot of existing pain points for merchants, consumers and logistics companies.

For merchants, among other things, tracking and insurance are much simpler. As co-founder Alexander Cotte explained, and as surely many reading this have experienced, it’s practically impossible to know what happened to a missing package, even if it’s something large or expensive. With better tracking, lossage can be mitigated to start, and the question of who’s responsible, where it was taken, and so on can be determined in a straightforward way.

For packaging and delivery companies, the standard form factor with adjustable interior makes these boxes easy to pack and difficult to meddle with or damage — tests with European online retail showed that handling time and costs can be reduced by more than half. LivingPackets also pays for pickup, so delivery companies can recoup costs without changing routes. And generally speaking, more data, more traceability, is a good thing.

For consumers, the most obvious improvement is returns; no need to print a label or for the company to pre-package one, just notify them and the return address appears on the box automatically. In addition there are opportunities once an essentially pre-paid box is in a consumer’s house: for instance, selling or donating an old phone or laptop. LivingPackets will be operating partnerships whereby you can just toss your old gear in the box and it will make its way to the right locations. Or a consumer can hang onto the box until the item they’re selling on eBay is bought and send it that way. Or a neighbor can — and yes, they’re working on the public health side of that, with antibiotic coatings and other protections against spreading COVID-19.

The Box locks securely but also folds down for storage when empty. Image Credits: LivingPackets

The idea underpinning all this, and which was wrapped up in this company from the start, is that of creating a real circular economy, building decentralized value and reducing waste. Even The Box itself is made of materials that can be reused, should it be damaged, in the creation of its replacement. In addition to the market efficiencies added by turning parcels into traveling IoT devices, reusing the boxes could reduce waste and carbon emissions — once you get past the first hundred uses or so, The Box pays for itself in more ways than one. Early pilots with carriers and retailers in France and Germany have borne this out.

That philosophy is embodied in LivingPackets’ unusual form of funding itself: a combination of bootstrapping and crowdsourced equity.

Cotte and his father founded investment firm the Cotte Group, which provided a good starting point for said bootstrapping, but he noted that every employee is taking a less than competitive wage with the hope that the company’s profit-sharing plan will pan out. Even so, with 95 employees, that amounts to several million a year even by the most conservative estimate — this is no small operation.

CEO Alex Cotte sits with V2 of The Box. Image Credits: LivingPackets

Part of keeping the lights on, then, is the ongoing crowdfunding campaign, which has pulled in somewhere north of €6 million, from individuals contributing as little as €50 or as much as €20,000. This, Cotte said, is largely to finance the cost of production, while he and the founding team essentially funded the R&D period. Half of future profits are earmarked for paying back these contributors multiple times their investment — not exactly the sort of business model you see in Silicon Valley. But that’s kind of the point, they explained.

“Obviously all the people working for us believe deeply in what we’re doing,” Cotte said. “They’re willing to take a step back now to create value together and not just take value out of an existing system. And you need to share the value you create with the people who helped you create it.”

It’s hard to imagine a future where these newfangled boxes replace even a noticeable proportion of the truly astronomical number of cardboard boxes being used every day. But even so, getting them into a few key distribution channels could prove they work as intended — and improvements to the well-oiled machines (and deeply rutted paths) of logistics can spread like wildfire once the innumerable companies the industry touches see there’s a better way.

The aims and means of LivingPackets may be rather utopian, but that could be the moonshot thinking that’s necessary to dislodge the logistics business from its current, decidedly last-century methods.

Powered by WPeMatico

My friend and colleague Natasha Mascarenhas has been reporting on the edtech beat quite a lot in 2020. So far reading her coverage, I’ve discovered that not only is edtech less dull than I anticipated, it’s actually somewhat interesting on a regular basis.

This week, for example, India’s Byju bought WhiteHat Jr., another Indian edtech company, for $300 million. So what, you’re thinking, that’s just another startup deal? Yes, but it was an all-cash transaction, and White Hat Jr. was only 18 months old.

That’s enough to tell you that edtech is hot at the moment. Which makes sense: much of the world is sheltering at home with school and offices shuttered.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The COVID-19 era has provided an enormous boon to many software startups, though some more than others. Luckily for its boosters, edtech, after being neglected by VCs due to an expectation of small exits and long sales cycles thanks to red tape, is one of the sectors enjoying renewed interest from private investors and customers alike.

According to a Silicon Valley Bank (SVB) markets-focused report, edtech venture funding reached a local-maxima in Q2 2020, jumping more than 60% from the first quarter of this year to the second. On a year-over-year basis, Q2’s VC edtech results were even more impressive.

According to a Silicon Valley Bank (SVB) markets-focused report, edtech venture funding reached a local-maxima in Q2 2020, jumping more than 60% from the first quarter of this year to the second. On a year-over-year basis, Q2’s VC edtech results were even more impressive.

But, there’s some nuance to the data that should temper declamations that private edtech funding is forever changed.

This morning let’s peel apart the SVB data and parse through edtech funding rounds themselves from the second quarter to see what we can learn. COVID-19 is remaking the global economy as we speak, so it’s up to us to understand its evolving form.

From the top-line numbers, you’d be forgiven for thinking that edtech’s Q2 venture capital results were across-the-board impressive.

Before we dig into the results themselves, here’s the chart you need:

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

As ever, I was joined by TechCrunch managing editor Danny Crichton and our early-stage venture capital reporter Natasha Mascarenhas. We had Chris on the dials and a pile of news to get through, so we were pretty hyped heading into the show.

But before we could truly get started we had to discuss Cincinnati, and TikTok. Pleasantries and extortion out of the way, we got busy:

It was another fun week! As always we appreciate you sticking with and supporting the show!

Equity drops every Monday at 7:00 a.m. PT and Friday at 6:00 a.m. PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Mashroom, the London proptech that offers an “end-to-end” lettings and property management service, has raised £4 million in new funding.

Backing comes from existing unnamed private investors and matched funding from the U.K. taxpayer-funded Future Fund. It brings total funding to date for the company to £7 million.

Pitching itself as going “beyond the tenant-finding service” to include the entire rental journey — from property advertising, arranging viewings, credit history checks and maintenance to end of tenancy and dispute resolution — the self-service platform lets landlords list their property, which tenants can then rent easily.

This includes digital credit and reference checks and the signing of rental agreements and tenancy renewals. In addition, open banking is employed to collect rental payments and provide real-time payment information to landlords.

“Letting and renting is, for the most part, still a fragmented, bricks-and-mortar industry,” says Mashroom founder and ex-venture capitalist Stepan Dobrovolskiy. “The experience as a landlord or tenant normally still involves a traditional estate agent who acts as intermediary and charges a hefty fee. While plenty of new players have come along with tech to solve certain points in the experience, we are the first to look at the entire process from end to end.”

Over on Extra Crunch, learn more about the opportunities within property tech with A/O PropTech, the European VC disrupting the €230 trillion real estate industry.

Dobrovolskiy says this sees Mashroom digitise about “98%” of the rental journey, although he maintains that some human interaction is, and perhaps always will be, necessary. “Unlike most traditional agents, we are also still there to help after tenants move in — things like maintenance requests, insuring contents, moving out or extending contracts at the end of the tenancy. We fundamentally believe that automation and tech should augment rather than replace human interactions in this market, and a big part of our brand is to create better relationships between landlords and tenants,” he says.

As an example, Mashroom incentivises tenants to help landlords with viewings at the end of their tenancy by offering a week’s worth of rent as a reward. “No one knows a property better than people who actually live in it, and it removes a lot of friction to have current tenants schedule and host viewings at times that suit them,” explains Dobrovolskiy. “This costs less than 2% of annual rent for landlords, compared to paying 10%+ to an estate agent for finding a new tenant. So we are unlocking financial benefits for landlords and tenants at the same time as giving them more flexibility.”

Mashroom has also developed a “Deposit Replacement Product” as an alternative to the traditional deposit. In partnership with insurer Arch Capital, it lets tenants pay one week’s rent while offering landlords more protection than a regular deposit — up to 12 weeks compared to the typical five weeks.

Noteworthy, the basic Mashroom service is free for tenants and landlords, with the proptech startup generating revenue via its financial products offering, which, along with deposit replacement, includes rent guarantee and other insurance products. The startup also operates its own in-house mortgage brokerage for buy-to-let mortgages and refinancing for landlords.

Powered by WPeMatico

Lucia, a six-year old, hides from Zoom calls and has rejected every edtech tool from Seesaw to Khan Academy. She will spend all of first grade in quarantine.

Her mother, Claire Díaz-Ortiz, says her daughter fits squarely into the “distance learning death zone.” The idea is that younger children are too young to do distance learning solo, even with tools meant to make it easier. Here’s one kindergartner’s remote fall class schedule:

Just got this schedule for my kindergartner’s “distance learning” in the fall and would just like to say LOL FOREVER TIMES A THOUSAND pic.twitter.com/CXXzdbwUWa

— Aubrey Hirsch (@aubreyhirsch) July 31, 2020

“And unfortunately for my daughter, I’m a VC, not a Zoom mom,” Díaz-Ortiz said.

The impact of the distance learning death zone, as Díaz-Ortiz calls it, is one of the reasons why many wealthy families with young children are considering a new solution: learning pods.

Learning pods are small clusters of children within the same age range who are paired with a private instructor. Depending on a parent’s preferences, learning pods could be an in-home or virtual experience and be either a full-time school replacement or supplemental learning.

In recent weeks, the concept has taken off all across the country, from suburbs to cities. There’s a Facebook group for Boulder, Colorado school districts; organizers launched Pandemic Pod San Diego to “connect families looking for in-home, teacher-led learning groups.” Some households are offering teachers a retainer. Among working mom groupchats, pods are taking off as a sanity lifesaver, especially as childcare responsibilities fall disproportionately on women.

Looking for the best 4-6th grade teacher in Bay Area who wants a 1-year contract, that will beat whatever they are getting paid, to teach 2-7 students in my back yard#microschool

If you know this teacher, refer them & we hire them, I will give you a $2k UberEats gift card

— jason@calacanis.com (@Jason) August 2, 2020

Startups are pivoting to keep up with the demand for private teachers. But because of high costs, only affluent families are able to form or join learning pods, which may limit the model’s ability to reach scale while extending the existing digital divide.

Powered by WPeMatico

Ginger, a provider of on-demand mental healthcare services, has raised $50 million in a new round of funding.

The new capital comes as interest and investment in mental health and wellness has emerged as the next big area of interest for investors in new technology and healthcare services companies.

Mental health startups saw record deal volumes in the second quarter of 2020 on the heels of rising demand caused by the COVID-19 epidemic, according to the data analysis firm CB Insights. More than 55 companies raised rounds of funding over the quarter, even though deal amounts declined 15%, to $491 million. That’s still nearly half a billion dollars invested into mental health in one quarter alone.

What started in 2011 as a research-based company spun out of work from the Massachusetts Institute of Technology has become one of the largest providers of mental health services primarily through employer-operated health insurance plans.

Through Ginger’s services, patients have access to a care coordinator that is the first point of entry into the company’s mental health plans. That person is a trained behavioral health coach — typically someone with a master’s degree in psychology with a behavioral health coaching certificate from schools like Duke, UCLA, Michigan or Columbia and 200 hours of training provided by Ginger itself.

These health coaches provide the majority of care that Ginger’s patients receive. For more serious conditions, Ginger will bring in specialists to coordinate care or provide access to medications to alleviate the condition, according to the company’s chief executive officer, Russell Glass.

Ginger began offering its on-demand care services in 2016 and counts tens of thousands of active users on the platform. The company charges companies a fee for access to its services on a per-employee, per-month basis and provides access to mental health services to hundreds of thousands of employees through corporate benefit plans, Glass said.

More than 200 companies, including Delta Air Lines, Sanofi, Chegg, Domino’s, SurveyMonkey and Sephora, pay Ginger to cost-efficiently provide employees with high-quality mental healthcare. Ginger members can access virtual therapy and psychiatry sessions as an in-network benefit through the company’s relationships with leading regional and national health plans, including Optum Behavioral Health, Anthem California and Aetna Resources for Living, according to a statement.

“Our entire mission here is to break the supply/demand imbalance and provide far more care,” said Glass in an interview. “Ultimately we want Ginger to be available to help anybody who has a need. Being accessible to anybody, anywhere, is an important part of the strategy. That means direct-to-consumer will be a direction we head in.”

For now, the company will use the money to build out its partner ecosystem with companies like Cigna, an investor in the company’s latest $50 million round. Ginger will also look to getting government payers to reach more people. Eventually direct-to-consumer could become a larger piece of the business as the company drives down costs of care.

It’s also investing in automation and natural language processing to automate care pathways and personalizing patient care using machine learning.

The company’s $50 million Series D round was co-led by Advance Venture Partners and Bessemer Venture Partners, with additional participation from Cigna Ventures and existing investors such as Jeff Weiner, executive chairman of LinkedIn, and Kaiser Permanente Ventures. To date, Ginger has raised roughly $120 million.

Even as Ginger is working through the existing network of employer benefit plans and standalone insurance providers to offer its mental health services, other startups are raising money to offer employer-provided mental health and wellness plans. SonderMind is working to make it easier for independent mental health professionals to bill insurers, AbleTo helps employers screen for undiagnosed mental health conditions and SilverLight Health partners with organizations to digitally monitor and manage mental health care.

Meanwhile, other startups are going direct-to-consumer with a flood of offerings around mental health. Well-financed, billion-dollar-valued companies like Ro and Hims are offering mental health and wellness packages to customers, while Headspace has both a consumer-facing and employer benefit offering. And upstart companies like Real are focusing on providing care specifically for women.

With its funding round, Ginger is adding David ibnAle, a founding partner at Advance Venture Partners (AVP), which is the investment firm behind S.I. Newhouse’s family-owned media and technology holding company, Advance; and the digital health investment guru Steve Kraus from Bessemer Venture Partners.

“AVP invests in companies that are using technology to tackle large-scale, global challenges and transform traditional businesses and business models,” said David ibnAle, founding partner of Advance Venture Partners. “Ginger is doing just that. We are excited to partner with an exceptional team to help make high-quality, on-demand mental health care a reality for millions of more people around the world.”

Powered by WPeMatico

Robinhood’s huge, two-part Series F round came partially in Q2 and partially in Q3. The app-based trading platform announced the first $280 million in early May, valuing the company at around $8.3 billion, up from a prior price tag of around $7.6 billion.

Then in July, Robinhood tacked on $320 million more at the same price, raising its valuation to around $8.6 billion.

While it has long been known that savings and investing apps and services are seeing a boom in 2020, precisely what caused investors to pour $600 million more into this already-wealthy company was less immediately evident. Recent data released by Robinhood concerning one of its revenue sources may help explain the rapid-fire capital events.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Filings from Robinhood covering the April through June period, Q2 2020, indicate that the company’s revenue from payment for order flow, a method by which a broker is paid to route customer orders through a particular group, or party rose during the period. As TechCrunch has covered, Robinhood generates a sizable portion of its revenue from such activities.

The company is hardly alone in doing so. As a new report from The Block, shared with The Exchange ahead of publication notes, Robinhood’s Q2 payment for order flow haul was impressive, but not singularly so; trading houses like E*Trade and Charles Schwab also grew their incomes from order flow routing in the period.

The company is hardly alone in doing so. As a new report from The Block, shared with The Exchange ahead of publication notes, Robinhood’s Q2 payment for order flow haul was impressive, but not singularly so; trading houses like E*Trade and Charles Schwab also grew their incomes from order flow routing in the period.

But Robinhood’s gains come in the wake of the firm’s promise to shake up its options trading setup after a customer took their own life. As we’ve written, there is a tension between Robinhood’s desire to limit who can access options trading, its need to grow and the incomes options-related order flow can drive for the budding fintech giant.

This morning, however, we are focusing on revenue growth over other issues (more to come on those later). Let’s dig into Robinhood’s Q2 order flow revenue numbers and see what we can learn about its run rate and current valuation.

According to The Block’s own calculations, Robinhood saw saw its total payment for order flow revenue roughly double, rising from $90.9 million in Q1 2020 to $183.3 million in Q2 2020, a 102% increase.

Powered by WPeMatico

Every major technology breakthrough of our era has gone through a similar cycle in pursuit of turning fiction to reality.

It starts in the stages of scientific discovery, a pursuit of principle against a theory, a recursive process of hypothesis-experiment. Success of the proof of principle stage graduates to becoming a tractable engineering problem, where the path to getting to a systemized, reproducible, predictable system is generally known and de-risked. Lastly, once successfully engineered to the performance requirements, focus shifts to repeatable manufacturing and scale, simplifying designs for production.

Since theorized by Richard Feynman and Yuri Manin, quantum computing has been thought to be in a perpetual state of scientific discovery. Occasionally reaching proof of principle on a particular architecture or approach, but never able to overcome the engineering challenges to move forward.

That’s until now. In the last 12 months, we have seen several meaningful breakthroughs from academia, venture-backed companies, and industry that looks to have broken through the remaining challenges along the scientific discovery curve. Moving quantum computing from science fiction that has always been “five to seven years away,” to a tractable engineering problem, ready to solve meaningful problems in the real world.

Companies such as Atom Computing* leveraging neutral atoms for wireless qubit control, Honeywell’s trapped ions approach, and Google’s superconducting metals, have demonstrated first-ever results, setting the stage for the first commercial generation of working quantum computers.

While early and noisy, these systems, even at just 40-80 error-corrected qubit range, may be able to deliver capabilities that surpass those of classical computers. Accelerating our ability to perform better in areas such as thermodynamic predictions, chemical reactions, resource optimizations and financial predictions.

As a number of key technology and ecosystem breakthroughs begin to converge, the next 12-18 months will be nothing short of a watershed moment for quantum computing.

Here are eight emerging trends and predictions that will accelerate quantum computing readiness for the commercial market in 2021 and beyond:

1. Dark horses of QC emerge: 2020 will be the year of dark horses in the QC race. These new entrants will demonstrate dominant architectures with 100-200 individually controlled and maintained qubits, at 99.9% fidelities, with millisecond to seconds coherence times that represent 2x -3x improved qubit power, fidelity and coherence times. These dark horses, many venture-backed, will finally prove that resources and capital are not sole catalysts for a technological breakthrough in quantum computing.

Powered by WPeMatico

You won’t find a better deal than this on Disrupt 2020 passes, but you won’t find it at all if you don’t take action within 48 short hours. The opportunity to save up to $300 dollars on your pass disappears when the early-bird deadline expires.

Wake up, smell the savings and buy your Disrupt pass before August 7 at 11:59 p.m. (PT).

This all-virtual Disrupt spans five days — September 14-18 — and it includes an unprecedented number of attendees and early-stage startups from around the world. Translation? More time and opportunity to learn, connect and collaborate with influential people who can help you move your business forward.

Let’s face facts. In our current global situation, building a successful startup requires every tool in the shed. Disrupt is a prime source for gathering new, effective tools. Still on the fence? Listen to what three of your peers have to say about their Disrupt experiences:

“Disrupt was a great place to look for potential partners beyond our blockchain world. We got to meet and collaborate with founders in complimentary technologies like IoT and AI. Building those relationships will help all of us provide customers with better solutions. It’s a win-win.” — Joel Neidig, founder of SIMBA Chain.

“I wanted to get the most out of my time at Disrupt. I learned a lot by splitting my time between the Startup Battlefield, the Main Stage speakers and the how-to presentations for founders on the Extra Crunch Stage.” — JC Bodson, founder and CEO of Arbitrage Technologies.

“I’ve attended many tech events and demo days. I like Disrupt’s approach. It combines demos with educational components — like speakers, panels and Q&As — that help you learn new trends and tactics. It’s more like a tech summit.” — Daniel Lloreda, general partner at H20 Capital Innovation.

Check out this preview of just some of the Disrupt speakers and sessions, take advantage of the new Pitch Deck Teardown and don’t forget about CrunchMatch. Our AI-driven networking platform opens weeks ahead of Disrupt so you have even more time to find and connect with the people who align with your business goals.

So many reasons to attend Disrupt 2020 and so little time left to score early-bird savings. Hop off the fence, buy your pass before August 7 at 11:59 p.m. (PT), save up to $300 and get ready to add a bunch of new tools to your startup arsenal.

Is your company interested in sponsoring or exhibiting at Disrupt 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

The Michigan startup scene is growing and venture capitalists see several key areas of opportunities. What follows is a survey of some of the top VCs in the state and how they see COVID-19 affecting the growth of Detroit, Ann Arbor and all of Michigan’s startup ecosystem. According to the Michigan Venture Capital Association (MVCA), there are 144 venture-backed startup companies in Michigan, which is an increase of 12% over the last five years.

The amount of capital available in the state hit a four-year high in 2019 after shrinking from record levels in 2015. The MVCA says the total amount of VC funds under management in Michigan is $4.3 billion. Out of that, 71% of the capital has been invested into companies and the MVCA states its members estimate an additional $1.2 billion of venture capital is needed to “adequately fund the growth of Michigan’s 144 startup companies in the next two years.”

As the VCs say below, life sciences is a large part of the Michigan ecosystem, attracting 38% of all investments made in the state. Information technology comes in second, receiving 34% of the total capital invested, with 85% going to those focused on software. Mobility, often thought as Michigan’s mainstay, only received 7% of the capital in 2019. Here’s who we spoke to:

Michigan has long been a hub for life science startups and the venture capitalists polled expect that to continue. Chris Stallman of Fontinalis Partners points to Michigan’s long-standing reputation in this field and expects this to continue.

Tim Streit of Grand Ventures agrees and sees the pandemic as accelerating the sector’s growth. In recent weeks he says his firm has seen a “number of promising digital therapeutics deals based in or near Michigan … and the timing couldn’t be more perfect for these kinds of companies to succeed.”

Chris Rizik of Renaissance Venture Capital notes that drug development will continue to drive growth around the country and is a strength of the Michigan ecosystem. He also points to Jeff Williams, CEO of NeuMoDx, as a leader in the life science community and who has led a number of Michigan’s most successful startups.

The notable exception to this are startups directly serving hospitals, according to Patricia Glaza of ID Ventures. She sees this as a challenging market in the era of COVID-19, saying “Hospitals are bleeding cash without elective surgeries and hard to prioritize nonessential technologies.”

Duo Security’s impressive exit to Cisco in 2018 is still resonating in the scene. As such, many venture capitalists are seeing Ann Arbor becoming a home for security startups.

Stallman of Fontinalis states, “I think the cybersecurity realm will be a bright spot as some of those spillover effects from the 2018 acquisition of Duo Security by Cisco take hold (this is still in its early days — employees will reach the end of their employment agreements and will start new companies, etc.).” Rizik of Renaissance Venture Capital said something similar: “The success of Duo Security highlighted Michigan’s growing reputation as a cybersecurity hub. The University of Michigan has always been strong in this area, and we now see a number of interesting startups in this field popping up around Ann Arbor.”

When asked about leaders in the Michigan startup scene, nearly all of the VCs listed Duo Security founders Dug Song and Jon Oberheide as key players. Perhaps Rizik said it best: “Dug Song is a great leader, who not only created a monster success for the region with Duo Security, but also has devoted much of his time to strategically working to help Michigan move forward as a responsible, startup-friendly community.”

Of course Michigan-based venture capitalists would be bullish on their own state, but nearly all of the VCs share the same reasons on why Michigan is a good place. They list low cost of living, amazing STEM-focused schools and a community of founders, VCs and business leaders eager to help each other.

Surprisingly, few of the VCs in the survey mention mobility or automotive as a highlight of the Michigan startup scene, which runs counter to the national narrative. Stallman sums up the situation this way: “The mobility space will see both headwinds and tailwinds. Companies vying for automotive customers may find that the industry’s challenges have resulted in a shorter ‘priority list’ for many automakers and suppliers; on the other side, companies helping to remove enterprise risk through innovation in supply chain, automation, workforce efficiency, etc. will have arguably more opportunity going forward.”

How much is local investing a focus for you now? If you are investing remotely in general now, are you filtering for local founders?

We have always been a thematically focused investor rather than a geographically focused investor; prior to COVID-19, we had invested 99% of our capital outside of Michigan. With that said, we’d love to invest more in Michigan and support more local founders.

What do you expect to happen to the startup climate in Detroit/Ann Arbor/Michigan longer term, with the shift to more remote work, possibly from more remote areas. Will it stay a tech hub?

Southeast Michigan has always been a story of two different startup worlds: health/life sciences and hardware/software tech. On the life sciences side, this region has a long-standing reputation of innovation and university research, and I expect that to remain largely the same going forward. It would seem to me that life sciences companies may not have as easy of a time adapting to new remote-work environments since much of the innovation work remains lab/clinic/facility-based.

For the world of other technology, I think there will certainly be more embracing of remote work and distributed teams — this area has always had some degree of that since it’s not uncommon to see companies with another office elsewhere or a few remote employees that come from very specific backgrounds that are hard to recruit for locally. Since this area has always had some of that, I could see a case that this new paradigm will be an easier adjustment for this region. However, the flip side of that is that so much of tech innovation and developing an ecosystem is about density and serendipitous collisions — for an area that was still on the come-up, losing what ground had been gained in recent years will no doubt make the spillover benefits of this aspect harder to come by. I worry a bit that angel and seed activity will slow locally (and hopefully that the growth in seed funds nationally will offset that).

Are there particular industry sectors that you expect to do uniquely well or poorly, locally?

I think a larger theme that is arising out of this COVID-19 situation is that people have a heightened sense of health, safety and security. Life sciences will remain resilient so long as there’s funding for continued research, and I think the cybersecurity realm will be a bright spot as some of those spillover effects from the 2018 acquisition of Duo Security by Cisco take hold (this is still in its early days — employees will reach the end of their employment agreements and will start new companies, etc.).

The mobility space will see both headwinds and tailwinds. Companies vying for automotive customers may find that the industry’s challenges have resulted in a shorter “priority list” for many automakers and suppliers; on the other side, companies helping to remove enterprise risk through innovation in supply chain, automation, workforce efficiency, etc. will have arguably more opportunity going forward.

In the short term, what challenges are facing Michigan’s startup scene?

Detroit has not yet hit a full critical mass from a startup ecosystem standpoint, and that is most evident in the more limited amount of angel and seed capital available to companies here; and, to a lesser extent, a more shallow pool of mentors and advisors for founders than what you would find in SF, LA, NYC, Boston, etc.

Who are some founders (who you’ve invested in or otherwise) that are leaders in the community?

Here are some of the prominent ones (note that we have invested in any): Dug Song and Jon Oberheide (Duo Security), Mina Sooch (has founded and led several prominent biotech companies), Amanda Lewan (Bamboo Detroit), Kyle Hoff (Floyd), Josh Luber and Greg Schwartz (StockX).

A lot of Bay Area founders and developers are looking to relocate. Why Michigan?

Quality research institutions, access to talent locally and ability to pull from Toronto/Ohio/etc., significant industry (automotive, logistics, manufacturing and financial services) in its footprint, supportive state programs for startups, cost of living, international airport with easy access (when the world moves again, that is), etc.

Powered by WPeMatico