Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Old-school approaches to marketing were often described as “spray and pray.” Marketers would launch a massive campaign in as many places as possible and hope that something worked.

More customers would show up, so it would appear that something had in fact worked.

But nobody could be sure exactly what that something was.

When we can’t predict what will have an impact, we need campaigns that cover all the bases, and those campaigns are consequently huge. They take a long time to create, are expensive to launch and come chock full of risk.

If a spray-and-pray campaign is a total failure (and we don’t have to go far to find examples of those), it’s quite possible an entire year’s worth of marketing budget has just been wasted.

Instead, marketers need to take a page from lean product development and begin creating Minimum Viable Campaigns (MVCs). Rather than wait until a massive multichannel launch is perfect, we can incrementally release a series of smaller, targeted, data-driven campaigns.

Over time these MVCs coalesce to look and act much like a Big Bang-style campaign from the spray-and-pray days, but they’ve done so in a much more data-driven and less risky way.

Just as with a Minimum Viable Product (MVP), it can be easy to misunderstand the real definition of an MVC. It’s not something thrown together with no regard for brand standards or strategic goals, and it’s not a blind guess.

Instead, a good MVC represents the smallest amount of well-designed work that could still achieve some of the campaign’s goals. Before we have any chance of figuring out what that looks like, we need to know the ultimate goal of the bigger campaign or initiative. If we don’t know this, we can’t possibly measure the effectiveness of the MVC.

Powered by WPeMatico

The expression “it takes a village” easily applies to building a successful mobility startup, especially in uncertain and tumultuous times. It also takes opportunities, and you’ll find plenty of those at TC Sessions: Mobility 2020 (October 6-7). Even better — you can bring your entire village, increase your opportunity potential and save money with our group discount. Win-win-ka-ching!

When you book four or more tickets to TC Sessions: Mobility, you’ll trim $25 off the price of each pass — but only if you buy them before the deadline: September 4 at 11:59 p.m. (PDT). Prices go up September 5.

The two-day conference focuses on every aspect of mobility and transportation — autonomy, micromobility, AI-based mobility applications, investment, regulatory issues, battery technology and more. Learn from the leading experts about the current state of the industry and what trends — and which players — will shape its future.

You and your village can divide and conquer — gather the latest intel, network to build essential connections and engage in the kinds of conversations that lead to lasting partnerships. What you learn can shift the way you think about your goals. Here’s what two team members from FlashParking had to say about their experience:

“We left TC Sessions: Mobility with a good vision of how the space will evolve over the next three to five years. It will help us position our company and understand how to think about strategy and partnerships going forward.” — Jeff Johnson, vice president of enterprise sales and solutions at FlashParking.

“TC Sessions: Mobility isn’t just an educational opportunity, it’s a real networking opportunity. Everyone was passionate and open to creating pilot programs or other partnerships. That was the most exciting part. And now — thanks to a conference connection — we’re talking with Goodyear’s Innovation Lab.” — Karin Maake, senior director of communications at FlashParking.

CrunchMatch — our free business matchmaking platform — makes networking in a virtual venue easier. Answer a few quick questions, and the AI-powered tool helps you find, connect and schedule 1:1 video calls with the kinds of people you need to grow your business. Looking for investors? Check. Need a developer? Can do. Want to add new startups to your portfolio? CrunchMatch covers all the bases.

We haven’t touched on the great speakers we have on tap or explored the TC Sessions: Mobility 2020 agenda. Peruse it at your leisure, but don’t dawdle. Buy your group discount passes by September 4 at 11:59 p.m. (PDT) and save. Opportunity calls, and it’ll take a village to take advantage of all of them.

Is your company interested in sponsoring or exhibiting at TC Sessions: Mobility 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Launching a company, even in the best of times, is one of the most challenging exercises a person can go through. In an economic recession, it can seem downright impossible. But founders across the country, and indeed across the globe, are in the midst of that process as I write.

They aren’t the first. Alexa von Tobel, founder of LearnVest and founding partner at Inspired Capital, publicly launched her fintech startup in 2009, and founded it in May of 2007. In that span of time, Lehman Brothers went under — in December of 2008.

The company was launched in the midst of the worst economic downturn in at least three generations (current circumstances notwithstanding). We briefly chatted with von Tobel about this in a recent episode of Extra Crunch Live, but the topic deserved much more exploration. Von Tobel was gracious enough to talk to us again, and gave us her advice and insights on what it means, and what it takes, to launch a business in the midst of economic uncertainty.

Von Tobel says that one of the most important exercises in forming LearnVest — a company that was acquired for $375 million by Northwestern Mutual — was writing out a business plan. It was 75 pages, and by no means a formal document. Rather, the LearnVest business plan was a brain dump of everything von Tobel could possibly think of as it relates to her idea.

“It was nothing beautiful and by no means a work of art,” said von Tobel. “But it was valuable to put it together and walk through this blueprint of all the big questions, all the concerns. How would the customer feel? How big was the market? What was the competition? I even drew up a product plan of how I would roll it out. It was a budget, looking at how much money we think we need to get up and running.”

This business plan also included the areas in which von Tobel felt she was not an expert. She wanted a clear expression of her own strengths and weaknesses built into the business from its very inception.

von Tobel had never written a formal business plan before. She had taken a few business classes at Harvard Business School, but didn’t see the exercise as preparation for publication, but rather her own personal space to develop a product and business.

“It was a macro, more thoughtful plan that allowed me to understand where things were positioned,” said von Tobel. “Perfect is the enemy of good enough. You don’t have to be perfect, but you have to do enough that you have a really clear sense of the picture and a really clear sense of the cracks.”

Powered by WPeMatico

In the aftermath of George Floyd’s death and widespread protests for racial justice, a number of venture capitalists made public statements about wanting to improve diversity in the tech industry — and more specifically to fund more diverse founders.

Their comments are certainly worth applauding, but actual change is a lot harder. And if it comes at all, it will take time. In the meantime, how can Black founders navigate a tech and venture capital industry where they have historically been underrepresented, overlooked and worse?

To answer that question, we’ll bring three Black founders together at Disrupt 2020 from September 14-18 who can speak directly about their experience raising funding and launching startups.

One of our speakers, Michael Seibel, is now funding startups himself as partner and CEO of startup accelerator Y Combinator. Before that, however, he was co-founder and CEO at Justin.tv (which became game streaming giant Twitch) and then at its spin-off, Socialcam (which was acquired by Autodesk). So he can talk about both sides, as both a founder and investor.

Joining Seibel will be two YC startup founders — Reham Fagiri of furniture marketplace AptDeco and Songe LaRon of barbershop software maker Squire. We’ll talk to all three of them on the Extra Crunch stage, getting as specific and tactical as possible about what Black founders can expect and what steps they can take to succeed.

Learn more at Disrupt 2020, which runs from September 14-18. Buy the Disrupt Digital Pro Pass, or if you’re an early-stage founder a Digital Startup Alley Exhibitor Package, today and get access to all the interviews on our Main Stage, workshops over on the Extra Crunch Stage, where you can get actionable tips, as well as CrunchMatch, our free, AI-powered networking platform. As soon as you register for Disrupt, you will have access to CrunchMatch and can start connecting with people. Use the tool to schedule one-on-one video calls with potential customers and investors or to recruit and interview prospective employees.

Powered by WPeMatico

Billion-dollar natural disasters are on the rise in the United States, according to CNBC. Even as I write, a hurricane is making landfall in Louisiana while wild fires rage in northern California. And those are just the big disasters.

There were more than 1.3 million fires in the United States in 2018, and nearly three out of every five deaths related to a house fire happened in a house where there was no smoke alarm or it didn’t function properly.

Harbor, a company that just closed on a $5 million seed round, wants to make users more prepared.

The product, which will launch in October, aims to gamify the process of doing everyday preparation for disasters. Using publicly available data from agencies like NOAA, FEMA and USGS, as well as land maps and building codes to pinpoint individual household risk, Harbor takes a look at the user’s location and the general state of their home to determine types of risks to that individual user and their property.

From there, the platform curates a weekly checklist for the user to stay prepared, whether it’s keeping track of the amount of water on hand (for those in the path of hurricane season) or checking the battery levels and functionality of a smoke alarm.

“For us, it’s not about buying a go bag,” said CEO Dan Kessler. “It’s about doing the things you need to be prepared. Your plan is a heck of a lot more important than your bag. Your bag is also important, but without the planning it’s completely pointless. The problem is a lot of people, especially right now with the wildfires happening are saying ‘I don’t have a go bag,’ and they buy one for $50 on Amazon. But they are not any more prepared at that moment as they were before they bought the bag.”

Not only does harbor want to help users prepare for disasters, including curated product recommendations around preparedness equipment, but also help guide them through the disaster itself and the aftermath, offering step by step instructions based on the specific situation.

Though harbor hasn’t launched the product publicly, the company is prepared with a two-fold business model which includes e-commerce and a freemium subscription plan for the app itself.

The sole investor in the $5 million round was 25madison, a New York-based venture studio that incubates and funds companies from inception. 25madison brought on Dan Kessler, a former Headspace executive, as CEO in January. Kessler brought on Eduardo Fonseca as chief technology officer, who previously served as CTO of GoodRx.

In total, harbor is made up of a team of 10 employees, and the company declined to share any stats around diversity and inclusion on the team, saying “Dan and the team are very proud that the makeup of women and underrepresented groups is above tech industry averages, including the advisory board.”

The advisory board includes a number of notable experts in the disaster space, including former administrator of FEMA Brock Long, current senior fellow for climate change policy at the Council on Foreign relations Alice Hill, and professor at Harvard’s Kennedy School of Government and CNN national security analyst (who served as Assistant Secretary at the DHS) Juliette Kayyem, among others.

Powered by WPeMatico

We’re big believers in second chances here at TechCrunch, and that’s great news for early-stage founders who didn’t apply to compete in the Startup Battlefield during Disrupt 2020 (September 14-18). Your second chance comes in the form of two Wild Card entries to the world’s most legendary startup competition.

Want a shot to go head-to-head with some of the best new startups from around the world? Go buy a Digital Startup Alley Package and exhibit your standout startup to thousands of Disrupt 2020 attendees. TechCrunch editors will designate two outstanding early-stage startups from Digital Startup Alley as Wild Card entries.

You’ll have just a few days to prepare before you join the other Startup Battlefield competitors and deliver a six-minute pitch and demo to a panel of judges — top-name VCs and technologists. You’ll also answer a Q&A after your pitch. If you make it through to round two, you’ll do it all again to a fresh set of experts.

The prize? Massive exposure to media and investors (whether you win or not), glory in the form of the Disrupt Cup and $100,000 in sweet, equity-free cash.

Pro tip: Exhibit in Digital Startup Alley and you’re eligible for a Wild Card slot — even if you applied to Startup Battlefield but didn’t make it into the final cohort. You came so close — don’t pass up your second chance!

Exhibiting in Digital Startup Alley by itself is a win-win proposition. Introduce your tech and talent to thousands of people around the world, expand your network, build partnerships, attract investors, build your customer base and increase your brand recognition.

“I met so many industry experts — manufacturers, marketers, engineers — I even met people interested in investing in my company. Fostering these relationships over the long term will help my company scale and help me grow as an innovator.” — Felicia Jackson, inventor and founder of CPRWrap.

Buy a Digital Startup Alley Package, hang your shingle in Startup Alley and get ready to connect with the influential people who can help you build your business. Believe in second chances — you just might earn a Wild Card entry to Startup Battlefield and take a page out of RecordGram’s playbook. They rode the Wild Card to total victory as Battlefield champs. Go for it!

Is your company interested in sponsoring or exhibiting at Disrupt 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Every API or platform that has been successful long term owes a large part of their success to a thriving developer community — including Slack. As the lead of our Developer Relations team and a senior marketing manager, we oversee the Slack Platform Community. The community has grown quickly, so we’re both often asked how to successfully build a similar group.

At Slack, our app ecosystem has expanded alongside the product. The Slack App Directory contains 2,200 apps and over 600,000 custom apps (apps people build just for their teams) are used every week. No technology company creates its ecosystem alone. The growth in ours is part of a wider trend, as the total number of APIs has increased by 30% over the last few years. We’re also currently experiencing a surge in app submissions as more workforces operate entirely at home, and companies need tools to support remote operations. In early April, we saw a 100% increase in app submissions week-over-week.

As more developers try a platform, community support is critical to everyone — the platform company, new developers and those who have been developing for years. If your platform doesn’t have a developer community yet, creating one takes a few purposeful steps. Here are some of the best practices we’ve learned over nearly three decades’ worth of combined work in developer communities.

You can’t build a community without participating in one first. If you already have people developing on your platform, and they’re open to receiving contact from you, reach out! Get to know the people behind the integrations you’re seeing built.

Powered by WPeMatico

When shelter-in-place was first announced in the United States, most companies in the travel space saw bookings drop. Some shuttered. Hipcamp, a San Francisco-based startup that provides private land for people who want to go glamping or camping, found itself in a similar spot (even though its entire sell is about getting you away from crowds).

“Bookings took a precipitous drop as people sheltered-in-place, and we actually encouraged people to cancel,” founder Alyssa Ravasio said in an interview. The startup conducted a round of layoffs back in April, citing “economic uncertainties.” One employee tells TechCrunch that 60% of the company was laid off in two weeks. Hipcamp did not comment directly on the number of layoffs, other than to say the percentage of laid off employees is significantly lower than the 60% report.

Months later, Hipcamp is in a far better spot. When stay-at-home orders lifted, bookings spiked with people eager to get outside, which the CDC says is a safer activity than being inside a place with less ventilation. Ravasio says that Hipcamp has even brought back some employees it originally laid off. The startup is currently hiring.

Off this new momentum, Hipcamp today announced that it has acquired Australia-based landsharing startup Youcamp, marking its first expansion into an international market. With the new business, Hipcamp will acquire Youcamp’s existing 50,000 listings, bringing its total to 420,000 listings.

Hipcamp declined to disclose the financials of the deal at this time.

Youcamp, founded by James Woodford, was born in New South Wales in 2013. Similar to Hipcamp, Youcamp worked to draw urban-based adults to the great outdoors. For its seven years as an independent company, Youcamp racked up listings by working directly with private landowners.

Ravasio says she made her first big international bet in Australia partly because of revenue predictability.

“Expanding to the Southern Hemisphere also helps us account for natural seasonality with outdoor recreation. Between the U.S. and Australia, it’s an endless summer,” the founder said.

The entire team at Youcamp will join Hipcamp, adding five to Hipcamp’s staff, bringing its employee base to a total of 35.

Along with the acquisition announcement, Hipcamp shared that it is officially launching in Canada. The startup already had a number of Canadian hosts, but it will now increase the total by partnering directly with private landowners.

The company declined to share profitability or growth statistics, instead pointing to aggregate usage numbers as some sort of cumulative revenue parallel. To date, Hipcamp has helped people spend 2.5 million nights outside across 6,000 hosts in the United States, Australia and Canada.

In July 2019, Hipcamp got a tranche of new capital from investors, including but not limited to Andreessen Horowitz, Benchmark, Slow Ventures, Marcy Ventures (co-founded by Shawn Carter, or Jay-Z) and Dreamers Fund (co-founded by Will Smith). The round valued the startup at $127 million.

Hipcamp, which has been dubbed by The New Yorker the “Airbnb of the outdoors,” is more optimistic than it was in March, as shown by this appetite for acquisition. The progress mirrors what we’re seeing out of the actual Airbnb, which has found bookings increasing year over year as people look to stay at properties for local holidays.

Powered by WPeMatico

Warby Parker, the optical e-commerce giant, has today announced the close of a $245 million funding round from D1 Capital Partners, Durable Capital Partners, T. Rowe Price and Baillie Gifford.

A source familiar with the company’s finances confirmed to TechCrunch that this brings Warby Parker’s valuation to $3 billion.

The fresh $245 million comes as a combination of a Series F round ($125 million led by Durable Capital Partners in Q2 of this year) and a Series G round ($120 million led by D1 Capital in Q3 of this year). Neither of the two rounds was previously announced.

In the midst of COVID-19, Warby has also pivoted a few facets of its business. For one, the company’s Buy A Pair, Give A Pair program, which has focused on vision services across the globe, pivoted to stopping the spread of COVID-19 in high-risk countries. The company also used their Optical Lab in New York as a distribution center to facilitate the donation of N95 masks to healthcare workers.

The company has also launched a telehealth service for New York customers, allowing them to extend an existing glasses or contacts prescription through a virtual visit with a Warby Parker OD, and expanded its Prescription Check app to new states.

Warby Parker was founded 10 years ago to sell prescription glasses online. At the time, e-commerce was still relatively nascent and the idea of direct-to-consumer glasses was novel, to say the least. By cutting out the cost of physical stores, and competing with an incumbent who had for years enjoyed the luxury of overpricing the product, Warby was able to sell prescription glasses for less than $100/frame.

Of course, it wasn’t as simple as throwing up a few pictures of frames on a website and watching the orders pour in. The company developed a process where customers could order five potential frames to be delivered to their home, try them on, and send them back once they made a selection.

Since, the company has expanded into new product lines, including sunglasses and children’s frames, as well as expanding its footprint with physical stores. In fact, the company has 125 stores across the U.S. and in parts of Canada.

Warby also developed the prescription check app in 2017 to allow users to extend their prescription through a telehealth check up.

In 2019, Warby launched a virtual try-on feature that uses AR to allow customers to see their selected frames on their own face.

The D2C giant, in its 10 years of existence, has balanced its technological innovation with its physical expansion, which could explain its newfound triple-unicorn status. These latest rounds bring Warby Parker’s total funding to $535.5 million.

Powered by WPeMatico

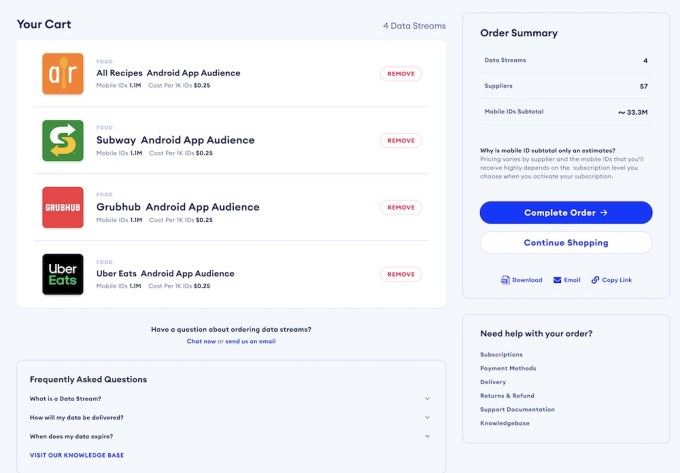

Narrative has raised $8.5 million in Series A funding and is launching a new product designed to further simplify the process of buying and selling data.

I’ve already written about the company’s existing marketplace and software for managing data transactions. With the new Data Streams Marketplace, the process should be simpler than ever — not much different than buying products on Amazon.

“Essentially, the idea was to take the best parts of the e-commerce and search models and apply that to a non-consumer offering to find, discover and ultimately buy data,” founder and CEO Nick Jordan (pictured above on the left) told me. “The premise is make it as easy to buy data as it is to buy stuff online.”

For example, Jordan showed me how a marketer could browse and search for different types of data in the marketplace. Once they find something they want to purchase (say, the mobile IDs of people who have the Uber Driver app installed on their phones, or the Zoom app) at a price they’re willing to pay (usually via subscription), they can just add the data set to their shopping cart, enter their credit card information, accept the terms of service and check out.

In Jordan’s view, this approach has become more attractive in recent months, because with all the uncertainty, companies need more data, and they need it quickly. For example, he suggested that a large company spending tens of millions of dollars on advertising “needs a way to find and buy the data almost programmatically and have the whole thing take five minutes instead of five months — those are the orders of magnitude we’re talking about here.”

Image Credits: Narrative

This data is generally sold by third-party sellers who are vetted by Narrative before they join the platform. Jordan also said the marketplace allows buyers to learn more about who they’re buying data from and even to establish a direct relationship — something that could be important for understanding things like regulatory compliance and data quality.

Although Narrative works to “deeply understand [sellers’] data collection methodologies,” Jordan warned, “There’s not necessarily a silver bullet for things being safe from a regulatory perspective.”

Similarly, he said that Narrative isn’t going to be grading the quality of the data sold on the platform. He argued, “Data quality is in the eye of the beholder. Someone’s signal is someone else’s noise.”

The goal with both of these issues is to provide transparency and allow buyers to do more research when necessary. Jordan also said Narrative is building out a marketplace of third-party applications — and that could include applications that score the quality of a data set.

“In the long run, I can imagine a number of use cases that’s almost infinite,” he said.

Narrative had previously raised $5.3 million in funding, according to Crunchbase. The Series A was led by G20 Ventures, with additional funding from existing investors Glasswing Ventures, MathCapital, Revel Partners, Tuhaye Venture Partners and XSeed Capital.

Jordan said the new round will allow the company to hire in areas like product, engineering, sales and marketing. He also noted that Narrative has long prioritized hiring team members from across North America, and recently it’s been placing a bigger focus on outreach and hiring from underrepresented groups.

“It’s easier said than done,” he acknowledged. “Any company that’s doing it well has to make it a priority and not just something they hope happens.”

Powered by WPeMatico