Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading.

Ready? Let’s talk money, startups and spicy IPO rumors.

With an ocean of neat stuff to get through below, we’ll be quick today on our thought bubble focused on Snowflake’s IPO. Up front it was a huge success as a fundraising event for the data-focused unicorn.

At issue is the mismatch between the company’s final IPO price of $120 and where it opened, which was around $245 per share. The usual forces were out on Twitter arguing that billions were left on the table, with commentary on the question of a mispriced IPO even reaching our friends at CNBC.

A good question given the controversy is how the company itself felt about its IPO price given that it was the party that, theoretically, left a few billion on some metaphorical table. As it turns out, the CEO does not give a shit.

Alex Konrad at Forbes — a good chap, follow him on Twitter here — caught up with Snowflake CEO Frank Slootman about the matter. He called the “chatter” that his company left money on the table “nonsense,” adding that he could have priced higher but that he “wanted to bring along the group of investors that [Snowflake] wanted, and [he] didn’t want to push them past the point where they really started to squeal.”

So Slootman found a new, higher price at which to value his company during its debut. He got the investors he wanted. He got Berkshire and Salesforce in on the deal. And the company roared out of the gate. What an awful, terrible, no-good, mess of an IPO.

Adding to the mix, I was chatting with a few SaaS VCs earlier this week, and they largely didn’t buy into the money-left-on-the-table argument, as presuming that a whole block of shares could be sold at the opening trade price is silly. Are IPOs perfect? Hell no. Are bankers out for their own good? Yes. But that doesn’t mean that Snowflake screwed up.

No time to waste at all, let’s get into it:

Again, there’s so much to get to that there is no space to waste words. Onward:

I am chatting with a Unity exec this evening, but too late to make it into this newsletter. Perhaps next week. Hugs until then, and stay safe.

Powered by WPeMatico

Editor’s note: Get this free weekly recap of TechCrunch news that any startup can use by email every Saturday morning (7 a.m. PT). Subscribe here.

While TechCrunch was busy producing our first-ever online Disrupt this week, the IPO market got even more exciting than expected — so here’s a quick look. Snowflake, Jfrog, Sumo Logic and Unity each raised price ranges days before IPO, to meet what had seemed like growing enthusiasm from public markets. Yet each still opened higher than its offering price, with cloud data-warehousing company Snowflake’s value doubling to make it the largest software IPO in history and Unity up 30%.

Despite the pandemic and various major turmoils around the world, the promise of these companies is helping to maintain optimism from retail investors to people thinking about founding a company.

Here’s a quick look at our coverage of the main companies in the IPO process this week, in chronological order:

Snowflake and JFrog raise IPO ranges as tech markets stay hot (EC)

As it heads for IPO, Palantir hires a chief accountant and gets approval from NYSE to trade

What’s ahead in IPO land for JFrog, Snowflake, Sumo Logic and Unity (EC)

JFrog and Snowflake’s aggressive IPO pricing point to strong demand for cloud shares (EC)

Unity raises IPO price range after JFrog, Snowflake target steep debut valuations

Go public now while software valuations make no sense, Part II

In its 4th revision to the SEC, Palantir tries to explain what the hell is going on

It’s game on as Unity begins trading

Unity Software has strong opening, gaining 31% after pricing above its raised range

And don’t miss Alex Wilhelm’s additional notes coming later today over on The Exchange weekend newsletter.

Image Credits: Canix

Our tenth annual startup conference was remote-first this year, but it managed to capture the same sort of vibe in my humble opinion.

First, a cannabis SaaS company took home the grand prize at the Startup Battlefield competition… we are truly living in the cloud these days. Here’s more, from Matt Burns:

Growing cannabis on an industrial scale involves managing margins while continually adhering to compliance laws. For many growers, large and small, this consists of constant data entry from seed to sale. Canix’s solution employs a robust enterprise resource planning platform with a steep tilt toward reducing the time it takes to input data. This platform integrates nicely with common bookkeeping software and Metrc, an industry-wide regulatory platform, through the use of RFID scanners and Bluetooth-enabled scales. Canix launched in June 2019, and in a little over a year (and during a pandemic), acquired over 300 customers spanning more than 1,000 growing facilities and tracking the movement of 2.5 million plants.

Next, here’s an especially pithy take on the future of startups, from senior Benchmark partner Peter Fenton.

I think this opportunity to build the tools for a world that’s ‘post place’ has just opened up and is as exciting as anything I’ve seen in my venture career. You walk around right now and you see these ghosts towns, with gyms, classes you might take [and so forth] and now maybe you go online and do Peloton, or that class you maybe do online. So I think a whole field of opportunities will move into this post-place delivery mechanism that are really exciting. [It] could be 10 to 20 years of innovation that just got pulled forward into today.

The truth is that I have not had time to watch all of the talks — I was busy with the Extra Crunch stage and other stuff, and that’s not even counting other programming we had going on. So check out the quick selection of picks below. To catch up more, you can browse the full agenda and watch the videos here.

We’ll also be offering coverage of the EC stage plus analysis from our conversations in the coming weeks, for subscribers (which includes anyone who bought a ticket and redeemed it for an annual subscription).

Quantum startup CEO suggests we are only five years away from a quantum desktop computer

Daphne Koller: ‘Digital biology is an incredible place to be right now’

Dropbox CEO Drew Houston says the pandemic forced the company to reevaluate what work means

Airtable’s Howie Liu has no interest in exiting, even as the company’s valuation soars

Indian decacorn Byju’s CEO talks about future acquisitions, coronavirus and international expansion

Fabletics’ Adam Goldenberg and Kevin Hart on what’s next for the activewear empire

Southeast Asia’s East Ventures on female VCs, foreign investment, consolidation

Ride-hailing was hit hard by COVID-19 — Grab’s Russell Cohen on how the company adapted

(Photo Illustration by Sheldon Cooper/SOPA Images/LightRocket via Getty Images)

Over in the real world, Tik Tok is still on track for a full shut-down despite the frantic dealmaking efforts by innumerable parties. At one point this week, it looked like Oracle and various business interests had a plan to keep Tik Tok alive as an independent company that would IPO (with some sort of national security oversight), and maybe that will still come about? I doubt Trump and his advisers will go along with that plan, given the national security problem of leaving algorithms controlled from China, and the long-term trade problem of US consumer tech being banned there too.

Meanwhile, the Bytedance-owned company also just announced 100 million users in Europe. Apparently it was a press push to counter the bad news, but as Ingrid Lunden notes, it’s hard to know what this user base means without the US. To which I’d add, European regulators are already busy going after foreign tech companies. I can’t imagine that they’ll leave an app this popular alone.

It’s another reminder that the next era will not offer startups the same possibilities for global success.

Lucas Matney talked with technical leaders and startup founders to figure out a key problem that many readers of this newsletter have had before (including me). How to get someone who can make your company a tech company? Here’s the intro, with the full thing on Extra Crunch:

Their advice spanned how to handle technical interviews, sourcing technical talent, how to decide whether your first engineering hire should become CTO — and how to best kick the can down the road if you’re not ready to start worrying about bringing on an engineer quite yet. Everyone I spoke to was quick to caution that their tips weren’t one-size-fits-all and that overcoming limited knowledge often comes down to tapping the right people to help you out and lend a greater understanding of your options.

I’ve broken down these tips into a digestible guide that’s focused on four areas:

- Sourcing technical candidates.

- How to conduct interviews.

- Making an offer.

- Taking a nontraditional route.

TechCrunch

Calling VCs in Zurich & Geneva: Be featured in The Great TechCrunch Survey of European VC

Opendoor to go public by way of Chamath Palihapitiya SPAC

Black Tech Pipeline proves the ‘pipeline problem’ isn’t real

Equity Monday: The TikTok mess, two funding rounds and Nvidia will buy ARM

Extra Crunch

3 VCs discuss the state of SaaS investing in 2020

The stages of traditional fundraising

Making sense of 3 edtech extension rounds

Facebook investor Jim Breyer picks Austin as Breyer Capital’s second home

Are high churn rates depressing earnings for app developers?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

This week Natasha Mascarenhas, Danny Crichton and myself hosted a live taping at Disrupt for a digital reception. It was good fun, though of course we’re looking forward to bringing the live show back to the conference next year, vaccine allowing.

Thankfully we had Chris Gates behind the scenes tweaking the dials, Alexandra Ames fitting us into the program and some folks to watch live.

What did we talk about? All of this (and some very, very bad jokes):

And then we tried to play a game that may or may not make it into the final cut. Either way, it was great to have Equity back at Disrupt. More to come. Hugs from us!

Equity drops every Monday at 7:00 a.m. PT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Whoever said you can’t make money playing video games clearly hasn’t taken a look at Unity Software’s stock price.

On its first official day of trading, the company rose more than 31%, opening at $75 per share before closing the day at $68.35. Unity’s share price gains came after last night’s pricing of the company’s stock at $52 per share, well above the range of $44 to $48 which was itself an upward revision of the company’s initial target.

Games like “Pokémon GO” and “Iron Man VR” rely on the company’s software, as do untold numbers of other mobile gaming applications that use the company’s toolkit for support. The company’s customers range from small gaming publishers to large gaming giants like Electronic Arts, Niantic, Ubisoft and Tencent.

Unity’s IPO comes on the heels of other well-received debuts, including Sumo Logic, Snowflake and JFrog .

TechCrunch caught up with Unity’s CFO, Kim Jabal, after-hours today to dig in a bit on the transaction.

According to Jabal, hosting her company’s roadshow over Zoom had some advantages, as her team didn’t have to focus on tackling a single geography per day, allowing Unity to “optimize” its time based on who the company wanted to meet, instead, of say, whomever was free in Boston or Chicago on a particular Tuesday morning.

Jabal’s comments aren’t the first that TechCrunch has heard regarding roadshows going well in a digital format instead of as an in-person presentation. If the old-school roadshow survives, we’ll be surprised, though private jet companies will miss the business.

Talking about the transaction itself, Jabal stressed the connection between her company’s employees, value and their access to that same value. Unity’s IPO was unique in that existing and former employees were able to trade 15% of their vested holdings in the company on day one, excluding “current executive officers and directors,” per SEC filings.

That act does not seemed to have dampened enthusiasm for the company’s shares, and could have helped boost early float, allowing for the two sides of the supply and demand curves to more quickly meet close to the company’s real value, instead of a scarcity-driven, more artificial figure.

Regarding Unity’s IPO pricing, Jabal discussed what she called a “very data-driven process.” The result of that process was an IPO price that came in above its raised range, and still rose during its first day’s trading, but less than 50%. That’s about as good an outcome as you can hope for in an IPO.

One final thing for the SaaS nerds out there. Unity’s “dollar-based net expansion rate” went from very good to outstanding in 2020, or in the words of the S-1/A:

Our dollar-based net expansion rate, which measures expansion in existing customers’ revenue over a trailing 12-month period, grew from 124% as of December 31, 2018 to 133% as of December 31, 2019, and from 129% as of June 30, 2019 to 142% as of June 30, 2020, demonstrating the power of this strategy.

We had to ask. And the answer, per Jabal, was a combination of the company’s platform strength and how customers tend to use more of Unity’s services over time, which she described as growing with their customers. And the second key element was 2020’s unique dynamics that gave Unity a “tailwind” thanks to “increased usage, particularly in gaming.”

Looking at our own gaming levels in 2020 compared to 2019, that checks out.

This post closes the book on this week’s IPO class. Tired yet? Don’t be. Palantir is up next, and then Asana .

Powered by WPeMatico

Most venture capital firms are based in hubs like Silicon Valley, New York City and Boston. These firms nurture those ecosystems and they’ve done well, but SaaS Ventures decided to go a different route: it went to cities like Chicago, Green Bay, Wisconsin and Lincoln, Nebraska.

The firm looks for enterprise-focused entrepreneurs who are trying to solve a different set of problems than you might find in these other centers of capital, issues that require digital solutions but might fall outside a typical computer science graduate’s experience.

Saas Ventures looks at four main investment areas: trucking and logistics, manufacturing, e-commerce enablement for industries that have not typically gone online and cybersecurity, the latter being the most mainstream of the areas SaaS Ventures covers.

The company’s first fund, which launched in 2017, was worth $20 million, but SaaS Ventures launched a second fund of equal amount earlier this month. It tends to stick to small-dollar-amount investments, while partnering with larger firms when it contributes funds to a deal.

We talked to Collin Gutman, founder and managing partner at SaaS Ventures, to learn about his investment philosophy, and why he decided to take the road less traveled for his investment thesis.

Gutman’s journey to find enterprise startups in out of the way places began in 2012 when he worked at an early enterprise startup accelerator called Acceleprise. “We were really the first ones who said enterprise tech companies are wired differently, and need a different set of early-stage resources,” Gutman told TechCrunch.

Through that experience, he decided to launch SaaS Ventures in 2017, with several key ideas underpinning the firm’s investment thesis: after his experience at Acceleprise, he decided to concentrate on the enterprise from a slightly different angle than most early-stage VC establishments.

Collin Gutman, founder and managing partner at SaaS Ventures (Image Credits: SaaS Ventures)

The second part of his thesis was to concentrate on secondary markets, which meant looking beyond the popular startup ecosystem centers and investing in areas that didn’t typically get much attention. To date, SaaS Ventures has made investments in 23 states and Toronto, seeking startups that others might have overlooked.

“We have really phenomenal coverage in terms of not just geography, but in terms of what’s happening with the underlying businesses, as well as their customers,” Gutman said. He believes that broad second-tier market data gives his firm an upper hand when selecting startups to invest in. More on that later.

Powered by WPeMatico

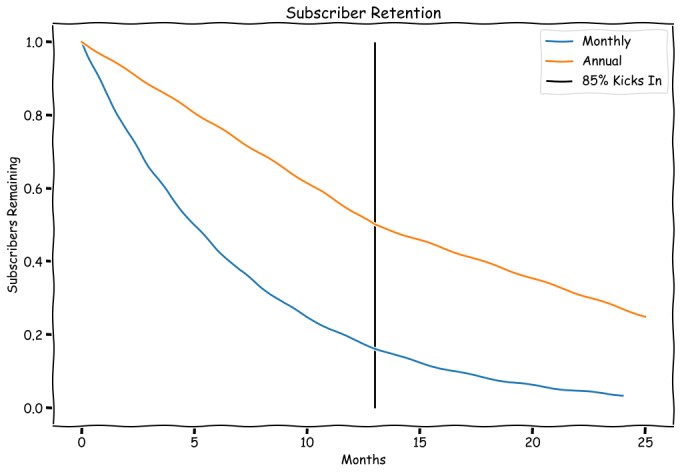

Ever since Apple opened up subscription monetization to more apps in 2016 — and enticed developers with an 85/15 split on revenue from customers that remain subscribed for more than a year — subscription monetization and retention has felt like the Holy Grail for app developers. So much so that Google quickly followed suit in what appeared to be an example of healthy competition for developers in the mobile OS duopoly.

But how does that split actually work out for most apps? Turns out, the 85/15 split — which Apple is keen to mention anytime developers complain about the App Store rev share — doesn’t have a meaningful impact for most developers. Because churn.

No matter how great an app is, subscribers are going to churn. Sometimes it’s because of a credit card expiring or some other billing issue. And sometimes it’s more of a pause, and the user comes back after a few months. But the majority of churn comes from subscribers who, for whatever reason, decide that the app just isn’t worth paying for anymore. If a subscriber churns before the one-year mark, the developer never sees that 85% split. And even if the user resubscribes, Apple and Google reset the clock if a subscription has lapsed for more than 60 days. Rather convenient… for Apple and Google.

Top mobile apps like Netflix and Spotify report churn rates in the low single digits, but they are the outliers. According to our data, the median churn rate for subscription apps is around 13% for monthly subscriptions and around 50% for annual. Monthly subscription churn is generally a bit higher in the first few months, then it tapers off. But an average churn of 13% leaves just 20% of subscribers crossing that magical 85/15 threshold.

In practice, what this means is that, for all the hype around the 85/15 split, very few developers are going to see a meaningful increase in revenue:

Image Credits: RevenueCat (opens in a new window)

Powered by WPeMatico

Earlier today at TechCrunch Disrupt, venture capitalist Peter Fenton joined us to talk about a variety of issues. Among them, we discussed how he’s putting his stamp on Benchmark now that, 15 years after joining the storied firm, he’s its most senior member.

Fenton said that he’s mostly focused on ensuring that the firm doesn’t change. It wants to remain small, with no more than six general partners at a time. It wants to keep investing funds that are half a billion dollars or less because its small team can only work closely with so many founders. He also made a point of noting that Benchmark’s partners still divide their investment profits equally, unlike at other, more hierarchical venture firms, where senior investors reap the biggest financial benefits.

We also talked about diversity because (hint hint) Benchmark — which is currently run by Fenton, Sarah Tavel, Eric Vishria and Chetan Puttagunta — is hiring one to two more general partners.

We talked about why Benchmark, a Series A investor in both Uber and WeWork, seemingly took so long to address cultural issues within both companies.

And we talked about the opportunities that has Benchmark, and Fenton specifically, most excited right now. Read on for more, or check out our full conversation below.

On whether Benchmark, which historically had all white male partners and now counts Fenton as its only white male partner, might hire a Black partner on his watch, given the dearth of Black investors in the industry (along with the changing demographics of the U.S.):

“That’s a personal issue for me, which is going to be measured in the outcomes, just like we have companies that take on initiatives that matter and then measure them and hold themselves accountable. I won’t feel good about our failure if we don’t continue to tilt towards diversity. It’s not enough that I’m the only white male partner. The industry is so systematically skewed in the wrong direction, and we’ve gotten so good at rationalizing how it ended up here, that I don’t think we can tolerate it anymore.”

Benchmark is looking to reinvent itself through “three interfaces,” he continued. “It’s who are we talking with and spending time with in terms of [who we might invest in] — that has to change; who are the people making investment decisions, [meaning] the partnership; and then what’s the composition of the companies we’ve invested in, meaning the executives and the boards.

“Before I’m done with the venture business, I want to be able to point to empirical outcomes . . .”

As for why Benchmark waited for the public to rally against its portfolio companies Uber and WeWork before taking action to address cultural issues (in Uber’s case, in reaction to former engineer Susan Fowler’s famous blog post and, in the case if WeWork, in reaction to its S-1 filing):

“I can’t give you a crisp answer because ultimately, what happens in the public eye isn’t the whole story of what was going on between Benchmark and those CEOs.” It’s “far more complicated, far more nuanced, far more engaged.”

Said Fenton: “What you start with in any partnership is this idea that we’re all flawed and providing what feels like unconditional support to a founder to nurture them and help them to understand in ways they might be able to from their direct reports where they are going to get in trouble, where they’re going to fall short, and then buttress them.

“I can say, having watched both [Benchmark investors] Bruce [Dunlevie] and Bill [Gurley] in those roles that they give their heart and soul to enable the full potential of those entrepreneurs, and in each case, it wasn’t enough.

“I don’t know what to say other than, I don’t envision another individual in that [board] role being able to do a better job because what they gave was everything, and those companies built enormous organizations, great success, delight and joy for customers, and they had, in each of their cases, pathologies in their culture. A number of companies that I’m involved with have pathologies in their culture. Every organization can build them. What motivated both Bill and Bruce was the constituencies that go beyond the CEO, the employees, the customers, and in the case of Uber, the drivers . . .

“You could say Susan Fowler was the reason it all happened; I can assure you that the work that was being done far preceded [the publication of her blog post]. Could we have done more, more quickly? You always look back and say, ‘Yeah.’ I think you learn as an organization. We’re not perfect.”

As for the trends that Fenton is watching most closely right now, he suggested a world of opportunities have opened up in the last six months, and he thinks they’ll only gain momentum from here:

“What I’m most excited about is, we’re not going back to normal. What’s so amazing is this shock to the system is really a big opportunity for entrepreneurs to come and say, ‘What do we need to build to recreate and unlock all these things we lost when we stopped going into workplaces?’

“So I think this opportunity to build the tools for a world that’s ‘post place’ has just opened up and is as exciting as anything I’ve seen in my venture career. You walk around right now and you see these ghosts towns, with gyms, classes you might take [and so forth] and now maybe you go online and do Peloton, or that class you maybe do online. So I think a whole field of opportunities will move into this post-place delivery mechanism that are really exciting. [It] could be 10 to 20 years of innovation that just got pulled forward into today.”

Powered by WPeMatico

TechCrunch hosted an unusual Startup Battlefield this week — the founders, judges, audience and moderator (me) were all in different locations, doing our best to interact over WebEx.

But the 20 startups still demonstrated their products and explained their visions, then were grilled by expert judges. And those judges helped the TechCrunch team select our five finalists.

Those finalists will be presenting tomorrow at 10:40 a.m. Pacific for a whole new set of judges, and you can watch the live stream by logging into TechCrunch. (Also: It’s not too late to sign up for the full Disrupt experience.) Those judges will choose a runner-up and a winner, and the winner will take home $100,000, equity-free.

Here are the finalists:

Canix has built a robust enterprise resource planning platform designed to reduce the time it takes cannabis growers to input data. It integrates nicely with common bookkeeping software, as well as Metrc, an industry-wide regulatory platform. You can read more about Canix here.

Hybrid rockets aren’t new, but they have always faced significant limitations in terms of their performance metrics and maximum thrust power. Firehawk Aerospace is building a stable, cost-effective hybrid rocket fuel engine that employs industrial-scale 3D printing to overcome the hurdles and limitations of previous designs. You can read more about Firehawk Aerospace here.

Tiffany Ricks founded HacWare in Dallas, Texas, in 2017 to help bring better email security awareness to small businesses. The technology sits on a company’s email server and uses machine learning to categorize and analyze each message for risk. You can read more about HacWare here.

Jefa is building a challenger bank specifically designed for women in Latin America. It focuses on solving the problems that women face when opening a bank account and managing it. You can read more about Jefa here.

Matidor is building a project platform for consultants and engineers to keep track of projects and geospatial data in a single dashboard. It offers an all-in-one data visualization suite for customers in the energy and environmental services fields. You can read more about Matidor here.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

This week Natasha Mascarenhas, Danny Crichton and myself hosted a live taping at Disrupt for a digital reception. It was good fun, though of course we’re looking forward to bringing the live show back to the conference next year, vaccine allowing.

Thankfully we had Chris Gates behind the scenes tweaking the dials, Alexandra Ames fitting us into the program and some folks to watch live.

What did we talk about? All of this (and some very, very bad jokes):

And then we tried to play a game that may or may not make it into the final cut. Either way, it was great to have Equity back at Disrupt. More to come. Hugs from us!

Equity drops every Monday at 7:00 a.m. PT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Impact Creative Systems (formerly Imagine Impact) is bringing a startup accelerator-style approach to finding fresh creative talent, and it announced this morning that, with funding from venture capital firm Benchmark, it’s spinning out from Imagine Entertainment — the production company founded by director Ron Howard and producer Brian Grazer.

Right after the news broke, the accelerator’s founders — Howard, Grazer and CEO Tyler Mitchell — joined us at TechCrunch’s Disrupt conference to discuss their vision. Grazer (whose films with Howard include “Apollo 13,” “A Beautiful Mind” and the upcoming “Hillbilly Elegy” for Netflix) recalled the Hollywood of 25 years ago, which he described as an “opaque” system where original writers often struggled to break in, and he felt that Impact could “democratize access to Hollywood.”

“How can we create opportunity to have access to the epicenter of employment in the media business, which is Hollywood?” he said.

For starters, Mitchell described what he claimed is a scalable system for evaluating 2,000 script submissions every week.

“We were able to build a system that leverages both technology as well as expert systems evaluating not just the writers, but the readers — almost like financial analysts — and try to come up with metrics in a world where there aren’t stats,” he said.

Mitchell also noted that in Impact’s first cohort of 87 writers, 39% were BIPOC, 10% were LGBTQ and it was split 50-50 between men and women, with 11 different countries represented.

“If you try to find the most talented writers in the world, they’re going to look like the world,” he said.

Howard made a similar point, saying that this diversity results from an interest in “fresh new voices” with “no statistical goals or agendas in mind — it’s just happening in a really honest way.” (At the same time, interviewer Ingrid Lunden couldn’t help but observe that this was a panel of three white men discussing diversity.)

Asked whether they’re interested in finding new talent from social media, Howard pointed to Grazer as the one who’s always encouraging him to “know what’s going on up north” (a.k.a. in Silicon Valley).

“Right now we’re in a creative renaissance with podcasts and Instagrams … finding their way into the center of the narrative,” Howard said.

Grazer said he often looks at YouTube, in particular. At the same time, he cautioned that creating content for these online platforms requires a different skill set than writing movies or TV.

“It doesn’t reduce the likelihood of their success necessarily, but it’s a different art form,” he said. “Because writing a teleplay or a screenplay, even the greatest playwrights can’t do that particular thing — you have to be trained.”

Still, Imagine found at least one idea in an Instagram Story, developing a comedic show around an actor (Grazer didn’t want to say who it is, but it’s probably Arnold Schwarzenegger) with a donkey named Lulu and a miniature horse named Whiskey. Apparently the show has attracted multiple bidders, and as for where it will end up, Grazer said, “It sort of seems like Amazon. I’ll let you know tomorrow.”

Powered by WPeMatico

Like plenty of other modern direct-to-consumer companies, influencer marketing has been an essential part of Fabletics’ journey. Actress Kate Hudson co-founded the company and co-CEO Adam Goldenberg believes that its network of spokespeople has been key to the company’s growth.

We were joined on our virtual TechCrunch Disrupt 2020 stage by Goldenberg and comedian Kevin Hart, who has been working as a brand partner for Fabletics.

“You can have the best product, which we believe we have, but if you can’t get it out there then you’re not going to be the leader that you want to be,” Goldenberg told us. “By having a very broad and diverse ambassador and influencer network, it allows us to become a very inclusive brand.”

Hart joined the company as an official brand partner earlier this year just as the pandemic took hold stateside and the company launched a menswear line. For Hart, the partnership is one of many relationships with brands and startups, but fits into his own lifestyle and thus made a lot of sense for him to work with, he says.

“[A company I invest in] has to coincide with myself and my lifestyle. If I’m going to talk about it, I have to be true to it,” Hart told TechCrunch. “There’s a plethora of things that I’m involved with that people would be shocked to know I was a part of, but it’s because I have the eyesight for it and a love for it.”

The Fabletics menswear line that Hart has advertised, and served as a brand spokesman for, has seen major growth amid a broader spike in athleisure wear sales. Goldenberg is bullish on just how much growth Fabletics will see from its men’s line so early in its life cycle.

“It’s a big goal, but I think we could do $75-100 million in sales next year with Fabletics Men, which is our first full year with this line, which would be very, very fast growth,” Goldenberg says.

As the company firms up its offering in activewear, they’re also keeping an eye on what trends will help them grow. Fabletics has already been building out technology trying to connect online and offline user habits in its stores. On the heels of Lululemon’s major acquisition of Mirror, which it announced in late June, moderator Jordan Crook inquired whether Fabletics had its own interests in expanding its footprint beyond activewear.

“We really believe in the importance of living an active lifestyle, so we’re not ready to share it yet, but we’re going to be doing something very large incorporating fitness into Fabletics,” Goldenberg said.

Check out the interview with Hart and Goldenberg below.

Powered by WPeMatico