Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

We recently invested in a team of co-founders who had voluntarily made their own vesting longer than four years. Four-year vesting is the industry standard. Why would someone voluntarily make it longer for themselves?

Their answer: “These days, with companies taking seven to 10 years to reach exit, it would make sense for founders to be on a similar schedule.”

This matters because the four-year co-founder vesting schedule frequently harms startup founders’ interests. Sometimes it damages their startup irreparably.

A growing number of founders are starting to realize this. I talked to quite a few about this over the last two years. Mostly, the “longer-than-four-years-

Importantly, this group of founders assumes they are going to be the ones actually building the company. They created the company. They are the company. Nobody is forcing them out. I suspect founders who already believe this about their own startup will find this post most helpful.

Given the massive implications of co-founder vesting schedules, all startup founders should consider co-founder vesting lengths more carefully and then choose what makes sense for them. You make this decision around the time of incorporation but feel the effects over the lifetime of your company.

As far back as the 1980s, the standard startup vesting schedule was four or five years, with five being more prevalent on the East Coast. Nobody seems to remember a time it was anything different. The closest I’ve gotten to a logical answer on why it’s four years today stretches back to a pre-401(k) era, from before Reagan’s tax reforms in the ’80s. Prior to then, tax rules incentivized big company pension plans to have vesting periods of at least five years.

Startups didn’t offer traditional pension plans. Instead, startups offered employees stock, vesting over four years instead of five as a competitive move. That is all moot today. It has no relevance for startup founders in 2020.

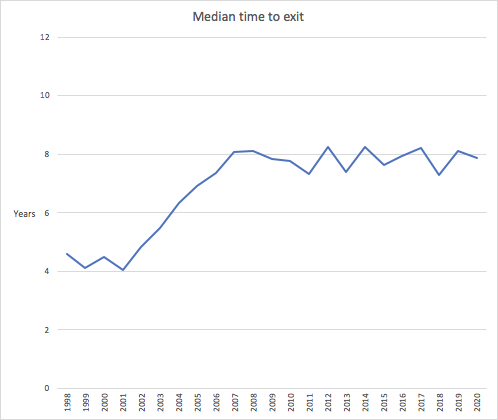

More relevantly, time from founding to exit has gone from four years in 1999 to eight years in 2020. Yet founder vesting remains stuck at four. This is dangerous.

Exit data from U.S. startups with minimum $1 million in venture funding. Image Credits: PitchBook

Powered by WPeMatico

These days when you found a startup, you don’t go out and buy a rack of servers. And you don’t build an in-house data center team. Instead, you farm out your infrastructure needs to the major cloud platforms, namely Amazon AWS, Microsoft Azure and Google Cloud.

That’s all well and good, but over time, any startup’s cloud setup will become more complex, varied and perhaps multi-provider. Throw in microservices and one can wind up with a big muddle, and an even bigger bill. That’s the problem that Yotascale wants to attack.

And there’s money backing the startup’s progress, including $13 million in new capital. The round, a Series B, was led by Aydin Senkut at Felicis, with participation from other capital pools, including Engineering Capital, Pelion Ventures and Crosslink Capital. Yotascale has now raised $25 million in total.

The funding event caught my eye, as I’ve heard startup CEOs discuss their public cloud spends in somewhat bitter terms; it’s hard for most startups to change infrastructure direction after they get off the ground, which means that as they grow, so too does their outflow of dollars to the major tech companies — the same megacaps that might turn around and compete with the very same startups that are pumping up their revenues and margins.

So spending less on AWS or Azure would be nice for startups. Yotascale wants to be the helper for lots of companies to better understand and attribute that spend to the correct part of their platform or service, perhaps lowering aggregate spend at the same time.

Let’s talk about how Yotascale got to where it is today.

The startup’s CEO, Asim Razzaq, talked TechCrunch through his company’s history, which didn’t get started until after he had wrapped up tenure at both another startup and PayPal.

When he set out to found Yotascale, Razzaq didn’t fire up a deck, raise capital and then get right to building. Instead, he first went out to do customer discovery work. That effort led him to the perspective that current solutions aimed at understanding cloud spend were insufficient and led to data being used against infrastructure teams in arguments for lower spend when it wasn’t a good idea (cutting backup expenses, for example).

During that time he also determined who Yotascale’s target customer is, namely the head of platform engineering at a company.

The startup self-funded for a while, with Razzaq telling TechCrunch that he wanted to be completely sure that he had conviction concerning the project before moving ahead.

After starting to work on Yotascale in mid 2015, the company raised some capital in 2016. It set out to solve the spend attribution problem that companies with public cloud contracts deal with — including having to contend with modern architecture and its related issues — while earning the trust of engineers, according to Razzaq.

From its period of customer discovery to working on product market fit after raising funds from Engineering Capital, Yotascale raised a Series A in mid-2018. Why? Because, Razzaq, told TechCrunch, as ones gains conviction, one must scale their team. And thus more capital was required.

During our chat with the CEO, it was notable how sequential his company-building process has proven. From talking to potential customers, to working to understand who his buyer is, to waiting on scaling the startup’s go-to-market efforts until he was confident in product-market fit, Yotascale seems to follow the inverse of the “raise lots and spend fast and try to win right away” model that became quite popular during the unicorn era.

How did Yotascale know when it found product market fit? According to its CEO, when companies started pulling the startup into their operations, and not the other way around.

Yotascale reported 4x year-over-year annual recurring revenue (ARR) growth at some point this year, though Razzaq was diffident about sharing specifics concerning the metric.

Sticking to the theme of reasonableness and caution, when asked about why his Series B is modest in size, Razzaq said that he was not interested in raising big rounds, and that $13 million is an amount of money that can move his company forward. What’s coming from the company? Yotascale wants to add support for Azure and Google Cloud in addition to its AWS work of today, to pick an example.

(You can find other hints that Yotascale is perhaps more mature than its peers at its current age. For example, in 2018 the company hired a new chief revenue officer, even putting out a release on the matter.)

That’s enough on this particular round. What will prove interesting is how far Yotascale can push its ARR up by the end of Q3 2021. And if it raises again before then.

Powered by WPeMatico

The gaming company Roblox announced today that it had confidentially filed paperwork with the SEC to make its public debut.

In February, the company, which operates a free-to-play gaming empire with tens of million of users, was valued at $4 billion after a Series G funding round led by Andreessen Horowitz . The company has raised more than $335 million in venture capital funding, according to Crunchbase.

The company has not detailed the number of shares it plans to offer and furthermore notes in standard legalese that their timely debut is “subject to market and other conditions.” After a slow 2019 for tech IPOs the rebound of public markets in mid-pandemic 2020 has provided an awfully wide window for tech startups reaching for their debuts.

In the games space, we recently saw the debut of Unity Technologies, which makes a popular game engine that developers use to build and monetize gaming titles.

Roblox offers an interesting sell to both consumers and developers, shipping a free-to-play vision of the future which pushes developers away from graphics-intense game design toward building content that can be played on a wide variety of devices. The games company has been more successful than most in translating a first-party experience’s success into a robust developer network. Roblox’s platform has been particularly successful with young audiences.

Powered by WPeMatico

The U.K.’s Seraphim Capital, the country’s only space tech accelerator, has released details of its newest cohort as part of its Space Camp programme, timed with the end of World Space Week last week.

4pi Lab

Raised so far: Undisclosed amount / Non-Equity Assistance from Creative Destruction Lab

Description: “4pi Lab is developing a Low-Earth Orbit (LEO) satellite constellation providing real-time, wildfire detection, monitoring and reporting. Their unique sensor gives them the ability to detect wildfires at a 10m resolution globally helping to eradicate major catastrophic wildfire events.”

Clutch Space Systems

Raised so far: £300,000 from FSE Group Enterprise M3 Expansion Loan

Description: “Clutch Space Systems provides software-defined radio (SDR) ground stations for satellite communications. SDR ground station technology improves downlink communications, provides significant cost savings and is far more dynamic, acting as an enabler for the exponentially growing Satcoms market.”

Helix Technologies

Raised so far: N/A

Description: “Helix Technologies – enables precision GPS antennas, providing 10cm level accuracy. Through breakthroughs in manufacturing and RF technology, Helix has developed a new GNSS antenna with a ceramic core capable of precision dynamic position accuracy whilst being space efficient for demanding tel and navigation applications. The design also enables the antenna to be highly immune to reflection off infrastructure and jamming.”

Kinnami

Raised so far: Undisclosed amount / seed from ICE71 Accelerate, 25 June 2020

Description: “Kinnami uniquely secures and optimises data sharing, ongoing data migration and management across distributed systems. Kinnami has created a unique storage and security system, ‘AmiShare’, which fragments and encrypts data. By storing these encrypted fragments across a distributed network of devices, it can secure data collected on the edge and have application within Satcoms, Defence and Enterprise.”

Starfish Space

Raised so far: Undisclosed amount / seed, 1 December 2019

Description: “Starfish Space aims to create an on-demand, in-space transportation and maintenance service for orbiting satellites. Their proximity Operations software uses a combination of breakthrough orbital mechanics, Machine Vision AI, and a low-thrust electric propulsion system to enable them to use smaller and cheaper space tugs that can operate across orbits. This addresses Counter-space and Mission opportunities.”

Sust Global

Raised so far: N/A

Description: “Sust Global provides real-time geospatial monitoring at an asset-level for analyzing Climate Risk. Their platform uses data from multiple satellites and ground sources to create full-stack ‘Asset-Level Geospatial Analytics’. Sust combines this data with the latest Climate Models and Standardised Risk Assessments to analyze risk and gain quantitative actionable insights for the Financial Services sector.”

Vector Photonics

Raised so far: 2018 secured undisclosed funding from ICURe; 2019 £70,000 of funding from Engineering and Physical Sciences Research Council and £30,000 from a Glasgow company to support that award

Description: “Vector Photonics’ disruptive and revolutionary photonic crystal lasers push the boundaries of what is possible with conventional semiconductor lasers providing comparable costs and flexibility with edge-emitting laser performance. Its unique beam steering capability is industry-changing in Datacoms and aligned markets like LIDAR.”

Powered by WPeMatico

As the American election looms and the IPO cycle slows some, it’s a good time to review how well the public offerings we have seen thus far have performed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Welcome to a Monday morning data rundown discussing how well the latest-stage startups that went public this year have performed after their first day. We’ll be awarding letter grades for post-IPO performance as well, because we can.

So, how did Snowflake do compared to Vroom, both stacked next to JFrog and One Medical? Let’s find out.

So, how did Snowflake do compared to Vroom, both stacked next to JFrog and One Medical? Let’s find out.

The fine folks at my former publication Crunchbase News have a running list of 2020 IPOs, which will help us not miss any names. Of course, we’re not going to include every possible deal; there have been some marginal debuts that we can leave behind.

But, the majors matter. So let’s get into them now:

Powered by WPeMatico

The U.S. economy may be in a precarious state right now, with a presidential election looming on the horizon and the country still in the grips of the coronavirus pandemic. But partly thanks to lower interest rates, the housing market continues to rise, and today a startup that has built technology to help it run more efficiently is announcing a major growth round of funding.

Snapdocs, which is used by some 130,000 real estate professionals to digitally manage the mortgage process and other paperwork and stages related to buying a home, has raised $60 million in new equity funding on the heels of a few bullish months of business.

In August 2020 — a peak in home sales in the U.S., reaching their highest level in 14 years — the startup saw 170,000 home sales, totaling some $50 million in transactions, closed on its platform. This accounted for almost 15% of all deals done that month in the U.S. Snapdocs is now on track to close 1.5 million deals this year, double its 2019 volume.

On top of this, the startup’s platform is being used by more than 70% of settlement agents nationally, with customers including Bell Bank, LeaderOne Financial Corporation, Googain and Georgia United Credit Union among its customers.

The Series C is being led by YC Continuity (Snapdocs was part of Y Combinator’s Winter 2014 cohort), with existing investors Sequoia Capital, F-Prime Capital and Founders Fund, and new backers Lachy Groom (formerly of Stripe and now a prolific investor) and DocuSign, a strategic backer, also participating.

“Like us they are on a mission to defragment an ecosystem,” King said, referring to it as a “perfect complement” to Snapdocs’ own efforts.

Snapdocs is not talking about its valuation. Aaron King, the founder and CEO, said in an interview that he believes disclosing it is nothing more than “grandstanding” — which is interesting considering that the industry he focuses on, real estate, is all about public disclosures of valuation — but he noted that most of the $103 million that the startup has raised to date is still in the bank, which says something about the company’s overall financial health.

And for some further context, according to PitchBook data estimates, Snapdocs was valued at $200 million in its last round, in October 2019.

Snapdocs’ central premise is that buying a house requires not just a lot of paperwork but also a lot of different parties to be on the same page, so to speak, to set the wheels in motion and get a deal done. There is not just the mortgage (with its multiple parties) to settle; you also have real estate brokers and agents, the home sellers, inspectors and appraisers, the insurance company, the title company and more — some 15 parties in all.

The complexity of all of them working together in a quick and efficient way often means the process of buying and selling a house can be long and costly. And that’s before the pandemic — with the problems associated with social distancing and remote working — hit us.

Snapdocs’ solution has been to build one platform in the cloud that helps to manage the documents needed by all of these different parties, providing access to data and the ability to flag or approve things remotely, to speed the process along. It also has built a number of features, using AI technology and analytics, to also help identify what might be potential issues early on and get them fixed.

King is not your typical tech startup entrepreneur. He began working in mortgages as a notary when he was still in high school — he’s effectively been in the industry for 23 years, he said — and his earliest startup efforts were focused on one aspect of the complexities that he knew first-hand: he saw an opportunity to lean on technology to get notarized signatures sorted out in a legal, orderly and quicker way.

He then got deeper into identifying the possibilities of how tech could be used to improve the larger process, and that is how Snapdocs came into existence.

Given how big the real estate market is — it’s the largest asset class in the world, by many estimates — and how many other industries tech has “disrupted” over the years, it’s interesting that there have been so few attempting to solve it. One of the reasons, it seems, is that there hasn’t been enough of a crossover between tech experts and mortgage experts, and Snapdocs is a testament to the virtues of building a startup specifically around a hard problem that you happen to know really well.

“Most people have identified this as a tech problem, and a lot of the tech — such as e-signatures — has existed for 20 years, but the fragmentation of real estate is the issue,” he said. “We’re talking about a mass constellation of companies and workflow. But we’re obsessed about the workflow of all of these constituents.”

That’s a position that has helped Snapdocs build its standing with the industry, as well as with investors.

“I’ve known the Snapdocs team for many years and have always been amazed by their focus and execution toward bringing each stakeholder in the mortgage process online,” said Anu Hariharan, partner at YC Continuity, in a statement. “In 2013, Snapdocs began as a notary marketplace before expanding horizontally to service title companies and, more recently, lenders. By connecting the numerous parties involved in a mortgage on a single platform, Snapdocs is quickly becoming the “operating system” for mortgage closings. Mortgages, much like commerce, will shift online, bringing improved efficiency and a far better customer experience to the outdated home-closing process.” Hariharan has real estate experience herself and is joining the board with this round.

There have been a number of companies taking new, tech-based approaches to the market to find new and faster ways of doing things, and to open up new kinds of value in the market.

Opendoor, for example, has rethought the whole process of selling and buying houses, taking on a role as a middleman in the process both to take on a lot of the harder work of fixing up a home, and handling all of the difficult stages in the sales process: it’s a role that has recently seen the company catapult to a valuation of $4.8 billion by way of a SPAC-based public listing. An interesting idea, King said, but still only accounting for a small sliver of house sales.

Others, like Orchard, Reonomy and Zumper, have all also raised large rounds on the back of a lot of promise of the market continuing to grow and the opportunity to take part in that process through new approaches. It’s a sign that “safe as houses” still has a place in the market, even with all the other unknowns in play.

“Over the next five years the real estate industry will be completely digitized, so a lot of companies are trying to figure out what their place are, and how to provide value,” King said.

Powered by WPeMatico

The retail landscape is shifting rapidly. While D2C brands have changed the way we shop, Quince is looking to change retail even more dramatically.

The brand, which raised $8.5 million in seed funding last year (and only revealed as much today), is looking to rethink the supply chain with its own line of 700 items, including men’s and women’s apparel, accessories, jewelry and home goods.

After beta testing for a year as “Last Brand,” Quince is launching with a new model called “M2C,” or manufacturer to consumer.

The idea is that Quince goes directly to factories with designs for essentials — not overly patterned or branded items — with an order that can dynamically adjust each week based on demand. As orders start coming in, Quince can work alongside manufacturers to ensure they aren’t over or under producing on a specific SKU. The factory then ships directly to the customer, rather than shipping to a distribution center or store and then again to the final destination.

You might think that factories wouldn’t be as amenable to this model, as they have little to lose when a brand overestimates demand for a SKU and doesn’t sell it through to the customer. But co-founder and CEO Sid Gupta says that this new model is being presented at a pivotal time in retail. Bigger brands, the ones that place orders for 100,000 units, are struggling during the pandemic and shrinking their SKU portfolio.

This leaves the factories with two options: turning to D2C brands or selling through a marketplace like Amazon.

“D2C demand is really fragmented, and most D2C companies are really sub-scale,” said Gupta. “It’s hard to get the efficiency gains out of it. The issue with selling on a marketplace, like Amazon, is you’ve got to compete with hundreds, if not thousands, of other sellers for the same exact good. If you’re a factory that actually makes high-quality goods, and you pay your workers fairly, and you don’t damage the environment, your cost might be 3% or 5%, higher.”

He added that it’s difficult for a factory to have those factors shine through to the customer on Amazon, and more difficult still to learn how to play the advertising game.

This environment has made manufacturers slightly more open to a new way of doing things.

By working directly with factories, Quince says it’s able to bring the cost of luxury items down significantly, selling a cashmere sweater for approximately $50 instead of $150+, as you’ll often find with other brands. Quince works with more than 30 factories across the world.

Gupta says the company has also thought very deeply about sustainability, setting standards around the materials used (are they organic or recycled?), the manufacturing process (is it ecologically sound?), worker pay and more. The company is also looking into giveback programs to share in the profits with the factories and the workers.

The funding from last fall has allowed Quince to beta test last year and grow the team to 16, including co-founders Becky Mortimer and Sourabh Mahajan. Thirty-five percent of employees are female, and 65% are minorities.

The company’s investors include Founders Fund, 8VC and Basis Set Ventures.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest big news, chats about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and don’t forget to check out last Friday’s episode.

So, what was on our minds this morning?

We hope that you are well and warm and full of good spirits. Back soon!

Equity drops every Monday at 7:00 a.m. PT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Sources have told TechCrunch that Twilio intends to acquire customer data startup Segment for between $3 and $4 billion. Forbes broke the story on Friday night, reporting a price tag of $3.2 billion.

We have heard from a couple of industry sources that the deal is in the works and could be announced as early as Monday.

Twilio and Segment are both API companies. That means they create an easy way for developers to tap into a specific type of functionality without writing a lot of code. As I wrote in a 2017 article on Segment, it provides a set of APIs to pull together customer data from a variety of sources:

Segment has made a name for itself by providing a set of APIs that enable it to gather data about a customer from a variety of sources like your CRM tool, customer service application and website and pull that all together into a single view of the customer, something that is the goal of every company in the customer information business.

While Twilio’s main focus since it launched in 2008 has been on making it easy to embed communications functionality into any app, it signaled a switch in direction when it released the Flex customer service API in March 2018. Later that same year, it bought SendGrid, an email marketing API company for $2 billion.

Twilio’s market cap as of Friday was an impressive $45 billion. You could see how it can afford to flex its financial muscles to combine Twilio’s core API mission, especially Flex, with the ability to pull customer data with Segment and create customized email or ads with SendGrid.

This could enable Twilio to expand beyond pure core communications capabilities and it could come at the cost of around $5 billion for the two companies, a good deal for what could turn out to be a substantial business as more and more companies look for ways to understand and communicate with their customers in more relevant ways across multiple channels.

As Semil Shah from early stage VC firm Haystack wrote in the company blog yesterday, Segment saw a different way to gather customer data, and Twilio was wise to swoop in and buy it.

Segment’s belief was that a traditional CRM wasn’t robust enough for the enterprise to properly manage its pipe. Segment entered to provide customer data infrastructure to offer a more unified experience. Now under the Twilio umbrella, Segment can continue to build key integrations (like they have for Twilio data), which is being used globally inside Fortune 500 companies already.

Segment was founded in 2011 and raised over $283 million, according to Crunchbase data. Its most recent raise was $175 million in April on a $1.5 billion valuation.

Twilio stock closed at $306.24 per share on Friday up $2.39%.

Segment declined to comment on this story. We also sent a request for comment to Twilio, but hadn’t heard back by the time we published. If that changes, we will update the story.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. You can subscribe here.

First, a big congrats on making it through the week. If you live in the United States, you just endured one of the wildest news weeks ever. Rapid-fire headlines and nigh-panic have been our lot since last Friday when the president announced he was COVID-19 positive. We’re all very tired. You get points for just surviving.

Second, I wanted to bring you something uplifting this weekend, as you deserve it. Sadly, that’s not what we’re going to talk about.

On Friday, The Exchange covered new data concerning the venture capital results of female founders during the third quarter. The data set was U.S.-focused, but we can presume that it is illustrative of global trends. Regardless of that nuance, the data was depressing.

In the third quarter, U.S.-based female founders and co-founders raised 136 rounds worth $434 million, per PitchBook data. That was a handful more rounds than Q2 2020, but far fewer dollars. And it was down across the board compared to Q3 2019. Even more, as we noted in the piece, the aggregate venture capital world did very well.

Here’s some PwC data making that point, and a bit more from my old employer Crunchbase. What matters is that female founders are doing worse when VCs are super active. This will only perpetuate inequalities and inequities in the startup market.

Speaking of which, here’s some more bad news. Vern Howard Jr., the co-founder and CEO of Hallo, a startup that has raised nearly $2 million, according to Crunchbase, compiled some data on Black founders’ VC performance in Q3. Here’s what he set out to do:

[W]e wanted to put hard numbers behind the promises of so many venture capitalists and create a benchmark for how we can track the investment into black founders over time. So our team pulled a list from Crunchbase of all the startups globally with a total funding amount of $500,000 — $20,000,000 and who raised a round between July 1 and October 1. There were over 1383 companies here and our team went through one by one, to see how many Black founders there were.

There were 31.

Now, you could open up the funding bands to include both smaller and larger funding events, but regardless of the data boundaries, the resulting number — just 2.2% of the total — is a disgrace.

Wrapping, this newsletter is a lot of fun and I appreciate your reading it. It is, also, a work in progress. So feel free to hit respond to it and let me know what you want to see more of. Or hit respond and send me a cute pic of your pet. Either is fine by me.

Chat soon,

Powered by WPeMatico