Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

In the world of software development, one term you’re sure to hear a lot of is full-stack development. Job recruiters are constantly posting open positions for full-stack developers and the industry is abuzz with this in-demand title.

But what does full-stack actually mean?

Simply put, it’s the development on the client-side (front end) and the server-side (back end) of software. Full-stack developers are jacks of all trades as they work with the design aspect of software the client interacts with as well as the coding and structuring of the server end.

In a time when technological requirements are rapidly evolving and companies may not be able to afford a full team of developers, software developers that know both the front end and back end are essential.

In response to the coronavirus pandemic, the ability to do full-stack development can make engineers extremely marketable as companies across all industries migrate their businesses to a virtual world. Those who can quickly develop and deliver software projects thanks to full-stack methods have the best shot to be at the top of a company’s or client’s wish list.

So how can you become a full-stack engineer and what are the expectations? In most working environments, you won’t be expected to have absolute expertise on every single platform or language. However, it will be presumed that you know enough to understand and can solve problems on both ends of software development.

Most commonly, full-stack developers are familiar with HTML, CSS, JavaScript and back-end languages like Ruby, PHP or Python. This matches up with the expectations of new hires as well, as you’ll notice a lot of openings for full-stack developer jobs require specialization in more than one back-end program.

Full-stack is becoming the default way to develop, so much so that some in the software engineering community argue whether or not the term is redundant. As the lines between the front end and back end blur with evolving tech, developers are now expected to work more frequently on all aspects of the software. However, developers will likely have one specialty where they excel while being good in other areas and a novice at some things… and that’s OK.

Getting into full-stack, though, means you should concentrate on finding your niche within the particular front-end and back-end programs you want to work with. One practical and common approach is to learn JavaScript because it covers both front and back-end capabilities. You’ll also want to get comfortable with databases, version control and security. In addition, it’s smart to prioritize design, as you’ll be working on the client-facing side of things.

Because full-stack developers can communicate with each side of a development team, they’re invaluable to saving time and avoiding confusion on a project.

One common argument against full stack is that, in theory, developers who can do everything may not do one thing at an expert level. But there’s no hard or fast rule saying you can’t be a master at coding and also learn front-end techniques, or vice versa.

One hold up you may have before diving into full-stack is you’re also mulling over the option to become a DevOps engineer. There are certainly similarities among both professions, including good salaries and the ultimate goal of producing software as quickly as possible without errors. As with full-stack developers, DevOps engineers are also becoming more in demand because of the flexibility they offer a company.

Powered by WPeMatico

Synthetaic is a startup working to create data — specifically images — that can be used to train artificial intelligence.

Founder and CEO Corey Jaskolski’s experience includes work with both National Geographic (where he was recently named Explorer of the Year) and a 3D media startup. In fact, he told me that his time with National Geographic made him aware of the need for more data sets in conservation.

Sound like an odd match? Well, Jaskolski said that he was working on a project that could automatically identify poachers and endangered animals from camera footage, and one of the major obstacles was the fact that there simply aren’t enough existing images of either poachers (who don’t generally appreciate being photographed) or certain endangered animals in the wild to train AI to detect them.

He added that other companies are trying to create synthetic AI training data through 3D worldbuilding (in other words, “building a replica of the world that you want to have an AI learn in”), but in many cases, this approach is prohibitively expensive.

In contrast, the Synthetaic (pronounced “synthetic”) approach combines the work of 3D artists and modelers with technology based on generative adversarial networks, making it far more affordable and scalable, according to Jaskolski.

Image Credits: Synthetaic

To illustrate the “interplay” between the two halves of Synthetaic’s model, he returned to the example of identifying poachers — the startup’s 3D team could create photorealistic models of an AK-47 (and other weapons), then use adversarial networks to generate hundreds of thousands of images or more showing that model against different backgrounds.

The startup also validates its results after an AI has been trained on Synthetaic’s synthesized images, by testing that AI on real data.

For Synthetaic’s initial projects, Jaskolski said he wanted to partner with organizations doing work that makes the world a better place, including Save the Elephants (which is using the technology to track animal populations) and the University of Michigan (which is developing an AI that can identify different types of brain tumors).

Jaskolski added that Synthetaic customers don’t need any AI expertise of their own, because the company provides an “end-to-end” solution.

The startup announced today that it has raised $3.5 million in seed funding led by Lupa Systems, with participation from Betaworks Ventures and TitletownTech (a partnership between Microsoft and the Green Bay Packers). The startup, which has now raised a total of $4.5 million, is also part of Lupa and Betaworks’ Betalab program of startups doing work that could help “fix the internet.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture-capital-focused podcast where we unpack the numbers behind the headlines.

It’s a big day in tech because the U.S. federal government is going after Google on anti-competitive grounds. Sure, the timing appears crassly political and the case is not picking up huge plaudits thus far for its air-tightness, but that doesn’t mean we can ignore it.

So Danny and I got on the horn to chat it up for about 10 minutes to fill you in. For reference, you can read the full filing here, in case you want to get your nails in. It’s not a complicated read. Get in there.

As a pair we dug into what stood out from the suit, what we think about the historical context and also noodled at the end about what the whole situation could mean for startups; it’s not all good news, but adding lots of competitive space to the market would be a net-good for upstart tech companies in the long-run.

And consumers. Competition is good.

You can read TechCrunch’s early coverage of the suit here, and our look at the market’s reaction here. Let’s go!

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

For all of the investors preaching that augmented reality technology will likely be the successor to the modern smartphone, today, most venture capitalists are still quite wary to back AR plays.

The reasons are plentiful, but all tend to circle around the idea that it’s too early for software and too expensive to try to take on Apple or Facebook on the hardware front.

Meanwhile, few spaces were frothier in 2016 than virtual reality, but most VCs who gambled on VR following Facebook’s Oculus acquisition failed to strike it rich. In 2020, VR did not get the shelter-in-place usage bump many had hoped for largely due to supply chain issues at Facebook, but VCs hope their new cheaper device will spell good things for the startup ecosystem.

To get a better sense of how VCs are looking at augmented reality and virtual reality in 2020, I reached out to a handful of investors who are keeping a close watch on the industry:

Some investors who are bullish on AR have opted to focus on virtual reality for now, believing that there’s a good amount of crossover between AR and VR software, and that they can make safer bets on VR startups today that will be able to take advantage of AR hardware when it’s introduced.

“Besides Pokémon Go I don’t think we have seen the engagement numbers needed for AR,” Boost VC investor Brayton Williams tells TechCrunch. “We believe VR is still the largest long-term opportunity of the two. AR complements the real world, VR creates endless new worlds.”

Most of the investors I got in contact with were still fairly active in the AR/VR world, but many still disagreed whether the time was right for VR startups. For Jacob Mullins of Shasta Ventures, “It’s still early, but it’s no longer too early.” While Gigi Levy-Weiss of NFX says that the market is “sadly not happening yet,” Facebook’s Quest headsets have shown promise.

On the hardware side, the ghost of Magic Leap’s formerly hyped glory still looms large. Few investors are interested in making a hardware play in the AR/VR world, noting that startups don’t have the resources to compete with Facebook or Microsoft on a large-scale rollout. “Hardware is so capital intensive and this entire industry is dependent on the big players continuing to invest in hardware innovation,” General Catalyst’s Niko Bonatsos tells us.

Even those that are still bullish on startups making hardware plays for more niche audiences acknowledge that life had gotten harder for ambitious founders in these spaces, “the spectacular flare-outs do make it harder for companies to raise large amounts with long product release horizons,” investor Tipatat Chennavasin notes.

Responses have been edited for length and clarity.

What are your general impressions on the health of the AR/VR market today?

We’re seeing some progress in VR and some of that is happening because of the Oculus ecosystem. They continue to improve the hardware and have a growing catalog of content. I think their onboarding and consumption experience is very consumer-friendly and that’s going to continue to help with adoption. On the consumer side, we’re seeing some companies across gaming, fitness and productivity that are earning and retaining their audiences at a respectable rate. That wasn’t happening even a year ago so it may be partially a COVID lift but habits are forming.

The VR bets of several years ago have largely struggled to pan out, if you were to make a startup investment in this space today what would you need to see?

Companies to watch are the ones that are creating cool experiences with mobile as the first entry point. Wave VR, Rec Room, VRChat are making it really easy for consumers to get a taste of VR with devices they already own. They’re not treating VR as just another gaming peripheral but as a way to create very cool, often celebrity-driven, content. These are the kinds of innovations that makes me optimistic about the VR category in general.

Most investors I chat with seem to be long-term bullish on AR, but are reticent to invest in an explicitly AR-focused startup today. What do you want to see before you make a play here?

In both AR/VR, a founder needs to be both super ambitious but patient. They’ll need to be flexible in thinking and open to pivoting a few times along the way. Product-market fit is always important but I want to see that they have a plan for customer retention. Fun to try is great, habit-forming is much better. Gaming continues to do pretty well as a category for VC dollars but it’d be interesting to see more founders look at making IRL sports experiences more immersive or figuring out how to enhance remote meeting experiences with VR to fix Zoom fatigue.

There have been a few spectacular flare-outs when it comes to AR/VR hardware investments, is there still a startup opportunity in AR/VR hardware?

Hardware is so capital intensive and this entire industry is dependent on the big players continuing to invest in hardware innovation. Facebook and Microsoft seem to be the main companies willing to spend here while others have backed away. If we expand our thinking for a minute, maybe the first real mainstream breakthrough AR/VR consumer experience isn’t visual. For VR, it might be the mobile experiences. For AR maybe AirPods or AirPod-like devices are the right entry point for consumers. They’re in millions of people’s ears already and who doesn’t want their own special-agent-like earpiece? That’s where founders might find some opportunity.

Powered by WPeMatico

This morning Root Insurance, a neoinsurance provider that has attracted ample private capital for its auto-insurance business, is targeting a valuation of as much as $6.34 billion in its pending IPO.

The former startup follows insurtech leader Lemonade to the public markets during a year in which IPOs have been well-received by investors focused more on growth than profitability. In the wake of Lemonade’s strong public offering and rich revenue multiples, it was not impossible to see another, similar startup test the same waters.

Root’s $6.34 billion valuation upper limit at its current price range matches expectations for its bulk. The company is targeting $22 to $25 per share in its debut.

The startup will raise over $500 million from the shares it is selling in its regular offering. Concurrent placements worth $500 million from Dragoneer and Silver Lake raise that figure to north of $1 billion and could help boost general demand for shares in the company. Snowflake’s epic IPO came with similar private placements from well-known investors in what became the transaction of the year.

Will we see Root boost its target? And what does Root’s IPO price range mean for insurtech startups? Let’s dig into the numbers.

We’ve dug into Root’s business a few times now, both before and after it formally filed its IPO documents. This morning we will merge both sets of work, snag a fresh revenue multiple from Lemonade, apply it to Root’s own numbers, observe any valuation deficit and ask ourselves what’s next for the debuting company.

Will we see Root’s IPO price rise? Here’s how to think about the question:

Powered by WPeMatico

Meadow was once called the Amazon of weed. Now it’s trying to be the Salesforce of weed, too.

Meadow, the maker of a popular point-of-sale system for cannabis dispensaries, is today launching new tools for its clients. Called the Meadow Platform, it includes two key tools for dispensaries: a customer relationship manager (CRM) and a text messaging platform for mobile marketing. As the company puts it in the news release, this system is designed to let users push a button and sell more weed.

This system is designed to help legal weed proprietors serve its client base with deep insights and targeted marketing — all while abiding by the strict regulations governing the budding industry (pun intended).

Meadow’s POS system is widely used throughout the legal cannabis industry, giving retailers inventory management, analytics, online ordering and more. Because of regulations, retailers have a wealth of information on their clientele, which Meadow’s system can use for target marketing. Because these new features are built into the Meadow platform, instead of through a third-party add-on, Meadow says it’s protected by the same security used throughout the rest of its platform.

Current regulations make it difficult for dispensaries to market their wares. These retailers cannot fully utilize modern marketing channels such as social media, leaving most retailers with limited options outside of billboards. Meadow’s new solution brings standard marketing tools to dispensaries.

“Marketing is not one-size-fits-all, especially in cannabis. Dispensaries need tools to select which customers they want to talk to in order to send relevant messages and promotions,” David Hua, CEO and co-founder of Meadow, said in a released statement. “Let brand-loyal customers know when their favorite brands release new strains, products, blends or flavors. Tell customers about new hours or delivery and pick-up options. Send reengagement offers to customers who have dropped off. Let members of your loyalty program know when they have points to cash in and include their point balance. Tip-off VIPs when a limited-edition strain becomes available and give them first dibs. This is the level of delight and sophistication that has been missing from cannabis marketing, and we’re very excited to debut it to dispensaries across California.”

David Hua, Harrison Lee, Rick Harrison and Scott Garman founded Meadow in 2014. Since then, the company has raised $2.1 million and participated in Y Combinator’s Winter 2015 class. The company currently has 14 employees.

Building this product has always been part of Meadow’s goal, Hua tells TechCrunch. COVID-19 helped accelerate the need.

“[Meadow] has always had three core priorities,” Hua said. “The first was compliance, which we had a big checkmark at the beginning of this year. The second was operational efficiency, and now marketing. These dispensary owners, especially in this COVID-19 world, can talk directly to their customers again, bring in more revenue and give them more information on what’s happening. Now they can leverage Meadow’s platform to do promo codes, automated discounts, loyalty rewards; we have all that. So you could have a customer that’s ordering an early-bird special at 9:00 am, and that’s a member of your senior group that gets 10% off. You can now send them a message regarding new topicals. Marketing just becomes more engaging.”

Powered by WPeMatico

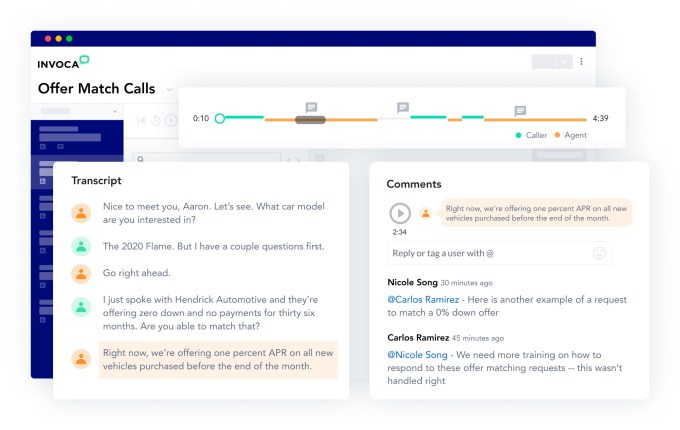

Invoca, which helps companies extract and use data from customer phone calls, is expanding today with the launch of products for e-commerce, customer experience and sales teams, as well as a new Invoca Exchange, where businesses can find all of the platform’s third-party integrations.

The company is making these announcements as part of its virtual Invoca Summit. Ahead of the event, CEO Gregg Johnson (previously an executive at Salesforce) told me that customers have been asking Invoca to expand beyond its previous focus on providing “conversation intelligence” to marketing teams.

“‘We need to get aligned on how we support the revenue journey,’” Johnson recalled businesses telling him. “We were already going down this path, but when COVID hit, we tripled down on it.”

He argued that the data that Invoca provides has become even more important during the pandemic and related lockdowns, when businesses only had “two sources of feedback” — digital interactions and customer conversations. And while there are plenty of analytics tools for tracking online behavior, Johnson said, “Customer conversations are really important because they get at why” people are behaving in a certain way.

And at the same time, Johnson said call center teams have had to shift to working at home, which meant that they had to switch to online software and “everything broke,” while supervisors “no longer had any visibility into how agents were performing.”

Image Credits: Invoca

Invoca is trying to address these issues by making sure that marketing, sales, customer experience and e-commerce teams all have access to the same call data.

For example, he said that agents at Invoca customer BBQGuys need data to understand what products to recommend for their customers if the specific grill that they want isn’t available. Or a healthcare provider might use call data to predict and prepare when COVID cases might be rising in their area.

“We’ve always viewed ourselves as an application and a platform,” Johnson added. “We already give you ability to use this data at Invoca to automatically apply these insights without any human intervention at all. So for us, we thought through use cases to feed this data into other tools and created four solutions … that are really joined at the hip.”

Invoca for eCommerce, Invoca for Customer Experience and the existing Invoca for Marketing product are all available now, while Invoca for Sales is currently signing up beta testers for November.

The Invoca Exchange, meanwhile, already includes more than 40 integrations, including Google, Salesforce, Facebook, Adobe, Tealium, and Five9. The company is also announcing new partnerships with FullStory and Criteo.

Powered by WPeMatico

Stampli, a collaborative invoice management software company, introduced a payments product today called Stampli Direct Pay.

The startup launched back in 2015 with a mission to simplify invoice management through collaboration (and a dash of AI). Interestingly, Stampli said it was uninterested at the time in providing a payments product alongside its collaborative suite, focusing instead on the process of procure to pay.

This latest announcement marks a shift in the company’s thinking. Cofounder and CEO Eyal Feldman explained that conversations with customers revealed just how frustrated many organizations are with the current B2B payments landscape.

Organizations have several options: cut and mail their own paper checks, use ACH, or sign on with a payments provider to use ‘e-payments.’

Cutting and mailing checks is a pre-historic, time-intensive activity that doesn’t really belong in 2020, while ACH (which comes at a very low, flat cost) often groups multiple transactions into a single sum, making it difficult for accounting to reconcile individual line item purchases.

“Under the misleading banner of “e-payments,” [payments providers] offer AP departments a rebate and promise vendors faster payment,” explained Feldman in a blog post. “However, in order for vendors to get the payment, they must accept payments as virtual credit cards, which come with up to a 3.5% credit card fee per transaction.”

And many payments providers do not provide the data extracted from invoices and transactions back to the organization as a way to stay sticky.

Stampli’s customers illuminated these problems for the startup, which used to be payments agnostic. With the launch of Stampli Direct Pay, the company is still payments flexible, letting organizations work with their existing or different payments providers. But Stampli now offers an option that aims to resolve many of these industry issues.

Because Stampli’s core product already tracks all the contextual and relevant info for every transaction, that information is readily available during payment approval. Direct Pay also offers ACH as a payment option, but separates individual transactions out for easy reconciliation. And for customers who want to stick with checks, Stampli Direct Pay offers a service that allows customers to approve digital checks which come directly from their bank account with their signature, with Stampli handling printing, stamping, and mailing.

Stampli also offers a vendor payment portal that extracts the needed data for each vendor and lets the customer own that data, which can be downloaded and taken to another payment provider.

The company has spent the last four years solving an entirely different problem.

Usually, teams purchase products or services and those invoices end up in the finance department with little to no context, setting off a game of duck duck goose within the organization as accountants try to get the information and approvals they need to pay out that vendor.

Stampli, which has raised $32 million to date, built out a collaborative platform that allows non-accountants to participate in the invoice management process in a way that’s straightforward and simple. Each invoice becomes a communications hub, allowing folks across various departments fill in the blanks and. answer questions about the purchase. Stampli also uses machine learning to recognize patterns around allocating costs, managing approval workflows, and the data that needs to be extracted from invoices.

Each invoice is turned into its own communications hub, allowing people across departments to fill in the blanks and answer questions so that payments are handled as efficiently as possible. Moreover, Stampli uses machine learning to recognize patterns around how the organization allocates cost, manages approval workflows and what data is extracted from invoices.

With the launch of Direct Pay, Stampli is poised to take on a variety of new competitors with an obvious differentiator. The company has processed more than $13 billion in invoices annually.

The team has also grown to more than 100 employees. Fifty-six percent of the company’s US workforce is non-white and 33 percent of the executive leadership team is female, according to Feldman.

Powered by WPeMatico

On Friday, former Tiger Global Management investor Lee Fixel registered plans for the second fund of his new investment firm, Addition, just four months after closing the first. According to a report on Friday by the Financial Times, the outfit spent last week finalizing the fundraising for the $1.4 billion fund, which Addition reportedly doesn’t plan to begin investing until next year.

But a source close to the firm now says the capital has not been raised. That’s perhaps good news for investors who were shut out of Addition’s $1.3 billion debut fund and who might be hoping to write a check this time around.

The mere fact that Fixel is back in the market already has tongues wagging about the dealmaker, one whose reluctance to talk on the record with media outlets seems only to add to his mystique. Forbes published a lengthy piece about Fixel this summer, in which Fixel seems to have provided just one public statement, confirming the close of Addition’s first fund and adding little else. “We are excited to partner with visionary entrepreneurs, and with our 15-year fund duration, we have the patience to support our portfolio companies on their journey to build impactful and enduring businesses,” it read.

According to Forbes, that first fund — which Fixel is actively putting to work right now — intends to invest one-third of its capital in early-stage startups and two-thirds in growth-stage opportunities.

Whether that includes some of the special purpose acquisition vehicles, or SPACs, that are coming together right and left, isn’t yet known, though one imagines these might appeal to Fixel, who has long seemed to be at the forefront of new trends impacting growth-stage companies in particular. (A growing number of SPACs is right now looking to transform into public companies some of the many hundreds of richly valued private companies in the world.)

Clearer is that Addition is wasting little time in writing some big checks. Among its announced deals is Inshorts, a seven-year-old, New Delhi, India-based popular news aggregation app that last week unveiled $35 million new funding led by Fixel.

The deal represents Addition’s first India-based bet, even while Fixel knows both the country and the startup well. He previously invested in Inshorts on behalf of Tiger; he’s also credited for snatching up a big stake in Flipkart on behalf of Tiger, a move that reportedly produced $3.5 billion in profits when Flipkart sold to Walmart.

Addition also led a $200 million round last month in Snyk, a five-year-old, London-based startup that helps companies securely use open-source code. The round valued the company at $2.6 billion — more than twice the valuation it was assigned when it raised its previous round 10 months ago.

And in August, Addition led a $110 million Series D round for Lyra Health, a five-year-old, Burlingame, California-based provider of mental health care benefits for employers that was founded by former Facebook CFO David Ebersman.

A smaller check went to Temporal, a year-old, Seattle-based startup that is building an open-source, stateful microservices orchestration platform. Last week, the company announced $18.75 million in Series A funding led by Sequoia Capital, but Addition also joined the round, having been an earlier investor in the company.

According to PitchBook data, Addition has made at least 17 investments altogether.

Fixel — whose bets while at Tiger include Peloton and Spotify — isn’t running Addition single-handedly, though according to Forbes, he is the single “key man” around which the firm revolves, as well as the biggest investor in Addition’s first fund.

He has also brought aboard at least three investment principals from Wall Street and a head of data science who worked formerly for Uber (per Forbes). Ward Breeze, a longtime attorney who worked formerly in the emerging companies practice of Gunderson Dettmer, is also working with Fixel at Addition.

(Correction: An earlier version of this story reported that Fixel’s newest fund was already raised, per the FT.)

Powered by WPeMatico

Today Juniper Networks announced it was acquiring smart wide area networking startup 128 Technology for $450 million.

This marks the second AI-fueled networking company Juniper has acquired in the last year and a half after purchasing Mist Systems in March 2019 for $405 million. With 128 Technology, the company gets more AI SD-WAN technology. SD-WAN is short for software-defined wide area networks, which means networks that cover a wide geographical area such as satellite offices, rather than a network in a defined space.

Today, instead of having simply software-defined networking, the newer systems use artificial intelligence to help automate session and policy details as needed, rather than dealing with static policies, which might not fit every situation perfectly.

Writing in a company blog post announcing the deal, executive vice president and chief product officer Manoj Leelanivas sees 128 Technology adding great flexibility to the portfolio as it tries to transition from legacy networking approaches to modern ones driven by AI, especially in conjunction with the Mist purchase.

“Combining 128 Technology’s groundbreaking software with Juniper SD-WAN, WAN Assurance and Marvis Virtual Network Assistant (driven by Mist AI) gives customers the clearest and quickest path to full AI-driven WAN operations — from initial configuration to ongoing AIOps, including customizable service levels (down to the individual user), simple policy enforcement, proactive anomaly detection, fault isolation with recommended corrective actions, self-driving network operations and AI-driven support,” Leelanivas wrote in the blog post.

128 Technologies was founded in 2014 and raised over $96 million, according to Crunchbase data. Its most recent round was a $30 million Series D investment in September 2019 led by G20 Ventures and The Perkins Fund.

In addition to the $450 million, Juniper has asked 128 Technology to issue retention stock bonuses to encourage the startup’s employees to stay on during the transition to the new owners. Juniper has promised to honor this stock under the terms of the deal. The deal is expected to close in Juniper’s fiscal fourth quarter, subject to normal regulatory review.

Powered by WPeMatico