Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

What do you call the grey area between a Series A and a Series B? In 2020, when the money is taken on opportunistically, you call it a Series A-1 extension, according to Teampay. Even if the new capital was raised at a new, higher valuation.

At least that’s what Teampay CEO Andrew Hoag has done with his company’s new $5 million investment, adding it onto its September, 2019-era Series A. TechCrunch covered that round, and the company’s $4 million seed round in 2018, keeping tabs on the corporate spend-management company as it grows.

Indeed, Teampay has posted big growth since its Series A was announced, pushing its annual recurring revenue (ARR) up by 320% and its total spend managed up by 800%. The first number implies that it has managed to monetize well as its usage, the second number, has spiked.

Teampay, Hoag said in an interview, wants to help companies control their bank accounts. This has gotten harder in 2020, as companies went from having an office with many employees to many employees in home offices. The rising complexity of running companies in the aftermath of COVID-19 and its economic disruptions has been a boon for the startup, with Teampay seeing its sales cycle cut in half, the CEO said, and bigger companies coming to its door, looking for help.

The startup targets the midmarket with its spend software, helping companies control what Hoag views as a business process problem, not merely an ability-to-spend issue. Teampay doesn’t want to reinvent the corporate card, but instead provide a set of tools to help companies manage their outflows, no matter what format they take (ACH, virtual cards, etc.).

So unlike Divvy, say, or Brex, Teampay generates most of its income from software fees instead of interchange revenues, though the company did tell TechCrunch that it has room to derive more revenues from spend over time. On the topic of competition, Teampay has lots in various forms. Brex and Ramp and Divvy and Airbase, not to mention old-guard products like Concur and Expensify, are in the market.

But with a fresh $5 million led by Fin Venture Capital and participated in by prior investors like Crosscut, and Tribe, and the ubiquitous Precursor, Teampay has new ammunition with which to go hunting.

With this raise, Teampay has now raised $21 million in known equity financing to date. I asked Hoag why the new round is not simply called a Series B. He said that the letter-series round demarcations have lost some of their specificity in 2020 (true), undercutting the main thrust of my quibble, and that this round was too small to be called a Series B (also true).

Instead, he said, Teampay pulled forward a bit of its future Series B on the back of big growth, presumably to help the company do more today in anticipation of its later, more traditionally sized next round.

TechCrunch has covered aggressive extension rounds in recent months, putting Teampay in good company with firms that are doing well, leading to their taking on more capital to go even faster. Let’s see how much further it can amp its ARR before its real Series B.

Powered by WPeMatico

U.K.-based Fertifa has bagged a £1 million (~$1.3 million) seed to plug into a fertility-focused workplace benefits platform. Passion Capital is investing in the round, along with some unnamed strategic angel investors.

The August 2019-founded startup sells bespoke reproductive health and fertility packages to U.K. employers to offer as workplace benefits to their staff — drawing on the use of technologies like telehealth to expand access to fertility support and cater to rising demand for reproductive health services.

Challenges conceiving can affect around one in seven couples, per the U.K.’s National Health Service (NHS).

In recent years fertility startups have been getting more investor attention as VC firms cotton on to growing market. Employers have also responded, with tech industry workplaces among those offering fertility “perks” to staff. Although the access-to-services issue can be more acute in the U.S. — given substantial costs involved in obtaining treatments like IVF.

In the U.K. the picture is a little different, given that the country’s taxpayer-funded NHS does fund some fertility treatments — meaning IVF can be free for couples to access. Although how much support couples get can depend on where in the country they live, with some NHS trusts funding more rounds of IVF than others. There can also be access restrictions based on factors such as a woman’s age and the length of time trying to conceive.

This means U.K. couples can run out of free fertility support before they’ve been able to conceive — pushing them toward paying for private treatment. Hence Fertifa spotting an opportunity for a workplace benefits model around reproductive health services.

It signed up its first employers this spring and summer, and says it now has a portfolio of corporate clients with an employee pool from a few hundreds to >10,000 — although it isn’t breaking out customer numbers. Rather, it says its services are available to around 700,000 U.K. employees at this point.

“At Fertifa we want to make fertility services more widely accessible to people,” says founder and CEO Tony Chen. “Some levels of fertility services can be provided by the NHS but every single NHS trust is different with eligibility, requirements and resources, and so unfortunately it can too often be reduced to a “postcode lottery”.

“We believe that everyone should have easy access to information, resources, education and services relating to fertility — and that working with workplaces is one way to start. With our efforts and partnerships we hope to normalise the conversations about fertility at work, just as other forms of health are openly discussed and provided for.”

Passion Capital partner Eileen Burbidge — who is joining Fertifa’s board (along with Passion’s Malin Posern) — has been public about her own use of IVF and takes a very personal interest in the fertility space.

“The unfortunate fact is that over recent years, even though success rates have increased and of course more and more patients are exploring the benefits of IVF, NHS funding has been declining and the number of patients using the NHS for their first cycle has also been decreasing,” she tells TechCrunch.

“This doesn’t take away from the fact that it’s brilliant what we get from the NHS here in the U.K., but there’s clearly a lot more which can be done to further increase accessibility and affordability — given less and less funding for the NHS in the face of increasing demand of both the NHS and private routes.”

Fertifa says its model is to provide direct care and support to employees — rather than being a broker or acting as part of a referral system. So it has two in-house clinicians at this stage (out of a team of 10-15 people). Although it also says it “partners” with clinicians and clinics across the U.K. So it’s not doing everything in-house.

It offers what it bills as a “full range” of fertility and gynaecology services — from assisted reproductive technology such as IVF, IUI and more; fertility planning such as egg, sperm and embryo freezing to donor-assisted and third-party reproduction such as donor eggs and sperm; as well as surrogacy and adoption.

Its doctors, nurses and “fertility advocates” are there to provide a one-to-one care service to support patients throughout the process.

“We use technology in a number of ways and are ambitious about how it will help us to maintain an advantage over others in the sector and provide the best customer experience,” says Chen, noting it has developed “a full end-to-end” app for patients to guide them through the various stages of their fertility journey.

“On the employer side we have a full employer portal as well which provides educational resources, support options and access to services for HR/People teams to use and share with their workforces. Additionally, we use telehealth to enable more efficient, convenient (particularly in the age of COVID-19 restrictions) and immediate consultations with clinicians and nurses. Finally, we are refining our machine learning algorithms to help drive more informed decision making for patients and clinicians alike.”

It’s not currently applying AI but says that over time its in-house medical experts will use artificial intelligence to aid decision-making — with the aim of reducing clinic visits, enhancing the patient experience and yielding better clinical pregnancy rates.

Chen points to the U.K.’s Human Fertilisation and Embryology Authority having already made its data publicly available on more than 100,000 couples and their treatment and outcomes — suggesting such data-sets will underpin the development of new predictive models for fertility.

“With additional insight and data sources [we] could more accurately predict probability of success for a patient — or the best type of treatment for them,” he adds.

While Fertifa’s current focus is U.K. expansion — targeting workplaces of all sizes and scale — it’s also got its eye on scaling overseas down the line. Although it will of course face more competition at that point, with the likes of Y Combinator backed Carrot already offering global fertility benefits packages for employers.

“Fertility and reproductive health is important to people all over the world,” says Chen. “Globally one in four women experience a miscarriage, every LGBT+ individual requires support to become a parent, and everyone needs to be increasingly empowered to take control of their reproductive health through fertility preservation treatment.”

Powered by WPeMatico

Coronavirus cases in the United States are reaching new peaks. E-commerce is continuing to boom. And b8ta, a San Francisco startup that is betting on the future of physical retailers, is doubling down on its in-person footprint.

B8ta offers shelf space to unique digital products, such as electric skateboards or a coffee alarm clock, on behalf of brands that want a physical presence. Today, the company acquired a 1-year-old company doing the same for direct to consumer businesses, Re:store.

Backed by Sequoia and SPC, Re:store has a three-story physical location in Maiden Lane in San Francisco, and hosts products ranging from beauty to consumer electronics to lifestyle products. It also has a community co-working space.

The Re:store community hub.

“The pandemic has emphasized the need for brands to be flexible with their product mix and distribution,” says Selene Cruz, CEO of Re:store. “Some products do well in these times, and brands in a retail-as-a-service model can adapt their offering a lot faster than those in a traditional wholesale model that relies on buying cycles.”

It’s the high-touch startups that are expected to struggle during this time, as rising virus rates threaten the global economy. But, as today’s deal shows, both b8ta and Re:store are bullish on in-person shopping long term.

In fact, in March, b8ta CEO and co-founder Vibhu Norby penned an extensive Twitter thread in favor of keeping his startups’ stores open, noting that closures would require the company to lose millions and send tens of thousands of employees home. B8ta’s entire value proposition is based on high-touch interactions, and a world in which consumers want to try and experience their products before they buy them.

At b8ta, we are in the business of physical retail stores. While we sell products online, our stores are the reason for our existence. We encourage our shoppers to touch and try all of the products at b8ta. We are truly in the business of touch and human-to-human relationships.

— Vibhu Norby (@vibhu) March 13, 2020

“I feel like we’ve lived through three lifetimes since I wrote that thread back in March,” Norby said, noting that it’s been an “extremely difficult year” for the company. However, the Re:store acquisition comes off of new momentum he’s seen since b8ta was able to safely reopen its stores in May.

“We launched more brands last quarter than any other in our history,” Norby said. “The traditional retail model and traditional real estate model has completely collapsed and brands are looking for something better.” To note, Macy’s, which has backed b8ta, narrowly dodged bankruptcy by securing a $4.5 billion lifeline in financing to temper down sales.

Image Credits: b8ta

B8ta’s Re:store acquisition is a response to a rebound among physical retailers, one that favors an experience instead of a catalog of aisles. A focus on creative in-person experiences versus department stores is an acceleration of a pre-pandemic trend. As direct-to-consumer investors told us in late March, companies can’t depend on a few channels for customer acquisition. As the field gets crowded, brands are looking to stand out, and stores like b8ta and Re:store could help them do that.

To balance out some of b8ta’s bullishness, Norby did note that “on the shopping side, visitation is way down but sales have almost come back to where they were pre-pandemic.” In other words, people are buying b8ta products online without the physical presence, which means that online platforms are still a preference for consumers.

Powered by WPeMatico

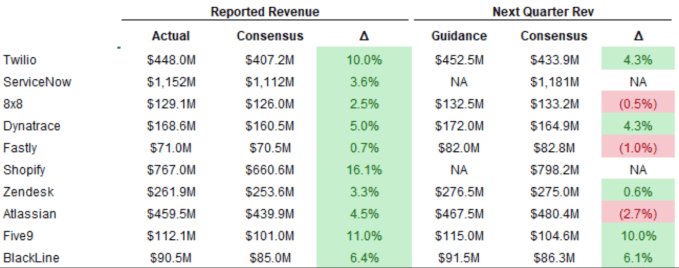

Yesterday’s earnings deluge made plain that tech shares are not rocketing higher as 2020 comes to a close. Indeed, in pre-market trading this morning, Microsoft, Apple, Facebook and Amazon are all down.

Alphabet is the only member of the Big Five that is worth more today than yesterday. Strong advertising and cloud results helped the search giant post a return-to-form quarter. But in most other reports there were signs of weakness or underperformance compared to expectations that could undermine the relentlessly bullish attitude tech shares have enjoyed for several months.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The tailwinds that lifted much of tech this year remain. Every CEO I speak to still thinks that the COVID-19 bump to digital services demand has room to run, and that the digital transformation’s acceleration that has been a regular point of optimism for VCs, founders and public company leaders, will continue.

But that doesn’t mean all tech companies will benefit or post outsize results. Those facts don’t imply that pandemic-induced friction won’t add up.

But that doesn’t mean all tech companies will benefit or post outsize results. Those facts don’t imply that pandemic-induced friction won’t add up.

It’s not only the biggest companies that are treading water. We’re seeing valuations pause in tech’s hottest category — SaaS and cloud — despite continued growth in its constituent companies. The combined sentiment-and-share change could dampen enthusiasm for startup shares, perhaps undercutting some of the hype and FOMO that we keep hearing is driving private valuations higher.

Are we seeing a change in tech’s temperature while the weather changes? Let’s take a look.

Starting with the biggest tech companies, Alphabet’s results were pretty good. The company’s YouTube and cloud segments outperformed expectations, helping the company best expectations.

From there, things get choppier. Apple beat expectations, but its shares fell after investors were less than impressed with its aggregate results. Microsoft posted good calendar Q3 earnings, including strong Azure performance, but its guidance left investors underwhelmed and its shares also fell. Facebook beat expectations in the quarter, but rising costs seemed to dampen investor sentiment. It lost a little ground after earnings. Amazon’s Q3 was hot, but its Q4 should reduce operating income due to COVID-19 costs. It also lost ground after reporting.

From that malaise we turn to the SaaS and cloud world. Redpoint’s Jamin Ball is doing his usual roundups, one of which we’re borrowing this morning. Here’s his digest of SaaS and cloud earnings thus far:

Takeaways? Every SaaS and cloud company crushed Q3, but Q4 is looking a bit more dicey. Beats look slim, some companies are declining to project and aside from an outlier or two, the numbers look slimmer overall.

Powered by WPeMatico

Here’s an example of ad targeting that’s actually good for public health: In a campaign encouraging people to wear masks, the Illinois state government has been focusing its digital ad dollars on the counties with the highest COVID risk.

To achieve this, the government’s been working with Civis Analytics, the data science company founded by Dan Wagner, who was previously chief analytics officer for Barack Obama’s 2012 reelection campaign. The campaign kicked off in August, but the state is now sharing more details about its work, including a map that shows the week-by-week risk assessment that it used for targeting.

Crystal Son, Civis’ director of healthcare analytics, explained that every week, her team pulls together the latest county-level COVID data for Governor J.B. Pritzker’s team, who then use it to determine where ad dollars for the It Only Works If You Wear It campaign should be spent.

Cameron Mock, chief of staff at the Governor’s Office of Management and Budget, said in a statement that the government is using “a one-of-a-kind formula to concentrate media dollars in the areas with the most risk.”

Mock continued, “The risk-based formula uses trends of cases and mobility on the county level to designate higher, medium and lower-risk counties. It then uses a pro rata share to dedicate the most dollars to the highest-risk areas.”

Image Credits: State of Illinois

This formula divides counties into five tiers, with Tier 1 being the highest risk and Tier 5 being the lowest. Tiers 4 and 5 still receive a baseline level of ad spend, but Tier 3 counties see more spending and Tiers 1 and 2 receive the maximum amount.

While the mask campaign isn’t limited to online advertising, the formula is only being used on the digital side because it’s more difficult to adjust funding for more traditional ad channels on a week-by-week basis.

“Each county has unique and changing circumstances due to the virus, so we designed this campaign to respond to the on-the-ground situation in all 102 counties in Illinois,” said Alex Hanns, deputy press secretary to Governor Pritzker, in a statement. “As an area’s risk increases, so too will its concentration of public health messaging. As the pandemic continues and another wave of coronavirus looms, the state of Illinois will continue to listen to scientists and follow the data to keep our residents safe.”

Son said she’s not aware of any other campaign responding to COVID-19 that uses a similar model to prioritize spending in the highest-risk geographies. Is it working? While this data doesn’t show the effects of a specific campaign, according to Carnegie Mellon University, 89% of Illinois residents wear masks — currently the 15th-highest usage rate in the U.S.

In the future, Son said she’s hopeful that we’ll see other organizations adopt “a much more customized communications approach” for healthcare.

“We still have the habit in healthcare of treating groups of people as if they are homogenous, as if they all act the same and think the same,” she said. “There are widespread applications beyond mask-wearing for more tailored approaches.”

Powered by WPeMatico

What does a hologram-obsessed entrepreneur do for a second act after setting up a virtual Ronald Reagan in the Reagan Memorial Library, or beaming Jimmy Kimmel all the way from Hollywood to the Country Music Awards in Nashville?

If that entrepreneur is David Nussbaum, the founder of PORTL Hologram, the next logical step is to build a machine that can bring the joy of hologram-based communication to the masses.

That’s the goal thanks to a new $3 million round that Nussbaum’s company raised from famed venture investor Tim Draper, former Electronic Arts executive Doug Barry and longtime awards-show producer Joe Lewis.

Barry is not only backing the company, he’s also coming on board as its first chief operating officer.

Much of this interest can be traced back to the hologram performance given posthumously by Tupac Shakur back at Coachella about eight years ago.

Nussbaum turned the excitement generated by that event into a business. He bought the patents that powered Tupac’s beyond-the-grave performance, and used the technology to beam Julian Assange out of the Ecuadoran embassy he had been holed up in during his years in London and making dead stars live (and tour) again.

Those visual feats were basically just an updated version of the Pepper’s Ghost technique that stage illusionists and moviemakers have been using since it was invented by John Pepper in the 19th century.

The PORTL is a significant upgrade, according to Nussbaum.

The projector can transmit images any time of the day or night, and using PORTL’s capture studio-in-a-box means that anyone with $60,000 to spend and a white background can beam themselves into any portal anywhere in the world.

The company has sold a hundred devices and already delivered several dozen to shopping malls, airports and movie theater lobbies. “We’ve manufactured and delivered several dozen,” Nussbaum said.

Part of the selling point, beyond just the gimmick of the hologram’s next-level verisimilitude, is its interactivity. Through the studio rig and PORTL hardware, users can hear what people standing around the PORTL are saying and then respond.

For its next trick, PORTL is looking to build a miniaturized version of its system that would be about the size of a desktop computer and could be used to both record and distribute the holograms to anyone with a PORTL device.

“The minis will have all of the features to capture your content and rotoscope you out of our background and have the studio effects that is important in displaying your realistic volumetric like effect and they will beam you to any other device,” Nussbaum said.

To build out the business, the PORTL minis will have more than just communications capabilities, but recorded entertainment as well, Nussbaum said.

“The minis will be bundled with content like Peloton and Mirror bundled with very specific types of content. We are in conversations with a number of extremely well-known content creators where we would bundle a portal but will also have dedicated and exclusive content… [and] bundle that for $39 to $49 per month.”

It’s a vision that Nussbaum admits is far more expansive than his intentions — and the person he has to thank for the more ambitious vision of the business is none other than Draper.

“When I started this I thought it was going to be a novelty company,” he said. “When the pandemic hit he knew we needed to do much more than that.”

Powered by WPeMatico

In 2019, only one Black woman was named partner in venture capital, according to All Raise, a nonprofit focused on accelerating female founders and investors. The data has shown, shows, and will continue to show how the tech industry fails to invest in underrepresented women of color.

Thus, hiring the next generation of founders and decision-makers is key (and promoting them is, too).

Sydney Thomas, who was the first hire at Precursor Ventures, a seed and early-stage focused fund led by Charles Hudson, has been promoted from senior associate to principal. Thomas is joined by Hudson, analyst Ayanna Kerrison and entrepreneur-in-residence Chapman Snowden, to make up Precursor.

After graduating from the Haas School of Business at Berkeley in 2016, Thomas joined Precursor to do what Hudson says most applicants wouldn’t: the operational work of bringing a solo-GP fund, then with less than $5 million in committed capital, to a more organized place.

“The fund was basically running out of my inbox,” Hudson said. “She really helped us get to a much better place operationally.” Thomas started off as an intern, toggling time between working for a Precursor portfolio company and the fund itself, and eventually came on as a senior associate.

As a principal, Thomas will now have more discretion to do deals and make decisions for the firm. “The goal was always for her to get us to a place operationally where she wasn’t as critical,” Hudson notes. Thomas did not respond to request for comment.

Roles within venture have grown increasingly, and often intentionally, vague over time. At any given fund, there can be principals, investors, partners, investing principal partners and senior associate investors. Depending on the fund, each person could just go under the guise of “partner” and call it a day. But in action, every member on a venture team has a varying range of investment autonomy, decision-making authority and weight at the firm.

While the vagueness can balance out egos within a firm, it can often leave founders confused over who has the ability to give them money.

Hudson says he takes role differentiation seriously, and (patiently) wants to build Precursor into a place that helps people in venture get their first start. With Thomas’s promotion, she has the ability to green light investments without the mass overhead of what it means to be a partner.

“I think the only reason to make someone a principal is if you think that they could develop into a partner,” he said.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

A few notes before we get into this. One, we have a bonus episode coming this Saturday focused on this week’s earnings reports. And, second, we did not record video this week. So, if you like watching the show on YouTube, this is not the week for that!

Right, here’s what Natasha, Danny and your humble servant got into this week:

We capped off with the latest from r2c, and then got the hell off the mics. Catch you all Saturday, and then back to regular programming on Monday morning.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

NASA just made history by landing a spacecraft on an asteroid. If that kind of technical achievement carbonates your glass of Tang, join us on December 16-17 for TC Sessions: Space 2020, an event dedicated to early-stage space startups.

We’ve launched early-bird pricing, and $125 buys you access to all live sessions, plus video on demand. Don’t procrastinate. Buy your pass now before the early-bird reenters Earth’s atmosphere (and prices go up) on November 13 at 11:59 p.m. (PT).

More ways to save: Go further together with early-bird group tickets ($100) — bring four team members and get the fifth one free. We also offer discount passes for students ($50) and government, military and nonprofits ($95). Looking for out-of-this-world exposure? An Early-Stage Startup Exhibitor Package ($360) includes four tickets, digital exhibition space, a pitch session to attendees and the ability to generate leads. Bonus savings: Extra Crunch subscribers get a 20% discount.

TC Sessions: Space is an unrivaled opportunity to learn from, connect and network with boundary-pushing founders, investors and officials from NASA, the Aerospace Corporation, the U.S. Air Force and leading space companies spanning public, private and defense sectors.

We’ve packed the conference with outstanding presentations, fireside chats and interviews. Plus, you’ll find breakout sessions on specialized topics, audience Q&As with Main Stage speakers and the expo area for partners and early-stage startups.

Here’s a taste of the topics, but keep an eye on the agenda, because we’ll add more speakers and sessions in the coming weeks.

Lisa Callahan, vice president/general manager of commercial civil space at Lockheed Martin Space, discusses all aspects of scientific and civil exploration of the solar system — from robots scooping rockets from the surface of galaxy-traveling asteroids, to preparing for the return of humans to the surface of the moon.

Lt. General Thompson is responsible for fostering an ecosystem of non-traditional space startups and the future of Space Force acquisitions, all to the end goal of protecting the global commons of space. He’ll discuss what the U.S. looks for in startup partnerships and emerging tech, and how it works with these young companies.

Corporate VC funds are a key source of investment for space startups, in part because they often involve partnerships that help generate revenue, and because they understand the timelines involved. SpaceFund’s Meagan Crawford and Lockheed Martin Ventures’ J. Christopher Moran discuss how these funds fit in with more standard venture to power the ecosystem.

TC Sessions: Space 2020 takes flight on December 16-17, but we’re starting our early-bird countdown right now. Great savings disappear in two weeks on November 13 at 11:59 p.m. (PT). Buy your early-bird passes today and celebrate your savvy shopping with a tall glass of Tang.

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico

Workplace SaaS tools for teams have seen rocket ship growth in the past several years, and that adoption has given rise to a host of software tools geared toward improving individual productivity. Many of the startups behind these tools see building a cult following among individual users as the best way to set themselves up for later enterprise-wide success.

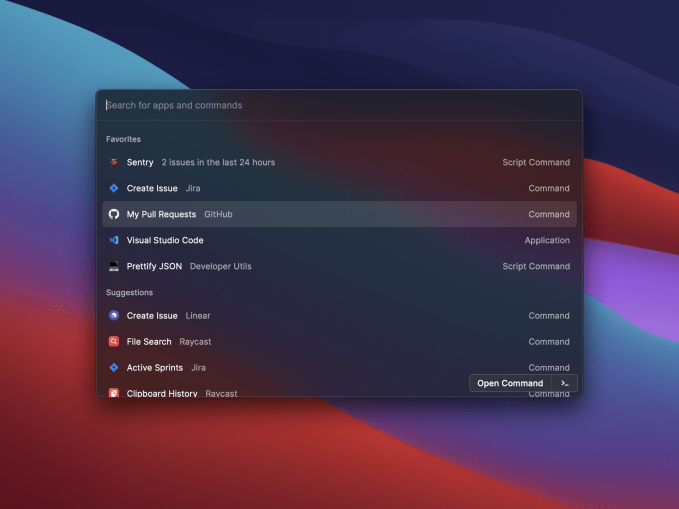

Raycast is a developer-focused productivity tool that aims to be the quickest way to get common tasks done. Today, it’s launching into public beta and sharing with TechCrunch that the team has raised new funding from Accel months after graduating from Y Combinator.

The company has closed a $2.7 million seed round led by Accel, with participation from YC, Jeff Morris Jr.’s Chapter One fund, as well as angel investors Charlie Cheever, Calvin French-Owen and Manik Gupta .

The desktop software takes a note from peers like Superhuman and Command E, allowing users to quickly pull up and modify data with keyboard shortcuts. Users can easily create and re-modify issues in Jira, merge pull requests in GitHub and find documents. The software is very much a developer-focused version of Apple’s Spotlight search that aims to help software engineers navigate with a single tool all the parts of their job that aren’t development work.

Image via Raycast.

Like plenty of workplace tools startups, one of the keys for Raycast is building out a network of extensions that can encompass a user’s workflow. For now, the software supports integrations from Asana, Jira, Zoom, Linear, G Suite, Calendar, GitHub and Reminders, alongside core functionality that can help manage system settings and a calculator that can handle complex math problems. As the startup launches out of public beta, they’re looking to double down on extensions and are rolling out a developer program for early access to their API.

The Mac-only software is free while in public beta, but the company does plan on charging a monthly subscription for the service eventually, though they aren’t quite ready to talk about pricing yet.

Raycast’s team is interested in appealing to individual users for now, but might eventually expand to becoming a teams-level enterprise product that could help onboard new employees faster by quickly orienting them with their office’s software suite, but that’s all a bit down the road, the team says.

“We’re staying focused on single-player mode for a while,” CEO Thomas Paul Mann tells TechCrunch.

Powered by WPeMatico