Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Data engineering is one of these new disciplines that has gone from buzzword to mission critical in just a few years. Data engineers design and build all the connections between sources of raw data (your payments information or ad-tracking data or what have you) and the ultimate analytics dashboards used by business executives and data scientists to make decisions. As data has exploded, so has their challenge of doing this key work, which is why a new set of tools has arrived to make data engineering easier, faster and better than ever.

One of those tools is Datafold, a YC-backed startup I covered just a few weeks ago as it was preparing for its end-of-summer Demo Day presentation.

Well, that Demo Day presentation and the company’s trajectory clearly caught the eyes of investors, since the startup locked in $2.1 million in seed funding from NEA, the company announced this morning.

As I wrote back in August:

With Datafold, changes made by data engineers in their extractions and transformations can be compared for unintentional changes. For instance, maybe a function that formerly returned an integer now returns a text string, an accidental mistake introduced by the engineer. Rather than wait until BI tools flop and a bunch of alerts come in from managers, Datafold will indicate that there is likely some sort of problem, and identify what happened.

Definitely read our profile if you want to learn more about the product and origin story.

Not a whole heck of a lot has changed over the past few weeks (some new features, some new customers), but with more money in its billfold, Datafold is going to keep on growing, hiring and taking on the world of data engineering.

Powered by WPeMatico

Affirm, a consumer finance business founded by PayPal mafia member Max Levchin, filed to go public this afternoon.

The company’s financial results show that Affirm, which doles out personalized loans on an installment basis to consumers at the point of sale, has an enticing combination of rapidly expanding revenues and slimming losses.

Growth and a path to profitability has been a winning duo in 2020 as a number of unicorns with similar metrics have seen strong pricing in their debuts, and winsome early trading. Affirm joins DoorDash and Airbnb in pursuing an exit before 2020 comes to a close.

Let’s get a scratch at its financial results, and what made those numbers possible.

Affirm recorded impressive historical revenue growth. In its 2019 fiscal year, Affirm booked revenues of $264.4 million. Fast forward one year and Affirm managed top line of $509.5 million in fiscal 2020, up 93% from the year-ago period. Affirm’s fiscal year starts on July 1, a pattern that allows the consumer finance company to fully capture the U.S. end-of-year holiday season in its figures.

The San Francisco-based company’s losses have also narrowed over time. In its 2019 fiscal year, Affirm lost $120.5 million on a fully-loaded basis (GAAP). That loss slightly fell to $112.6 million in fiscal 2020.

More recently, in its first quarter ending September 30, 2020, Affirm kept up its pattern of rising revenues and falling losses. In that three-month period, Affirm’s revenue totaled $174.0 million, up 98% compared to the year-ago quarter. That pace of expansion is faster than the company managed in its most recent full fiscal year.

Accelerating revenue growth with slimming losses is investor catnip; Affirm has likely enjoyed a healthy tailwind in 2020 thanks to the COVID-19 pandemic boosting ecommerce, and thus gave the unicorn more purchase in the realm of consumer spend.

Again, comparing the company’s most recent quarter to its year-ago analog, Affirm’s net losses dipped to just $15.3 million, down from $30.8 million.

Affirm’s financials on a quarterly basis — located on page 107 of its S-1 if you want to follow along — give us a more granular understanding of how the fintech company performed amidst the global pandemic. After an enormous fourth quarter in calendar year 2019, growing its revenues to $130.0 million from $87.9 million in the previous quarter, Affirm managed to keep growing in the first, second, and third calendar quarters of 2020. In those periods, the consumer fintech unicorn recorded a top line of $138.2 million, $153.3 million, and $174 million, as we saw before.

Perhaps best of all, the firm turned a profit of $34.8 million in the quarter ending June 30, 2020. That one-time profit, along with its slim losses in its most recent period make Affirm appear to be a company that won’t hurt for future net income, provided that it can keep growing as efficiently as it has recently.

The pandemic has had more impact on Affirm than its raw revenue figures can detail. Luckily its S-1 filing has more notes on how the company adapted and thrived during this Black Swan year.

Certain sectors provided the company with fertile ground for its loan service. Affirm said that it saw an increase in revenue from merchants focused on home-fitness equipment, office products, and home furnishings during the pandemic. For example, its top merchant partner, Peloton, represented approximately 28% of its total revenue for the 2020 fiscal year, and 30% of its total revenue for the three months ending September 30, 2020.

Peloton is a success story in 2020, seeing its share price rise sharply as its growth accelerated across an uptick in digital fitness.

Investors, while likely content to cheer Affirm’s rapid growth, may cast a gimlet eye at the company’s dependence for such a large percentage of its revenue from a single customer; especially one that is enjoying its own pandemic-boost. If its top merchant partner losses momentum, Affirm will feel the repercussions, fast.

Regardless, Affirm’s model is resonating with customers. We can see that in its gross merchandise volume, or total dollar amount of all transactions that it processes.

GMV at the startup has grown considerably year-over-year, as you likely expected given its rapid revenue growth. On page 22 of its S-1, Affirm indicates that in its 2019 fiscal year, GMV reached $2.62 billion, which scaled to $4.64 billion in 2020.

Akin to the company’s revenue growth, its GMV did not grow by quite 100% on a year-over-year basis. What made that growth possible? Reaching new customers. As of September 30, 2020, Affirm has more than 3.88 million “active customers,” which the company defines as a “consumer who engages in at least one transaction on our platform during the 12 months prior to the measurement date.” That figure is up from 2.38 million in the September 30, 2019 quarter.

The growth is nice by itself, but Affirm customers are also becoming more active over time, which provides a modest compounding effect. In its most recent quarters, active customers executed an average of 2.2 transactions, up from 2.0 in third quarter of calendar 2019.

Also powering Affirm has been an ocean of private capital. For Affirm, having access to cash is not quite the same as a strictly-software company, as it deals with debt, which likely gives the company a slightly higher predilection for cash than other startups of similar size.

Luckily for Affirm, it has been richly funded throughout its life as a private company. The fintech unicorn has raised funds well in excess of $1 billion before its IPO, including a $500 million Series G in September of 2020, a $300 million Series F in April of 2019, and a $200 million Series E in December of 2017. Affirm also raised more than $400 million in earlier equity rounds, and a $100 million debt line in late 2016.

What to make of the filing? Our first-read take is that Affirm is coming out of the private markets as a healthier business than the average unicorn. Sure, it has a history of operating losses and not yet proven its ability to turn a sustainable profit, but its accelerating revenue growth is promising, as are its falling losses.

More tomorrow, with fresh eyes.

Powered by WPeMatico

In retrospect, 2019 feels like the working world’s last dance with spontaneity. The pre-pandemic past is rife with conferences, running into co-workers and post-work happy hours. Now, as companies such as Microsoft and Twitter declare remote work as the future, the very existence of physical offices is unclear for the long-term.

Yet, to a growing number of entrepreneurs in the Valley, when one physical door closes, a virtual one opens. With the goal of making remote work more spontaneous, there are dozens of new startups working to create virtual HQs for distributed teams. The three that have risen to the top include Branch, built by Gen Z gamers; Gather, created by engineers building a gamified Zoom; and Huddle, which is still in stealth.

The platforms are all racing to prove that the world is ready to be a part of virtual workspaces. By drawing on multiplayer gaming culture, the startups are using spatial technology, animations and productivity tools to create a metaverse dedicated to work.

The biggest challenge ahead? The startups need to convince venture capitalists and users alike that they’re more than Sims for Enterprise or an always-on Zoom call. The potential success could signal how the future of work will blend gaming and socialization for distributed teams.

Companies within the virtual HQ world sit on a spectrum. On one end, there are the productivity companies, and on the other end, there are the video game companies. In the middle sits a mix between work and play, which is where Branch hopes to live.

There are more than 500 companies on Branch’s waitlist, and of current users, the retention has been 60% after a month of using the platform. So far, it has raised $1.5 million from investors including Homebrew, Naval Ravikant, Sahil Lavingia and Cindy Bi.

Walk through Branch’s virtual HQ and there are all the normal details you’d find in an office on Market Street: There are meeting rooms, lunch tables, a literal watercooler and, yes, succulents on your co-worker’s desk. Most employees log on for 12 hours, and for Election Day, they all had a watch party with a projected live stream in one area of the office.

The founder tells me that he’s hired people — and fired people — all in the virtual offices. Doors, he says, make a big difference.

The platform wasn’t built as a pandemic phenomenon, but in fact, was the result of years of experimentation by the founders, Dayton Mills and Kai Micah Mills. Both founders, since the age of 15, have spent time building Minecraft servers to sell to gamers, netting each thousands of dollars a month. In fact, Kai dropped out of high school to run Minecraft servers full-time, while Dayton tried at 13 to create his own game studio, even hiring an artist to do the illustrations. The game studio failed due to the fact that he was a “kid, 13, and had no money.”

“I spent the majority of my time online playing games with people. So my whole day was playing video games and having people to talk to in the background because I was on constant calls with people,” co-founder Dayton Mills said. “So for me, it’s not hard at all to use it. The question is can I get other people to think the same way?”

For now, Dayton Mills remains confident that his team’s platform will do well. After all, work is a non-negotiable place that you have to show up every day. And why not make that a little more fun?

“You can build a space where everyone comes to work,” he said. “Then after that, you can start building the spaces where they go after work. And it kind of spirals from there.”

Branch, like other virtual HQ platforms, is forced into an interesting spot of being both relevant enough to be used, but passive enough of an app to not feel like a burden. Dayton Mills says that this dynamic has made the team add features like no mandatory video or audio, and a talking icon per user to give the appearance of live interaction. The focus is to keep it casual so people can actually be online for six hours a day.

“People use Slack to work remotely but you go into a physical office and people are still using Slack, he said. The co-founder hopes the same for Branch, and has started measuring how many times people talk to each other in a given day. He says there are hundreds of chats per day, even if some are only for a few seconds.

The key technology that Branch and others are using to create spontaneity is spatial gaming infrastructure. At its core, the technology allows users to only hear people within their nearby proximity, and get quieter as they “walk” away. It gives the feeling of a hallway bump-in.

Dayton Mills thinks that the winning company in this crowded space is the one that can create a space that cultivates and sparks spontaneity.

“You can’t create the serendipity itself directly,” he said. “So create that environment.”

Gather, likely the largest virtual HQ platform out there, has embedded features to do what Mills is suggesting, such as “shoulder taps” to prompt a co-worker to chat, or pool tables where employees can circle around and start a virtual game of pool. The office tour included seeing a corgi on the desk, jack-o-lanterns and this reporter even added some floor plants to the set-up.

Gather’s main floor.

“You don’t need to worry about constantly worrying about if you’re being seen or not, but you will hear anyone who tries to come and talk to you,” said Phillip Wang, the founder of Gather.

The office design includes whiteboards and floating Google Docs to promote announcements and conversations.

Gather has been in the works for more than 18 months, since Wang and his friends graduated college. The team first tried to create custom wearables that would show you which of your friends were able to talk so you can tap into a conversation. When that didn’t work, they pivoted into apps, VR and full-body robotics. Then COVID-19 hit, and they saw an opening in the workplace.

Gather raised some money from angel investors, but has largely stayed away from institutional investors due to the potential of their cap table “biasing” the growth and direction of the company.

“You could easily end up in situations where the only options are ones you’re not happy with,” Wang said, of bringing VCs on at this stage. “We always want the way we make money to be aligned and incentivized to do good for our users.”

Angel investor Josh Elman tells me that many VCs are interested in the product, given traction and team, but also because virtual HQs have the potential to be more than just, well, virtual HQs. While offices are one space that the technology can occupy, the same base can be applied to schools, events, weddings and more.

To show potential, Elman nodded at Hopin, an online events platform that recently raised $125 million at a $2.1 billion valuation. It seems that most VCs agree there will be a number of winners in the events space, but it just comes down to the stickiness of the platform.

With the right value proposition, it’s not hard for people to understand multiplayer online gaming. For example, Epic Games’ Fortnite threw a psychedelic Travis Scott concert and more than 12.3 million people watched.

Thus, people are smart enough to understand gaming — but what about wanting to do it every single day with their colleagues, sans music and flashing lights? The total addressable market for professional, social gaming is murky. What if these platforms are a little bit more palatable as healthy businesses, instead of betting that the upstarts are a venture-backable business that could one day become a $100 billion business?

Image Credits: Bryce Durbin

Huddle’s Florent Crivello disagrees. He thinks the market opportunity for his company, an in-stealth remote HQ, is in the trillions because it has the potential to disrupt real estate, transportation and, in a macro sense, urban cities.

“I tell my former colleagues at Uber that I’m still working on transportation,” he said. “It’s just that the future of transportation is no transportation.”

Huddle has been in private beta for six months and is used by teams at Apple and Uber. There have been tens of thousands of hours of meeting on the platform, and Crivello says that some customers have stopped using Slack or Zoom altogether.

“The mistake they’re making at Slack is that there’s a difference between seeing a list of names on the screen and clicking on a name. And there’s a difference between seeing someone in the office and saying hi,” he said. “I think there’s something very human about the latter.”

Sahil Lavingia, the founder of Gumroad, got rid of Gumroad’s office in 2016, and says that they’re never going back.

“Offices are just too expensive and not necessary 40 hours a week,” he said. “I don’t think physical offices will go away, but they’ll be vastly diminished now that people know work can happen quite effectively, remotely. It’s also much cheaper.” Lavingia invested in Branch’s seed round.

Megan Zengerle, a partner at Sweat Equity who previously had a career in HR, said that companies considering virtual HQs should think about how long-term the solution is.

“Is that truly the culture you want to build for the company? Is that something that will serve the company long term? Is it logical sense to set up that way?” Zengerle said. “Culture is living and breathing, it’s not a static thing that you set and is done.”

Zengerle thinks that virtual HQs depend largely on the scope and product of the team. Most definitely, she does not think the solution is one size fits all.

“There’re a lot of playbooks coming out of the pandemic,” she said. “But the way you vary happens across each employee in the organization, much less organization by organization.”

These are the hurdles that have limited startups in the past, including 2011 TechCrunch Disrupt winner Shaker, from attracting a large customer base.

Before the pandemic, the world was not culturally ready for widespread remote work. Then, COVID-19 forced offices closed and employees adapted. These startups are betting that with the mass adaptation will come another cultural shift, one that could bring the metaverse into mainstream.

Powered by WPeMatico

It takes a bold vision and nerves of steel to venture into outer space. The same holds true for the pioneering startups forging the future of space technology. Connect with other bold visionaries at TC Sessions: Space 2020 to go farther and faster together.

If you want to go farther and faster for less, you have only three more days to take advantage of early-bird pricing. Purchase your ticket ($125) before the early-bird launch window closes on 11.13.20 at 11:59 p.m. PST and keep $100 in your wallet.

Looking for more ways to save? We offer discounts for groups, students and current employees in government, the military and nonprofits. Want to increase your brand recognition on a global scale? Exhibit in the expo with a Space Startup Exhibitor Package. The package includes three passes, and exhibitors get to pitch live to attendees around the world. Pro Tip: Hit record right before you pitch — it makes a great learning or marketing tool.

Wondering whether a virtual conference measures up? Here’s what Katia Paramonova, founder and CEO of Centrly, says about the real benefits she found by going virtual with TechCrunch:

“I really enjoyed the virtual experience. I didn’t have to be there 24/7 or spend money on a flight, and I still could get work done in the afternoon. The platform was convenient and flexible. If wanted to attend simultaneous sessions, I could easily toggle between them.”

Your ticket to TC Sessions: Space also includes video on demand, which means you won’t have to miss a minute of expert insight, tips and trend spotting from the top founders, investors, technologists, government officials and military minds across public, private and defense sectors.

You’ll find panel discussions, interviews, fireside chats and interactive Q&As on range of topics: mineral exploration, global mapping of the Earth from space, deep tech software, defense capabilities, 3D-printed rockets and the future of agriculture and food technology. Don’t miss the breakout sessions dedicated to accessing grant money. Explore the event agenda now and get a jump on organizing your schedule.

Nothing moves faster than tech, and keeping pace won’t chart a flightpath to success. It requires a prescience that comes from a deep understanding of the industry, the players and the possibilities. Or as Jeff Johnson, vice president of enterprise sales and solutions at FlashParking, puts it:

“Attending TC Sessions helps us keep an eye on what’s coming around the corner. It uncovers crucial trends so we can identify what we should be thinking about before anyone else.”

TC Sessions: Space 2020 takes flight December 16-17, but you have just three days left to take advantage of the early bird special. Be a bold visionary and go farther together — for less. Buy your pass before the deadline hits on 11.13.20 at 11:59 p.m. PST).

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico

When Zoom announced Zapps last month — the name has since been wisely changed to Zoom Apps — VC Twitter immediately began speculating that Zoom could make the leap from successful video conferencing service to becoming a launching pad for startup innovation. It certainly caught the attention of former TechCrunch writer and current investor at Signal Fire Josh Constine, who tweeted that “Zoom’s new ‘Zapps’ app platform will crush or king-make lots of startups.”

As Zoom usage exploded during the pandemic and it became a key tool for business and education, the idea of using a video conferencing platform to build a set of adjacent tooling makes a lot of sense. While the pandemic will come to an end, we have learned enough about remote work that the need for tools like Zoom will remain long after we get the all-clear to return to schools and offices.

We are already seeing promising startups like Mmhmm, Docket and ClassEdu built with Zoom in mind, and these companies are garnering investor attention. In fact, some investors believe Zoom could be the next great startup ecosystem.

Salesforce paved the way for Zoom more than a decade ago when it opened up its platform to developers and later launched the AppExchange as a distribution channel. Both were revolutionary ideas at the time. Today we are seeing Zoom building on that.

Jim Scheinman, founding managing partner at Maven Ventures and an early Zoom investor (who is credited with naming the company) says he always saw the service as potentially a platform play. “I’ve been saying publicly, before anyone realized it, that Zoom is the next great open platform on which to build billion-dollar businesses,” Scheinman told me.

He says he talked with Zoom leadership about opening up the platform to external developers several years ago before the IPO. It wasn’t really a priority at that point, but COVID-19 pushed the idea to the forefront. “Post-IPO and COVID, with the massive growth of Zoom on both the enterprise and consumer side, it became very clear that an app marketplace is now a critical growth area for Zoom, which creates a huge opportunity for nascent startups to scale,” he said.

Jason Green, founder and managing director at Emergence Capital (another early investor in Zoom and Salesforce) agreed: “Zoom believes that adding capabilities to the core Zoom platform to make it more functional for specific use cases is an opportunity to build an ecosystem of partners similar to what Salesforce did with AppExchange in the past.”

Before a platform can succeed with developers, it requires a critical mass of users, a bar that Zoom has clearly passed. It also needs a set of developer tools to connect to the various services on the platform. Then the substantial user base acts as a ready market for the startup. Finally, it requires a way to distribute those creations in a marketplace.

Zoom has been working on the developer components and brought in industry veteran Ross Mayfield, who has been part of two collaboration startups in his career, to run the developer program. He says that the Zoom Apps development toolset has been designed with flexibility to allow developers to build applications the way that they want.

For starters, Zoom has created WebViews, a way to embed functionality into an application like Zoom. To build WebViews in Zoom, the company created a JS Kit, which in combination with existing Zoom APIs enables developers to build functionality inside the Zoom experience. “So we’re giving developers a lot of flexibility in what experience they create with WebViews plus using our very rich set of API’s that are part of the existing platform and creating some new API’s to create the experience,” he said.

Powered by WPeMatico

As IBM transitions from software and services to a company fully focussed on hybrid cloud management, it announced its intention to buy Instana, an applications performance management startup with a cloud native approach that fits firmly within that strategy.

The companies did not reveal the purchase price.

With Instana, IBM can build on its internal management tools, giving it a way to monitor containerized environments running Kubernetes. It hopes by adding the startup to the fold it can give customers a way to manage complex hybrid and multi-cloud environments.

“Our clients today are faced with managing a complex technology landscape filled with mission-critical applications and data that are running across a variety of hybrid cloud environments – from public clouds, private clouds and on-premises,” Rob Thomas, senior vice president for cloud and data platform said in a statement. He believes Instana will help ease that load, while using machine learning to provide deeper insights.

At the time of the company’s $30 million Series C in 2018, TechCrunch’s Frederic Lardinois described the company this way. “What really makes Instana stand out is its ability to automatically discover and monitor the ever-changing infrastructure that makes up a modern application, especially when it comes to running containerized microservices.” That would seem to be precisely the type of solution that IBM would be looking for.

As for Instana, the founders see a good fit for the two companies, especially in light of the Red Hat acquisition in 2018 that is core to IBM’s hybrid approach. “The combination of Instana’s next generation APM and Observability platform with IBM’s Hybrid Cloud and AI technologies excited me from the day IBM approached us with the idea of joining forces and combining our technologies,” CEO Mirko Novakovic wrote in a blog post announcing the deal.

Indeed, in a recent interview IBM CEO Arvind Krishna told CNBC’s Jon Fortt, that they are betting the farm on hybrid cloud management with Red Hat at the center. When you combine that with the decision to spin out the company’s managed infrastructure services business, this purchase shows that they intend to pursue every angle

“The Red Hat acquisition gave us the technology base on which to build a hybrid cloud technology platform based on open-source, and based on giving choice to our clients as they embark on this journey. With the success of that acquisition now giving us the fuel, we can then take the next step, and the larger step, of taking the managed infrastructure services out. So the rest of the company can be absolutely focused on hybrid cloud and artificial intelligence,” Krishna told CNBC.

Instana, which is based in Chicago with offices in Munich, was founded in 2015 in the early days of Kubernetes and the startup’s APM solution has evolved to focus more on the needs of monitoring in a cloud native environment. The company raised $57 million along the way with the most recent round being that Series C in 2018.

The deal per usual is subject to regulatory approvals, but the company believes it should close in the next few months.

Powered by WPeMatico

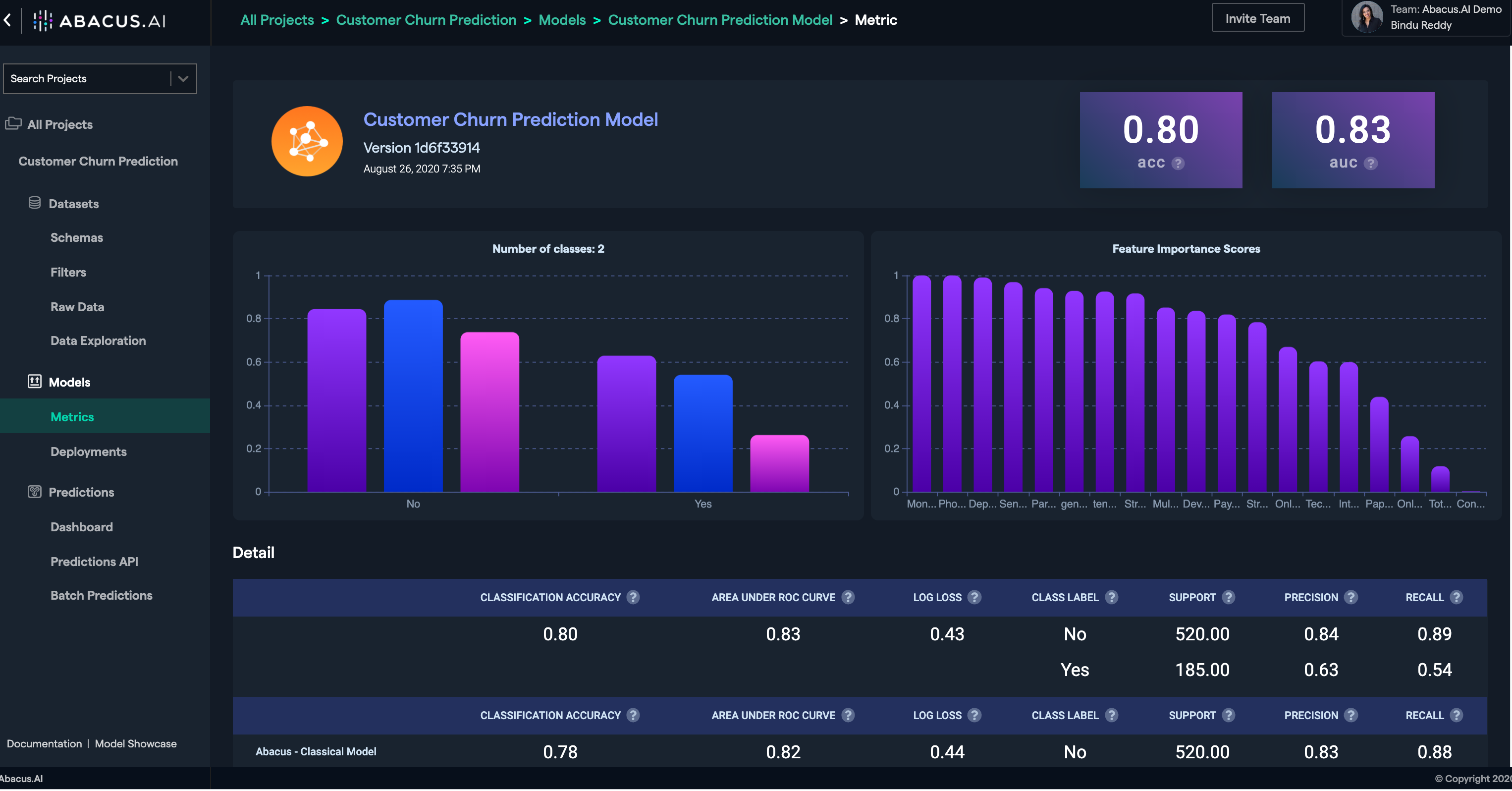

AI startup RealityEngines.AI changed its name to Abacus.AI in July. At the same time, it announced a $13 million Series A round. Today, only a few months later, it is not changing its name again, but it is announcing a $22 million Series B round, led by Coatue, with Decibel Ventures and Index Partners participating as well. With this, the company, which was co-founded by former AWS and Google exec Bindu Reddy, has now raised a total of $40.3 million.

Abacus co-founder Bindu Reddy, Arvind Sundararajan and Siddartha Naidu. Image Credits: Abacus.AI

In addition to the new funding, Abacus.AI is also launching a new product today, which it calls Abacus.AI Deconstructed. Originally, the idea behind RealityEngines/Abacus.AI was to provide its users with a platform that would simplify building AI models by using AI to automatically train and optimize them. That hasn’t changed, but as it turns out, a lot of (potential) customers had already invested into their own workflows for building and training deep learning models but were looking for help in putting them into production and managing them throughout their lifecycle.

“One of the big pain points [businesses] had was, ‘look, I have data scientists and I have my models that I’ve built in-house. My data scientists have built them on laptops, but I don’t know how to push them to production. I don’t know how to maintain and keep models in production.’ I think pretty much every startup now is thinking of that problem,” Reddy said.

Image Credits: Abacus.AI

Since Abacus.AI had already built those tools anyway, the company decided to now also break its service down into three parts that users can adapt without relying on the full platform. That means you can now bring your model to the service and have the company host and monitor the model for you, for example. The service will manage the model in production and, for example, monitor for model drift.

Another area Abacus.AI has long focused on is model explainability and de-biasing, so it’s making that available as a module as well, as well as its real-time machine learning feature store that helps organizations create, store and share their machine learning features and deploy them into production.

As for the funding, Reddy tells me the company didn’t really have to raise a new round at this point. After the company announced its first round earlier this year, there was quite a lot of interest from others to also invest. “So we decided that we may as well raise the next round because we were seeing adoption, we felt we were ready product-wise. But we didn’t have a large enough sales team. And raising a little early made sense to build up the sales team,” she said.

Reddy also stressed that unlike some of the company’s competitors, Abacus.AI is trying to build a full-stack self-service solution that can essentially compete with the offerings of the big cloud vendors. That — and the engineering talent to build it — doesn’t come cheap.

Image Credits: Abacus.AI

It’s no surprise then that Abacus.AI plans to use the new funding to increase its R&D team, but it will also increase its go-to-market team from two to ten in the coming months. While the company is betting on a self-service model — and is seeing good traction with small- and medium-sized companies — you still need a sales team to work with large enterprises.

Come January, the company also plans to launch support for more languages and more machine vision use cases.

“We are proud to be leading the Series B investment in Abacus.AI, because we think that Abacus.AI’s unique cloud service now makes state-of-the-art AI easily accessible for organizations of all sizes, including start-ups,” Yanda Erlich, a p artner at Coatue Ventures told me. “Abacus.AI’s end-to-end autonomous AI service powered by their Neural Architecture Search invention helps organizations with no ML expertise easily deploy deep learning systems in production.”

Powered by WPeMatico

Jinx is launching a simple way to buy dog food and manage orders via text message.

The startup says it has developed “the first text-to-buy platform in the legacy pet food space,” in partnership with its investor Initialized Capital and the firm’s co-founder Alexis Ohanian (who departed earlier this year and is raising a new fund).

Jinx CEO Terri Rockovich told me that while Jinx’s most important differentiator is creating kibble and treats that are healthier and better-suited to modern dog lifestyles, the increasing competitiveness of the dog food market means that it’s also important to rethink the broader consumer experience.

“As a brand that’s committed to redefine dog nutrition … we’re required to go above and beyond in delivering a really unparalleled customer experience,” Rockovich said.

And that includes offering an easy shopping experience on our phones. Jinx provided a demo in which a user could starts a dog food purchase on the startup’s mobile website, enters their phone number for text updates, then confirms their purchase via text.

Rockovich added that since the startup’s general launch earlier this year, she’s seen subscriptions as increasingly central to Jinx’s business. (For example, a two-pound a bag of Jinx’s salmon, brown rice and sweet potato kibble normally costs $15, but you save 10% if you sign up for shipments every three weeks.)

And while the initial rollout of text-to-buy functionality is focused on the basic purchase experience, Jinx will be adding subscription management features next week, so that subscribers can make adjustments in a “seamless” way.

“We could send a push notification that says, ‘Hey, your order is going to ship in a week and arrives in a week and a half, do you want to add this product?’” Rockovich said. “Or if you want to pause your subscription indefinitely because you’re going on vacation, it’s so easy to do that via text.”

And because the underlying platform was built with Initialized, it can be used across the firm’s startup portfolio. Rockovich said the technology puts “a lot of automation at your disposal,” with chatbots that can tap into a business’ existing content library and FAQ, while also handing the conversation over to human agents when necessary.

In a statement, Ohanian said:

I’ve spent a lot of time looking at the DTC e-commerce space and as a product-builder my whole career, realized I could build a better system for all the companies in our portfolio and that there’d be no better partner to launch it than Jinx, who have consistently been at the cutting edge of the industry. [Although] there are many plug and play text-to-buy options available in the marketplace, our goal was to create a proprietary technology that offered convenience and personalization to Jinx’s customers and allowed us to hone in on consumer findings that would be valuable to all our portfolio brands.

Powered by WPeMatico

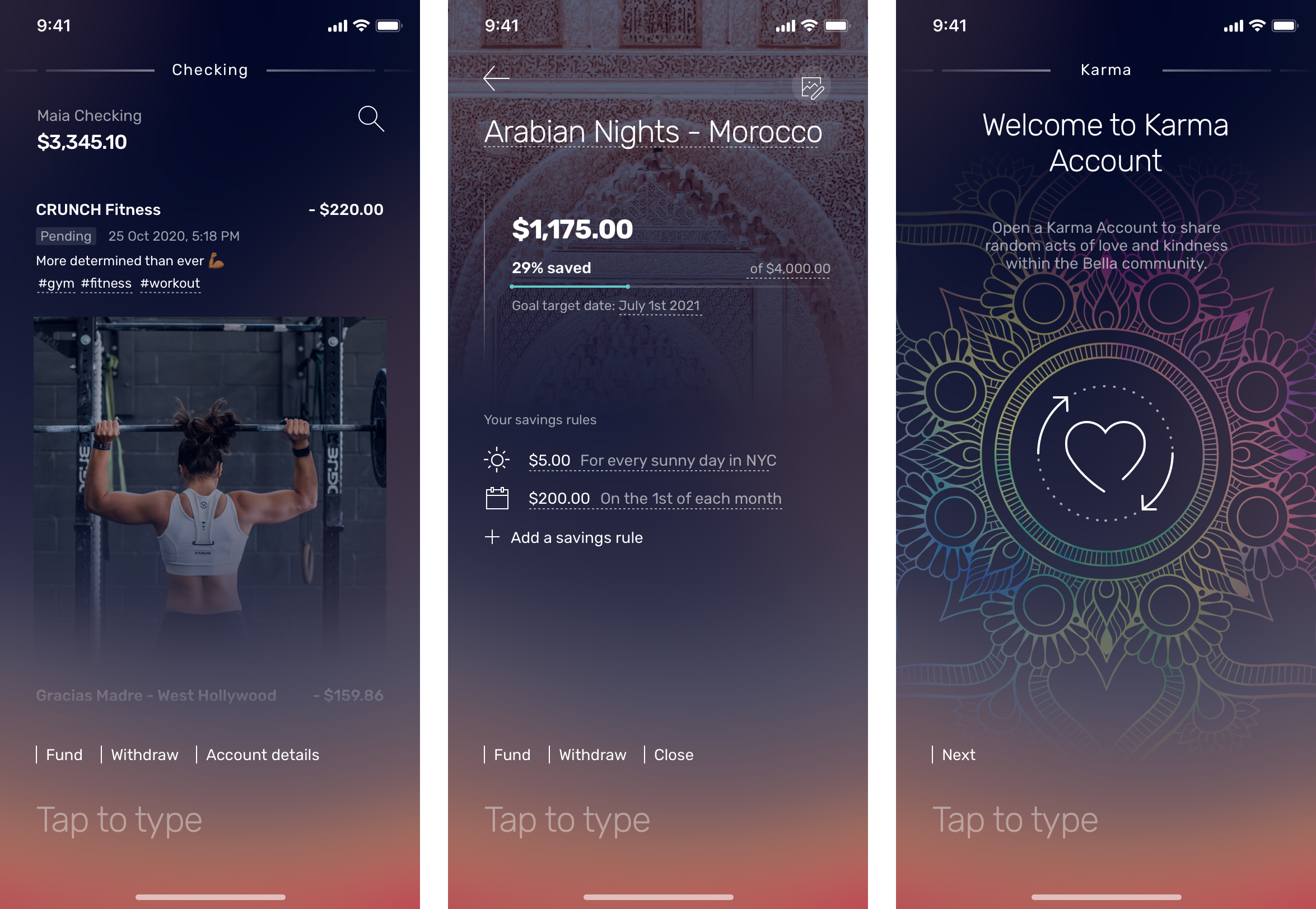

Meet Bella, a new challenger bank launching on November 30th. The company is trying to differentiate itself with two distinctive features. First, you can interact with the app using keywords and text commands. Second, Bella is trying to build a community that helps each other to differentiate its product from soulless monolithic banking services.

Let’s start with the basics. When you open a Bella account, you receive a rainbow debit card that works on the Visa network. You get a checking account as well as the ability to create savings accounts. Behind the scenes, Bella works with nbkc bank for the banking infrastructure. Accounts are FDIC insured up to $5 million.

Your card works with Apple Pay, Google Pay and Samsung Pay. There are no foreign transaction fees and Bella reimburses all ATM fees. There are no account minimums and service fees either.

Image Credits: Bella

But the app doesn’t look like your average banking app. There’s a text field at the bottom of the screen at all times. If you tap that field and enter a keyword, you can do all the interactions you’d expect to do. That feature is called Socratex.

This isn’t a chatbot, it’s more like a command line interface. For instance, if you type “Send”, it’ll suggest “Send money”. You can then enter an amount and hit next. After that, you can type the name of a contact, or add a contact, and then hit send.

You don’t have to find the right menu and hit the right button. The app tries to guide you so that you can construct a full sentence describing your intent. Bella uses LivePerson for that text-based interface. LivePerson is also Bella’s strategic backer.

Image Credits: Bella

And then, there is the Karma account. Over a hundred years ago in Naples, people started ordering two espressos and drinking just one. The second one would be a caffè sospeso. A poor person could ask for a caffè sospeso later that day and get a free coffee.

Bella is basically doing the same thing with its Karma account. Users can deposit up to $20 into a personal Karma account. Another user could use its Bella card and get a notification saying that their purchase is covered by someone else’s Karma account.

Similarly, Bella is introducing a randomized cashback program. The company randomly picks purchases and sends you back 5 to 200% in cashback.

When it comes to savings accounts, you can open as many savings accounts as you want and set some unconventional rules. For instance, you can set up a rule that puts some money aside when it’s sunny, when your sports team is winning, etc.

As you can see, Bella wants to introduce some randomized events so that you get surprised by your own bank account. The company wants to give back $1 million in cashback over the first four weeks on the market. Let’s see if that could turn the financial service into a viral experience.

Powered by WPeMatico

Creating a great customer experience requires a lot of data from a variety of sources, and pulling that disparate data together has captured the attention of companies and big and small from Salesforce and Adobe to Segment and Klaviyo. Today, Grouparoo, a new startup from three industry vets is the next company up with an open source framework designed to make it easier for developers to access and make use of customer data.

The company announced a $3 million seed investment led by Eniac Ventures and Fuel Capital with participation from Hack VC, Liquid2, SCM Advisors and several unnamed angel investors.

Grouparoo CEO and co-founder Brian Leonard says that his company has created this open source customer data framework based on his own experience and difficulty getting customer data into the various tools he has been using since he was technical founder at TaskRabbit in 2008.

“We’re an open source data framework that helps companies easily sync their customer data from their database or warehouse to all of the SaaS tools where they need it. [After you] install it, you teach it about your customers, like what properties are important in each of those profiles. And then it allows you to segment them into the groups that matter,” Leonard explained.

This could be something like high earners in San Francisco along with names and addresses. Grouparoo can grab this data and transfer it to a marketing tool like Marketo or Zendesk and these tools could then learn who your VIP customers are.

For now the company is just the three founders Leonard, CTO Evan Tahler and COO Andy Jih, and while he wasn’t ready to commit to how many people he might hire in the next 12 months, he sees it being less than 10. At this early stage, the three co-founders have already been considering how to build a diverse and inclusive company, something he helped contribute to while he was at TaskRabbit.

“So, coming from [what we built at TaskRabbit] and starting something new, it’s important to all three of us to start [building a diverse company] from the beginning, and especially combined with this notion that we’re building something open source. We’ve been talking a lot about being open about our culture and what’s important to us,” he said.

TaskRabbit also comes into play in their investment where Fuel GP Leah Solivan was also founder of TaskRabbit. “Grouparoo is solving a real and acute issue that companies grapple with as they scale — giving every member of the team access to the data they need to drive revenue, acquire customers and improve real-time decision making. Brian, Andy and Evan have developed an elegant solution to an issue we experienced firsthand at TaskRabbit,” she said.

For now the company is taking an open source approach to build a community around the tool. It is still pre-revenue, but the plan is to find a way to build something commercial on top of the open source tooling. They are considering an open core license where they can add features or support or offer the tool as a service. Leonard says that is something they intend to work out in 2021.

Powered by WPeMatico