Startups

Auto Added by WPeMatico

Auto Added by WPeMatico

Wolt, the Helsinki-based online ordering and delivery company that initially focused on restaurants but has since expanded to other verticals, has raised $530 million in new funding. The round was led by Iconiq Growth, with participation from Tiger Global, DST, KKR, Prosus, EQT Growth and Coatue.

Previous backers 83North, Highland Europe, Goldman Sachs Growth Equity, EQT Ventures and Vintage Investment Partners also followed on. The new round takes the total amount of financing Wolt has raised to $856 million. Wolt declined to disclose the company’s latest valuation, although we know from the previous D round that the company is one of Europe’s so-called unicorns.

“We operate in an extremely competitive and well-funded industry, and this round allows us to have a long-term mindset when it comes to doubling down on our different markets,” says co-founder and CEO Miki Kuusi in a statement. “Despite the turbulence of 2020, we’ve remained focused on growth, tripling our revenue to a preliminary $330 million against a net loss of just $38 million. Compared to the $670 million in new capital that we’ve raised during this year, this puts us into a strong position for investing in our people, technology, and markets when thinking about the next few years ahead”.

Since launching with 10 restaurants in its home city in 2015, five years on Wolt has expanded to 23 countries and 120 cities, mostly in Europe but also including Japan and Israel. More recently, like others in the restaurant delivery space, Wolt has expanded beyond restaurants and takeout food into the grocery and retail sectors. This, says the company, sees it offer anything from cosmetics to pet food and pharmaceuticals on its platform.

“This was mostly a primary raise,” Kuusi tells me when I ask if the new round includes secondary funding (i.e. shareholders that exited to new investors). “We’re not looking to disclose the valuation at this time, but we’ve previously shared that the Series D round that we raised in early 2020 valued the company at above €1 billion,” he adds.

Kuusi says that the latest funding round is based on the belief that local services in the offline world will gradually be brought online by players “that can execute and maintain a great customer experience”. “We started with an exclusive focus on the restaurant, as it’s the biggest local service with an underlying high-frequency use case,” he says. “We quickly learnt that the magical product market fit for bringing the restaurant online was to offer a quick and predictable delivery experience from restaurants that didn’t use to be available for delivery. We do this by handling the complexity of the delivery on the restaurant’s behalf”.

However, this was especially difficult to do efficiently and sustainably in a small and difficult home market in the Nordics. To solve this, Wolt needed to build an “optimization-heavy logistics setup for last-mile delivery” that Kuusi says lets the service operate even in “very small cities with low income disparity, limited population density and high labor costs”.

“This means that we can operate efficiently even with relatively low order volumes, enabling us to grow and expand rapidly with much less financing than some of the other players in the market. We simply had no other choice than to do it this way as we came from such a difficult home market”.

On this foundation, Wolt is expanding into other ordering and local delivery verticals, aiming to be what Kuusi dubs as “the everything app” of goods and services. “Today, Wolt is much more than a restaurant delivery service; you can order groceries, electronics, flowers, clothes and many other things on our platform,” he explains. “We believe that the future of how people buy Nike shoes is a few taps on Wolt and some 30 minutes later you get any pair of shoes brought to your door. This is what we strive to make into a reality with our team at Wolt”. (I’m an Adidas guy myself, steadfastly European.)

Asked what he thinks about all the money being pumped into the dark convenience store model, Kuusi says Wolt is investing into its own dark store operation called Wolt Market. “It’s not surprising to also see a growing amount of financing going into this sector”, he admits. “We’re huge believers in a hybrid model where there will be both offline/online retailers as well as focused online retailers in the mix. Obviously the latter category is only getting started, and we should see a massive amount of growth for the coming years ahead”.

Powered by WPeMatico

Taboola is the latest company seeking to go public via special purpose acquisition company — more commonly known as a SPAC.

To achieve this, it will merge with ION Acquisition Corp., which went public in 2020 with the aim of funding an Israeli tech acquisition (Haaretz reported last month that Taboola was in talks with ION). The transaction is expected to close in the second quarter, and the combined company will trade on the New York Stock Exchange under the ticker symbol TBLA.

Founded in 2007, Taboola powers content recommendation widgets (and advertising on those widgets) across 9,000 websites for publishers including CNBC, NBC News, Business Insider, The Independent and El Mundo. It says it reaches 516 million daily active users while working with more than 13,000 advertisers.

The company had previously planned to merge with competitor Outbrain before the deal was canceled last fall, with sources pointing to the market impact of the COVID-19 pandemic, a “challenging culture fit” and regulatory issues to explain the deal’s end.

Taboola’s founder and CEO Adam Singolda (pictured above, left) told me that this didn’t lead directly to the SPAC deal. But he said, “I always wanted to go public,” which wasn’t possible while the merger was in the works. Once that deal was called off, and with 2020 turning out to be a strong year for Taboola — it’s projecting revenue of $1.2 billion, including $375 million ex-TAC revenue (revenue after paying publishers), with over $100 million in adjusted EBITDA — the time seemed right, and ION seemed like the right partner.

“We believe Taboola is an open web recommendation leader which is well positioned to challenge the walled gardens,” said ION CEO Gilad Shany in a statement. “We were looking to merge with a global technology leader with Israeli DNA and we found that in Taboola. The combination of long-term partnerships built by the company with thousands of open web digital properties, their direct access to advertisers, massive global reach and proven AI technology, allows Taboola to provide significant value to their partners while also achieving attractive unit economics as the company grows.”

The deal will value Taboola at $2.6 billion. Through this transaction, the company plans to raise a total of $545 million, including $285 million in PIPE financing secured from Fidelity Management & Research Company, Baron Capital Group, funds and accounts managed by Hedosophia, the Federated Hermes Kaufmann Funds and others.

Singolda said that the company plans to invest $100 million in R&D this year, and that he hopes to expand the technology into areas like e-commerce and TV advertising, with the goal of moving “beyond the browser.” More broadly, he said he wants Taboola to be “a strong public company that champions the open web.”

“The open web is a $64 billion advertising market [according to Taboola estimates], but there’s no Google for the open web,” he said.

Yes, Google itself spends plenty of time talking about similar ideas, but Singolda argued that while Google has consumer products like search and YouTube that compete with other publishers for time and attention, “Taboola is not in the consumer business … We serve our partners, and it’s in our identity to drive audience growth, engagement and revenue.”

Powered by WPeMatico

Sano Genetics, a startup with a broad mission to support personalised medicine research by increasing participation in clinical trials, has raised £2.5 million in seed funding.

The round is led by Episode1 Ventures, alongside Seedcamp, Cambridge Enterprise, January Ventures and several Europe and U.S.-based angel investors. It adds to £500,000 in pre-seed funding from 2018.

Sano Genetics says part of the new capital will be to fund free at-home DNA testing kits for 3,000 people affected by Long COVID. It will also further invest in the development of its tech platform and grow the team.

Founded in 2017 by Charlotte Guzzo, Patrick Short and William Jones after they met at Cambridge University while studying genomics as postgrads, Sano Genetics has built what it describes as a “private-by-design” tech platform to help patients take part in medical research and clinical trials. This includes at-home genetic testing capabilities, and is seeing the company support research into multiple sclerosis, ankylosing spondylitis, NAFLD and ulcerative colitis2, with a research programme for Parkinson’s disease on the agenda for later in 2021.

“For participants in medical research, the process is not user friendly,” says Sano Genetics CEO Patrick Short. “There is usually little to no benefit for participants beyond altruism, taking part is difficult and time-consuming and people are also concerned about the privacy of their sensitive genetic and medical information.

“[Therefore], for researchers in biotech, pharma and academia, it is very difficult to attract and retain research participants, which adds substantial costs and time to their research. In particular for research involving genetics and precision therapies, it is doubly challenging to find the ‘right’ patients because genetic testing is not routine in the healthcare system”.

To help solve this, Sano Genetics matches relevant participants to research via its platform. It then makes participation easier by enabling at-home genetic testing and by guiding participants through the process.

“The system is designed so users know exactly what will happen with their data, and we give them straightforward ways to control their data,” explains Short. “We keep our users engaged and involved in the research process by giving them updates on the research they have been a part of, and with free personalised content including genetic reports, and stories from other people like them on our blog”.

A typical end user is someone who has a chronic or rare disease and is using the platform to take part in research that helps them personally (e.g. access to a new therapy via a clinical trial) or to help others like them.

Meanwhile, Sano Genetics generates revenue by charging biotech and pharma companies fees to find the right patients for their studies. “The typical study for us consists of a set-up fee, a per-test fee for our at-home genetic testing and analysis, and a fee for each referral we make of an interested and eligible participant to their research study,” adds the Sano Genetics CEO.

Powered by WPeMatico

The line between social networking and gaming is increasingly blurring, and internet incumbents are taking notice. NetEase, the second-largest gaming company in China (behind Tencent), is among a group of investors who just backed IMVU, an avatar-focused social network operating out of California.

Menlo Park-based Structural Capital among other institutions that also joined in the strategic round totaling $35 million. IMVU has raised more than $77 million from five rounds since it was co-founded by “The Lean Startup” author Eric Ries back in 2004. The company declined to disclose its post-money valuation.

The fresh investment will be used to fund IMVU’s product development and comes fresh off a restructuring at the company. A new parent organization called Together Labs was formed to oversee its flagship platform IMVU, in which users can create virtual rooms and chat with strangers using custom avatars, a product that’s today considered by some a dating platform; a new service called Vcoin, which lets users buy, gift, earn and convert a digital asset from the IMVU platform into fiat; and other virtual services.

“NetEase operates some of the most successful, biggest in scale, and evergreen MMO [massively multiplayer online] games in China and they see in IMVU business highlights echoing theirs,” Daren Tsui, chief executive officer at Together Labs, told TechCrunch.

“IMVU operates one of the world’s oldest, yet most vibrant and young — in terms of our user base — metaverses. We have many shared business philosophies and complementary know-how. It is a natural fit for us to become partners,” he added.

Founded in 2005, NetEase is now known for its news portal, music streaming app, education products and video games that compete with those of Tencent. It has over the years made a handful of minority investments in companies outside China, though it’s not nearly as aggressive as Tencent in terms of investment pace and volume.

A NetEase spokesperson declined to comment on the investment in IMVU.

The partnership, according to Tsui, would allow the virtual networking company to tap NetEase’s game development and engineering capabilities as well as leverage NetEase’s knowledge in global market strategy as Together Labs launches future products, including one called WithMe.

In 2020, IMVU saw record growth, with over 7 million monthly active users and 400,000 products created every month by IMVU users. The service currently has a footprint in more than 140 countries and is “always looking to expand” in existing markets, including Asia, in which it already has a localized Korean app, according to Tsui.

“With IMVU’s accelerating growth over recent years, the launch of VCOIN, and the development of the new WithMe platform, we felt timing was right to bring all of these products under a new roof to reinforce our commitment for creating authentic human connections in virtual spaces,” said the chief executive.

Powered by WPeMatico

Pula, a Kenyan insurtech startup that specialises in digital and agricultural insurance to derisk millions of smallholder farmers across Africa, has closed a Series A investment of $6 million.

The round was led by Pan-African early-stage venture capital firm, TLcom Capital, with participation from nonprofit Women’s World Banking. The raise comes after Pula closed $1 million in seed investment from Rocher Participations with support from Accion Venture Lab, Omidyar Network and several angel investors in 2018.

Founded by Rose Goslinga and Thomas Njeru in 2015, Pula delivers agricultural insurance and digital products to help smallholder farmers navigate climate risks, improve their farming practices and bolster their incomes over time.

Agriculture insurance has traditionally relied on farm business. In the U.S. or Europe with typically large farms, an average insurance premium is $1,000. But in Africa, where smallholding or small-scale farms are the norm, the number stands at an average of $4.

It is particularly telling that the value of agricultural insurance premiums in Africa represents less than 1% of the world’s total when the continent has 17% of the world’s arable land.

This disparity stems from the fact that the traditional method of calculating insurance through farm visits is often unaffordable for these smallholder farmers. Thus, they are often neglected from financial protection against climate risks like flood, drought, pestilence and hail.

Pula is solving this problem by using technology and data. Through its Area Yield Index Insurance product, the insurtech startup leverages machine learning, crop-cut experiments and data points relating to weather patterns and farmer losses, to build products that cater to various risks.

But getting farmers on board has never been easy, Goslinga told TechCrunch. According to her, Pula has understood not to sell insurance directly to small-scale farmers, because they can suffer from optimism bias. “Some think a climate disaster wouldn’t hit their farms for a particular season; hence, they don’t ask for insurance initially. But if they witness any of these climate risks during the season, they would want to get insurance, which is counterproductive to Pula,” said the founder in a phone call.

Image Credits: Pula

So the startup instead partners with banks. Banks provide loans to farmers and make it compulsory for them to have insurance. With the loan, banks can pay the insurance on behalf of the farmers at the start of the season. But at the end of the season, the farmer has to repay the loan with interest.

“The unit economics doesn’t work for us to work with farmers directly. But with banks, we know they provide loans to farmers with much better margins to pay for insurance. Also, we work together with government subsidy programs since they’re also interested in protecting their farmers.”

Through its partnerships with banks, governments and agricultural input companies, Pula is at the center of an ecosystem that provides insurance to smallholder farmers and has amassed 50 insurance partners and six reinsurance partners.

Its clientele includes the likes of the World Food Programme and Central Bank of Nigeria, as well as the Zambian and Kenyan governments. Social enterprises like One Acre Fund, startups like Apollo Agriculture and agribusiness giants like Flour Mills and Export Trading Group are also among Pula’s clients.

When Goslinga met Njeru in 2008, she worked for Syngenta Foundation for Sustainable Agriculture (SFSA). There, she started Kilimo Salama as a micro-insurance program for more than 200,000 farmers in Kenya and Rwanda. She met Njeru, who was the lead actuary at UAP Insurance, a partner to the Kilimo Salama program, at the time.

After staying with Syngenta for six years and recognising the need to provide standard insurance products for smallholder farmers, Goslinga left to start Pula with Njeru in 2015. However, it wasn’t until two years later that Njeru joined fulltime as he had a six-year engagement with Deloitte South Africa from 2012 as a consultant actuary. The pair both act as co-CEOs.

“When Thomas and I launched Pula in 2015, we had one goal in mind: to build and deliver scalable insurance solutions for Africa’s 700 million smallholder farmers,” Goslinga said. “With our latest funding, now is the time to break into new ground. In our five years since launching, we’ve built strong traction for our products. However, the fact remains that across Africa and other emerging markets, there are still millions of smallholder farmers with risks to their livelihoods that have not been covered.”

According to Goslinga, the COVID-19 pandemic helped Pula double its footprint and size as rural farming activities and operations continued despite pandemic-induced lockdowns.

Pula co-founders and Co-CEOs (Rose Goslinga and Thomas Njeru)

Therefore, the new financing will scale up operations in its existing 13 markets across Africa, where it has insured over 4.3 million farmers. They include Senegal, Ghana, Mali, Nigeria, Ethiopia, Madagascar, Tanzania, Kenya, Rwanda, Uganda, Zambia, Malawi and Mozambique. Likewise, the Kenyan startup hopes to propel its expansion for smallholder farmers in Asia and Latin America.

Pula is one of the few African startups disrupting the farming industry with technology. Its Series A investment attests that investors’ appetite for agritech startups is still on the rise.

A week ago, Aerobotics, a South African startup that uses artificial intelligence to help farmers protect their trees and fruits from risks, raised a Series B round of $17 million. Last month, SunCulture, a Kenyan startup that provides solar power systems, water pumps and irrigation systems for small-scale farmers, raised $14 million.

Another startup is Apollo Agriculture which raised $6 million Series A, akin to Pula. Not only did the pair raise the same round, Apollo Agriculture and Pula both deal with providing financial resources to smallholder farmers. But while both companies might look like competitors, even to the admission of Goslinga, she argues that the startups are partners and complement each other.

As part of the new fundraise, TLcom’s senior partner Omobola Johnson will join Pula’s board. However, it was her colleague, Maurizio Caio, the firm’s managing partner, who had something to say about the round.

“The potential for the insurance market for smallholder farmers in Africa is huge, and under the leadership of Rose and Thomas, Pula has rapidly established a strong presence throughout the continent and has several high-profile clients on their books. We are confident of Pula’s potential for growth in spite of the pandemic and look forward to partnering with them as they execute the next phase of their journey,” he said in a statement.

For the lead investor, Pula’s investment marks the culmination of its busiest run of investments having led and co-led rounds in Okra, Shara, Autochek and Ilara Health within the past year.

Christina Juhasz, CIO at Women’s World Banking, the other investor in the round, explained that the organisation cut a check for Pula “given the legions of women engaged in small-hold farming and securing the food supply for communities around the globe.”

Powered by WPeMatico

French startup Alma is raising a $59.4 million Series B funding round (€49 million). The company has been building a new payment option for expensive goods. You can choose to pay over three or four installments. This product sounds familiar if you’ve used Klarna in the past. But Klarna isn’t available in France.

Cathay Innovation, Idinvest, Bpifrance’s Large Venture fund, Seaya Ventures and Picus Capital are participating in today’s funding round. In addition to today’s equity round, Alma is raising a credit line of $25.5 million (€21 million) to finance merchant payments.

What makes Alma attractive to merchants is that the startup is handling 100% of the risk involved with a payment over multiple installments. When a customer buys a bike over four installments, they’ll get charged over several months. But the merchant gets paid on day one.

Since I first covered Alma, the startup has launched the ability to pay later. You enter your card information right now but you get charged 15 days or a month later. It can be particularly useful if you’re unsure about something you’re buying and if you think there’s a chance you’ll send it back.

And it’s an attractive option in France where debit cards are the norm — not credit cards. Alma also plans to offer longer plans, such as the ability to buy now and pay over 6, 10 or 12 installments.

Thanks to the new influx of cash, the startup plans to triple the size of its team and reach €1 billion in annual payment volume within two years. It’s also going to expand to other countries, but with a specific focus on helping French merchants reach European customers living in other European countries.

Powered by WPeMatico

German drone technology startup Wingcopter has raised a $22 million Series A – its first significant venture capital raise after mostly bootstrapping. The company, which focuses on drone delivery, has come a long way since its founding in 2017, having developed, built and flown its Wingcopter 178 heavy-lift cargo delivery drone using its proprietary and patented tilt-rotor propellant mechanism, which combines all the benefits of vertical take-off and landing with the advantages of fixed-wing aircraft for longer distance horizontal flight.

This new Series A round was led by Silicon Valley VC Xplorer Capital, as well as German growth fund Futury Regio Growth. Wingcopter CEO and founder Tom Plümmer explained to the in an interview that the addition of an SV-based investor is particularly important to the startup, since it’s in the process of preparing its entry into the U.S., with plans for an American facility, both for flight testing to satisfy FAA requirements for operational certification, as well as eventually for U.S.-based drone production.

Wingcopter has already been operating commercially in a few different markets globally, including in Vanuatu in partnership with Unicef for vaccine delivery to remote areas, in Tanzania for two-way medical supply delivery working with Tanzania, and in Ireland where it completed the world’s first delivery of insulin by drone beyond visual line of sight (BVLOS, the industry’s technical term for when a drone flies beyond the visual range of a human operator who has the ability to take control in case of emergencies).

Wingcopter CEO and co-founder Tom Plümmer. Credit: Jonas Wresch

While Wingcopter has so far pursued a business as an OEM manufacturer of drones, and has had paying customers eager to purchase its hardware effectively since day one (Plümmer told me that they had at least one customer wiring them money before they even had a bank account set up for the business), but it’s also now getting into the business of offering drone delivery-as-a-service. After doing the hard work of building its technology from the ground up, and seeking out the necessary regulatory approvals to operate in multiple markets around the world, Plümmer says that he and his co-founders realized that operating a service business not only meant a new source of revenue, but also better-served the needs of many of its potential customers.

“We learned during this process, through applying for permission, receiving these permissions and working now in five continents in multiple countries, flying BVLOS, that actually operating drones is something we are now very good at,” he said. This was actually becoming a really good source of income, and ended up actually making up more than half of our revenue at some point. Also looking at scalability of the business model of being an OEM, it’s kind of […] linear.”

Linear growth with solid revenue and steady demand was fine for Wingcopter as a bootstrapped startup founded by university students supported by a small initial investment from family and friends. But Plümmer says the company say so much potential in the technology it had developed, and the emerging drone delivery market, that the exponential growth curve of its drone delivery-as-a-service model helped make traditional VC backing make sense. In the early days, Plümmer says Wingcopter had been approached by VCs, but at the time it didn’t make sense for what they were trying to do; that’s changed.

“We were really lucky to bootstrap over the last four years,” Plümmer said. “Basically, just by selling drones and creating revenue, we could employ our first 30 employees. But at some point, you realize you want to really plan with that revenue, so you want to have monthly revenues, which generally repeat like a software business – like software as a service.”

Wingcopter 178 cargo drone performing a delivery for Merck.

Wingcopter has also established a useful hedge regarding its service business, not only by being its own hardware supplier, but also by having worked closely with many global flight regulators on their regulatory process through the early days of commercial drone flights. They’re working with the FAA on its certification process now, for instance, with Plümmer saying that they participate in weekly calls with the regulator on its upcoming certification process for BVLOS drone operators. Understanding the regulatory environment, and even helping architect it, is a major selling point for partners who don’t want to have to build out that kind of expertise and regulatory team in-house.

Meanwhile, the company will continue to act as an OEM as well, selling not only its Wingcopter 178 heavy-lift model, which can fly up to 75 miles, at speeds of up to 100 mph, and that can carry payloads up to around 13 lbs. Because of its unique tilt-rotor mechanism, it’s not only more efficient in flight, but it can also fly in much windier conditions – and take-off and land in harsher conditions than most drones, too.

Plümmer tells me that Wingcopter doesn’t intend to rest on its laurels in the hardware department, either; it’s going to be introducing a new model of drone soon, with different capabilities that expand the company’s addressable market, both as an OEM and in its drones-as-a-service business.

With its U.S. expansion, Wingcopter will still look to focus specifically on the delivery market, but Plümmer points out that there’s no reason its unique technology couldn’t also work well to serve markets including observation and inspection, or to address needs in the communication space as well. The one market that Wingcopter doesn’t intend to pursue, however, is military and defense. While these are popular customers in the aerospace and drone industries, Plümmer says that Wingcopter has a mission “to create sustainable and efficient drone solutions for improving and saving lives,” and says the startup looks at every potential customer and ensures that it aligns with its vision – which defense customers do not.

While the company has just announced the close of its Series A round, Plümmer says they’re already in talks with some potential investors to join a Series B. It’s also going to be looking for U.S. based talent in embedded systems software and flight operations testing, to help with the testing process required its certification by the FAA.

Plümmer sees a long tail of value to be built from Wingcopter’s patented tilt-rotor design, with potential applications in a range of industries, and he says that Wingcopter won’t be looking around for any potential via M&A until it has fully realized that value. Meanwhile, the company is also starting to sow the seeds of its own potential future customers, with training programs in drone flights and operations it’s putting on in partnership with UNICEF’s African Drone and Data Academy. Wingcopter clearly envisions a bright future for drone delivery, and its work in focusing its efforts on building differentiating hardware, plus the role it’s playing in setting the regulatory agenda globally, could help position it at the center of that future.

Powered by WPeMatico

Buzzy live voice chat app Clubhouse has confirmed that it has raised new funding – without revealing how much – in a Series B round led by Andreessen Horowitz through the firm’s partner Andrew Chen. The app was reported to be raising at a $1 billion valuation in a report from The Information that landed just before this confirmation. While we try to track down the actual value of this round and the subsequent valuation of the company, what we do know is that Clubhouse has confirmed it will be introducing products to help creators on the platform get played, including subscriptions, tipping and ticket sales.

This funding round will also support a ‘Creator Grant Program’ being set up by Clubhouse, which will be used to “support emerging Clubhouse creators” according to the startup’s blog post. While the app has done a remarkable job attracting creator talent, including high-profile celebrity and political users, directing revenue towards creators will definitely help spur sustained interest, as well as more time and investment from new creators who are potentially looking to make a name for themselves on the platform, similar to YouTube and TikTok influencers before them.

Of course, adding monetization for users also introduces a method for Clubhouse itself to monetize. The platform is free to all users, and doesn’t yet offer any kind of premium plan or method of charging users, nor is it ad-supported. Adding ways for users to pay other users provides an opportunity for Clubhouse to retain a cut for its services.

The plans around monetization routes for creators appear to be relatively open-ended at this point, with Clubhouse saying it’ll be launching “first tests” around each of the three areas it mentions (tipping, tickets and subscriptions) over the “next few months.” It sounds like these could be similar to something like a Patreon built right into the platform. Tickets are a unique option that would go well with Clubhouse’s more formal roundtable discussions, and could also be a way that more organizations make use of the platform for hosting virtual events.

The startup also announced that it will be starting work on its Android app (it’s been iOS only for now) and that it will also invest in more backend scaling to keep up with demand, as well as support team growth and tools for detecting and prevuing abuse. Clubhouse has come under fire for its failure in regards to moderation and prevention of abuse in the past, so this aspect of its product development will likely be closely watched. The platform will also see changes to discovery aimed at surfacing relevant users, groups (‘clubs’ in the app’s parlance) and rooms.

During a regular virtual town hall the app’s founders host on the platform, CEO Paul Davison revealed that Clubhouse now has 2 million weekly active users. It’s also worth noting that Clubhouse says it now has “over 180 investors” in the company, which is a lot for a Series B – though many of those are likely small, independent investors with very little stake.

Powered by WPeMatico

SpaceX has set a new all-time record for the most satellites launched and deployed on a single mission, with its Transporter-1 flight on Sunday. The launch was the first of SpaceX’s dedicated rideshare missions, in which it splits up the payload capacity of its rocket among multiple customers, resulting in a reduced cost for each but still providing SpaceX with a full launch and all the revenue it requires to justify lauding one of its vehicles.

The launch today included 143 satellites, 133 of which were from other companies who booked rides. SpaceX also launched 10 of its own Starlink satellites, adding to the already more than 1,000 already sent to orbit to power SpaceX’s own broadband communication network. During a launch broadcast last week, SpaceX revealed that it has begun serving beta customers in Canada and is expanding to the UK with its private pre-launch test of that service.

Customers on today’s launch included Planet Labs, which sent up 48 SuperDove Earth imaging satellites; Swarm, which sent up 36 of its own tiny IoT communications satellites, and Kepler, which added to its constellation with eight more of its own communication spacecraft. The rideshare model that SpaceX now has in place should help smaller new space companies and startups like these build out their operational on-orbit constellations faster, complementing other small payload launchers like Rocket Lab, and new entrant Virgin Orbit, to name a few.

This SpaceX launch was also the first to deliver Starlink satellites to a polar orbit, which is a key part of the company’s continued expansion of its broadband service. The mission also included a successful landing and recovery of the Falcon 9 rocket’s first-stage booster, the fifth for this particular booster, and a dual recovery of the fairing halves used to protect the cargo during launch, which were fished out of the Atlantic ocean using its recovery vessels and will be refurbished and reused.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Click here if you want it in your inbox every Saturday morning.

Ready? Let’s talk money, startups and spicy IPO rumors.

We’re shaking things up this weekend in the newsletter, focusing on a series of larger themes and news items instead of having a few discrete sections. Why? Because there was too much to fit into our usual format. If you were a fan of the original layout, we’ll be back to it next week.

Today we’re talking Coinbase’s growth, how Juked.gg tapped the equity crowdfunding market, a noodle or two on the a16z media game, Talkspace’s SPAC, VC and founder predictions for 2021, and where’s the right place to found a company.

Sound good? Let’s get into it!

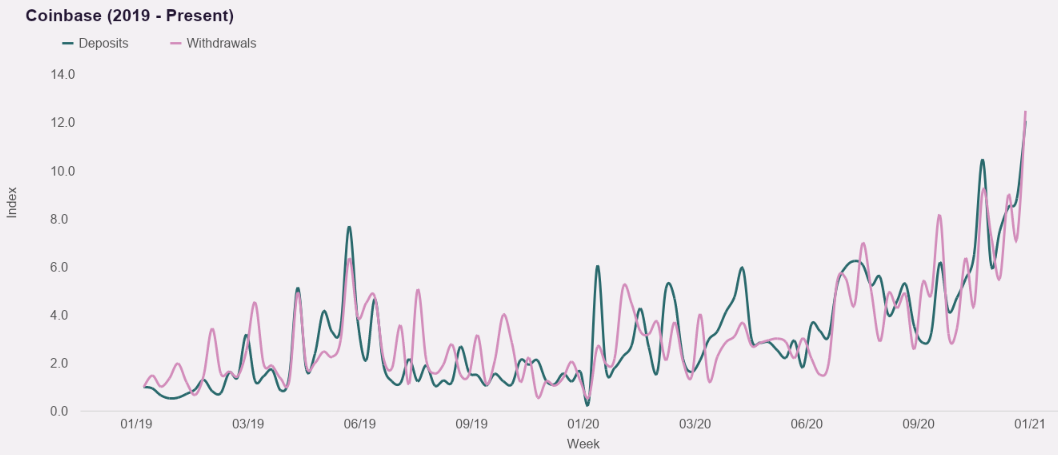

Thanks to Kazim Rizvi of Drop, parent company to Cardify which provides data on consumer spending, we have a look into how quickly deposits have scaled at American cryptocurrency platform Coinbase. As Coinbase has filed to go public, and we’re eagerly anticipating its eventual S-1 filing, we were stoked to get a directional look at how quickly consumer interest was growing for the assets it helps folks buy.

They are scaling rapidly. Using the first week of January 2019 as a baseline, by the last week of December 2020 deposits and withdrawals from Coinbase had grown by more than 12x apiece. That’s staggering growth, and while the data is somewhat volatile — and we’d treat it as directional instead of exact — on a week-to-week basis, it underscores how well companies like Coinbase may be performing as Bitcoin booms once again, bringing in more trading interest and consumer demand.

Via Cardify, Cardify data.

The Cardify data also indicates a multiplying of new customer acquisition at Coinbase over the same time period, and deposits scaling alongside the price of Bitcoin. As Bitcoin has topped the $30,000 mark recently, sharply higher than in recent quarters, the price gains may have helped Coinbase not only a solid Q4 2020, but perhaps put it on a path for a bonkers Q1 2021 as well.

If we were 10/10 excited about the Coinbase S-1 before this dataset, we’re now a heckin’ 12/10.

Esports is super cool and if you don’t agree, you are incorrect. But it doesn’t matter if you or I are right or not on the question, as the market has largely decided that competitive gaming is worth time, attention and investors’ money.

The proliferation of esports leagues and games and the like has led to a decidedly fragmented universe, however, lacking a central hub akin to what ESPN provides the world of traditional sports.

But not to worry, Juked.gg just raised capital to build a content hub for esports. This means that old folks like myself can still find out when tournaments are happening, and enjoy a dabble of League of Legends or Starcraft 2 pro play when we can, sans hunting around the internet for dates and times.

Juked.gg went through 500 Startups (more on its class here), catching our eye at the time as a neat nexus for esports-related content. Now flush with a little over $1 million that it raised on the Republic platform, it has big plans.

The Exchange spoke with Juked.gg’s co-founder and CEO Ben Goldhaber about his company’s performance to date. Per Goldhaber, Juked has scaled from 500 users when it launched in late 2019, to 50,000 in December of 2020. Ahead, Juked may invest more in journalism, more into social features, and more into user-generated content. We’ll have more on Juked as it gets its vision built, now powered by over a million dollars from 2,524 investors, each betting that the startup is building the right product to help unify a growing, if distributed, entertainment category.

To preserve our collective sanity, I’m not going to bang on at length here, but building out content at a VC firm is not new. Hell, how long ago did the First Round Review launch? What a16z appears to have in mind is different in scale, not substance. We chatted about it on Equity this week, in case you need more on the matter.

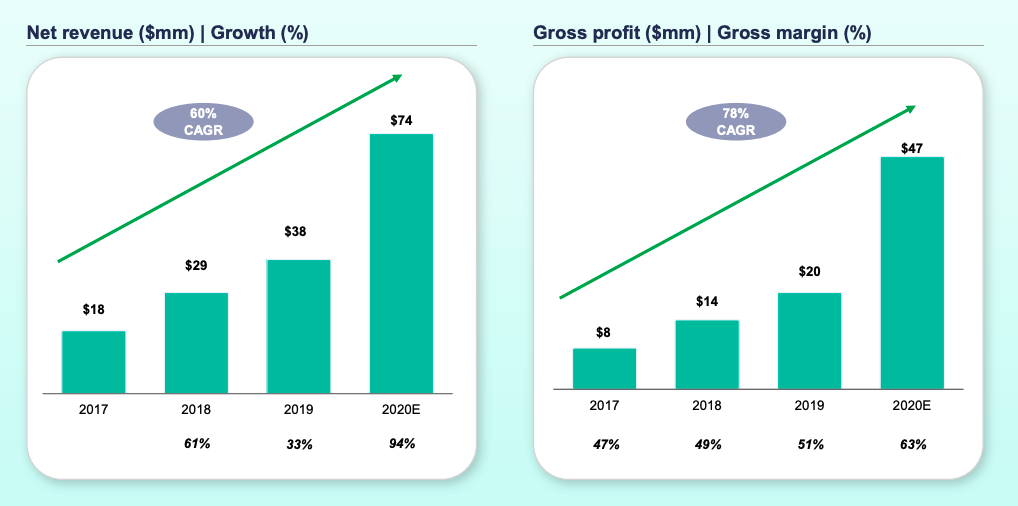

While it is enjoyable to mock SPACs, featuring as many do companies that are nascent to say the least, not all SPAC-led debuts are as silly as the rest. This is the case with the impending Talkspace deal, the deck for which you can read here.

What matters is this set of charts:

Look at that! Historical revenue growth! Improving gross margins! Rising gross profit!

You may argue that the company is not really worth an enterprise value of $1.4 billion that it will sport after its combination with Hudson Executive Investment Corp., but, hey, at least it’s a real business.

Seed VC NFX dropped a VC and founder survey the other day that I’ve been meaning to share with you. You can read the whole thing here, if you’d like.

I have two pull-outs for you this morning:

Initialized Capital put together some data on where founders think it is best to found a company. In 2020, nearly 42% of surveyed founders said the Bay Area. By 2021 that number had slipped to a little over 28%, with a plurality of 42% indicating that a distributed company is the best way to go.

I hear about this a lot from early-stage founders. They are often building what I call micro-multinationals, small companies that have a few employees in one country, and then a handful in others. Making that setup work is going to be a hotspot for HR software I reckon.

Regardless, the requirement of founding companies in the Bay Area is kaput. The advantages of founding there will linger much longer.

Coming up on The Exchange next week: The first entries of our new $50 million ARR series, featuring interviews with Assembly, SimpleNexus, Picsart, OwnBackup and others. And we have some $100 million ARR interviews in the can, as well.

Finally, to keep the The Powers That Be happy, The Exchange covered some neat stuff this week, including American VC results, fintech and unicorn venture capital, European and Asian venture capital results, how the IPO market is even more bonkers than you thought, and notes on what Qualtrics may be worth when it goes public.

Hugs, and let’s all get a nap in,

Powered by WPeMatico