SnapDeal

Auto Added by WPeMatico

Auto Added by WPeMatico

Khatabook, a startup that is helping small businesses in India record financial transactions digitally and accept payments online with an app, has raised $60 million in a new financing round as it looks to gain more ground in the world’s second most populous nation.

The new financing round, Series B, was led by Facebook co-founder Eduardo Saverin’s B Capital. A range of other new and existing investors, including Sequoia India, Partners of DST Global, Tencent, GGV Capital, RTP Global, Hummingbird Ventures, Falcon Edge Capital, Rocketship.vc and Unilever Ventures, also participated in the round, as did Facebook’s Kevin Weil, Calm’s Alexander Will, CRED’s Kunal Shah and Snapdeal co-founders Kunal Bahl and Rohit Bansal.

The one-and-a-half-year-old startup, which closed its Series A financing round in October last year and has raised $87 million to date, is now valued between $275 million to $300 million, a person familiar with the matter told TechCrunch.

Hundreds of millions of Indians came online in the last decade, but most merchants — think of neighborhood stores — are still offline in the country. They continue to rely on long notebooks to keep a log of their financial transactions. The process is also time-consuming and prone to errors, which could result in substantial losses.

Khatabook, as well as a handful of young and established players in the country, is attempting to change that by using apps to allow merchants to digitize their bookkeeping and also accept payments.

Today more than 8 million merchants from over 700 districts actively use Khatabook, its co-founder and chief executive Ravish Naresh told TechCrunch in an interview.

“We spent most of last year growing our user base,” said Naresh. And that bet has worked for Khatabook, which today competes with Lightspeed -backed OkCredit, Ribbit Capital-backed BharatPe, Walmart’s PhonePe and Paytm, all of which have raised more money than Khatabook.

The Khatabook team poses for a picture (Khatabook)

According to mobile insight firm AppAnnie, Khatabook had more than 910,000 daily active users as of earlier this month, ahead of Paytm’s merchant app, which is used each day by about 520,000 users, OkCredit with 352,000 users, PhonePe with 231,000 users and BharatPe, with some 120,000 users.

All of these firms have seen a decline in their daily active users base in recent months as India enforced a stay-at-home order for all its citizens and shut most stores and public places. But most of the aforementioned firms have only seen about 10-20% decline in their usage, according to AppAnnie.

Because most of Khatabook’s merchants stay in smaller cities and towns that are away from large cities and operate in grocery stores or work in agritech — areas that are exempted from New Delhi’s stay-at-home orders, they have been less impacted by the coronavirus outbreak, said Naresh.

Naresh declined to comment on AppAnnie’s data, but said merchants on the platform were adding $200 million worth of transactions on the Khatabook app each day.

In a statement, Kabir Narang, a general partner at B Capital who also co-heads the firm’s Asia business, said, “we expect the number of digitally sophisticated MSMEs to double over the next three to five years. Small and medium-sized businesses will drive the Indian economy in the era of COVID-19 and they need digital tools to make their businesses efficient and to grow.”

Khatabook will deploy the new capital to expand the size of its technology team as it looks to build more products. One such product could be online lending for these merchants, Naresh said, with some others exploring to solve other challenges these small businesses face.

Amit Jain, former head of Uber in India and now a partner at Sequoia Capital, said more than 50% of these small businesses are yet to get online. According to government data, there are more than 60 million small and micro-sized businesses in India.

India’s payments market could reach $1 trillion by 2023, according to a report by Credit Suisse .

Powered by WPeMatico

Many Silicon Valley companies and fintech startups in India today share a common mission: They all want to bring their financial services to the next billion users. Dozens of fintech startups that we have spoken to in recent months have told us that they all want to address much of India, one of the last great growth markets globally, in the next few years.

So you can imagine our excitement when we learned there is at least one startup that is going after just a few million users in the immediate future. We’re talking about CRED, a nine-month-old, Bangalore-based startup that is building solutions to incentivize credit card users in India to become more responsible with money and thereby improve their credit score.

CRED has raised $120 million in a Series B financing round, Kunal Shah, founder and CEO of the startup, told TechCrunch on Monday. He declined to share more information. The startup, which has raised about $145 million to date, is now valued between $430 million to $450 million, a person familiar with the matter told TechCrunch.

According to a regulatory filing, existing investors Sequoia Capital, Ribbit Capital and DST Global’s Gemini Investments led the round, with participation from Tiger Global, Hillhouse Capital, General Catalyst, Greenoaks Capital and Dragoneer.

Hundreds of millions of Indians today don’t have a credit score because they have never taken a loan from a recognized entity nor owned a credit card. According to the government’s official figures, fewer than 50 million credit cards are in circulation in India currently, with industry reports suggesting that the actual number of unique credit card holders is about half of that.

“Nobody taught us about how to use money,” Shah told TechCrunch in a recent interview. “This has created a huge trust gap in India. If you look at developed markets, systematic trust is very high between all the entities. Members don’t have to rely on third-parties. In India, even if you wanted to rent a flat, you look for brokers, for instance.”

You can build that trust when you know how someone handles their money, and how they have handled it in recent history. “Our aim is to create a big membership community with high credit worthiness, therefore open up more opportunities for them,” Shah explained.

Shah is not going after the masses. He wants to focus on just the credit card users for now, and if he could win the trust of just half of those plastic card holders in India, he would consider it a success.

“Instead of chasing the mythological mass customers who are currently useful only on paper if you wanted to boast about your daily active user or monthly active user metric, our goal is to serve the existing users,” he said.

On CRED, users are offered a range of features, including the ability to better track their spending, get reminders and check their credit score, but more importantly, access to a range of lofty offers such as membership to a gym at a discounted price, access to good restaurants at low prices and subscription to various services at little to no charge. Users can access these features by earning points, which they can secure every time they pay their credit card bills on time.

Varun Krishnan, editor of technology news site FoneArena, told TechCrunch that he has found CRED useful in getting reminders to pay his bills and likes that he can pay them through a range of payment options, including UPI apps and debit cards. “I have several cards and it is hard to track amounts and due dates of payment for each one. They send all these alerts on WhatsApp, which is a blessing,” he said.

These are the reasons that attracted many people like Krishnan to join CRED. That, and some incentive to pay his bills — though he hopes that CRED expands the range of offers it currently provides to customers.

That wish may soon come true. In the coming months, CRED will enable these highly sought-after customers to access some financial services from banks in a single-click. Additionally, it is also exploring expansion to some international markets, the aforementioned source said.

CRED does not charge users any money for joining its platform, nor for availing any of the features it offers. But it is generating revenue from some of the partners that are supplying offers on the app.

It’s not a surprise that Shah, an industry veteran known for speaking the uncomfortable truths at conferences, has won the trust of so many investors already. He built one of the biggest payment apps in India, Freecharge, and sold it to e-commerce giant Snapdeal for a whopping $400 million in one of the increasingly rare exits that India’s fintech market has seen to date.

Powered by WPeMatico

At a conference in New Delhi early last year, Netflix CEO Reed Hastings was confronted with a question that his company has been asked many times over the years. Would he consider lowering the subscription cost in India?

It’s a tactic that most Silicon Valley companies have adapted to in the country over the years. Uber rides aren’t as costly in India as they are elsewhere. Spotify and Apple Music cost less than $2 per month to users in the country. YouTube Premium as well as subscriptions to U.S. news outlets such as WSJ and New York Times are also priced significantly lower compared to the prices they charge in their home turf.

Hastings had also come prepared: He acknowledged that the entertainment viewing industry in India is very different from other parts of the world. To be sure, much of the pay-TV in India is supported by ads and the access fee remains too low ($5). But that was not going to change how Netflix likes to roll, he said.

“We want to be sensitive to great stories and to fund those great stories by investing in local content,” he said. “So yes, our strategy is to build up the local content — and of course we have got the global content — and try to uplevel the industry,” he said, identifying movie-goers who spend about Rs 500 ($7.25) or more on tickets each month as Netflix’s potential customers.

Indian commuters walking below a poster of “Sacred Games”, an original show produced by Netflix (Image: INDRANIL MUKHERJEE/AFP/Getty Images)

Less than a year and a half later, Netflix has had a change of heart. The company today rolled out a lower-priced subscription plan in India, a first for the company. The monthly plan, which restricts usage of the service to mobile devices only, is priced at Rs 199 ($2.8) — a third of the least expensive plan in the U.S.

At a press conference in New Delhi today, Netflix executives said that the lower-priced subscription tier is aimed at expanding the reach of its service in the country. “We want to really broaden the audience for Netflix, want to make it more accessible, and we knew just how mobile-centric India has been,” said Ajay Arora, Director of Product Innovation at Netflix.

The move comes at a time when Netflix has raised its subscription prices in the U.S. by up to 18% and in the UK by up to 20%.

Netflix’s strategy shift in India illustrates a bigger challenge that Silicon Valley companies have been facing in the country for years. If you want to succeed in the country, either make most of your revenue from ads, or heavily subsidize your costs.

But whether finding users in India is a success is also debatable.

Powered by WPeMatico

Truecaller, an app that helps users screen strangers and robocallers, will soon allow users in India, its largest market, to borrow up to a few hundred dollars.

The crediting option will be the fourth feature the nine-year-old app adds to its service in the last two years. So far it has added to the service the ability to text, record phone calls and mobile payment features, some of which are only available to users in India. Of the 140 million daily active users of Truecaller, 100 million live in India.

The story of the ever-growing ambition of Truecaller illustrates an interesting phase in India’s internet market that is seeing a number of companies mold their single-functioning app into multi-functioning so-called super apps.

This may sound familiar. Truecaller and others are trying to replicate Tencent’s playbook. The Chinese tech giant’s WeChat, an app that began life as a messaging service, has become a one-stop solution for a range of features — gaming, payments, social commerce and publishing platform — in recent years.

WeChat has become such a dominant player in the Chinese internet ecosystem that it is effectively serving as an operating system and getting away with it. The service maintains its own “app store” that hosts mini apps. This has put it at odds with Apple, though the iPhone-maker has little choice but to make peace with it.

For all its dominance in China, WeChat has struggled to gain traction in India and elsewhere. But its model today is prominently on display in other markets. Grab and Go-Jek in Southeast Asian markets are best known for their ride-hailing services, but have begun to offer a range of other features, including food delivery, entertainment, digital payments, financial services and healthcare.

The proliferation of low-cost smartphones and mobile data in India, thanks in part to Google and Facebook, has helped tens of millions of Indians come online in recent years, with mobile the dominant platform. The number of internet users has already exceeded 500 million in India, up from some 350 million in mid-2015. According to some estimates, India may have north of 625 million users by year-end.

This has fueled the global image of India, which is both the fastest growing internet and smartphone market. Naturally, local apps in India, and those from international firms that operate here, are beginning to replicate WeChat’s model.

Founder and chief executive officer (CEO) of Paytm Vijay Shekhar Sharma speaks during the launch of Paytm payments Bank at a function in New Delhi on November 28, 2017 (AFP PHOTO / SAJJAD HUSSAIN)

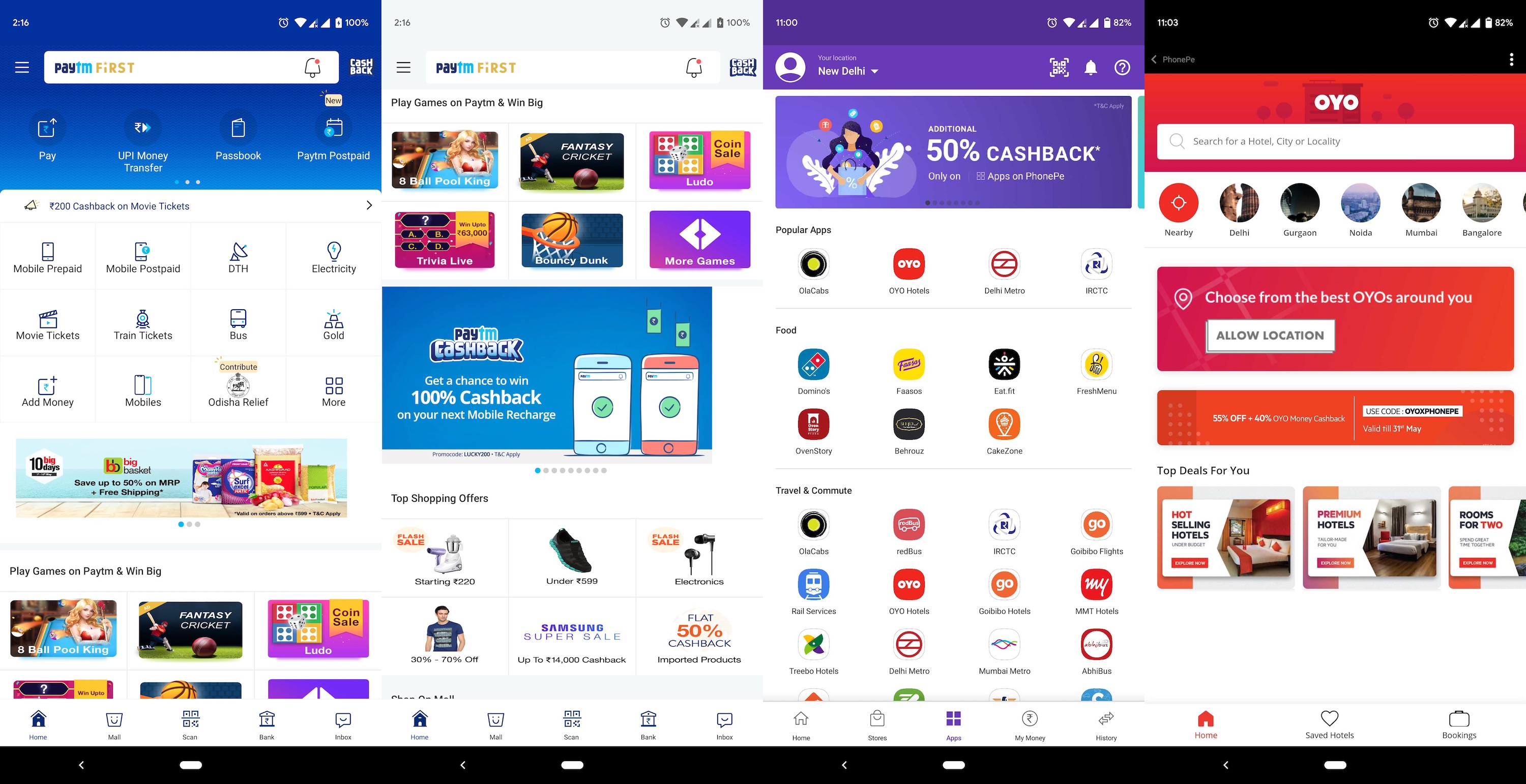

Leading that pack is Paytm, the popular homegrown mobile wallet service that’s valued at $18 billion and has been heavily backed by Alibaba, the e-commerce giant that rivals Tencent and crucially missed the mobile messaging wave in China.

In recent years, the Paytm app has taken a leaf from China with additions that include the ability to text merchants; book movie, flight and train tickets; and buy shoes, books and just about anything from its e-commerce arm Paytm Mall . It also has added a number of mini games to the app. The company said earlier this month that more than 30 million users are engaging with its games.

Why bother with diversifying your app’s offering? Well, for Vijay Shekhar Sharma, founder and CEO of Paytm, the question is why shouldn’t you? If your app serves a certain number of transactions (or engagements) in a day, you have a good shot at disrupting many businesses that generate fewer transactions, he told TechCrunch in an interview.

At the end of the day, companies want to garner as much attention of a user as they can, said Jayanth Kolla, founder and partner of research and advisory firm Convergence Catalyst.

“This is similar to how cable networks such as Fox and Star have built various channels with a wide range of programming to create enough hooks for users to stick around,” Kolla said.

“The agenda for these apps is to hold people’s attention and monopolize a user’s activities on their mobile devices,” he added, explaining that higher engagement in an app translates to higher revenue from advertising.

Paytm’s Sharma agrees. “Payment is the moat. You can offer a range of things including content, entertainment, lifestyle, commerce and financial services around it,” he told TechCrunch. “Now that’s a business model… payment itself can’t make you money.”

Other businesses have taken note. Flipkart -owned payment app PhonePe, which claims to have 150 million active users, today hosts a number of mini apps. Some of those include services for ride-hailing service Ola, hotel booking service Oyo and travel booking service MakeMyTrip.

Paytm (the first two images from left) and PhonePe offer a range of services that are integrated into their payments apps

What works for PhonePe is that its core business — payments — has amassed enough users, Himanshu Gupta, former associate director of marketing and growth for WeChat in India, told TechCrunch. He added that unlike e-commerce giant Snapdeal, which attempted to offer similar offerings back in the day, PhonePe has tighter integration with other services, and is built using modern architecture that gives users almost native app experiences inside mini apps.

When you talk about strategy for Flipkart, the homegrown e-commerce giant acquired by Walmart last year for a cool $16 billion, chances are arch rival Amazon is also hatching similar plans, and that’s indeed the case for super apps.

In India, Amazon offers its customers a range of payment features such as the ability to pay phone bills and cable subscription through its Amazon Pay service. The company last year acquired Indian startup Tapzo, an app that offers integration with popular services such as Uber, Ola, Swiggy and Zomato, to boost Pay’s business in the nation.

Another U.S. giant, Microsoft, is also aboard the super train. The Redmond-based company has added a slew of new features to SMS Organizer, an app born out of its Microsoft Garage initiative in India. What began as a texting app that can screen spam messages and help users keep track of important SMSs recently partnered with education board CBSE in India to deliver exam results of 10th and 12th grade students.

This year, the SMS Organizer app added an option to track live train schedules through a partnership with Indian Railways, and there’s support for speech-to-text. It also offers personalized discount coupons from a range of companies, giving users an incentive to check the app more often.

Like in other markets, Google and Facebook hold a dominant position in India. More than 95% of smartphones sold in India run the Android operating system. There is no viable local — or otherwise — alternative to Search, Gmail and YouTube, which counts India as its fastest growing market. But Google hasn’t necessarily made any push to significantly expand the scope of any of its offerings in India.

India is the biggest market for WhatsApp, and Facebook’s marquee app too has more than 250 million users in the nation. WhatsApp launched a pilot payments program in India in early 2018, but is yet to get clearance from the government for a nationwide rollout. (It isn’t happening for at least another two months, a person familiar with the matter said.) In the meanwhile, Facebook appears to be hatching a WeChatization of Messenger, albeit that app is not so big in India.

Ride-hailing service Ola too, like Grab and Go-Jek, plans to add financial services such as credit to the platform this year, a source familiar with the company’s plans told TechCrunch.

“We have an abundance of data about our users. We know how much money they spend on rides, how often they frequent the city and how often they order from restaurants. It makes perfect sense to give them these valued-added features,” the person said. Ola has already branched out of transport after it acquired food delivery startup Foodpanda in late 2017, but it hasn’t yet made major waves in financial services despite giving its Ola Money service its own dedicated app.

The company positioned Ola Money as a super app, expanded its features through acquisition and tie ups with other players and offered discounts and cashbacks. But it remains behind Paytm, PhonePe and Google Pay, all of which are also offering discounts to customers.

Super apps indeed come in all shapes and sizes, beyond core services like payment and transportation — the strategy is showing up in apps and services that entertain India’s internet population.

MX Player, a video playback app with more than 175 million users in India that was acquired by Times Internet for some $140 million last year, has big ambitions. Last year, it introduced a video streaming service to bolster its app to grow beyond merely being a repository. It has already commissioned the production of several original shows.

In recent months, it has also integrated Gaana, the largest local music streaming app that is also owned by Times Internet. Now its parent company, which rivals Google and Facebook on some fronts, is planning to add mini games to MX Player, a person familiar with the matter said, to give it additional reach and appeal.

Some of these apps, especially those that have amassed tens of millions of users, have a real shot at diversifying their offerings, analyst Kolla said. There is a bar of entry, though. A huge user base that engages with a product on a daily basis is a must for any company if it is to explore chasing the super app status, he added.

Indeed, there are examples of companies that had the vision to see the benefits of super apps but simply couldn’t muster the requisite user base. As mentioned, Snapdeal tried and failed at expanding its app’s offerings. Messaging service Hike, which was valued at more than $1 billion two years ago and includes WeChat parent Tencent among its investors, added games and other features to its app, but ultimately saw poor engagement. Its new strategy is the reverse: to break its app into multiple pieces.

“In 2019, we continue to double down on both social and content but we’re going to do it with an evolved approach. We’re going to do it across multiple apps. That means, in 2019 we’re going to go from building a super app that encompasses everything, to Multiple Apps solving one thing really well. Yes, we’re unbundling Hike,” Kavin Mittal, founder and CEO of Hike, wrote in an update published earlier this year.

It remains unclear how users are responding to the new features on their favorite apps. Some signs suggest, however, that at least some users are embracing the additional features. Truecaller said it is seeing tens of thousands of users try the payment feature for the first time each day. It’s also being used to send 3 billion texts a month.

Regardless, the race is still on, and there are big horses waiting to enter to add further competition.

Reliance Jio, a subsidiary of conglomerate Reliance Industry that is owned by India’s richest man, Mukesh Ambani, is planning to introduce a super app that will host more than 100 features, according to a person familiar with the matter. Local media first reported the development.

It will be fascinating to see how that works out. Reliance Jio, which almost single-handedly disrupted the telecom industry in India with its low-cost data plans and free voice calls, has amassed tens of millions of users on the bouquet of apps that it offers at no additional cost to Jio subscribers.

Beyond that diverse selection of homespun apps, Reliance has also taken an M&A-based approach to assemble the pieces of its super app strategy.

It bought music streaming service Saavn last year and quickly integrated it with its own music app JioMusic. Last month, it acquired Haptik, a startup that develops “conversational” platforms and virtual assistants, in a deal worth more than $100 million. It already has the user bases required. JioTV, an app that offers access to over 500 TV channels; and JioNews, an app that additionally offers hundreds of magazines and newspapers, routinely appear among the top apps in Google Play Store.

India’s super app revolution is in its early days, but the trend is surely one to keep an eye on as the country moves into its next chapter of internet usage.

Powered by WPeMatico

Twelve years after filing for U.S. residency, I finally took the oath of citizenship in a quaint suburban theater, having spent seven of those prime entrepreneurship years mired in the Green Card queue. This wait damages the entrepreneurship spirit and, worse, impacts career prospects, thereby crimping the economy. Our immigration system hinders entrepreneurship, innovation and productivity. Read More

Twelve years after filing for U.S. residency, I finally took the oath of citizenship in a quaint suburban theater, having spent seven of those prime entrepreneurship years mired in the Green Card queue. This wait damages the entrepreneurship spirit and, worse, impacts career prospects, thereby crimping the economy. Our immigration system hinders entrepreneurship, innovation and productivity. Read More

Powered by WPeMatico

India’s Snapdeal has been on an acquisition spree in the last several months, tapping into the $1.1 billion it has raised from the likes of Softbank to expand from being a marketplace for goods into a platform for all kinds of online transactions. The latest chapter in this story is today’s news that it has acquired a majority stake in RupeePower, a provider of loans and credit… Read More

India’s Snapdeal has been on an acquisition spree in the last several months, tapping into the $1.1 billion it has raised from the likes of Softbank to expand from being a marketplace for goods into a platform for all kinds of online transactions. The latest chapter in this story is today’s news that it has acquired a majority stake in RupeePower, a provider of loans and credit… Read More

Powered by WPeMatico

Finnish smartphone OS startup Jolla has inked the first licensing deal for its Android alternative Sailfish OS, some three years after starting out on a grand plan to save the in-house OS Nokia was abandoning in favor of Microsoft’s mobile platform.

Finnish smartphone OS startup Jolla has inked the first licensing deal for its Android alternative Sailfish OS, some three years after starting out on a grand plan to save the in-house OS Nokia was abandoning in favor of Microsoft’s mobile platform.  Xiaomi is broadening its horizons in India with news that its Mi devices will soon be available through two of the country’s major e-commerce sites, and offline retailers for the first time.

Xiaomi is broadening its horizons in India with news that its Mi devices will soon be available through two of the country’s major e-commerce sites, and offline retailers for the first time.