real estate

Auto Added by WPeMatico

Auto Added by WPeMatico

More than a year into the coronavirus pandemic, early-stage startups across the world are re-inventing how we work. But founders aren’t flocking to build just another SaaS tool or Airtable copycat — they’re trying to disrupt the only thing possibly more annoying than e-mail: the work meeting.

On an episode of this week’s podcast, Equity hosts Alex Wilhelm, Danny Crichton and Natasha Mascarenhas discussed a flurry of funding rounds related to the future of work.

Rewatch, which makes meetings asynchronous, raised $20 million from Andreessen Horowitz, AnyClip got $47 million in a round led by JVP for video search and analytics technology, Interactio, a remote interpretation platform, landed $30 million from Eight Roads Ventures and Silicon Valley-based Storm Ventures, and Spot Meetings got Kleiner Perkins on board in a $5 million seed.

We connected the dots between these funding rounds to sketch out three perspectives on the future of workplace meetings. Part of our reasoning was the uptick of investment as mentioned above, and the other is that our calendars are full of them. We all agree that the traditional meeting is broken, so below you’ll find each of our arguments on where they go next and what we’d like to see.

I’ve worked for companies that were in love with meetings, and for companies where meetings were more infrequent. I prefer the latter by a wide margin. I’ve also worked in offices full-time, half-time and fully remote. I immensely prefer the final option.

Why? Work meetings are often a waste of time. Mostly you don’t need to align, most folks taking part are superfluous and as accidental team-building exercises they are incredibly expensive in terms of human-hours.

I am not into wasting time. The more remote I’ve been and the less time I’ve spent in less-formal meetings — the usual chit-chat that pollutes productive work time, making the days longer and less useful — the more I’ve managed to get done.

But I’ve been the lucky one, frankly. Most folks were still trapped in offices up until the pandemic shook up the world of work, finally giving more companies a shot at a whole-cloth rebuild of how they toil.

The good news is that CEOs are taking note. Chatting with Sprout Social CEO Justyn Howard this week, he explained how we have a unique, new chance to not live near where we work in 2021, but to instead bring work to where we live. He’s also an introvert, which meant that as a pair we’ve found a number of positives in some of the changes to how tech and media companies operate. Perhaps we’re a little biased.

A number of startups are rushing to fill the gap between the new expectations that Howard noted and our old digital and IRL realities.

Tandem.chat might be one such company. The former Y Combinator launch-day darling has spent its post-halo period building. Its CEO sent me a manifesto of sorts the other day, discussing how his company approaches the future of work meetings. Tandem is building for a world where communication needs to be both real-time and internal; it leaves asynchronous internal communication to Slack, real-time external communications to Zoom and asynchronous external chats to email. I agree, I think.

Powered by WPeMatico

Fintech and proptech are two sectors that are seeing exploding growth in Latin America, as financial services and real estate are two categories in particular dire need of innovation in a region.

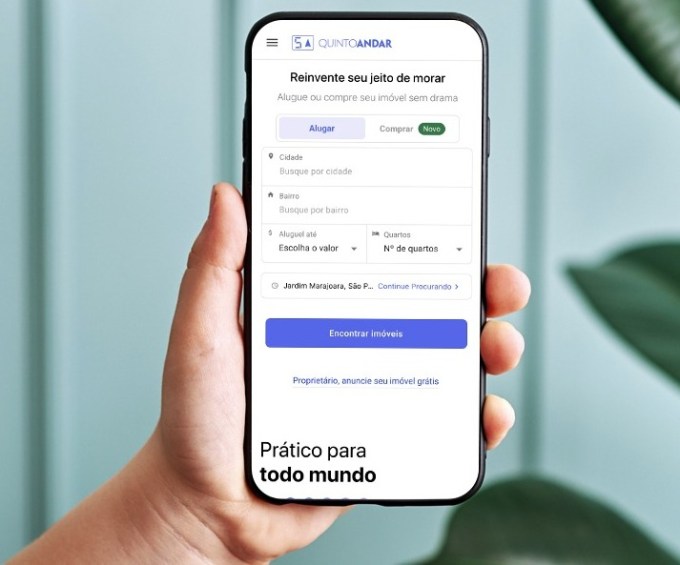

Brazil’s QuintoAndar, which has developed a real estate marketplace focused on rentals and sales, has seen impressive growth in recent years. Today, the São Paulo-based proptech has announced it has closed on $300 million in a Series E round of funding that values it at an impressive $4 billion.

The round is notable for a few reasons. For one, the valuation — high by any standards but especially for a LatAm company — represents an increase of four times from when QuintoAndar raised a $250 million Series D in September 2019.

It’s also noteworthy who is backing the company. Silicon Valley-based Ribbit Capital led its Series E financing, which also included participation from SoftBank’s LatAm-focused Innovation Fund, LTS, Maverik, Alta Park, an undisclosed U.S.-based asset manager fund with over $2 trillion in AUM, Kaszek Ventures, Dragoneer and Accel partner Kevin Efrusy.

Having backed the likes of Coinbase, Robinhood and CreditKarma, Ribbit Capital has historically focused on early-stage investments in the fintech space. Its bet on QuintoAndar represents clear faith in what the company is building, as well as its confidence in the startup’s plans to branch out from its current model into a one-stop real estate shop that also offers mortgage, title, insurance and escrow services.

The latest round brings QuintoAndar’s total raised since its 2013 inception to $635 million.

Ribbit Capital Partner Nick Huber said QuintoAndar has over the years built “a unique and trusted brand in Brazil” for those looking for a place to call home.

“Whether you are looking to buy or to rent, QuintoAndar can support customers through the entire transaction process: from browsing verified inventory to signing the final contracts,” Huber told TechCrunch. “The ability to serve customers’ needs through each phase of life and to do so from start to finish is a unique capability, both in Brazil and around the world.”

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it expanded also into connecting a home buyers to sellers.

Image Credits: QuintoAndar

TechCrunch spoke with co-founder and CEO Gabriel Braga and he shared details around the growth that has attracted such a bevy of high-profile investors.

Like most other businesses around the world, QuintoAndar braced itself for the worst when the COVID-19 pandemic hit last year — especially considering one core piece of its business is to guarantee rents to the landlords on its platform.

“In the beginning, we were afraid of the implications of the crisis but we were able to honor our commitments,” Braga said. “In retrospect, the pandemic was a big test for our business model and it has validated the strength and defensibility of our business on the credit side and reinforced our value proposition to tenants and landlords. So after the initial scary moments, we actually felt even more confident in the business that we are building.”

QuintoAndar describes itself as “a distant market leader” with more than 100,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four. Part of its plans with the new capital is to expand into new markets within Brazil, as well as in Latin America as a whole.

The startup claims that, in less than a year, QuintoAndar managed to aggregate the largest inventory among digital transactional platforms. It now offers more than 60,000 properties for sale across Sao Paulo, Rio de Janeiro, Belho Horizonte and Porto Alegre. To give greater context around the company’s growth of that side of its platform: In its first year of operation, QuintoAndar closed more than 1,000 transactions. It has now surpassed the mark of 8,000 transactions in annualized terms, growing between 50% and 100% quarter over quarter.

As for the rentals side of its business, Braga said QuintoAndar has more than 100,000 rentals under management and is closing about 10,000 new rentals per month. The company is not profitable as it’s focused on growth, although it’s unit economics are particularly favorable in certain markets such as Sao Paulo, which is financing some of its growth in other cities, according to Braga.

Now, the 2,000-person company is looking to begin its global expansion with plans to enter the Mexican market later this year. With that, Braga said QuintoAndar is looking to hire “top-tier” talent from all over.

“We want to invest a lot in our product and tech core,” he said. “So we’re trying to bring in more senior people from abroad, on a global basis.”

CEO Braga and CTO André Penha came up with the idea for QuintoAndar after receiving their MBAs at Stanford University. As many startups do, the company was founded out of Braga’s personal “nightmare” of an experience — in this case, of trying to rent an apartment in Sao Paulo.

The search process, he recalls, was difficult as there was not enough information available online and renters were forced to provide a guarantor, or co-signer, from the same city or pay rent insurance, which Braga described as “very expensive.”

“Overall, I felt it was a very inefficient and fragmented process with no transparency or tech,” Braga told me at the time of the company’s last raise. “There was all this friction and high cost involved, just real tangible problems to solve.”

The concept for QuintoAndar (which can be translated literally to “Fifth Floor” in Portuguese) was born.

“Little by little, we created a platform that consolidated supply and inventory in a uniform way,” Braga said.

The company took the search phase online for the first time, according to Braga. It also eliminated the need for tenants to provide a guarantor, thereby saving them money. On the other side, QuintoAndar also works to help protect the landlord with the guarantee that they will get their rent “on time every month,” Braga said.

It’s been interesting watching the company evolve and grow over time, just as it’s been fascinating seeing the region’s startup scene mature and shine in recent years.

Powered by WPeMatico

How are mom-and-pop self-storage facilities meant to keep up with the tech offered by the massive, ever-growing chains?

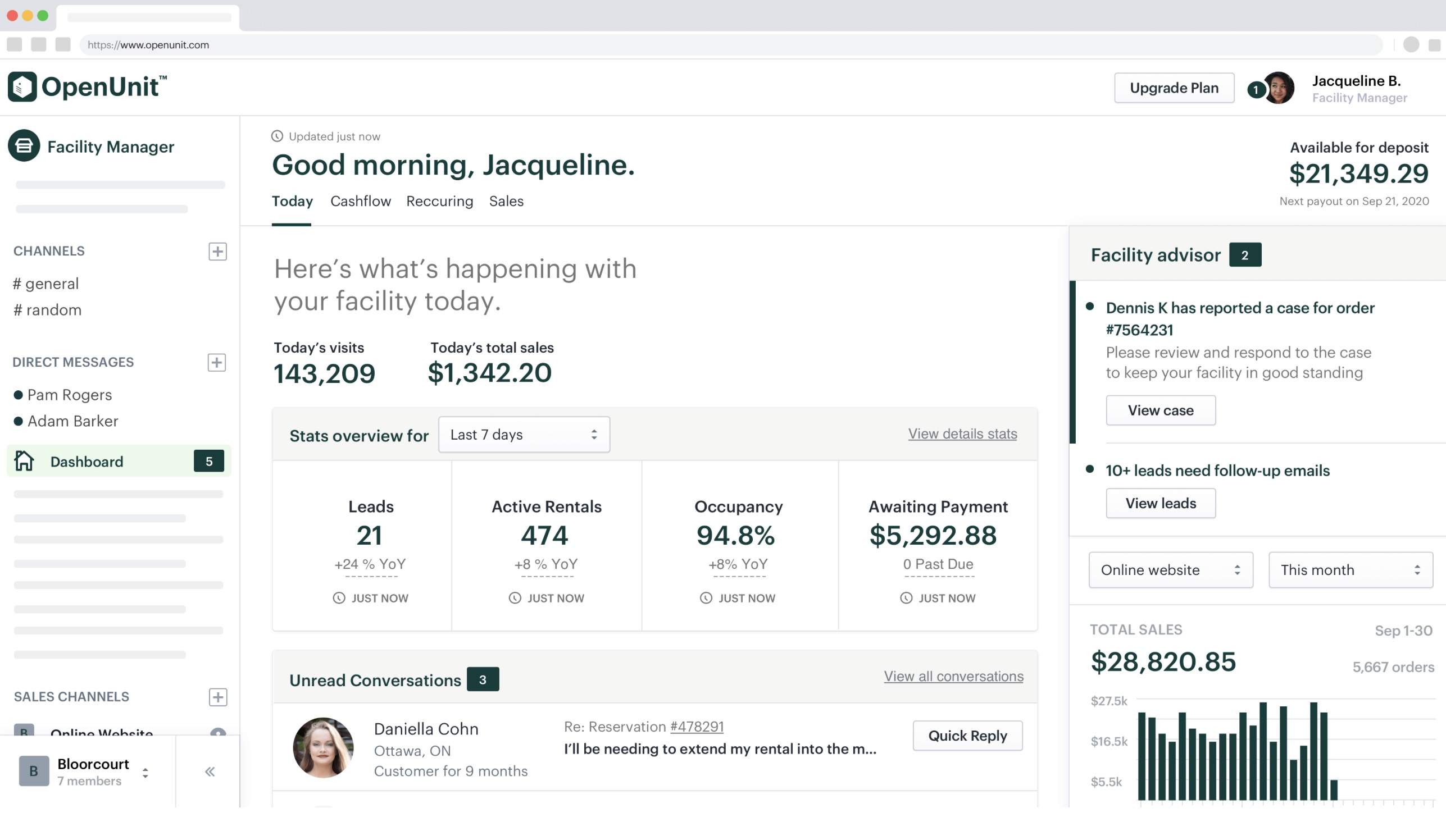

That’s a key part of the idea behind OpenUnit, a team I first wrote about in August of last year. You bring the storage units, they bring the website, payment processing and backend tools you need to manage them. They don’t charge facility owners a monthly subscription fee, instead taking a cut of each payment as the payments processor.

OpenUnit has now raised a $1 million seed round, and acquired the IP of a fellow YC company along the way.

Since we last heard from OpenUnit, they’ve been expanding to locations around the U.S. and Canada, and now have a waitlist over 800 facilities deep, the team tells me.

Image Credits: OpenUnit

OpenUnit co-founder Taylor Cooney was quick to point out that this seed round is as much about strategic partnerships as it is about the money. Neither Taylor nor co-founder Lucas Playford had much to do with the storage industry until a knock at the door led them down a rabbit hole. As I wrote back in August:

…Taylor’s landlords came to him with an offer: they wanted to sell the place he was renting, and they’d give him a stack of cash if he could be out within just a few days. Pulling that off meant finding a place to keep all of his stuff while he looked for a new home, which is when he realized how antiquated the self-storage process could be.

Of the 20+ investors participating in the round, six are from the self-storage industry, from prior/current facility owners to the director of the Canadian Self Storage Association. For some of them, it’s their first time investing in a tech or software company — but all potentially bring something to the table beyond money.

Of course, that’s not to say they’re just letting that money sit around. They’ve grown the team from just Taylor and Lucas up to five, and are still looking to grow. Meanwhile, Taylor tells me the company has acquired the IP of fellow Y Combinator W20 batchmate Affiga, a product that aimed to automatically provide insights about a new customer after a transaction is made.

Writes Taylor: “As self-storage companies move services like rentals, leases, and payments online, it’s becoming increasingly difficult for them to ‘know’ their customers. We see the integration into our product as a way to help self-storage operators bridge the gap between their online and in-store customer experiences, where the personal touch tends to be lost.”

Affiga initially shut down its operations back in 2020. After OpenUnit realized they wanted something similar in their product, they set out to buy rather than build. “With a decade in e-commerce under their belt,” Taylor tells me, “their founder had a much better approach to this then we would’ve come up with.”

So what’s next? Besides getting more people off the waitlist and onto the platform, they’re exploring other opportunities, including potentially providing loans to facilities looking to expand or renovate. Because OpenUnit is both the management platform and the payments provider, they have deep insights on how a facility is doing; they know how much a location makes, how punctual their customers are with payments, etc. Take that data and mash it up with insights on what improvements can increase revenue, and it seems like a pretty straightforward formula.

This round includes investment from Garage Capital, Advisors Fund, Insite Property Group, SquareFoot co-founder Jonathan Wasserstrum, and a number of angel investors.

Powered by WPeMatico

The public markets give, and the public markets take away. Earlier this morning, enterprise cloud storage and productivity company Box got into a more public spat with some of its shareholders upset with its performance and management decisions. But while Box endures the more difficult chapters of being a public company, other companies are racing to join the ranks of the listed concerns of the world.

If it feels like IPO news slowed for a few weeks at the start of the second quarter, your gut is correct. Investors previously told The Exchange that the first, third and fourth quarters of 2021 would be hot periods for public debuts, but that Q2 would be slower. Their argument revolved around reporting cadences and how long it takes for certain periods of accounting work to be completed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So we weren’t surprised when the second quarter’s IPO cycle began to feel a bit soft compared to the rapid-fire first quarter. And, as we’ve all heard in recent days, the great SPAC rush is slowing.

But that hasn’t stopped a number of firms from defying expectations and going public all the same. Online hosting and website builder Squarespace has not only filed but filled in its public filing with notes on its anticipated direct listing. We have to talk about its choice to list directly in light of new financial information we have concerning its recent performance.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

The final element in the current IPO landscape is the recent Darktrace IPO in the United Kingdom, which, after that market had a rough start to its tech IPO calendar, is now seeing better results. So, let’s discuss IPOs to fully understand where we stand today in the realm of unicorn liquidity.

When The Exchange first dug into Squarespace’s IPO filing, we did our best to parse its full-year results because we lacked its quarterly details. This leaves us with two things to chew on: Why is Squarespace pursuing a direct listing over another listing technique, and what can its current and more granular operating results tell us about the choice?

On the first count, if Squarespace is direct listing, we can presume that it doesn’t need more cash to operate. So, how much cash does the company have on hand? A good chunk of change: $183.3 million.

Powered by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

Farshad Yousefi and Masoud Jalali used to drive through Palo Alto neighborhoods and marvel at the outrageous home prices. But the drives sparked an idea. They were not in a financial position to purchase a home in those neighborhoods (to be clear, not many people are) either for investment or to live. But what if they could invest in homes in up and coming cities throughout the U.S.?

Then they realized that even that might be a challenge, considering that with all their student debt, affording a down payment would be impossible.

“There was nothing available out there besides a crowdfunding platform, which when we first signed up, took away $1,000 from our account that we didn’t have, and then our capital would be locked up for three to 10 years,” recalls Yousefi.

So the pair started doing research and spoke to 1,000 individuals under the age of 35. Eight out of 10 said they would like to invest in real estate but were deterred by all the barriers to entry.

“There is clearly a large demand for access to real estate,” Yousefi said. “And we wanted to give people a way to invest in it like they can in stocks, via a mobile app.”

And so the idea for Fintor was born.

Yousefi and Jalali founded the company in 2020 with the goal of purchasing homes via an LLC, and turning each into shares through an SEC-approved broker dealer. Individuals can then buy shares of the homes via Fintor’s platform. Its next step is to sign agreements with individual real estate investors or bigger real estate development firms to list their properties on the platform and give people the opportunity to buy shares.

And now Fintor has raised $2.5 million in seed money to continue building out its fractional real estate investing platform. The startup aims to “fractionalize” houses and other residential property, giving people in the U.S. access to investment opportunities “starting with as little as $5.” The company attracted the interest of investors such as 500 Startups, Hustle Fund, Graphene Ventures, Houston-based real estate investor Manny Khoshbin, Mana Ventures and other angel investors such as Cindy Bi, Skyler Fernandes, VU Venture Partners, Minal Hasan, Andrew Zalasin, Alluxo CEO and founder Safa Mahzari, SquareFoot CEO and founder Jonathan Wasserstrum and Teachable CEO and founder Ankur Nagpal.

Image Credits: Fintor

Fintor is eying markets such as Kansas City, South Carolina and Houston, where it already has some properties. It’s looking for homes in the $80,000 to $350,000 price range, and millennials and Gen Zers are its target demographic.

“Fintor can give the same return as the stock market, but at half the risk,” Yousefi said. “As two [Iranian] immigrants, we’ve seen how much this country has to offer and how real estate sits at the top of everything, yet is so inaccessible.”

The pair had originally set out to raise just $1 million but the round was quickly “way oversubscribed,” according to Yousefi, and they ended up raising $2.5 million at triple the original valuation.

Jalali said the company will use machine learning technology to filter and rate properties as it scales its business model.

“We’ll use ML to categorize neighborhoods and to come up with the price of properties to offer to potential sellers,” he added. “Our ultimate goal is to create indexes so that people can invest in multiple properties in a given city. That creates diversification right away.”

Elizabeth Yin, co-founder and general partner of Hustle Fund, believes that Fintor is solving a generational problem with real estate.

“Retail investors have almost no access to great real estate investments today and the best opportunities are reserved for the select few,” she told TechCrunch. “Not to mention that in addition to access, retail investors often need a lot of capital in order to have a diversified portfolio or be accredited to join funds.”

Fintor’s approach to securitize real estate assets will give millions of investors who are not accredited investors access they would otherwise not have had, Yin added.

“Simultaneously, it provides increased liquidity to property owners, while improving the user experience for both parties,” she said. “Effectively this becomes a new asset class, because it’s entirely turnkey and is fractionalized, which opens up many new pockets of investors.”

Powered by WPeMatico

We’ve all heard the phrase “passive income” to describe how people can make money by owning rental properties. Many Americans would love to passively earn money, but the process of becoming a landlord can be intimidating and complicated.

I mean, how many people have looked back and wished they hadn’t sold a property after seeing its value rise years after selling it?

And those who are already landlords can get overwhelmed by the complexities of managing properties.

One startup out of Boston, Knox Financial, aims to help people identify and manage residential rentals with its algorithm-based platform, and it’s raised a $10 million Series A to help it further that goal. Boston-based G20 Ventures led the round, which included participation from Greycroft, Pillar VC, 2LVC, and Gaingels.

The investment brings Knox’s total raised since its inception in 2018 to $14.7 million. The company closed on a $3 million seed round in January 2020, led by Greycroft.

Knox co-founder and CEO David Friedman is no stranger to startups. He founded Boston Logic — an integrated marketing platform and online marketing services for real estate offices and agents — in 2004. He sold that company (now under the name Propertybase) to Providence Equity for an undisclosed amount in 2016.

Knox launched its platform in March of 2019, with the goal of offering homeowners who are ready to move “a completely hands-off way” of converting a home they’re moving out of into an investment property. It also claims to help landlords more easily and efficiently manage their rentals.

At the time of its seed round early last year, the company was only operating in the Boston market and had 50 units on its platform. It’s now operating in seven states, has “hundreds” of investment properties on its platform and is overseeing a portfolio of more than $100 million.

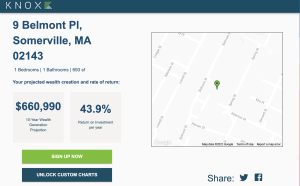

So how does it work? Once a property is enrolled on Knox’s “Frictionless Ownership Platform,” the company automates and oversees the property’s finances and taxes, insurance, leasing and legal, tenant and property care, banking and bill pay.

Knox also has developed a rental pricing and projection model for calculating the investment rate of return a property will produce over time.

Image Credits: Knox Financial

“We save investors a lot and almost always make their portfolios more profitable,” Friedman said. “If someone is moving or upsizing, we can turn properties into incredible ROI generators or cash flow.”

The company’s revenue model is simple.

“When a dollar of rent moves through our system, we keep a dime,” Friedman told TechCrunch. “We align our interests with our customers. If there’s no rent coming in, we’re not making money. Or if a tenant doesn’t pay rent, we don’t make money.”

Knox plans to use its new capital to continue expanding geographically and getting the word out to more people.

“We want to become the de facto platform for real estate investment acquisition and ownership,” Friedman said. “And we have to be coast to coast to really do that for everybody. So, we’re still very early in our growth trajectory.”

Bob Hower, co-founder and partner of G20 Ventures, shared that weeks after his college graduation, he had bought a fixer upper with his mother’s help. A week after finishing renovations, he put the house on the market. Over the subsequent five months, he gradually reduced the price as the market softened, and eventually the property sold at a small profit.

“That house now is worth a multiple of what I paid for it,” Hower recalls. “In hindsight, the mistake I made was deciding to sell the house at all.”

That experience helped Hower appreciate what he describes as a “clarity of thinking” in Knox’s business model.

“Had Knox existed decades ago, I’d likely still have that fixer-upper I bought after college,” he said. “Investing platforms such as Betterment have collapsed multiple advising and optimization activities into a simple single-sign-on service, and Knox is the first company to apply this type model to residential real estate investing.”

Powered by WPeMatico

Casa Blanca, which aims to develop a “Bumble-like app” for finding a home, has raised $2.6 million in seed funding.

Co-founder and CEO Hannah Bomze got her real estate license at the age of 18 and worked at Compass and Douglas Elliman Real Estate before launching Casa Blanca last year.

She launched the app last October with the goal of matching home buyers and renters with homes using an in-app matchmaking algorithm combined with “expert agents.” Buyers get up to 1% of home purchases back at closing. Similar to dating apps, Casa Blanca’s app is powered by a simple swipe left or right.

Samuel Ben-Avraham, a partner and early investor of Kith and an early investor in WeWork, led the round for Casa Blanca, bringing its total raise to date to $4.1 million.

The New York-based startup recently launched in the Colorado market and has seen some impressive traction in a short amount of time.

Since launching the app in October, Casa Blanca has “made more than $100M in sales” and is projected to reach $280 million this year between New York and its Denver launch.

Bomze said the app experience will be customized for each city with the goal of creating a personalized experience for each user. Casa Blanca claims to streamline and sort listings based on user preferences and lifestyle priorities.

Image Credits: Casa Blanca

“People love that there is one place to book, manage feedback, schedule and communicate with a branded agent for one cohesive experience,” Bomze said. “We have a breadth of users from first time buyers to people using our platform for $15 million listings.”

Unlike competitors, Casa Blanca applies a direct-to-consumer model, she pointed out.

“While our agents are an integral part of the company, they are not responsible for bringing in business and have more organizational support, which allows them to focus on the individual more and creates a better end-to-end experience for the consumer,” Bomze said.

Casa Blanca currently has over 38 agents in NYC and Colorado, compared to about 15 at this time last year.

“We are in a growth phase and finding a unique opportunity in this climate, in particular, because there are many women exploring new, more flexible job opportunities,” Bomze noted.

The company plans to use its new capital to continue expanding into new markets, nationally and globally; as well as enhancing its technology and scaling.

“As we continue to grow in new markets, the app experience will be curated to each city — for example, in Colorado you can edit your preferences based on access to ski areas — to make sure we’re offering a personalized experience for each user,” Bomze said.

Powered by WPeMatico

E-commerce is booming, but among the biggest challenges for entrepreneurs of online businesses are finding a place to store the items they are selling and dealing with the logistics of operating.

Tyler Scriven, Maxwell Bonnie and Paul D’Arrigo co-founded Saltbox in an effort to solve that problem.

The trio came up with a unique “co-warehousing” model that provides space for small businesses and e-commerce merchants to operate as well as store and ship goods, all under one roof. Beyond the physical offering, Saltbox offers integrated logistics services as well as amenities such as the rental of equipment and packing stations and access to items such as forklifts. There are no leases and tenants have the flexibility to scale up or down based on their needs.

“We’re in that sweet spot between co-working and raw warehouse space,” said CEO Scriven, a former Palantir executive and Techstars managing director.

Saltbox opened its first facility — a 27,000-square-foot location — in its home base of Atlanta in late 2019, filling it within two months. It recently opened its second facility, a 66,000-square-foot location, in the Dallas-Fort Worth area that is currently about 40% occupied. The company plans to end 2021 with eight locations, in particular eyeing the Denver, Seattle and Los Angeles markets. Saltbox has locations slated to come online as large as 110,000 square feet, according to Scriven.

The startup was founded on the premise that the need for “co-warehousing and SMB-centric logistics enablement solutions” has become a major problem for many new businesses that rely on online retail platforms to sell their goods, noted Scriven. Many of those companies are limited to self-storage and mini-warehouse facilities for storing their inventory, which can be expensive and inconvenient.

Scriven personally met with challenges when starting his own e-commerce business, True Glory Brands, a retailer of multicultural hair and beauty products.

“We became aware of the lack of physical workspace for SMBs engaged in commerce,” Scriven told TechCrunch. “If you are in the market looking for 10,000 square feet of industrial warehouse space, you are effectively pushed to the fringes of the real estate ecosystem and then the entrepreneurial ecosystem at large. This is costing companies in significant but untold ways.”

Now, Saltbox has completed a $10.6 million Series A round of financing led by Palo Alto-based Playground Global that included participation from XYZ Venture Capital and proptech-focused Wilshire Lane Partners in addition to existing backers Village Global and MetaProp. The company plans to use its new capital primarily to expand into new markets.

The company’s customers are typically SMB e-commerce merchants “generating anywhere from $50,000 to $10 million a year in revenue,” according to Scriven.

He emphasizes that the company’s value prop is “quite different” from a traditional flex office/co-working space.

“Our members are reliant upon us to support critical workflows,” Scriven said.

Besides e-commerce occupants, many service-based businesses are users of Saltbox’s offering, he said, such as those providing janitorial services or that need space for physical equipment. The company offers all-inclusive pricing models that include access to loading docks and a photography studio, for example, in addition to utilities and Wi-Fi.

Image Credits: Saltbox

Image Credits: Saltbox

The company secures its properties with a mix of buying and leasing by partnering with institutional real estate investors.

“These partners are acquiring assets and in most cases, are funding the entirety of capital improvements by entering into management or revenue share agreements to operate those properties,” Scriven said. He said the model is intentionally different from that of “notable flex space operators.”

“We have obviously followed those stories very closely and done our best to learn from their experiences,” he added.

Investor Adam Demuyakor, co-founder and managing partner of Wilshire Lane Partners, said his firm was impressed with the company’s ability to “structure excellent real estate deals” to help them continue to expand nationally.

He also believes Saltbox is “extremely well-positioned to help power and enable the next generation of great direct to consumer brands.”

Playground Global General Partner Laurie Yoler said the startup provides a “purpose-built alternative” for small businesses that have been fulfilling orders out of garages and self-storage units.

Saltbox recently hired Zubin Canteenwalla to serve as its chief operating officer. He joined Saltbox from Industrious, an operator co-working spaces, where he was SVP of Real Estate. Prior to Industrious, he was EVP of Operations at Common, a flexible residential living brand, where he led the property management and community engagement teams.

Powered by WPeMatico

While several tech companies are opting to delay their IPOs in the face of less-than-enthusiastic market demand for their shares, real estate tech company Compass forged ahead and went public today. After pricing its shares at $18 apiece last night, the low end of a lowered IPO price range, Compass shares closed the day up just under 12% at $20.15 apiece.

TechCrunch caught up with Compass CEO and founder Robert Reffkin to chat about his company’s debut in the market’s suddenly choppy waters for tech and tech-enabled debuts.

Regarding whether Compass is a tech company or a real estate brokerage, Reffkin — who raised the comparison himself — used the opportunity to note that companies like Amazon or Tesla aren’t only one thing. Amazon is a logistics company, an e-commerce company, a cloud-computing business and a media concern all at the same time. Price that.

The argument was good enough for Compass to sell 25 million shares — a lowered amount — at its IPO price for a gross worth $450 million. That, the CEO said, was his company’s goal for its public offering.

Sparing TechCrunch the usual CEO line about an IPO not being a destination but merely one stop on a longer journey at that juncture, Reffkin instead argued that putting nine figures of capital into his company was his objective, not a particular price or resulting valuation.

That might sound simple, but as Kaltura and Intermedia Cloud Communications have pushed their IPOs back, it’s a bit gutsy. Still, if financing was the key objective, Compass did succeed in its debut. It was even rewarded with a neat little bump in value during its first day’s trading.

Reffkin did confirm to TechCrunch what we’ve been reporting lately, namely that the IPO market has changed for the worse in recent weeks. He described it as “challenging.”

So why go public now when there is so much capital available for private companies?

Reffkin cited a few numbers, but centered his view around having what he construes as the “right team” and the “right results.” We’ll get a bit more on the latter when Compass reports its first set of public earnings.

For now, it’s a company that braved stormier seas than we might have expected to see so soon after a blistering first few months of the year for IPOs.

And because I would also bring her along if I ever took a company public, here’s the company’s founder and CEO with his mother:

Image Credits: Compass

Powered by WPeMatico