Fundings & Exits

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our week-starting primer in which we go over the latest news, dig into the week ahead, talk about some neat funding rounds and dive into the latest big news from the startup world. (You can follow the show on Twitter here, and myself here, if you are so inclined! Don’t forget to check out last Friday’s episode as well. All the cool kids are doing it.)

Some weekends are slow. This weekend was not. Here’s the round-up of news that we had to talk about:

Up ahead we have a fascinating earnings season, one that the media doesn’t expect to go very well. Stocks were up as we wrote the show, so it appears that Wall Street is more bullish than worried. We’ll see. Netflix reports later this week. Then, next week, we really get underway with Snap, IBM, Microsoft and others.

We also touched on three funding rounds: More money for cancer-focused AI startup Paige, $6.3 million for FitXR to keep working on its fitness VR work, and this small round from Russia, which reminded us that you can build a startup even in a failing democracy.

Wrapping, this earnings season is a big deal. Lots of tech investors are betting that an accelerated digital transformation is going to push most tech shops into a growth curve that makes their equity attractive, even at elevated prices. Quite a lot of capital has been sunk in this idea. We’ll see what happens when the numbers come in.

Equity drops every Monday at 7:00 a.m. PDT and Friday at 6:00 a.m. PDT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Welcome to The Exchange, an upcoming weekly newsletter featuring TechCrunch and Extra Crunch reporting on startups, money, and markets. You can sign up for it here to receive it regularly when it launches on July 25th. You can email me about it here, or talk to me about it on Twitter. Let’s go!

Ahead of parsing Q2 venture capital data, we got a look this week into the VC world’s take on making deals over Zoom. A few months ago it was an open question whether VCs would simply stop making new investments if they couldn’t chop it up in person with founders. That, it turns out, was mostly wrong.

This week we learned that most VCs are open to making remote deals happen, even if 40% of VCs have actually done so. This raises a worrying question: If only 40% of VCs have actually made a fully remote deal, how many deals happened in Q2?

Judging from my inbox over the past few months, it’s been an active period. But we can’t lean on anecdata for this topic; The Exchange will parse Q2 VC data next week, hopefully, provided that we can scrape together the data points we need to feel confident in our take. More soon.

As TechCrunch reported Friday, some startups are delaying raising capital for a few quarters. They can do this by limiting expenses. The question for startups that are doing this is what shape they’ll be in when they do surface to hunt for fresh funds; can they still grow at an attractive pace while trying to extend their runway through burn conservation?

But there’s another option besides waiting to raise a new round, and not raising at all. Startups can raise an extension to their preceding deal! Perhaps I am noticing something that isn’t a trend, or not a trend yet, but there have been a number of startups recently raised extensions lately that caught my eye. For example, this week MariaDB raised a $25 million Series C extension, for example. Also this week Sayari put together $2.5 million in a Series B extension. And CALA put together $3 million in a Seed extension. Finally, across the pond Machine Labs put together one million pounds in another Seed extension this week.

I don’t know yet how to numerically drill into the available venture data to tell if we’re really seeing an extension wave, but do let me know if you have any notes to share. And, to be completely clear, the above rounds could easily be merely random and un-thematic, so please don’t read into them more deeply than that they were announced in the last few days and match something that we’re watching.

On the public markets front, the news is all good. Tech stocks are up in general, and software stocks set some new record highs this week. It’s nearly impossible to recall how scary the world was back in March and April in today’s halcyon stock market run, but it was only a few months back that stocks were falling sharply.

The return-to-form has helped a number of companies go public this year like Vroom, Accolade, Agora, and others. This week was another busy period for startups, former startups, and other companies looking to go out.

In quick fashion to save time, this week we got to see GoHealth’s first IPO range, nCino’s second (more on the two companies’ finances here), learned that Palantir is going public (it’s financial history as best we can tell is here), and even got an IPO filing (S-1) from Rackspace, as it looks towards the public markets yet again.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, and now you can receive it in your inbox. Sign up for The Exchange newsletter, which drops every Friday starting July 25.

The IPO waters are so warm that Lemonade is still up more than 100% from its IPO price. So long as growth companies that are miles from making money can command rich valuations, expect companies to keep running through the public market’s door.

There’s fun stuff on the horizon. Coinbase might file later this year, or in early 2021. And the Airbnb IPO is probably coming within four or five quarters. Gear up to read some SEC filings.

The coolest funding round of the week was obviously the one that I wrote about, namely the $2.2 million that MonkeyLearn put together from a pair of lead investors. But other companies raised money, and among them the following investments stood out:

That’s The Exchange for the week. Keep your eye on SaaS valuations, the latest S-1 filings, and the latest fundings. Chat Monday.

Powered by WPeMatico

If you’re an angel who invested in a startup that was meant to go public in 2014, you might be getting a little bit impatient. High-risk, high-reward investing has lost its shine in this environment: the stock market is a mess these days, and you want your cash back.

Enter recapitalization events, where startups restructure their entire cap table to squeeze out old investors, bring on new ones and shift the way equity and debt is managed. For investors, it’s a killer way to enter a company on friendlier terms than normal (read: desperation), and a nice way to get liquidity on a startup you’re betting on.

For founders, it’s rarely good news, as departing investors is not a metric they’re going to add to the pitch deck. As one investor said on background, the spur of coronavirus-related recapitalization events shows “hella dilution for desperate times.”

That’s what makes Workhuman’s transparency with its recent recapitalization event all the more enticing.

Last year, the human-resources platform brought in $580 million in revenue from customers like LinkedIn, Cisco, J&J and other clients. In April, business grew 40%. Co-founder and CEO Eric Mosley says business has grown five times in size since the company pulled back from its 2014 plans to IPO. Workhuman hasn’t raised a single venture round since 2004 (and doesn’t plan to any time soon).

Being conservative has paid off; although Workhuman has operated for nearly two decades, Mosley says he thinks the company is still at the “tip of the iceberg.” The company recently had a recapitalization event to sell the stakes of its earliest investors, who cut a $200,000 check more than 20 years ago.

Powered by WPeMatico

After going private in 2016 after accepting a $32 per share, or $4.3 billion, price from Apollo Global Management, Rackspace is looking once again to the public markets. First going public in 2008, Rackspace is taking second aim at a public offering around 12 years after its initial debut.

The company describes its business as a “multicloud technology services” vendor, helping its customers “design, build and operate” cloud environments. That Rackspace is highlighting a services focus is useful context to understand its financial profile, as we’ll see in a moment.

But first, some basics. The company’s S-1 filing denotes a $100 million placeholder figure for how much the company may raise in its public offering. That figure will change, but does tell us that firm is likely to target a share sale that will net it closer to $100 million than $500 million, another popular placeholder figure.

Rackspace will list on the Nasdaq with the ticker symbol “RXT.” Goldman, Citi, J.P. Morgan, RBC Capital Markets and other banks are helping underwrite its (second) debut.

Similar to other companies that went private, only later to debut once again as a public company, Rackspace has oceans of debt.

The company’s balance sheet reported cash and equivalents of $125.2 million as of March 31, 2020. On the other side of the ledger, Rackspace has debts of $3.99 billion, made up of a $2.82 billion term loan facility, and $1.12 billion in senior notes that cost the firm an 8.625% coupon, among other debts. The term loan costs a lower 4% rate, and stems from the initial transaction to take Rackspace private ($2 billion), and another $800 million that was later taken on “in connection with the Datapipe Acquisition.”

The senior notes, originally worth a total of $1,200 million or $1.20 billion, also came from the acquisition of the company during its 2016 transaction; private equity’s ability to buy companies with borrowed money, later taking them public again and using those proceeds to limit the resulting debt profile while maintaining financial control is lucrative, if a bit cheeky.

Rackspace intends to use IPO proceeds to lower its debt-load, including both its term loan and senior notes. Precisely how much Rackspace can put against its debts will depend on its IPO pricing.

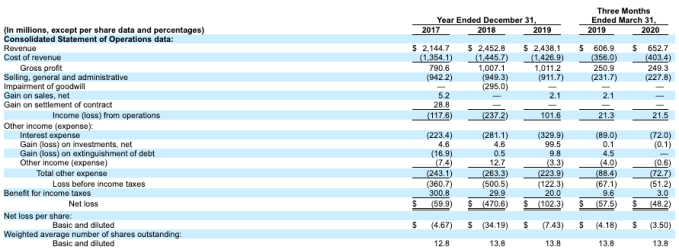

Those debts take a company that is comfortably profitable on an operating basis and make it deeply unprofitable on a net basis. Observe:

Image Credits: SEC

Looking at the far-right column, we can see a company with material revenues, though slim gross margins for a putatively tech company. It generated $21.5 million in Q1 2020 operating profit from its $652.7 million in revenue from the quarter. However, interest expenses of $72 million in the quarter helped lead Rackspace to a deep $48.2 million net loss.

Not all is lost, however, as Rackspace does have positive operating cash flow in the same three-month period. Still, the company’s multi-billion-dollar debt load is still steep, and burdensome.

Returning to our discussion of Rackspace’s business, recall that it said that it sells “multicloud technology services,” which tells us that its gross margins will be service-focused, which is to say that they won’t be software-level. And they are not. In Q1 2020 Rackspace had gross margins of 38.2%, down from 41.3% in the year-ago Q1. That trend is worrisome.

The company’s growth profile is also slightly uneven. From 2017 to 2018, Rackspace saw its revenue expand from $2.14 billion to $2.45 billion, growth of 14.4%. The company shrank slightly in 2019, falling from $2.45 billion in revenue in 2018 to $2.44 billion the next year. Given the economy that year, and the importance of cloud in 2019, the results are a little surprising.

Rackspace did grow in Q1 2020, however. The firm’s $652.7 million in first-quarter top-line easily bested in its Q1 2019 result of $606.9 million. The company grew 7.6% in Q1 2020. That’s not much, especially during a period in which its gross margins eroded, but the return-to-growth is likely welcome all the same.

TechCrunch did not see Q2 2020 results in its S-1 today while reading the document, so we presume that the firm will re-file shortly to include more recent financial results; it would be hard for the company to debut at an attractive price in the COVID-19 era without sharing Q2 figures, we reckon.

How to value Rackspace is a puzzle. The company is tech-ish, which means it will find some interest. But its slow growth rate, heavy debts and lackluster margins make it hard to pin a fair multiple onto. More when we have it.

Powered by WPeMatico

Amie, a new productivity app from ex-N26 product manager Dennis Müller, has picked up $1.3 million in pre-seed funding to “kickstart” development and hiring.

Backing 23-year-old Müller is Creandum — the European VC best known for being an early investor in Spotify — along with Tiny.VC and a plethora of angels. They include Laura Grimmelmann (Ex-Accel), Nicolas Kopp (CEO, N26 U.S.), Roland Grenke (Dubsmash co-founder) and Zachary Smith (SVP of product at U.S. challenger bank Chime).

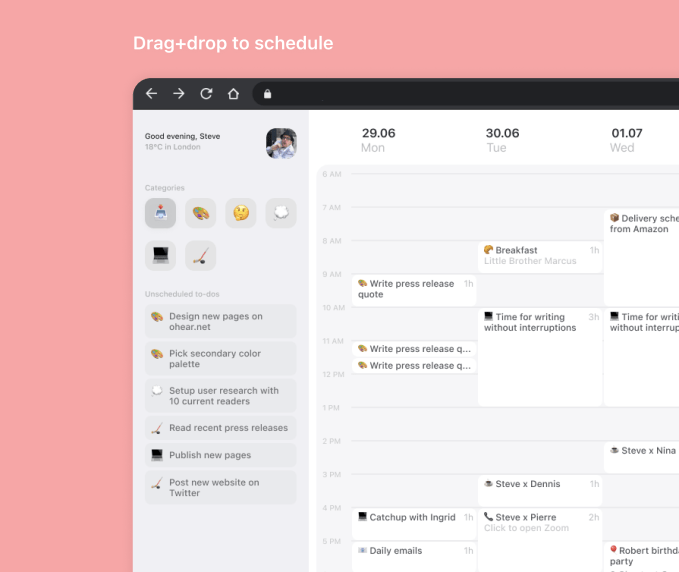

Founded early this year and with a planned launch in early 2021, Berlin-based Amie is developing a productivity app that combines a person’s calendar and to-dos in one place. Previously called coco, it promises to work across all devices, with an interface that “works just like you think.”

“Back in the day, you had a calendar on your office wall, and a to-do list on a notepad,” Müller tells me. “You could take your list with you elsewhere, but not your calendar. Those were digitized instead of rethinking the flow. Most productivity apps solve very specific problems, creating a new one, [and] users need too many tools.”

Amie pre-release app screenshot.

Müller says Amie is built on the principle that “to-dos, habits and events all take time, and all belong in the same place.” Many people already schedule to-dos and the startup wants to offer the fastest way to create to-dos, schedule events, check your calendar “and even jump into Zoom calls.”

As a glimpse of what’s to come, Amie promises to let you drag ‘n’ drop to-dos into your day, or turn links and screenshots into to-dos. “With Amie’s Alfred-like app, you can create an event and invite people in a different timezone, all while other apps are still loading,” says the young company.

More broadly, Amie wants to act as a central workspace, letting you also do things like join video calls, take notes and do email, without the need to open extra browser tabs and therefore avoid “context switching.”

“Amie will target professionals who are currently using Google Calendar, due to our integration,” adds Müller. “The waitlist already counts thousands of users, who are mostly professionals working in the tech industry (e.g., designers, developers, bizdevs, etc.”

Powered by WPeMatico

At first glance, Colvin — which recently announced that it has raised a $15 million Series B — might look like just another flower and plant delivery company, but co-founder and CEO Andres Cester said the startup has a much grander vision.

“We were born with the ambition to be the company that would redesign global flower trade,” he said.

Apparently, when Cester and his co-founder/COO Sergi Bastardas started researching the flower supply chain, they found an industry that was both “fragmented” in terms of growers and sellers, but also surprisingly centralized, with the Aalsmeer Flower Auction in the Netherlands accounting for 77% of all flower bulbs sold globally.

With all the middlemen, Cester said flowers end up being more expensive (with the growers getting a smaller share of the overall payment), and it takes longer for the flowers to reach the consumer.

So the startup created a marketplace where consumers are buying flowers straight from the growers, with Colvin as the only intermediary. That results in average savings of 50% to 100% compared to online competitors, Cester said. (For example, the bouquets featured on the Colvin homepage all cost about €33 or €34).

And while the flower business is hurting overall due to the COVID-19 pandemic, Bastardas said consumers are turning to online options, with Colvin seeing a fourfold sales increase year-over-year, and delivery volumes worth $1 million in a single day. The challenge, he said, has been making sure to deliver those flowers within the promised time window.

Image Credits: Colvin

Cester said Colvin started by selling directly to consumers because it was a good way to build the supply from growers, and that consumer sales should become a profitable, “cash-generating business.” However, the company’s big focus moving forward is building out its sales to flower wholesalers, who in turn sell to the retailers.

“We’re envisioning the B2B part of the business is going to drive most of the returns and valuation,” Bastardas added.

Colvin was founded in Spain and currently operates in Spain, Italy, Germany and Portugal. There are no plans to come to the U.S. anytime soon, but Cester said, “We believe that if we really want to … redesign how the flower industry works, we’re going to have to land in U.S. sooner or later.”

The startup has now raised a total of $27 million. The new round was led by Italian investment fund Milano Investment Partners, with participation from P101 sgr and Samaipata.

And if you’re wondering about the name, Bastardas said the company was named for civil rights pioneer Claudette Colvin, who was arrested several months before Rosa Parks in Montgomery, Alabama for refusing to give up her bus seat to a white person.

It’s an incongruous choice for a flower startup, but Bastardas said the founders took inspiration from Colvin’s story and the idea that “from several small actions, we can really change an industry.”

Powered by WPeMatico

If necessity is the mother of invention, then new business owners are getting very inventive in the ways in which they access cash. Relying on some long-tested and some new avenues to raise money, entrepreneurs are finding more ways to get public market cash faster than they would have in the past.

Whether it’s from Reg A crowdfunding dollars, Special Purpose Acquisition Companies (SPACs) or direct listings, these somewhat arcane and specialized financing vehicles are making a comeback alongside a rise in new funding mechanisms to get to market quickly and avoid the dilution that comes from private market rounds (especially since those rounds are likely to come at a reduced valuation given market conditions).

Some of these tools have existed for a while and are newly popular in an era where retail investors are driving much of the daily fluctuations of the public markets. Wall Street institutions are largely maintaining their conservative postures with regard to new offerings, so secondary market retail volume growth is outpacing institutional. Retail investors want into these new issues and are pouring into the markets, contributing to huge pops to new public offerings for companies like Lemonade this Thursday and creating an environment where SPACs and crowdfunding campaigns can flourish.

The rise of zero-commission brokerages and the popularization of fractional trading led by the startup Robinhood and adopted by every one of the major online brokers including Charles Schwab, TD Ameritrade, E-Trade and Interactive Brokers has created a stock market boom that defies the underlying market conditions in the U.S. and globally. For instance, daily trades on Robinhood are up 300% year-over-year as of March 2020.

According to data from the BATS exchange, the total trade count in the U.S. was up 71% and May trading was up more than 43% over 2019. Meanwhile, E-Trade daily average revenue trades posted a 244% increase in May over last year’s numbers.

The appetite for new issues is growing and if many of the largest venture-backed companies are holding off on going public, smaller names are using SPACs to access public capital and reach these new investors.

Powered by WPeMatico

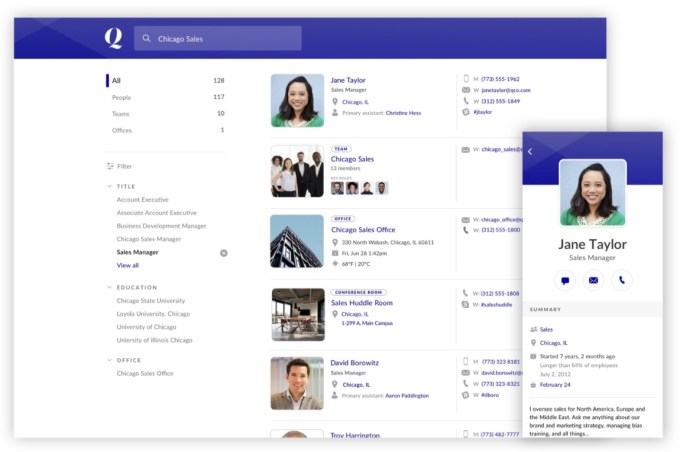

For the second time in less than 24 hours, an enterprise company bought an early-stage startup. Yesterday afternoon DocuSign acquired Liveoak, and this morning Slack announced it was buying corporate directory startup Rimeto, which should help employees find people inside the organization who match a specific set of criteria from inside Slack.

The companies did not share the purchase price.

Rimeto helps companies build directories to find employees beyond using tools like Microsoft Active Directory, homegrown tools or your corporate email program. When we covered the company’s $10 million Series A last year, we described what it brings to directories this way:

Rimeto has developed a richer directory by sitting between various corporate systems like HR, CRM and other tools that contain additional details about the employee. It of course includes a name, title, email and phone like the basic corporate system, but it goes beyond that to find areas of expertise, projects the person is working on and other details that can help you find the right person when you’re searching the directory.

In the build versus buy equation that companies balance all the time, it looks like Slack weighed the pros and cons and decided to buy. You could see how a tool like this would be useful to Slack as people try to build teams of employees, especially in a world where so many are working from home.

While the current Slack people search tool lets you search by name, role or team, Rimeto should give users a much more robust way of searching for employees across the company. You can search for the right person to help you with a particular problem and get much more granular with your search requirements than the current tool allows.

Image Credit: Rimeto

At the time of its funding announcement, the company, which was founded in 2016 by three former Facebook employees, told TechCrunch it had bootstrapped for the first three years before taking the $10 million investment last year. It also reported it was cash-flow positive at the time, which is pretty unusual for an early-stage enterprise SaaS company.

In a company blog post announcing the deal, as is typical in these deals, the founders saw being part of a larger organization as a way to grow more quickly than they could have alone. “Joining Slack is a special opportunity to accelerate Rimeto’s mission and impact with greater reach, expanded resources, and the support of Slack’s impressive global team,” the founders wrote in the post.

The acquisition is part of a continuing trend around enterprise companies buying early-stage startups to fill in holes in their product road maps.

Powered by WPeMatico

Even in the best of times, finding a notary can be a challenge. In the middle of a pandemic, it’s even more difficult. DocuSign announced it has acquired Liveoak Technologies today for approximately $38 million, giving the company an online notarization option.

At the same time, DocuSign announced a new product called DocuSign Notary, which should ease the notary requirement by allowing it to happen online along with the eSignature. As we get deeper into the pandemic, companies like DocuSign that allow workflows to happen completely digitally are in more demand than ever. This new product will be available for early access later in the summer.

The deal made sense given that the two companies had a partnership already. Liveoak brings together live video, collaboration tooling and identity verification that enables parties to get notarized approval as though you were sitting at the desk in front of the notary.

Typically, you might get a document that requires your signature. Without electronic signature, you would need to print it, sign the document, scan it and return it. If it requires a notary, you would need to sign it in the notary’s presence, which requires an in-person visit. All of this can be streamlined with an online workflow, which DocuSign is providing with this acquisition.

It’s like the perfect pandemic acquisition, making a manual process digital and saving people from having to make face-to-face transactions at a time when it can be dangerous.

Liveoak Technologies was founded in 2014 and is part of the Austin, Texas startup scene. The company raised just under $28 million during its life as a private company. The firm most recently raised $8 million at a post-money valuation of $30.4 million, according to PitchBook data. Given the amount that DocuSign paid for the startup, it appears to have gotten a bargain.

This acquisition is part of a growing pandemic acquisition trend of sorts, where larger public enterprise companies are plucking early-stage startups, in some cases for relatively bargain prices. Among the recent acquisitions are Apple buying Fleetsmith and ServiceNow acquiring Sweagle last month.

Powered by WPeMatico

OwnBackup has made a name for itself primarily as a backup and disaster recovery system for the Salesforce ecosystem, and today the company announced a $50 million investment.

Insight Partners led the round, with participation from Salesforce Ventures and Vertex Ventures. This chunk of money comes on top of a $23 million round from a year ago, and brings the total raised to more than $100 million, according to the company.

It shouldn’t come as a surprise that Salesforce Ventures chipped in when the majority of the company’s backup and recovery business involves the Salesforce ecosystem, although the company will be looking to expand beyond that with the new money.

“We’ve seen such growth over the last two and a half years around the Salesforce ecosystem, and the other ISV partners like Veeva and nCino that we’ve remained focused within the Salesforce space. But with this funding, we will expand over the next 12 months into a few new ecosystems,” company CEO Sam Gutmann told TechCrunch.

In spite of the pandemic, the company continues to grow, adding 250 new customers last quarter, bringing it to over 2,000 customers and 250 employees, according to Gutmann.

He says that raising the round, which closed at the beginning of May, had some hairy moments as the pandemic began to take hold across the world and worsen in the U.S. For a time, he began talking to new investors in case his existing ones got cold feet. As it turned out, when the quarterly numbers came in strong, the existing ones came back and the round was oversubscribed, Gutmann said.

“Q2 frankly was a record quarter for us, adding over 250 new accounts, and we’re seeing companies start to really understand how critical this is,” he said.

The company plans to continue hiring through the pandemic, although he says it might not be quite as aggressively as they once thought. Like many companies, even though they plan to hire, they are continually assessing the market. At this point, he foresees growing the workforce by about another 50 people this year, but that’s about as far as he can look ahead right now.

Gutmann says he is working with his management team to make sure he has a diverse workforce right up to the executive level, but he says it’s challenging. “I think our lower ranks are actually quite diverse, but as you get up into the leadership team, you can see on the website unfortunately we’re not there yet,” he said.

They are instructing their recruiting teams to look for diverse candidates whether by gender or ethnicity, and employees have formed a diversity and inclusion task force with internal training, particularly for managers around interviewing techniques.

He says going remote has been difficult, and he misses seeing his employees in the office. He hopes to have at least some come back before the end of the summer and slowly add more as we get into the fall, but that will depend on how things go.

Powered by WPeMatico