Fundings & Exits

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest big news, chats about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here, and myself here, and don’t forget to check out last Friday’s episode.

This morning we had a bit of a detour, wandering into the world of Big Tech to wonder what is going on with those megacorps. Too big for their own good, or too big to be good, here’s what’s up with the incumbents:

All told it seems that the biggest tech companies are busy defending their market position instead of re-earning it with great products. A good time for startups? I think so. When incumbents are busy fighting with governments, themselves and each other, it’s a great time to show up, steal a march and build neat products that take away their momentum.

On the funding front, we peeked at the neat Help Lightning round, the Agiloft investment and the Vertafore exit.

And then there was this report concerning Asana, which is growing nicely for a company of its size and could actually be cheap at its current price. Anyway, we want the company to get on with getting public so that we can read its S-1 filing. Give it to us!

All that and we had some fun, chat soon!

Equity drops every Monday at 7:00 a.m. PT and Friday at 6:00 a.m. PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

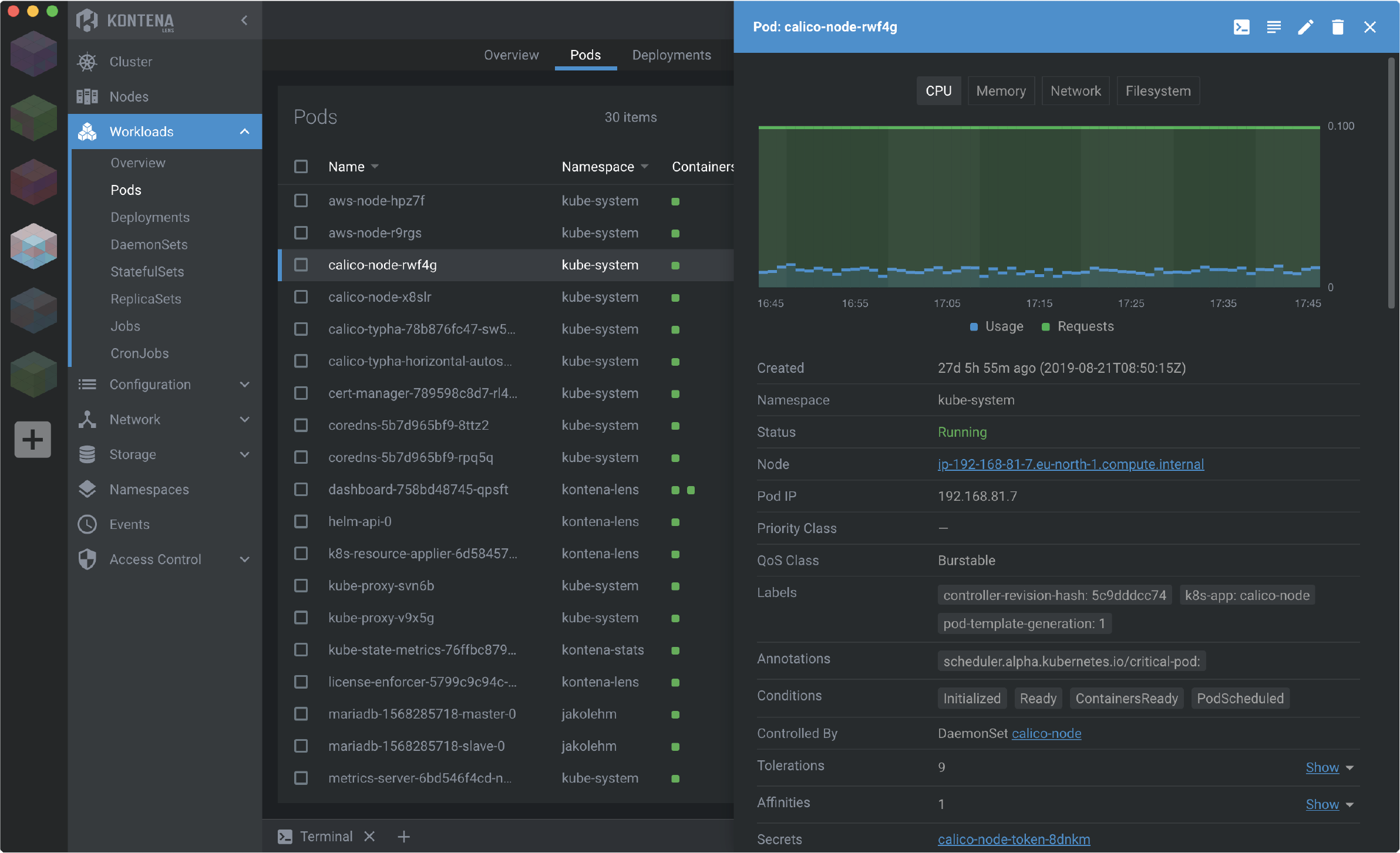

Mirantis, the company that recently bought Docker’s enterprise business, today announced that it has acquired Lens, a desktop application that the team describes as a Kubernetes-integrated development environment. Mirantis previously acquired the team behind the Finnish startup Kontena, the company that originally developed Lens.

Lens itself was most recently owned by Lakend Labs, though, which describes itself as “a collective of cloud native compute geeks and technologists” that is “committed to preserving and making available the open-source software and products of Kontena.” Lakend open-sourced Lens a few months ago.

Image Credits: Mirantis

“The mission of Mirantis is very simple: We want to be — for the enterprise — the fastest way to [build] modern apps at scale,” Mirantis CEO Adrian Ionel told me. “We believe that enterprises are constantly undergoing this cycle of modernizing the way they build applications from one wave to the next — and we want to provide products to the enterprise that help them make that happen.”

Right now, that means a focus on helping enterprises build cloud-native applications at scale and, almost by default, that means providing these companies with all kinds of container infrastructure services.

“But there is another piece of the story that’s always been going through our minds, which is, how do we become more developer-centric and developer-focused, because, as we’ve all seen in the past 10 years, developers have become more and more in charge off what services and infrastructure they’re actually using,” Ionel explained. And that’s where the Kontena and Lens acquisitions fit in. Managing Kubernetes clusters, after all, isn’t trivial — yet now developers are often tasked with managing and monitoring how their applications interact with their company’s infrastructure.

“Lens makes it dramatically easier for developers to work with Kubernetes, to build and deploy their applications on Kubernetes, and it’s just a huge obstacle-remover for people who are turned off by the complexity of Kubernetes to get more value,” he added.

“I’m very excited to see that we found a common vision with Adrian for how to incorporate Lens and how to make life for developers more enjoyable in this cloud-native technology landscape,” Miska Kaipiainen, the former CEO of Kontena and now Mirantis’ director of Engineering, told me.

He describes Lens as an IDE for Kubernetes. While you could obviously replicate Lens’ functionality with existing tools, Kaipiainen argues that it would take 20 different tools to do this. “One of them could be for monitoring, another could be for logs. A third one is for command-line configuration, and so forth and so forth,” he said. “What we have been trying to do with Lens is that we are bringing all these technologies [together] and provide one single, unified, easy to use interface for developers, so they can keep working on their workloads and on their clusters, without ever losing focus and the context of what they are working on.”

Among other things, Lens includes a context-aware terminal, multi-cluster management capabilities that work across clouds and support for the open-source Prometheus monitoring service.

For Mirantis, Lens is a very strategic investment and the company will continue to develop the service. Indeed, Ionel said the Lens team now basically has unlimited resources.

Looking ahead, Kaipiainen said the team is looking at adding extensions to Lens through an API within the next couple of months. “Through this extension API, we are actually able to collaborate and work more closely with other technology vendors within the cloud technology landscape so they can start plugging directly into the Lens UI and visualize the data coming from their components, so that will make it very powerful.”

Ionel also added that the company is working on adding more features for larger software teams to Lens, which is currently a single-user product. A lot of users are already using Lens in the context of very large development teams, after all.

While the core Lens tools will remain free and open source, Mirantis will likely charge for some new features that require a centralized service for managing them. What exactly that will look like remains to be seen, though.

If you want to give Lens a try, you can download the Windows, macOS and Linux binaries here.

Powered by WPeMatico

Michael Waxman, co-founder and CEO of dog food startup Sundays, acknowledged that dog owners have no shortage of options when it comes to feeding their beloved pets — but he still thinks there’s room for something new.

“There’s a sort of ‘Water everywhere, but not a drop to drink’ phenomenon,” Waxman said. “There are over 3,000 dog foods, and yet I think there isn’t really one that is the no-brainer, compelling answer.”

Sundays “soft launched” its first product in February and now has around 1,000 paying customers. It’s launching more broadly today and is also announcing that it has raised $2.27 million in funding from Red Sea Ventures, Box Group, Great Oaks Ventures, Matt Salzberg, Zach Klein and others.

Waxman’s past startups include dating app Grouper, while his wife/co-founder Tory Waxman is a veterinarian (and serves as the startup’s chief veterinary officer). He told me that the two of them became interested in pet food a couple years ago when one of their dogs started to have stomach issues, and they “went down this rabbit hole of trying to find the best dog food.”

The market can be divided two broad categories, Waxman said. There’s kibble, which is relatively cheap and affordable but not as healthy. Then there’s refrigerated food, including direct-to-consumer options like The Farmer’s Dog, which are healthier but also pricier and require more preparation.

“Those are so unbelievably inconvenient,” Waxman argued. “You’re not going to find too many people crazier about their dogs than we are, and we would do literally anything for our dogs — except prepare their food for an hour a day.”

Image Credits: Sundays

So he’s pitching Sundays as a “new, third category of dog food between kibble and refrigerated.” It’s supposed to be human-grade dog food that’s 90% fresh meat, organs and bones, created through a unique air drying process.

For dog owners who rely on kibble, Waxman said the startup offers “a much higher-quality product that tastes much better and doesn’t compromise on the convenience that you’re used to,” while for owners who currently pay for refrigerated options, he promised “an all-around unbelievable increase in convenience, without any compromise in quality and taste.”

Several early customers compared the food to beef jerky in their reviews. Waxman added that in taste tests, dogs preferred Sundays to premium kibble 40-to-0.

The food is available for both one-time and subscription purchase. A single 40-ounce box currently costs $75, while the same box costs $59 via subscription.

Waxman suggested that it hasn’t been easy getting to this point — with a new process for creating dog food, “there were no supply chains set up for this.” Ultimately, he said Sundays selected a “USDA-monitored jerky kitchen in the U.S. to create this new form factor.”

“It took us much longer than we expected,” he admitted. “However, the short-term headache is a long-term feature that we’re really excited about. Ultimately, it should serve as a pretty deep moat to prevent would-be competitors from offering similarly high quality and differentiated products.”

Powered by WPeMatico

SlideShare has a new owner, with LinkedIn selling the presentation-sharing service to Scribd for an undisclosed price.

According to LinkedIn, Scribd will take over operation of the SlideShare business on September 24.

Scribd CEO Trip Adler argued that the two companies have very similar roots, both launching in 2006/2007 with stories on TechCrunch, and both of them focused on content- and document-sharing.

“The two products always had kind of similar missions,” Adler said. “The difference was, [SlideShare] focused on more on PowerPoint presentations and business users, while we focused more on PDFs and Word docs and long-form written content, more on the general consumer.”

Over time, the companies diverged even further, with SlideShare acquired by LinkedIn in 2012, and LinkedIn itself acquired by Microsoft in 2016.

Scribd, meanwhile, launched a Netflix-style subscription service for e-books and audiobooks, but Adler said that both the “user-generated side” and the “premium side” remain important to the business.

“We get people who come in looking for documents, then sign up for our premium content,” he said. “But they do continue to read documents, too.”

So when Microsoft and LinkedIn approached Scribd about acquiring SlideShare, Adler saw an opportunity to expand the document side of the product dramatically, incorporating SlideShare’s content library of 40 million presentations and its audience of 100 million unique monthly visitors.

The deal, Adler said, is fundamentally about tapping into SlideShare’s “content and audience,” though he said there may be aspects of the service’s technology that Scribd could incorporate as well. Scribd isn’t taking on any new employees as part of the deal; instead, its existing team is taking responsibility for SlideShare’s operation.

He added that SlideShare will continue to operate as a standalone service, separate from Scribd, and that he’s hopeful it will continue to be well-integrated with LinkedIn.

“Nothing will change in the initial months,” Adler said. “We have a lot of experience with a product like this, both the technology stack and with users uploading content. We’re in a good position make SlideShare really successful.”

Meanwhile, a statement from LinkedIn Vice President of Engineering Chris Pruett highlighted the work that the company has done on SlideShare since the acquisition:

LinkedIn acquired SlideShare in May 2012 at a time when it was becoming clear that professionals were using LinkedIn for more than making professional connections. Over the last eight years, the SlideShare team, product, and community has helped shape the content experience on LinkedIn. We’ve incorporated the ability to upload, share, and discuss documents on LinkedIn.

Powered by WPeMatico

According to The Wall Street Journal, Airbnb could file confidentially to go public as early as this month. The same report states that Airbnb could follow that filing with an IPO before year’s end. Morgan Stanley and Goldman are helping the former startup with its IPO process, the Journal writes.

The news that Airbnb’s IPO could be back on caps a tumultuous year for the home-sharing unicorn, which promised in 2019 to go public in 2020. The company was widely tipped to be considering a direct listing before COVID-19 arrived, crashing the global travel market, and with it, Airbnb’s financial health.

Airbnb declined to comment on its IPO plans.

As travelers stayed home, the company was forced to sharply cut staff and take on billions in capital at prices that, compared to its late 2019-momentum, looked rather expensive.

But since those blows, Airbnb has begun to make noise about positive progress regarding its platform usage, and, implicitly, its financial performance.

In June, Airbnb said that between “May 17 to June 6, 2020, there were more nights booked for travel to Airbnb listings in the US than during the same time period in 2019,” and that “globally, over the most recent weekend (June 5-7), we saw year-over-year growth in gross booking value” for “the first time since February.”

And in July, the company said that its users had “booked more than 1 million nights’ worth of future stays at Airbnb listings” globally in a single day, the first time since March 3rd that that had happened.

Precisely how far Airbnb has financially clawed its way back is not clear. But the company’s cost basis in the wake of its layoffs could lower the revenue base it needs to recover to reach something akin to profitability, a traditional IPO benchmark, though one that has lost luster in recent years.

And with local travel taking off — slowly-improving airline occupancy rates are, therefore, not indicative of Airbnb’s performance or health — the company could have retooled its business in the wake of COVID to something that can still put up attractive revenues at strong margins.

Needless to say, I am hyped to read the Airbnb S-1, so the sooner it drops the happier I’ll be. Getting an in-depth look at what happened to the unicorn during COVID-19 is going to be fascinating.

Airbnb joins DoorDash, Coinbase, Palantir and others on our IPO shortlist. More as we have it.

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

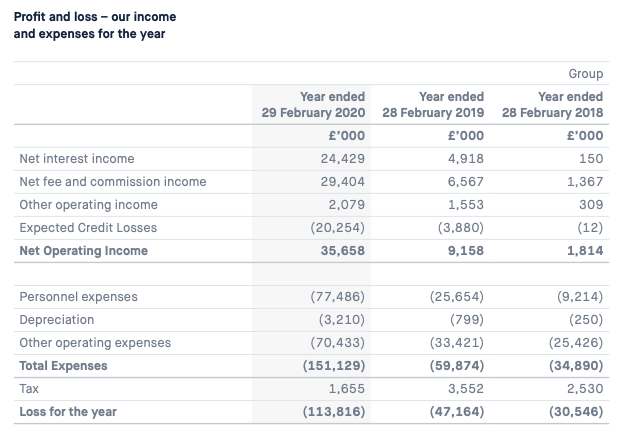

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Mobile device maker HMD Global has announced a $230M Series A2 — its first tranche of external funding since a $100M round back in 2018 when it tipped over into a unicorn valuation. Since late 2016 the startup has exclusively licensed Nokia’s brand for mobile devices, going on to ship some 240M devices to date.

Its latest cash injection is notable both for its size (HMD claims it as the third largest funding round in Europe this year); and the profile of the strategic investors ploughing in capital — namely: Google, Nokia and Qualcomm.

Though whether a tech giant (Google) whose OS dominates the world’s smartphone market (Android) becoming a strategic investor in Europe’s last significant mobile OEM (HMD) catches the attention of regional competition enforcers remains to be seen. Er, vertical integration anyone? (To wit: It’s a little over two years since Google was slapped with a $5BN penalty by EU regulators for antitrust violations related to how it operates Android — and the Commission has said it continues to monitor the market ‘remedies’.)

In a further quirk, when we spoke to HMD Global CEO, Florian Seiche, ahead of today’s announcement, he didn’t expect the names of the investors to be disclosed — but a press spokesperson had already shared them with us so he duly confirmed the trio are investors in the round. (But wouldn’t be drawn on how much equity Google is grabbing.)

HMD’s smartphones run on Google’s Android platform, which gives the tech giant a firm business reason for supporting the mobile maker in growing the availability of Google-packed hardware in key growth markets around the world.

And while HMD likens its consistent (and consistently updated) flavor of Android to the premium ‘pure’ Android experience you get from Google’s own-brand Pixel smartphones, the difference is the Finnish company offers devices across the range of price points, and targets hardware at mobile users in developing markets.

The upshot is relatively little overlap with Google’s Pixel hardware, and still plenty of business upside for Google should HMD grow the pipeline of Google services users (as it makes money by targeting ads).

Connoisseurs of mobile history may see more than a little irony in Google investing into Nokia branded smartphones (via HMD), given Android’s role in fatally disrupting Nokia’s lucrative smartphone business — knocking the Finnish giant off its perch as the world’s number one mobile maker and ushering in an era of Android-fuelled Asian mobile giants. But wait long enough in tech and what goes around oftentimes comes back around.

“We’re extremely excited,” said Seiche, when we mention Google’s pivotal role in Nokia’s historical downfall in smartphones. “How we are going to write that next chapter on smartphones is a critical strategic pillar for the company and our opportunity to team up so closely with Google around this has been a very, very great partnership from the beginning. And then this investment definitely confirms that — also for the future.”

“It’s a critical time for the industry therefore having a clear strategy — having a clear differentiation and a different point of view to offer, we believe, is a fantastic asset that we have developed for ourselves. And now is a great moment for us to double down on this,” he added.

We also asked Seiche whether HMD has any interest in taking advantage of the European Commission’s Android antitrust enforcement decision — i.e. to fork Android and remove the usual Google services, perhaps swapping them out for some European alternatives, which is at least a possibility for OEMs selling in the region — but Seiche told us: “We have looked at it but we strongly believe that consumers or enterprise customers actually love [Google] services and therefore they choose those services for themselves.” (Millions of dollars of direct investment from Google also, presumably, helps make the Google services business case stack up.)

Nokia, meanwhile, has always had a close relationship with HMD — which was established by former Nokia execs for the sole purpose of licensing its iconic mobile brand. (The backstory there is a clause in the sale terms of Nokia’s mobile device division to Microsoft expired in 2016, paving the way for Nokia’s brand to be returned to the smartphone market without the prior Windows Mobile baggage.)

Its investment into HMD now looks like a vote of confidence in how the company has been executing in the fiercely competitive mobile space to date (HMD doesn’t break out a lot of detail about device sales but Seiche told us it sold in excess of 70M mobiles last year; that’s a combined figure for smartphones and feature phones) — as well as an upbeat assessment of the scope of the growth opportunity ahead of it.

On the latter front US-led geopolitical tensions between the West and China do look poised to generate a tail-wind for HMD’s business.

Mobile chipmaker Qualcomm, for example, is facing a loss of business, as US government restrictions threaten its ability to continue selling chips to Huawei; a major Chinese device maker that’s become a key target for US president Trump. Its interest in supporting HMD’s growth, therefore, looks like a way for Qualcomm to hedge against US government disruption aimed at Chinese firms in its mobile device maker portfolio.

While with Trump’s recent threats against the TikTok app it seems safe to assume that no tech company with a Chinese owner is safe.

As a European company, HMD is able to position itself as a safe haven — and Seiche’s sales pitch talks up a focus on security detail and overall quality of experience as key differentiating factors vs the Android hoards.

“We have been very clear and very consistent right from the beginning to pick these core principles that are close to our heart and very closely linked with the Nokia brand itself — and definitely security, quality and trust are key elements,” he told TechCrunch. “This is resonating with our carrier and retail customers around the world and it is definitely also a core fundamental differentiator that those partners that are taking a longer term view clearly see that same opportunity that we see for us going forward.”

HMD does use manufacturing facilities in China, as well as in a number of other locations around the world — including Brazil, India, Indonesia and Vietnam.

But asked whether it sees any supply chain risks related to continued use of Chinese manufacturers to build ‘secure’ mobile hardware, Seiche responded by claiming: “The most important [factor] is we do control the software experience fully.” He pointed specifically to HMD’s acquisition of Valona Labs earlier this year. The Finnish security startup carries out all its software audits. “They basically control our software to make sure we can live up to that trusted standard,” Seiche added.

Landing a major tranche of new funding now — and with geopolitical tension between the West and the Far East shining a spotlight on its value as alternative, European mobile maker — HMD is eyeing expansion in growth markets such as Africa, Brail and India. (Currently, HMD said it’s active in 91 markets across eight regions, with its devices ranged in 250,000 retail outlets around the world.)

It’s also looking to bring 5G to devices at a greater range of price-points, beyond the current flagship Nokia 8.3. Seiche also said it wants to do more on the mobile services side. HMD’s first 5G device, the flagship Nokia 8.3, is due to land in the US and Europe in a matter of weeks. And Seiche suggested a timeframe of the middle of next year for launching a 5G device at a mid tier price point.

“The 5G journey again has started, in terms of market adoption, in China. But now Europe, US are the key next opportunity — not just in the premium tier but also in the mid segment. And to get to that as fast as possible is one of our goals,” he said, noting joint-working with Qualcomm on that.

“We also see great opportunity with Nokia in that 5G transition — because they are also working on a lot of private LTE deployments which is also an interesting area since… we are also very strongly present in that large enterprise segment,” he added.

On mobile services, Seiche highlighted the launch of HMD Connect: A data SIM aimed at travellers — suggesting it could expand into additional connectivity offers in future, forging more partnerships with carriers.

“We have already launched several services that are close to the hardware business — like insurance for your smartphones — but we are also now looking at connectivity as a great area for us,” he said. “The first pilot of that has been our global roaming but we believe there is a play in the future for consumers or enterprise customers to get their connectivity directly with their device. And we’re partnering also with operators to make that happen.”

“You can see us more as a complement [to carriers],” he added, arguing that business “dynamics” for carriers have also changed substantially — and customer acquisition hasn’t been a linear game for some time.

“In a similar way when we talk about Google Pixel vs us — we have a different footprint. And again if you look at carriers where they get their subscribers from today is already today a mix between their own direct channels and their partner channels. And actually why wouldn’t a smartphone player be a natural good partner of choice also for them? So I think you’ll see that as a trend, potentially, evolving in the next couple of years.”

Powered by WPeMatico

Tech stocks retain their highs as the second quarter’s earnings season begins to fade into the rearview mirror, and there are still a number of companies looking to go public while the times are good. It looks like a smart move, as public investors are hungry for growth-oriented shares — which is just what tech and venture-backed companies have in spades.

The companies currently looking to go public are diverse. China-based real-estate giant KE Holdings — a hybrid listings company and digital transaction portal for housing — is looking to raise as much as $2.3 billion in a U.S. listing. Xpeng, another China-based company that builds electric vehicles, is looking to list in the U.S as well. Xpeng has the distinction of being gross-margin negative in every key time period detailed in its S-1 filing.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

And then there’s Duck Creek Technologies, a domestic tech company looking to go public on the back of growing SaaS revenues. This morning let’s quickly spin through Duck Creek’s history, peek at its financial results, calculate its expected valuation and see how its pricing fits compared to current norms.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

Duck Creek is a Boston-based software company that serves the property and casualty (P&C) insurance market. Its customers include names like AIG, Geico and Progressive, along with smaller players that aren’t as well known to the American mass market.

The KE IPO will be a big affair because the company is huge and profitable with $3.86 billion in H1 2020 revenue leading to $227.5 million in net income. The Xpeng IPO will be interesting because Tesla’s strong share price has given float to a great many EV boats. But Duck Creek is a company slowly letting go of perpetual license software sales and scaling its SaaS incomes while still generating nearly half its revenues from services. It’s a company we can understand, in other words.

So let’s get under the skin of the Boston-based company that also claims low-code functionality. This will be fun.

Powered by WPeMatico

This morning, Mux, a startup that provides API-based video streaming tooling and analytics, announced that it has closed a $37 million Series C round of capital.

Andreessen Horowitz led the round, which included participation from Accel and Cobalt. Prior to this funding round, Mux most recently raised a roughly $20 million round in mid-2019. In total, the company had raised a hair under $32 million before its Series C, according to PitchBook data.

The Mux round lands amidst a number of trends that we’re tracking here at TechCrunch, namely API-based startups, which are hot as a group at the moment, and startups that are serving an accelerating digital transformation.

Let’s explore a bit of Mux’s history, and then dig into how the startup’s current pace of revenue growth explains its fresh infusion of capital.

TechCrunch spoke with Mux’s founder Jon Dahl about the round, curious about how the company came to be. Dahl was a co-founder of Zencoder back in the early 2010s, which sold to Brightcove. When Zencoder launched, TechCrunch said that it wanted “to be the Amazon Web Services of video encoding.” It wound up selling for $30 million, a figure that stood a bit taller in 2012, when the transaction was announced.

Dahl stuck around Brightcove for a few years while angel investing. Then in late 2015 he founded Mux. The new startup first built an analytics tool called Mux Data. Dahl said the analytics product was needed because more conventional tooling like Google Analytics don’t work well with online video.

Mux Data is a SaaS product. But what made Mux even more interesting is its on-demand infra play, namely Mux Video.

Mux Video is delivered via an API, supporting both live and on-demand video for other companies. The startup likes to argue that it’s doing for video what Stripe has done for payments, namely take a bundle of complexity and headache, wrestle it into shape, then offer it via a developer-friendly hook.

Delivering video, we’ve seen via the bootstrapped growth of Cloudinary and recent Daily.co round, is growing work in 2020.

That fact shows up in Mux’s numbers, which are somewhat bonkers. The company’s aggregate revenue numbers are growing at a pace that Dahl described as 4x, while Mux Video’s revenues are growing at a pace of 8x, he said. Dahl shared a few other metrics — startups: if you want folks to care about your funding round, follow this example — including that Mux Video’s LTV/CAC ratio is somewhere around 5x-6x, and that its net retention is around 160%.

The collected performance data that Mux shared explain why a16z wanted to put its capital into the company.

But to better understand that all the same, I caught up with Kristina Shen, a general partner at the venture firm. Shen stressed that Mux was heading in the right direction before the pandemic, but that COVID has accelerated the importance of video in how humans interact with one another — an accelerating secular shift for Mux to surf, in other words.

COVID has bolstered Mux, with a release regarding its new investment, noting that its “social media customers [have seen] an increase of 118% in video streaming since mid-February while fitness and health streaming surged by 162%, e-learning grew by 230% and religious streams jumped nearly 3 orders of magnitude.”

Shen said during our call that Mux is one of the fastest-growing enterprise SaaS companies that her firm has seen.

Finally, when asked about Mux’s gross margins, Shen said the company would eventually look similarly to other companies in the infra space, like Twilio and Stripe. This matches what Dahl told this publication, though the founder included a fun wrinkle. Remember Mux Data, the analytics product? Its margins more closely resembles SaaS economics, while Mux Video is more similar to other API, infra plays. So Mux has a bit of SaaS and a bit of infra in it, which should give it a super interesting blended gross margin profile.

Fun. The next time we talk to the firm we’ll be curious to see how far into the double-digit millions it can stretch its run rate.

Powered by WPeMatico

Entrepreneurial creators have to do a lot with limited time. They need to, well, create, but then they also need to build their marketing funnels, convert users to their paid products and manage business operations. Yet, perhaps the most important task they face is keeping their existing fans engaged, because ultimately, that engagement ties directly to the health of their brand long-term.

Social tools are abysmal on platforms like YouTube and Instagram, particularly when it comes to creators owning their own communities and building deeper relationships with them. Other products like Discord have been used to some success, although Discord was built with a different focus in mind and is being hammered in to fix the problem.

Circle believes there is a better way. The New York City-based startup officially launched today for creators (following eight months of product beta testing). The platform is designed from the bottom-up to offer better community building and engagement tools for creators, while also integrating with other software typical in the creator toolkit.

Circle co-founders Sid Yadav, Rudy Santino and Andrew Guttormsen. Photo via Circle.

The key DNA for the company is another NYC-based startup called Teachable. Two of Circle’s three founders, Sid Yadav and Andrew Guttormsen, hail from the edtech platform, which helps entrepreneurial teachers setup online storefronts for their classes. Teachable was sold to Hotmart earlier this year for what was reported to be a quarter of a billion dollars. Yadav was VP of Product there, and Guttormsen was VP of Growth and Marketing. Their third co-founder, Rudy Santino, knew Yadav from previous work.

Yadav spun out of Teachable and actually got his start as a contractor for Sahil Lavingia, the founder of Gumroad we were just talking about last week because he launched a new seed fund. He worked part-time as a product and design consultant, allowing him the flexibility to begin spending time thinking about new product ideas.

“I always knew that my next startup was going to be in [the creator] space,” Yadav said. “I just loved what they’re all about, which is about making an income from what they love doing.”

Teachable’s rapid growth in a small slice of the creator space taught Yadav some of the key challenges that creators face, and what a new product needed to solve in order to help them. With his co-founders, he enlisted a group of creators — including Pat Flynn at Smart Passive Income and Anne-Laure Le Cunff, who operates a newsletter called Ness Labs — to actively build communities on Circle to prove out their various design and product decisions.

The growth of the platform and the engagement of potential customers attracted the attention of Notation Capital, a NYC-based pre-seed fund that just announced its third fund late last month. Notation led a $1.5 million seed round into Circle, which also included Lavingia, Ankur Nagpal (the founder and CEO of Teachable), Dave Ambrose and Matthew Ziskie, among others.

There is a growing movement of software designed to help creators start their businesses. Substack of course has gotten the most attention in Silicon Valley, with a platform designed mostly around email newsletter subscriptions. Pico, meanwhile, has focused on building out more of the infrastructure of the creator business through a CRM that integrates with most other platforms. Patreon handles more of the payments and revenue engagement of fans.

Circle may end up touching on those areas, but today, wants to be the destination where you send all your creators in between newsletters or blog posts or Instragrams. It’s a smart part of the creator stack to play in, and with strong early customer enthusiasm and a chunk of funding, seems ready to make a mark in this burgeoning market.

Powered by WPeMatico