funding

Auto Added by WPeMatico

Auto Added by WPeMatico

Clear is an early-stage startup with a big ambition. It wants to build a blockchain for high-volume transaction systems like payments between telcos. Today it announced a $13 million Series A investment.

The round was led by Eight Roads with participation from Telefónica Innovation Ventures, Telekom Innovation Pool of Deutsche Telekom, HKT and Singtel Innov8.

That the strategic investors were telcos is not a coincidence. The early use case for Clear’s blockchain transaction network involves moving payments between worldwide telcos, a system that today is highly manual and prone to errors.

Clear co-founder Gal Hochberg says what his company does is to take commercial contracts and turn them into digital representations, often known in digital ledger terms as a smart contract.

“What that lets us do is create a trusted view of the true status of the relationship within the company’s business partners because they’re now looking at the same pricing and usage. They can find any issues in real time, either in commercial information or in service delivery, and they can even actually resolve those inside our platform,” Hochberg explained.

By putting these high-volume, cross-border transactions onto the blockchain with these smart contracts to act as automated enforcer of the terms, it means that instead of waiting until the end of the month to find errors and begin a resolution process, this can be done in real time, reducing time to payment and speeding up conflict resolution.

“We use blockchain technology to create those interactions in ways that it is auditable, cryptographically secure and ensures that both sides are synced and seeing the same information,” Hochberg said.

For starters, the company is working with worldwide telco companies because the number of transactions, and the way they cross borders make this a good test case, but Hochberg says this is only the starting point. They are not in full-blown production yet, but he says they have proven they can process hundreds of millions of billable events.

The money should help the company get into full carrier-grade production some time in the first half of this year, and then begin to expand into other verticals beyond telcos with the help of today’s investment.

Powered by WPeMatico

Fearing weak fundraising options in the wake of the WeWork implosion, late stage startups are tightening their belts. The latest is another Softbank-funded company, joining Zume Pizza (80% of staff laid off), Wag (80%+), Fair (40%), Getaround (25%), Rappi (6%), and Oyo (5%) that have all cut staff to slow their burn rate and reduce their funding needs. Freight forwarding startup Flexport that is laying off 3% of its global staff.

“We’re restructuring some parts of our organization to move faster and with greater clarity and purpose. With that came the difficult decision to part ways with around 50 employees” a Flexport spokesperson tells TechCrunch after we asked today if it had seen layoffs like its peers.

Flexport CEO Ryan Petersen

Flexport had raised a $1 billion Series D led by SoftBank at a $3.2 billion valuation a year ago, bringing it to $1.3 billion in funding. The company helps move shipping containers full of goods between manufacturers and retailers using digital tools unlike its old-school competitors.

“We underinvested in areas that help us serve clients efficiently, and we over-invested in scaling our existing process, when we actually needed to be agile and adaptable to best serve our clients, especially in a year of unprecedented volatility in global trade” the spokesperson explained.

Flexport still had a record year, working with 10,000 clients to finance and transport goods. The shipping industry is so huge that it’s still only the seventh largest freight forwarder on its top Trans-Pacific Eastbound leg. The massive headroom for growth plus its use of software to coordinate supply chains and optimize routing is what attracted SoftBank.

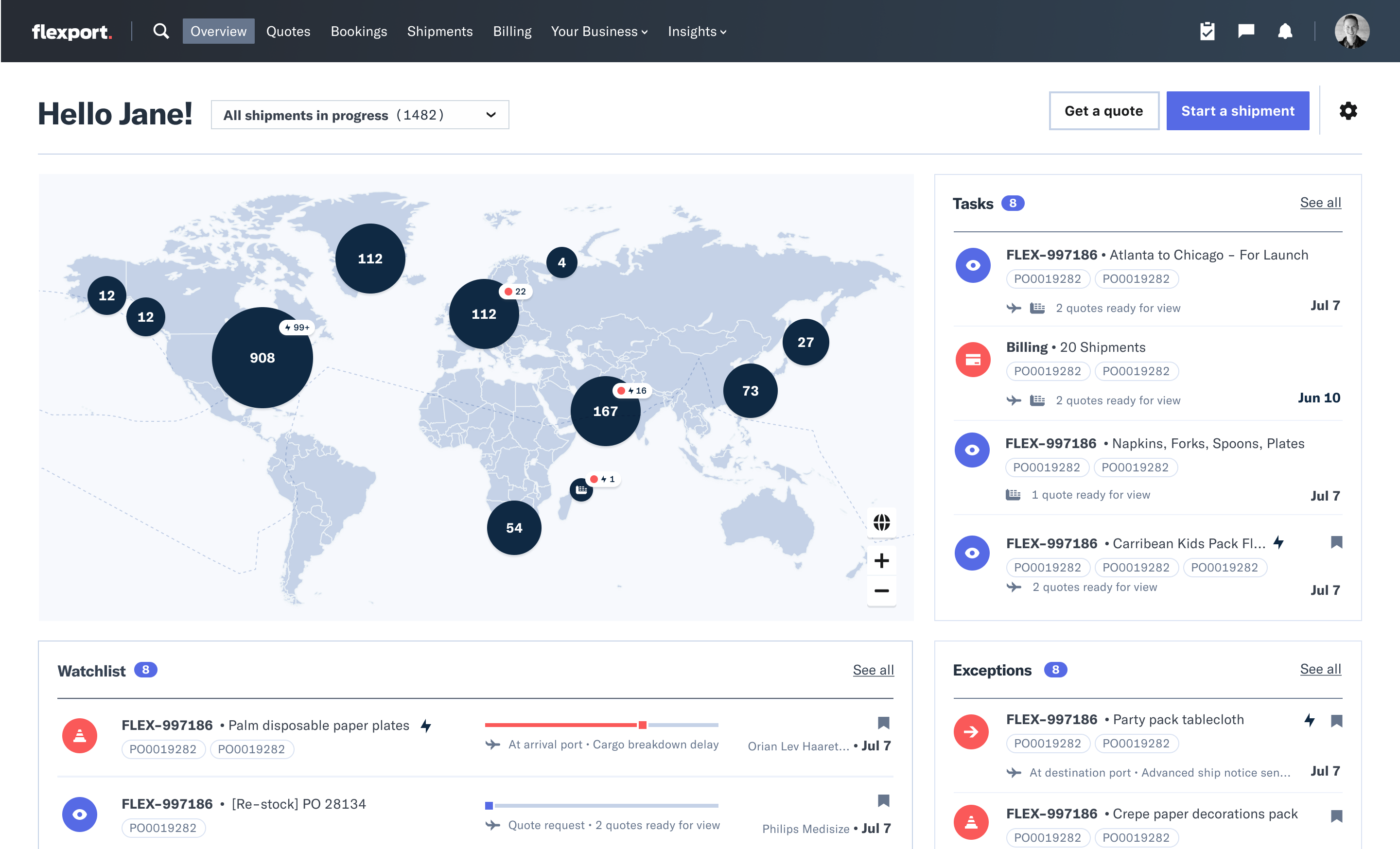

The Flexboard Platform dashboard offers maps, notifications, task lists, and chat for Flexport clients and their factory suppliers.

But many late-stage startups are worried about where they’ll get their next round after taking huge sums of cash from SoftBank at tall valuations. As of November, SoftBank had only managed to raise about $2 billion for its Vision Fund 2 despite plans for a total of $108 billion, Bloomberg reported. LPs were partially spooked by SoftBank’s reckless investment in WeWork. Further layoffs at its portfolio companies could further stoke concerns about entrusting it with more cash.

Unless growth stage startups can cobble together enough institutional investors to build big rounds, or other huge capital sources like sovereign wealth funds materialize for them, they might not be able to raise enough to keep rapidly burning. Those that can’t reach profitability or find an exit may face down-rounds that can come with onerous terms, trigger talent exodus death spirals, or just not provide enough money.

Flexport has managed to escape with just 3% layoffs for now. Being proactive about cuts to reach sustainability may be smarter than gambling that one’s business or the funding climate with suddenly improve. But while other SoftBank startups had to spend tons to edge out direct competitors or make up for weak on-demand service margins, Flexport at least has a tried and true business where incumbents have been asleep at the wheel.

Powered by WPeMatico

Factories and warehouses have been two of the biggest markets for robots in the last several years, with machines taking on mundane, if limited, processes to speed up work and free up humans to do other, more complex tasks. Now, a startup out of Poland that is widening the scope of what those robots can do is announcing funding, a sign not just of how robotic technology has been evolving, but of the growing demand for more automation, specifically in the world of logistics and fulfilment.

Nomagic, which has developed way for a robotic arm to identify an item from an unordered selection, pick it up and then pack it into a box, is today announcing that it has raised $8.6 million in funding, one of the largest-ever seed rounds for a Polish startup. Co-led by Khosla Ventures and Hoxton Ventures, the round also included participation from DN Capital, Capnamic Ventures and Manta Ray, all previous backers of Nomagic.

There are a number of robotic arms on the market today that can be programmed to pick up and deposit items from Point A to Point B. But we are only starting to see a new wave of companies focus on bringing these to fulfilment environments because of the limitations of those arms: they can only work when the items are already “ordered” in a predictable way, such as on an assembly line, which has mean that fulfilment of, for example, online orders is usually carried out by humans.

There are a number of robotic arms on the market today that can be programmed to pick up and deposit items from Point A to Point B. But we are only starting to see a new wave of companies focus on bringing these to fulfilment environments because of the limitations of those arms: they can only work when the items are already “ordered” in a predictable way, such as on an assembly line, which has mean that fulfilment of, for example, online orders is usually carried out by humans.

Nomagic has incorporated a new degree of computer vision, machine learning and other AI-based technologies to elevate the capabilities of those robotic arm. Robots powered by its tech can successfully select items from an “unstructured” group of objects — that is, not an assembly line, but potentially another box — before picking it up and placing it elsewhere.

Kacper Nowicki, the ex-Googler CEO of Nomagic who co-founded the company with Marek Cygan (an academic) and Tristan d’Orgeval (formerly of Climate Corporation), noted that while there has been some work on the problem of unstructured objects and industrial robots — in the US, there are some live implementations taking shape, with one, Covariant, recently exiting stealth mode — it has been mostly a “missing piece” in terms of the innovation that has been done to make logistics and fulfilment more efficient.

That is to say, there has been little in the way of bigger commercial roll outs of the technology, creating an opportunity in what is a huge market: fulfilment services are projected to be a $56 billion market by 2021 (currently the US is the biggest single region, estimated at between $13.5 billion and $15.5 billion).

“If every product were a tablet or phone, you could automate a regular robotic arm to pick and pack,” Nowicki said. “But if you have something else, say something in plastic, or a really huge diversity of products, then that is where the problems come in.”

Nowicki was a longtime Googler who moved from Silicon Valley back to Poland to build the company’s first engineering team in the country. In his years at Google, Nowicki worked in areas including Google Cloud and search, but also saw the AI developments underway at Google’s DeepMind subsidiary, and decided he wanted to tackle a new problem for his next challenge.

His interest underscores what has been something of a fork in artificial intelligence in recent years. While some of the earliest implementations of the principles of AI were indeed on robots, these days a lot of robotic hardware seems clunky and even outmoded, while much more of the focus of AI has shifted to software and “non-physical” systems aimed at replicating and improving upon human thought. Even the word “robot” is now just as likely to be seen in the phrase “robotic process automation”, which in fact has nothing to do with physical robots, but software.

“A lot of AI applications are not that appealing,” Nowicki simply noted (indeed, while Nowicki didn’t spell it out, DeepMind in particular has faced a lot of controversy over its own work in areas like healthcare). “But improvements in existing robotics systems by applying machine learning and computer vision so that they can operate in unstructured environments caught my attention. There has been so little automation actually in physical systems, and I believe it’s a place where we still will see a lot of change.”

Interestingly, while the company is focusing on hardware, it’s not actually building hardware per se, but is working on software that can run on the most popular robotic arms in the market today to make them “smarter”.

“We believe that most of the intellectual property in in AI is in the software stack, not the hardware,” said Orgeval. “We look at it as a mechatronics problem, but even there, we believe that this is mainly a software problem.”

Having Khosla as a backer is notable given that a very large part of the VC’s prolific investing has been in North America up to now. Nowicki said he had a connection to the firm by way of his time in the Bay Area, where before Google, Vinod Khosla backed a startup of his (which went bust in one of the dot-com downturns).

While there is an opportunity for Nomagic to take its idea global, for now Khosla’s interested because of the a closer opportunity at home, where Nomagic is already working with third-party logistics and fulfilment providers, as well as retailers like Cdiscount, a French Amazon-style, soup-to-nuts online marketplace.

“The Nomagic team has made significant strides since its founding in 2017,” says Sven Strohband, Managing Director of Khosla Ventures, in a statement. “There’s a massive opportunity within the European market for warehouse robotics and automation, and NoMagic is well-positioned to capture some of that market share.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

It was yet another jam-packed week full of big news, IPO happenings and venture activity. As always, we’ve done our best to deliver the gist on what’s been going on. We had Alex Wilhelm and Danny Crichton on hand to handle it all, which went medium-good. In other Equity news, we’re back with guests over the next few weeks, so if you miss us having a venture capitalist along for the ride, fear not, their return is just around the corner.

Up top this week was Jon Shieber’s report that Kleiner Perkins has rapidly deployed its most recent fund, a $600 million vehicle. While the news felt surprising, digging back through our archives we were reminded that the firm had indicated it might put its capital to work quickly. Still, as Danny pointed out, it’s rare that venture capitalists have to go out raising from LPs on an annual basis.

After that, we turned to some funding rounds that held our attention, including the Free Agency round that is working to bring talent management to the technology industry similar to the sports and entertainment worlds.

The concept makes some sense, as compensation packages for top talent in the industry can extend into the seven-figures (Free Agency takes a 5-10% cut of an employee’s income using the increasingly popular income-share agreements). Also, this round felt a bit like a reminder that the labor market is tight at the moment.

We then moved on to Josh Constine’s story about “Ring for enterprise” startup Verkada, which raised a massive $80 million round at a $1.6 billion valuation. That’s eye-popping, since the extremely small dilution implied with those numbers (5%) is very rare in the venture world.

After that we turned to a few rounds that Alex has had his eye on, namely the somewhat-recent Insurify round, the pretty-recent Gabi round and the most-recent Policygenius. All told, they sum to $150 million, which made us ask the question, why are venture capitalists so into insurance marketplace startups?

Finally, we touched on the latest from the intra-SoftBank delivery war between DoorDash and Uber Eats, including who is impacted, and what it means for future consolidation in the on-demand world. Or more precisely, why hasn’t there been more?

Finally, don’t forget that IPO season is upon us. Are you caught up?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

The Bouqs plans to take a slice of Japan’s $6 billion flower market this year with a $30 million strategic growth round from Japanese enterprise business investor Yamasa. While The Bouqs still must compete with bigger contenders like 1-800-Flowers and FTD in the U.S., it will now have to take on incumbents like Ayoma Flower Market and FloraJapan, both of which also offer same-day delivery throughout the land of the rising sun.

So why Japan? According to The Bouqs founder and CEO John Tabis, his company had been looking to expand internationally for awhile and Japan seemed to fit well within that plan.

The Bouqs CEO and founder John Tabis

But as far as bigger competition in any country, Tabis is undeterred, telling TechCrunch there’s plenty of opportunities in the flower delivery business if you know where to look. “There’ve been four or five other startups that tried something similar — some of them no longer exist,” Tabis said. “But the thing that’s worked for us, the first is the way that we’ve sourced is unique and it’s really the foundation of our brand.”

The Bouqs sprung up in a wave of Silicon Valley funded flower delivery startups like BloomThat, Farm Girl and Urban Stems, all promising Pinterest -worthy bouquets at the click of a button. But what set it apart was its farm-direct supply chain, cutting out costs from middlemen and delivering flowers that last longer.

This particular round now puts The Bouqs up top as far as total funding raised among its flower delivery startup peers, bringing in $74 million in total funding to date, with competitor Urban Stems in second place with $27 million in funding, according to Crunchbase.

Tabis also tells TechCrunch the new funds will further the company’s development into brick-and-mortar stores and that it’s jumping into the wedding biz. As anyone who’s ever planned a wedding will tell you, it’s an industry ripe for disruption — with brides and grooms spending about 8% of the budget on the flowers alone.

One other renewed focus for the company will be its subscription business, keeping customers set up with a fresh bunch of flowers once the old bouquet is ready for tossing. “It’s sort of the linchpin of our business that’s grown very nicely…expanding both our revenue and profitability,” Tabis told TechCrunch.

The SVP of Yamasa, Norikazu Sano, also mentioned further expansion into Asia for the company in a company press release, so we could see The Bouqs in more international areas over time, if all goes right in Japan.

“This financing will enable us to fully realize our vision to create a global network of top-quality farms paired with a category-defining local floral brand enabled by proprietary supply chain technology and vertically integrated sourcing capabilities. We’re so excited for this next phase of the business, and all of the opportunities that lie ahead,” Tabis said.

Powered by WPeMatico

I work every day with company founders who are grappling with the challenges of driving business growth while keeping their finances on an even keel. One topic we often discuss is how to take advantage of debt to drive business growth — without it turning into a problem.

In my experience, debt can serve as a valuable piece of a company’s capital structure. The key is to use debt for the right purposes and to understand the implications of doing so. For example, short-term loans (one to two-year terms) are useful for financing receivables and inventory to help manage cash flow. These working capital facilities have attractive interest rates (often in the 5% range) and are well understood by the lending community.

By contrast, mezzanine loans (usually three to five-year terms) are better suited to provide the flexibility and runway needed to prove out certain initiatives prior to securing an equity investment or a liquidity event. These loans tend to have limited covenants, are not secured by specific working capital assets and are junior to the working capital loans. Given their higher-risk profile, they are more expensive than short-term loans, with lenders typically targeting a return of 15% to 20%, split between a current pay interest rate of 10%+ and expected stock appreciation from the receipt of warrant coverage.

Regardless of the type of debt a company takes on, there are certain principles to consider to keep the debt from threatening the success of the business. Should you decide to take on debt, understand the implications and consider the following five rules:

Powered by WPeMatico

At the FAA’s 23rd Annual Commercial Commercial Space Transportation Conference in Washington, DC on Wednesday, a panel dedicated to the topic of trends in VC around space startups touched on public vs. private funding, the right kinds of space companies that should even be considering venture funding, and, perhaps most notably, the big L: Liquidity.

Moderator Tess Hatch, Vice President at Bessemer Venture Partners, addressed the topic in response to an audience question that noted while we’ve heard a lot about how much money will flow into space-related startups from the VC community, we haven’t actually et seen much in the way of liquidity events that prove out the validity of these investments.

“In 2008, a company called Skybox was created and a handful of years later Google acquired the company for $500 million,” Hatch said. “Every venture capitalist’s ears perked up and they thought ‘Hey, that’s pretty good ROI in a short amount of time – maybe the space thing is an investable area’ and then a ton of venture capital investments flooded into space startups, and all of these venture capitalists made one, or maybe two investments in the area. Since then, there have not been many — if any – liquidity events: Perhaps Virgin Galactic going public via the SPAC (special uprose vehicle) on the New York Stock Exchange late last year would be the second. So we’re still waiting; we’re still waiting for those exits, we are still waiting for companies to pave the path for the 400+ startups in the ecosystem to return our investment.”

Hatch added that she’s looking at a number of companies who have the potential to break this somewhat prolonged exit drought in 2020, including five who are either quite mature in terms of their development, naming SpaceX, Rocket Lab, Planet and Spire as all likely candidates to have some kind of liquidity event in 2020, with the mostly likely being an IPO.

Space as an industry was described to me recently as a ‘maturing’ startup market by Space Angels CEO Chad Anderson, by virtue of the distribution of activity in terms of the overall investment rounds in the sector. There is indeed a lot of activity with early stage companies and seed rounds, but the fact remains that there hasn’t been much in the way of exits, and it’s also worth pointing out that corporate VCs haven’t been as acquisitive in space as some of their consumer and enterprise technology counterparts.

The panel touched on a lot more apart from liquidity, which actually only came up towards the end of the discussion, which included panelists Astranis CEO and co-founder John Gedmark; Capella Space CEO and founder Payam Banazadeh and Rocket Lab VP of Global Commercial Launch Services Shane Fleming. Both Gedmark and Banazadeh addressed aspects of the risks and benefits of seeking VC as a space technology company.

“Not every space business is a venture-backable business,” said Banazadeh earlier in the conversation. “But there are a lot of space businesses that are specifically going after raising venture money, and that’s dangerous for everyone – because at the end of the day venture is looking at high risk, high return. The ‘high return’ comes from being able to get substantial amount of revenue in a market that’s big

enough for those revenues to be coming from. But if your idea is to go build, maybe, some very specific part in a satellite, then you have to make the case of why you’ll be able to make those returns for the investors, and in a lot of cases, that’s just not possible.”

Banazadeh also concedes that doing any kind of space technology development is expensive, and the money has to come from somewhere. Gedmark talked about one popular source, government funding and grants, and why that often isn’t as obviously a positive thing for startups as it might seem.

“Small government grants can be great, and obviously a fantastic source of non dilutive capital,” Gedmark said. “But there is a little bit of a trick there, or something to be aware of: I think people are often surprised how much time is spent in the early days of a startup refining the exact idea and the product, and if you’re not certain that you have the that product market fit […] then, the government grant can be extremely dangerous, because they will fund you to do something that is sort of similar to what to what you’re doing, but it really prevents you changing your approach later; you’re going to end up spending time executing on the specific project of the program manager on the government side and you’re executing on what they want.”

VC funds, on the other hand, come with the built-in expectation that you’re going to refine and potentially even change direction altogether, Gedmark says. Depending on the terms of the public funding you’re seeking, that flexibility may not be part of the arrangement, which ultimately could be more important than a bit of equity dilution.

Powered by WPeMatico

Fifty iPads were stolen from Verkada co-founder Hans Robertson’s old company. Only when they checked the security system did they realize the video cameras hadn’t been working for months. He was pissed. “The market lagged behind the progress seen in the consumer space, where someone could buy high-end cameras with cloud-based software to protect their home,” Verkada’s CEO and co-founder Filip Kaliszan tells me of his own attempt to buy enterprise-grade security hardware.

Usually, startups ascend on the backs of fresh technologies and developer platforms. But Kaliszan and Robertson realized that commercial security was so backward that just implementing the established principles of machine vision and the cloud could create a huge company. The plan was to keep data secure yet accessible and train its cameras to take clearer photos when AI detects suspicious situations instead of just grainy video.

At first, few could see the vision through the slow upgrade cycles and basement security rooms common with most potential clients. “The seed and the A were extremely difficult rounds to raise compared to the later rounds because people didn’t believe we could execute what were are proposing,” Kaliszan glumly recalls.

But today Verkada receives a huge vote of confidence. It just raised an $80 million Series C at a stunning $1.6 billion post-money valuation thanks to lead investor Felicis Ventures writing Verkada its biggest check to date. The cash brings Verkada to $139 million in funding to sell dome cameras, fisheye lenses, footage viewing stations and the software to monitor it all from anywhere.

Why sink in so much cash at a valuation triple that of Verkada’s $540 million price tag after its April 2019 Series B? Because Verkada wants to bring two-factor authentication to doors with its new access control system that it’s announcing is now in beta testing ahead of a Spring launch. Instead of just allowing a stealable key fob or badge to open your office entryway, it could ask you to look into a Verkada camera too so it can match your face to your permissions.

“Our mission is to be the essential physical security software layer for every building, and the foundation of a larger enterprise IoT infrastructure,” Kaliszan tells me. By uniting security cameras and door locks in one system, it could keep banks, schools, hospitals, government buildings and businesses safe while offering new insights on how their spaces are used.

The founders’ pedigrees don’t hurt its efforts to sell that future to investors like Next47, Sequoia Capital and Meritech Capital, which joined the round. Robertson co-founded IT startup Meraki and sold it to Cisco for $1.2 billion. Kaliszan and his other co-founders Benjamin Bercovitz and James Ren started CourseRank for education software while at Stanford before selling it to Chegg.

Making a better product than what’s out there isn’t rocket science, though. Many building security systems only let footage be accessed from a control room in the building… which doesn’t help much if everyone’s trying to escape due to emergency or if a manager elsewhere simply wants to take a look. Verkada’s cloud lets the right employees keep watch from mobile, and data is also stored locally on the cameras so they keep recording even if the internet cuts out. “Our competitors stream unencrypted video and it’s on you to protect it. We’re responsible for handling that data,” Kaliszan says.

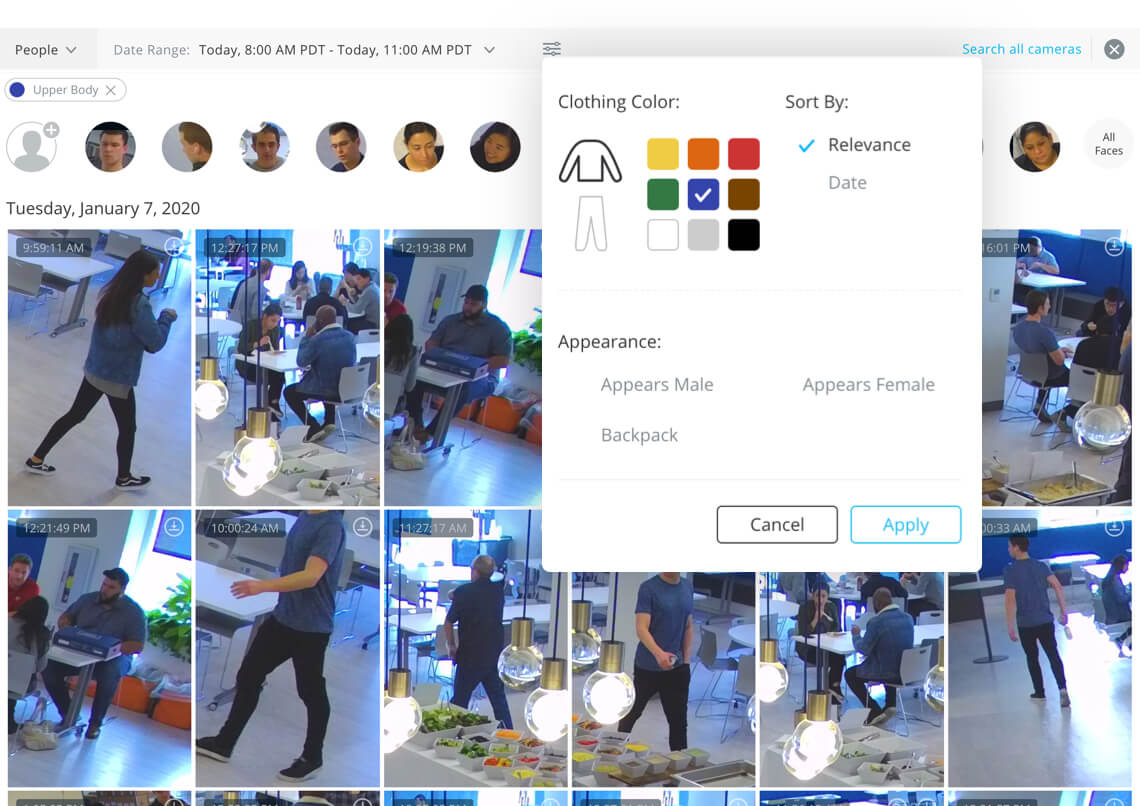

Verkada’s machine vision software can make sense of all the footage its cameras collect. “We can immediately show them all the video containing a particular person of interest rather than manually searching through hours of footage,” Kaliszan insists. “Our platform can use AI/machine learning to recognize patterns and behaviors that are out of the norm in real time.”

For example, a hostage negotiator was able to use Verkada’s system to assess whether a SWAT team needed to invade a building. Verkada can group all spottings of an individual together for review, or scan all the footage for people wearing a certain color or with other search filters.

Indeed, 2,500 clients, including 25 Fortune 500 companies, are already using Verkada. In the last year it has tripled revenue, partnered with 1,100 resellers, launched nine new camera models, added people and vehicle analytics, opened its first London office and is on track to grow from 300 to 800 employees by the end of 2020.

“We call this reinvention,” says Felicis Ventures founder and managing director Aydin Senkut. “One thing people underestimate is how big this market is. Honeywell is valued at $110 billion-plus. There’s a Chinese company that’s over $50 billion. The opportunity to be the operating system for all buildings in the world? Sounds like that market couldn’t be better.” Senkut knows Verkada works because he had it installed in all his homes and offices.

Most enterprise software companies don’t have to worry about the complexities of hardware supply chains. There’s always a risk that its sales process stumbles, leaving it stuck with too many cameras. “We’re still burning money. We’re not there yet or we wouldn’t be raising venture. Because we’re going after a mature market, you can’t come at it with a model that doesn’t make sense. Investors come at it from a hard-nosed approach,” Robertson admits.

“People have a tendency to write off Verkada as a boring camera company. They don’t realize how access control as the second product is going to supercharge the company’s potential,” Senkut declares.

One bullet Verkada dodged is the one firmly lodged in Amazon’s chest. Ring security cameras have received stern criticism over Amazon’s cooperation with law enforcement that some see as a violation of privacy and expansion of a police state. “We don’t have any arrangements with law enforcement like Ring,” Kaliszan tells me. “We view ourselves as providing great physical security tools to the people that run schools, hospitals and businesses. The data that those organizations gather is their own.”

Powered by WPeMatico

Early Stage SF is around the corner, on April 28 in San Francisco, and we are more than excited for this brand new event. The intimate gathering of founders, VCs, operators and tech industry experts is all about giving founders the tools they need to find success, no matter the challenge ahead of them.

Struggling to understand the legal aspects of running a company, like negotiating cap tables or hiring international talent? We’ve got breakout sessions for that. Wondering how to go about fundraising, from getting your first yes to identifying the right investors to planning the timeline for your fundraise sprint? We’ve got breakout sessions for that. Growth marketing? PR/Media? Building a tech stack? Recruiting?

We. Got. You.

Today, we’re very proud to announce one of our few Main Stage sessions that will be open to all attendees. Reid Hoffman and Sarah Guo will join us for a conversation around “How To Raise Your Series A.”

Reid Hoffman is a legendary entrepreneur and investor in Silicon Valley. He was an Executive VP and founding board member at PayPal before going on to co-found LinkedIn in 2003. He led the company to profitability as CEO before joining Greylock in 2009. He serves on the boards of Airbnb, Apollo Fusion, Aurora, Coda, Convoy, Entrepreneur First, Microsoft, Nauto and Xapo, among others. He’s also an accomplished author, with books like “Blitzscaling,” “The Startup of You” and “The Alliance.”

Sarah Guo has a wealth of experience in the tech world. She started her career in high school at a tech firm founded by her parents, called Casa Systems. She then joined Goldman Sachs, where she invested in growth-stage tech startups such as Zynga and Dropbox, and advised both pre-IPO companies (Workday) and publicly traded firms (Zynga, Netflix and Nvidia). She joined Greylock Partners in 2013 and led the firm’s investment in Cleo, Demisto, Sqreen and Utmost. She has a particular focus on B2B applications, as well as infrastructure, cybersecurity, collaboration tools, AI and healthcare.

The format for Hoffman and Guo’s Main Stage chat will be familiar to folks who have followed the investors. It will be an updated, in-person combination of Hoffman’s famously annotated LinkedIn Series B pitch deck that led to Greylock’s investment, and Sarah Guo’s in-depth breakdown of what she looks for in a pitch.

They’ll lay out a number of universally applicable lessons that folks seeking Series A funding can learn from, tackling each from their own unique perspectives. Hoffman has years of experience in consumer-focused companies, with a special expertise in network effects. Guo is one of the top minds when it comes to investment in enterprise software.

We’re absolutely thrilled about this conversation, and to be honest, the entire Early Stage agenda.

Here’s how it all works:

There will be about 50+ breakout sessions at the event, and attendees will have an opportunity to attend at least seven. The sessions will cover all the core topics confronting early-stage founders — up through Series A — as they build a company, from raising capital to building a team to growth. Each breakout session will be led by notables in the startup world.

Don’t worry about missing a breakout session, because transcripts from each will be available to show attendees. And most of the folks leading the breakout sessions have agreed to hang at the show for at least half the day and participate in CrunchMatch, TechCrunch’s app to connect founders and investors based on shared interests.

Here’s the fine print. Each of the 50+ breakout sessions is limited to around 100 attendees. We expect a lot more attendees, of course, so signups for each session are on a first-come, first-serve basis. Buy your ticket today and you can sign up for the breakouts that we’ve announced. Pass holders will also receive 24-hour advance notice before we announce the next batch. (And yes, you can “drop” a breakout session in favor of a new one, in the event there is a schedule conflict.)

Grab yourself a ticket and start registering for sessions right here. Interested sponsors can hit up the team here.

Powered by WPeMatico

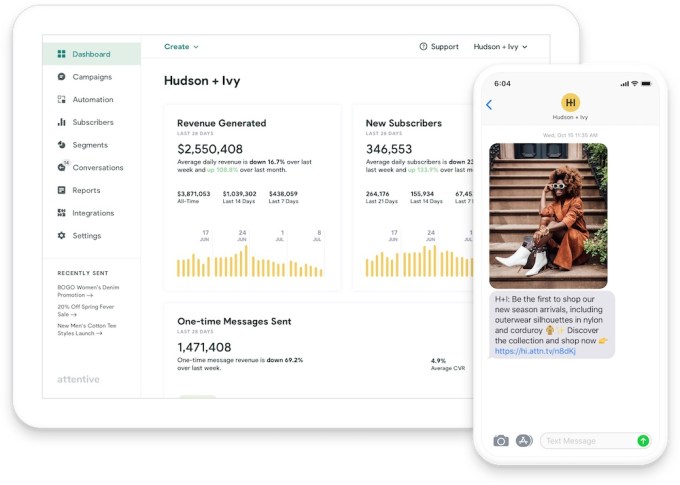

Less than six months after it announced $40 million in funding, Attentive has raised another $70 million — this time in Series C funding.

The new round was led by Sequoia and IVP, two firms that were part of the Series B. Previous investors Eniac Ventures and NextView Ventures also participated.

CEO Brian Long (who, along with his Attentive co-founder Andrew Jones, sold his previous startup TapCommerce to Twitter) told me that he wasn’t planning to raise money again so soon, but things were going even better than expected, with a client list that has grown to more than 750 businesses, including Coach, Urban Outfitters, CB2, PacSun, Party City and Jack in the Box.

Long noted that it’s always smarter to raise money when things are going swimmingly, rather than dealing with the “not-so-fun process” of trying to raise “when you really need it.”

He added, “When you see that you’re doing that well, you think, ‘Hey, we should hire a lot more people to support this growth.’ And then the other piece is just being able to move faster into new areas.”

Long attributed the success Attentive has had thus far to the growing importance of text messages as a channel for businesses to reach consumers, particularly as those consumers are less inclined to open marketing emails or download retailers’ mobile apps. And in contrast to broader messaging platforms, Long said Attentive is “focused on just doing this channel right.”

He said the platform is designed to solve the main problems faced by retailers trying to build a mobile messaging strategy — first, by helping them create a text subscriber list in a way that complies with regulations, then by offering “the ability to send messages that frankly aren’t going to piss people off.”

“We want the messages to be relevant for the consumer, we want to send them things that they care about,” Long said. “The package is on the way, real-time customer service, a product that you were looking at recently is on-sale … there’s a lot of data that you can put to work in order to do it at scale.”

Looking ahead, he hopes to expand beyond the United States and Canada, and to move into industries beyond e-commerce — for example, into more traditional retail, and also to start working with colleges that are looking to attract more applicants.

“Attentive’s growth is a clear indication that people want to interact with brands in new ways, and brands are embracing messaging as an effective way to reach consumers,” said Sequoia partner Pat Grady in a statement. “We are thrilled to double down on our partnership with Attentive so they can continue to deliver fantastic results for their customers and valuable experiences for consumers.”

Attentive has now raised a total of $124 million.

Powered by WPeMatico