credit card

Auto Added by WPeMatico

Auto Added by WPeMatico

Paystone, a payments and integrated software company, secured another strategic investment this year, this time $23.8 million ($30 million CAD) from Crédit Mutuel Equity, the private equity arm of Crédit Mutuel Alliance Fédérale.

The Canada-based company got its start in 2008 as the payment processing company Zomaron, and rebranded itself as Paystone in 2019. Today it provides electronic payments and customer engagement technology to businesses, particularly those that provide services, CEO Tarique Al-Ansari told TechCrunch.

“Paystone is on a mission to help businesses grow, and we were enthralled by their commitment to that mission and their focus on service-oriented verticals,” said Léa Perge, investor at Crédit Mutuel Equity in Canada, via email.

While most of the company’s peers focus on product companies, Al-Ansari saw how underserved the service side was: their needs are different, and unlike retail, aren’t looking to sell online. Rather, they need an online presence and digital marketing to engage with customers, but their focus is being findable and having content that tells people why they should do business with them.

Paystone provides the marketing through content, help with reviews and with loyalty and rewards programs. However, rather than reward for spending, Paystone rewards for behavior. Refer a friend, get a reward. Write a review, get a reward. Al-Ansari calls it “payments as a benefit.” Referrals and reviews are how businesses become more findable, and the more content that’s out there, the more it helps people consider the business trustworthy, he added.

The new funding gives Canada-based Paystone total funds raised in 2021 of $78.8 million in a mix of debt and equity. It raised $54.9 million in January, funds that were barely touched as of yet, Al-Ansari said.

Though he wasn’t actively seeking new funds, Al-Ansari had been speaking with Crédit Mutuel Equity, which used to be CIC Capital Canada, prior to the pandemic, and their deal was put on hold.

Crédit Mutuel Equity came back with similar interest, and taking into account the kind of talent Paystone wanted to go after and its acquisition strategy — the company has already acquired five companies — Al-Ansari decided to take the additional funds. He said it gives the company options to hire more and double down on building the company, as well as enough capital to look for more acquisitions.

This year, Paystone entered the U.S. market for the first time and will do a proper launch later this year. The company has over 30,000 merchant locations on its platform throughout North America, and Al-Ansari expects that to grow by 5,000 this year. The company has 150 employees currently, and another 50 are expected to come on board by the end of the year.

In addition, Al-Ansari expects growth to accelerate for the rest of the year. The company processes around $6 billion in credit card payments and is on track to bring in $55.7 million in revenue this year. It is cash flow positive, residuals from the company’s origins of being bootstrapped, he said.

“We want to become the go-to destination for service businesses to set up a digital presence to accept payments and provide loyalty and rewards,” Al-Ansari said. “We will do this by solidifying our market position and growing our platform with the tools that customers want.”

Powered by WPeMatico

Brazil is a country riven with economic contradictions. It has one of the largest and most profitable banking industries in Latin America, and is among the world’s most developed financial markets. Financial transactions that would take days to process in the United States through ACH happen instantaneously in Brazil. This sophistication, however, masks a backward state of affairs plagued by appalling customer service, exorbitant fees and lack of banking access for many.

The country’s financial system is volatile and often leaves its citizens with few or no alternatives. According to an HBS case study, “in December 2018 the interest rate in Brazil for corporate loans was 52.3%, for consumer loans it was 120.0% and for credit card indebtedness it was 272.42%.” Those rates are many multiples higher compared to figures in neighboring countries.

Brazil’s banking system is a massive market, and one ill-served by incumbents. If someone could thread the needle of product development, strategy and political horse trading required to build a bank in a country where it is nearly impossible for foreigners to own or invest in a bank, it would be one of the great startup and economic success stories of this century.

Nubank is on its way to realizing that objective. Its story is one of unmitigated success, even by the standards of our EC-1 series on high-flying companies and their hard-learned lessons. Just last week, this Brazilian credit card and banking fintech raised a $750 million round led by Berkshire Hathaway at a $30 billion valuation, becoming one of the most valuable startups in the world. It has 40 million users across Brazil, as well as Mexico and Colombia.

Yet, it’s a startup with a CEO and co-founder who isn’t Brazilian, didn’t speak the local language of Portuguese, hadn’t started a company before, and didn’t really know a lot about banking to begin with. This is a story of how raw execution, a “faster, faster” mentality and a fanaticism for making customer experience as enjoyable as a trip to Disney World can completely change the history of an industry — and country — forever.

Our lead writer for this EC-1 is Marcella McCarthy. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions. The lead editor for this package was Danny Crichton, the assistant editor was Ram Iyer, the copy editor was Richard Dal Porto, and illustrations were drawn by Nigel Sussman.

Nubank had no say in the content of this analysis and did not get advance access to it. McCarthy has no financial ties to Nubank or other conflicts of interest to disclose.

The Nubank EC-1 comprises four main articles numbering 9,200 words and a reading time of 37 minutes. Here’s what’s in the bank:

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico

For most startups, the hardest early challenge is identifying a market and a product to serve it. That wasn’t the case for Nubank CEO David Velez, who understood the massive potential for success if he could break into Latin America’s most valuable economy with even a moderately modern banking offering.

Instead, the challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

Nubank knew its market and geography, and through tenacious fundraising, inventive marketing and product development, and a series of contrarian hires, Velez and his team stripped bare the morass of Brazilian banking to build one of the world’s great fintech companies.

The challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

In the first part of this EC-1, I’ll look at how Velez brought his skills and experience to bear on this market, how Nubank was founded in 2013, and how the team brought a Californian rather than Brazilian vibe to their first office on — no joke — California Street, in a neighborhood called Brooklin in the city of São Paulo.

The idea of being his own boss was ingrained in Velez from his earliest days in Colombia, where he grew up in an entrepreneurial family, with a father who owned a button factory. “I heard from my dad over and over again that you need to start your own company,” Velez said.

But years would pass and Velez still had no idea what he wanted to do. To “kill time,” and also to surround himself with entrepreneurial energy, Velez attended Stanford University — partially financed by the sale of some livestock — and then worked as an analyst at Goldman Sachs and Morgan Stanley before switching to venture capital at General Atlantic and Sequoia.

Powered by WPeMatico

As we mentioned in part 1 of this EC-1, David Velez had two key co-founding roles he needed to fill to get started building Nubank. For one, he needed a CTO to lead the engineering side of the business, as Velez didn’t have an engineering background.

Edward Wible, an American computer science graduate who spent most of his career in private equity, would take that responsibility. He didn’t bring years of coding experience, but he had qualities that Velez considered more important: A strong belief in the potential of the product and an equally intense commitment to working on it.

Given the occasionally hostile reaction of most incumbent banks to their customers in Brazil, Nubank’s starkly contrasting openness and transparency has garnered a huge following.

That left an even more important role to fill — one that was much harder to define. This other co-founder would need to blend knowledge of the Brazilian market and local savvy with expertise in banking, all while embodying a Silicon Valley ethos of focusing on customers. This person would also have to work in São Paulo for minimal wages out of a small office with just one bathroom, all in the belief that their equity (both stock and sweat) would one day be worth it.

Velez would eventually stumble upon Cristina Junqueira, who was qualified to do all this, and much, much more.

“Once someone said I was the glue of the operation, and that someone else was the brains. And I said, ‘No, I’m the glue and the brains, and I bet my brain is even better than his,”’ Junqueira said.

Junqueira didn’t just lead Nubank’s drive into the Brazilian market, she also upended age-old notions of what it means to be a 21st-century bank. Her inspiration was nothing short of Disney, and her mission was to create a bank as popular as the magical kingdom itself.

A bank. As popular as Disney. Sounds like a fairy tale, frankly.

Unlike her co-founders Velez and Wible, Junqueira grew up in Nubank’s home market of Brazil. The eldest of four sisters, she remembers her parents — both dentists — always assiduously working to maintain their practice.

Their work ethic trickled down, but so did responsibility. As the oldest at home, she was forced to grow up quickly and take on responsibilities from an early age. “I remember being 11 years old and doing grocery shopping for the month,” she said. “I did everything very young.”

Powered by WPeMatico

As we saw in parts 1 and 2 of this EC-1, by mid-2013, Nubank CEO David Velez had most of what he needed to get started. He’d brought on two co-founders, assembled ambitious engineering and operations teams, raised $2 million in seed funding from Sequoia and Kaszek, rented a tiny office in São Paulo, and was armed with a mission to deliver the kind of banking services that customers in a market as large and lucrative as Brazil’s should expect.

Despite being named Nubank, however, the startup couldn’t actually be a bank: Brazil’s laws made it illegal at the time for a foreigner-run company to operate a bank. That restriction required the team to develop an inventive product strategy to find a foothold in the market while they waited for a license directly from the country’s president.

Nubank was so adamant about differentiating itself from other banks that it chose Barney purple for its brand color and first credit card.

Nubank therefore pursued a credit card as its first offering, but it had to race against a clock counting quickly down to zero. At the time, Brazil didn’t have ownership restrictions on this product segment like it did with banking, but new rules were coming into force in just a few months in May 2014 that would block a company like Nubank from launching.

The company needed to execute rapidly over the next eight months if it wanted to be grandfathered into the existing regulations. The speed of operations was frantic to say the least, and the company would go on to work even faster, ultimately propelling itself into the stratosphere of fintech startups.

It’s easy to assume that the name Nubank refers to “new bank,” but that’s not really what the founders were going for. The word “nu” in Portuguese means “naked,” and Velez and his team wanted the name to reflect their vision: To build a 21st-Century bank without any of the shackles imposed by the traditional banks in Brazil.

The team wanted to offer services to as many people as possible, as there is a huge wealth gap in Brazil, where the minimum wage is around $200 a month.

Launching with just a credit card was both a strategic and practical business decision. Credit cards were widely used in the country, and everyone understood how they worked. Additionally, you could only use credit cards to shop online in Brazil, because debit cards weren’t accepted.

Powered by WPeMatico

Nubank’s first office, on California Street in the Brooklin neighborhood of São Paulo, makes for a great beginning to the company’s story. It wasn’t a Silicon Valley garage, but this tiny, one-bathroom rented house, where 30 people worked insane hours to push out the company’s debut credit card, lends just as well to an image of entrepreneurial spirit and drive.

As Nubank continues to make international waves, more and more VC investors are taking a look at the Brazilian ecosystem and could potentially fund other upstarts in the years to come.

But as Nubank’s story continued, the team eventually had to move out of that early office, and the next several offices, too. Eventually Nubank had to relocate to an eight-story building in São Paulo, which houses a large part of the company’s now 3,000-person team.

The startup reached decacorn status in far less than a decade, and it is growing faster than ever. When I interviewed CEO David Velez back in January to discuss Nubank’s $400 million Series G, he said, “We’ve gone from 12 million customers in 2019 to 34 million solely based on word of mouth.” By September last year, the company was onboarding 41,000 new customers per day.

In the five months since our interview, Nubank has managed to rope in a whopping 6 million customers to reach 40 million. It’s now valued at $30 billion.

Nubank’s present day headquarters in São Paulo, Brazil. Image Credits: NELSON ALMEIDA/AFP / Getty Images

Getting there hasn’t been easy. The company’s three co-founders, Velez, Edward Wible and Cristina Junqueira, had to make key strategic decisions about how to scale themselves to retain the company’s lead in the neobanking market. That lead is getting tougher to sustain every day. Nubank’s proliferating offerings and broader geographical remit has painted a massive target on its back, and a wide number of competitors have cropped up to run on the paths it pioneered.

Like most Disney films, a fairy-tale ending seems in order, but it’ll take a few more rotations of the film wheel to get to the ending.

For the co-founding trio, it became increasingly clear that Nubank’s growing scale demanded critical strategic decisions on how to bring order to the company.

By 2018, the company had thousands of employees, millions of customers, and they still didn’t have a head of HR. Growth until then had been somewhat unstructured. According to Junqueira, waiting so long to hire a head of HR was one of their early mistakes, because it stunted their ability to grow. “[Good] people continue to be our biggest bottleneck,” she says.

Powered by WPeMatico

It looks like everyone and their mother is trying to reinvent the Brazilian banking system. Earlier this year we wrote about Nubank’s $400 million Series G, last month there was the PicPay IPO filing and today, alt.bank, a Brazilian neobank, announced a $5.5 million Series A led by Union Square Ventures (USV).

It’s no secret that the Brazilian banking system has been poised for disruption, considering the sector’s little attention to customer service and exorbitant fee structure that’s left most Brazilians unbanked, and alt.bank is just the latest company trying to take home a piece of the pie.

Following Nubank’s strategy of launching a bank with colors that are very un-bank-like, signaling that they do things differently, alt.bank similarly launched its first financial product in 2019 — a fluorescent-yellow debit card which the locals have endearingly dubbed, “o amarelinho,” meaning, “the little yellow card.”

The company, founded by serial entrepreneur Brad Liebmann, follows the founder’s $480 million exit of Simply Business, which was acquired by U.S. insurance giant Travelers in 2017.

Unlike many fintechs, alt.bank has a strong social mission and pays commissions for referrals that last for the customer’s lifetime.

“Most fintechs just help wealthy people get wealthier, so I thought let’s do something with a social mission,” Liebmann told TechCrunch in an interview.

To drive home the mission, and really target the unbanked, Liebman and his team of 80 employees have designed an app that can be used by the illiterate. Instead of words, users can follow color-coded prompts to complete a transaction. The company also plans to launch credit products soon.

According to the company, close to a million people have downloaded the android app since launch, but Liebman declined to disclose how many active users the company actually has.

Today, the company’s core offerings include the debit card, a prepaid credit card, Pix (similar to Zelle), a savings account and even telemedicine visits via a partnership with Dr. Consulta, a network of healthcare clinics throughout the country. The prepaid credit card is key because online stores in Brazil don’t accept debit card purchases.

In addition to the perk of ongoing commissions, alt.bank has also partnered with three major drugstores, allowing their users to get 5-30% off any item at the stores, including medication.

While the company is based in São Paulo and São Carlos, Liebmann and his family are currently based in London due to regulations around the pandemic.

The investment in alt.bank marks USV’s first investment in South America, solidifying a trend by other major U.S. investors such as Sequoia who only in the last several years have started looking to LatAm for deals.

“The bar was high for our first investment in South America,” said Union Square Ventures partner John Buttrick. “The combination of the alt.bank business model and world-class management team enticed us to expand our geographic focus to help build the leading digital bank targeting the 100 million Brazilians who are currently being neglected by traditional lenders,” he added in a statement.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

First and foremost, Equity was nominated for a Webby for “Best Technology Podcast”! Drop everything and go Vote for Equity! We’d appreciate it. A lot. And even if we lose, well, we’ll keep doing our thing and making each other laugh. (Note: We are in last place, which is, well, something.)

Regardless, the Equity team got together once again this week to not only go over the news of the week, but also to do a little soul searching. You see, some news broke yesterday, so we figured that we had to talk about it in our usual style. So, here’s the rundown:

We are back Monday morning with our weekly kick-off show. Have a great weekend!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

With the increase of digital transacting over the past year, cybercriminals have been having a field day.

In 2020, complaints of suspected internet crime surged by 61%, to 791,790, according to the FBI’s 2020 Internet Crime Report. Those crimes — ranging from personal and corporate data breaches to credit card fraud, phishing and identity theft — cost victims more than $4.2 billion.

For companies like Sift — which aims to predict and prevent fraud online even more quickly than cybercriminals adopt new tactics — that increase in crime also led to an increase in business.

Last year, the San Francisco-based company assessed risk on more than $250 billion in transactions, double from what it did in 2019. The company has over several hundred customers, including Twitter, Airbnb, Twilio, DoorDash, Wayfair and McDonald’s, as well a global data network of 70 billion events per month.

To meet the surge in demand, Sift said today it has raised $50 million in a funding round that values the company at over $1 billion. Insight Partners led the financing, which included participation from Union Square Ventures and Stripes.

While the company would not reveal hard revenue figures, President and CEO Marc Olesen said that business has tripled since he joined the company in June 2018. Sift was founded out of Y Combinator in 2011, and has raised a total of $157 million over its lifetime.

The company’s “Digital Trust & Safety” platform aims to help merchants not only fight all types of internet fraud and abuse, but to also “reduce friction” for legitimate customers. There’s a fine line apparently between looking out for a merchant and upsetting a customer who is legitimately trying to conduct a transaction.

Sift uses machine learning and artificial intelligence to automatically surmise whether an attempted transaction or interaction with a business online is authentic or potentially problematic.

Image Credits: Sift

One of the things the company has discovered is that fraudsters are often not working alone.

“Fraud vectors are no longer siloed. They are highly innovative and often working in concert,” Olesen said. “We’ve uncovered a number of fraud rings.”

Olesen shared a couple of examples of how the company thwarted fraud incidents last year. One recently involved money laundering through donation sites where fraudsters tested stolen debit and credit cards through fake donation sites at guest checkout.

“By making small donations to themselves, they laundered that money and at the same tested the validity of the stolen cards so they could use it on another site with significantly higher purchases,” he said.

In another case, the company uncovered fraudsters using Telegram, a social media site, to make services available, such as food delivery, with stolen credentials.

The data that Sift has accumulated since its inception helps the company “act as the central nervous system for fraud teams.” Sift says that its models become more intelligent with every customer that it integrates.

Insight Partners Managing Director Jeff Lieberman, who is a Sift board member, said his firm initially invested in Sift in 2016 because even at that time, it was clear that online fraud was “rapidly growing.” It was growing not just in dollar amounts, he said, but in the number of methods cybercriminals used to steal from consumers and businesses.

“Sift has a novel approach to fighting fraud that combines massive data sets with machine learning, and it has a track record of proving its value for hundreds of online businesses,” he wrote via email.

When Olesen and the Sift team started the recent process of fundraising, Insight actually approached them before they started talking to outside investors “because both the product and business fundamentals are so strong, and the growth opportunity is massive,” Lieberman added.

“With more businesses heavily investing in online channels, nearly every one of them needs a solution that can intelligently weed out fraud while ensuring a seamless experience for the 99% of transactions or actions that are legitimate,” he wrote.

The company plans to use its new capital primarily to expand its product portfolio and to scale its product, engineering and sales teams.

Sift also recently tapped Eu-Gene Sung — who has worked in financial leadership roles at Integral Ad Science, BSE Global and McCann — to serve as its CFO.

As to whether or not that meant an IPO is in Sift’s future, Olesen said that Sung’s experience of taking companies through a growth phase such as what Sift is experiencing would be valuable. The company is also for the first time looking to potentially do some M&A.

“When we think about expanding our portfolio, it’s really a buy/build partner approach,” Olesen said.

Powered by WPeMatico

There are many reasons why you could have a good or a bad credit score. But if you’re just entering the job market, you may end up with reliable income and a low limit on your credit card. X1 Card wants to solve that by setting limits based on your current and future income instead of your credit score.

The company says some customers can expect limits up to five times higher than what they would get from a traditional credit card. And that limit can move up if you get a promotion at your job, for instance.

“The consumer credit card industry has been almost untouched by tech and has relied on the archaic credit score system. Max [Levchin], David [Sacks] and I have similar scores — that makes no sense!” co-founder Deepak Rao told me. “We reimagined the credit card from the ground up to have smarter limits, intelligent features, modern rewards and a new look.”

Depending on your creditworthiness, you’ll get a variable APR of 12.9 to 19.9% and a balance transfer fee of 2%. There’s no annual subscription fee and X1 Card doesn’t change any late fee or foreign transaction fee.

Behind the scene, X1 Card is built by Thrive, the company that created ThriveCash, a loan platform that lets you get a credit line based on offer letters for an upcoming summer internship or your first full-time job after college.

You can then borrow as much as 25% of your total internship salary or 25% of your first three paychecks if it’s a full-time job. There are some fees, but it can be helpful if you’re signing a new lease and you don’t have any money on your bank account, for instance.

Thrive has raised $10.25 million in funding from PayPal and Affirm founder Max Levchin, former Twitter COO Adam Bain, Craft Ventures general partner David Sacks and others. Read TechCrunch’s Natasha Mascarenhas’ article on ThriveCash if you want to learn more about that product.

Coming back to X1 Card, the card is a stainless steel Visa card that works with Apple Pay and Google Pay. It helps you track your subscriptions in different ways. First, you can cancel your subscription payments from the app. If you’re trying out a new service and they require you to enter your credit card information to start a free trial, you can also generate an auto-expiring virtual credit card.

If you receive a refund, X1 Card sends you a notification. You can also attach receipts to your transaction in the app.

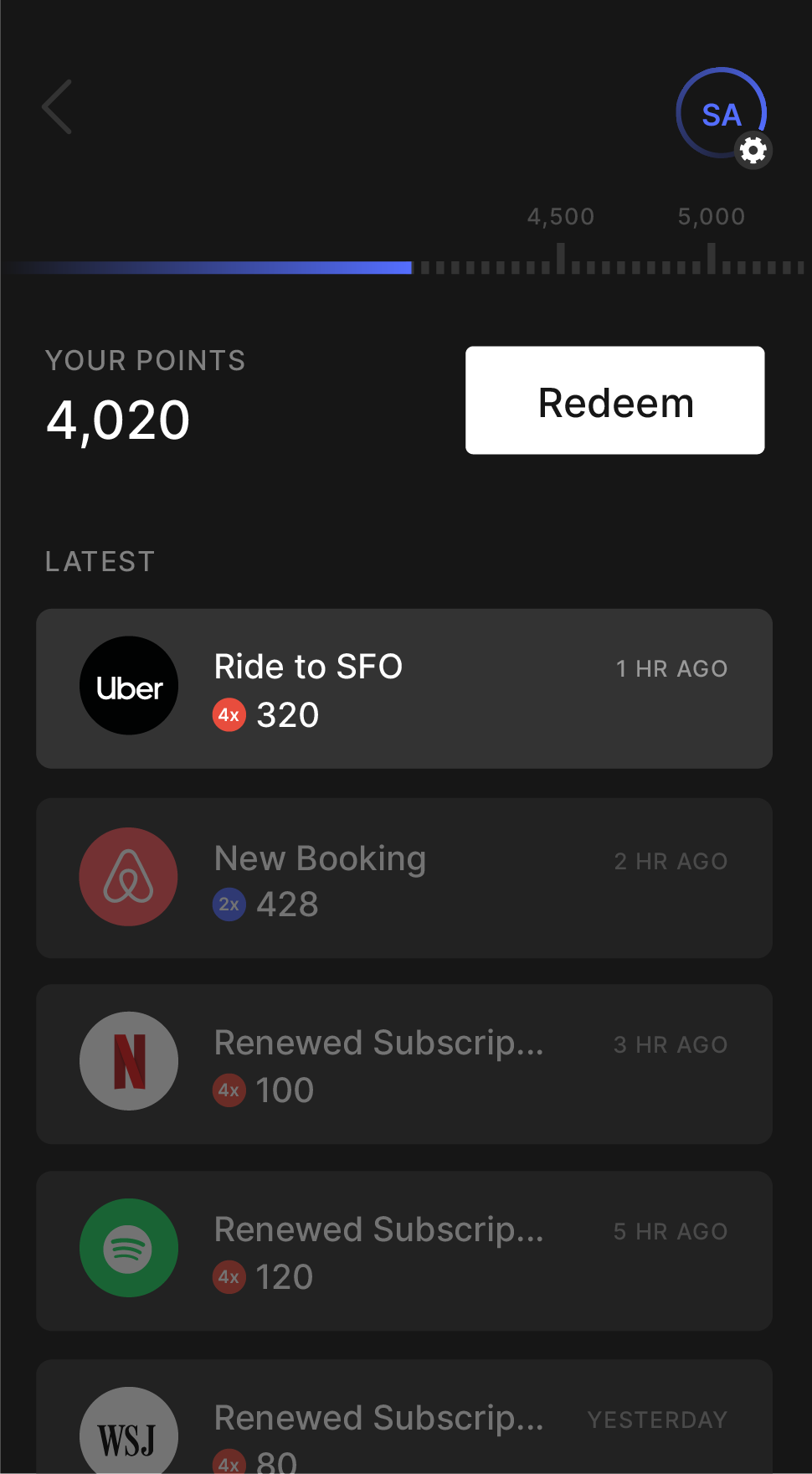

When it comes to rewards, X1 Card uses points. You get 2x points on all purchases by default — there’s no category or retailers that give you special rewards. If you spend more than $15,000 using the card in a year, you get 3X points. If you refer a friend, you get 4X points on your purchases for a month — each new referral adds an extra month with 4X points. Points can be redeemed at retail partners, such as Apple, Airbnb, Delta, Everlane, etc.

In other words, it’s a credit card. But what makes this product more interesting than your average Chase-branded card is that it wants to disrupt the credit score system. It’s going to be interesting to see if people can really get higher limits with that system.

Image credits: X1 Card

Powered by WPeMatico